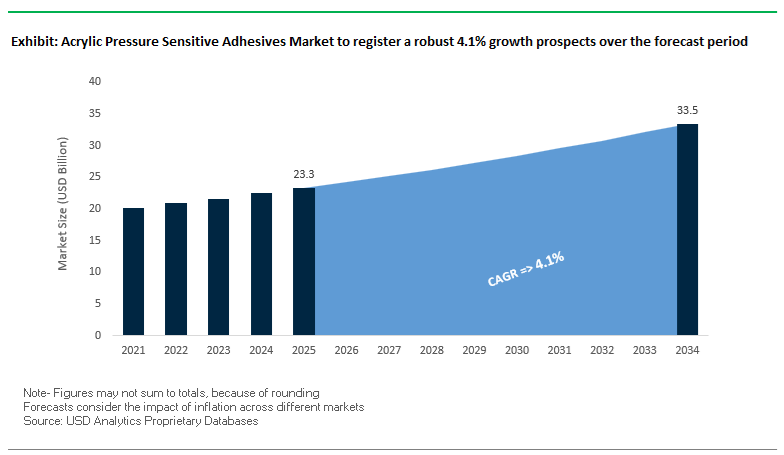

The Global Acrylic Pressure Sensitive Adhesives (PSA) Market is forecast to grow from USD 23.3 billion in 2025 to USD 33.5 billion by 2034, exhibiting a CAGR of 4.1%. The market’s long-term trajectory is shaped by the rising adoption of water-based and low-VOC acrylic PSA formulations, expanding use in automotive, packaging, labeling, and electronics applications, and regulatory policies that accelerate the industry’s transition toward sustainable, solvent-free adhesive technologies. Industry professionals are prioritizing eco-compliance, heat resistance, and substrate versatility, which are redefining performance benchmarks across pressure-sensitive tape and label applications.

In 2026, water-based acrylic PSA technology continues to dominate as industries replace solvent-based systems with environmentally friendly dispersion adhesives. The automotive sector—driven by lightweighting and EV battery assembly requirements—is increasingly dependent on high-strength, temperature-resistant Acrylic PSAs for bonding trim, emblems, insulation, and NVH (Noise, Vibration & Harshness) materials. Furthermore, VOC-compliant products are growing over 21% year-on-year, signaling rapid innovation in polymerization and crosslinking technologies designed to meet stringent global standards such as VDA 278 and ISO 10993 for automotive and medical applications respectively.

The labeling segment remains a cornerstone of demand, reflecting the indispensability of acrylic PSAs in packaging, consumer goods, and industrial labeling. Specialty formulations highlight a global shift toward customized acrylic PSA chemistries optimized for low surface energy substrates, flexible packaging, and wearable medical devices. Over the forecast period, Acrylic PSAs are set to emerge as critical enablers of high-performance, sustainable, and multifunctional adhesive systems.

The Acrylic PSA Market is undergoing a transformation shaped by R&D breakthroughs, capacity expansions, and environmental compliance. In July 2025, the University of Minnesota achieved a significant innovation milestone by developing bio-based monomers that can be grafted onto acrylic acrylates—creating renewable Acrylic PSAs with up to 60% bio-content. This addresses one of the market’s key challenges: balancing sustainability with high shear strength and thermal durability required for industrial and packaging adhesives.

In June 2025, a leading European adhesives producer launched a new series of water-based acrylic PSA dispersions engineered for flexible packaging. The new line offers superior moisture and humidity resistance, directly responding to the packaging sector’s demand for sustainable yet high-performance Acrylic PSAs that meet food-grade and environmental safety standards. Meanwhile, tesa SE (Beiersdorf Group) completed a major production capacity expansion in May 2025, increasing its output of high-temperature, chemical-resistant Acrylic PSAs, a strategic move to serve the surging automotive assembly and EV battery module markets.

The industry is also witnessing increased investment in R&D for next-generation PSAs. Henkel, in March 2025, announced major investments in its North American R&D centers to accelerate the development of UV-curable Acrylic PSAs designed for the electronics and display bonding markets, where clarity and thermal control are critical. Similarly, Dow Inc., through a joint venture in February 2025, introduced a solvent-free hot-melt Acrylic PSA line optimized for building and construction tapes, which eliminates VOC emissions while improving manufacturing efficiency.

In January 2025, a major Asian chemical producer commissioned a new water-based Acrylic PSA facility in Southeast Asia to meet escalating pressure-sensitive label and durable goods demand. Earlier, Avery Dennison Corporation’s November 2024 acquisition of a specialized coating company enabled the integration of thin-film optically clear acrylic PSAs (OCAs) for high-value display technologies, a move that strengthens its foothold in the electronics materials value chain.

Further highlighting the market’s regulatory pivot, the European Union in September 2024 intensified enforcement of volatile monomer restrictions, prompting adhesive manufacturers to accelerate the transition toward low-VOC and waterborne Acrylic PSAs. Complementing this trend, H.B. Fuller’s October 2024 launch of a medical-grade, biocompatible Acrylic PSA underscores the diversification of acrylic adhesive technologies into wearable healthcare devices and wound-care patches.

The global transition from fossil-derived acrylates to bio-based monomers marks one of the most disruptive shifts in the acrylic PSA market. Driven by sustainability commitments from adhesive manufacturers and brand owners, R&D efforts are increasingly focused on developing high-performance bio-acrylic PSAs that meet industrial adhesion requirements while significantly reducing carbon footprints.

Arkema’s €400 million expansion into bio-based polymer capacity in 2023, specifically emphasizing its REAFREE® bio-acrylic platform, demonstrates the pace of the transition. BASF’s biomass-balanced approach, which cuts fossil input in acrylic monomer production by up to 30%, underscores how supply chains are being decarbonized at scale. Complementing the, Dow and LanzaTech’s breakthrough in converting captured carbon emissions into 99.8% pure glacial acrylic acid introduces a circular carbon loop into adhesive manufacturing an industry-first achievement in carbon capture utilization.

Henkel’s sustainability roadmap, targeting 85% recyclable packaging by 2025, is simultaneously catalyzing internal R&D for recyclable adhesive systems using bio-acrylic PSAs. Academic research supports the direction: a 2023 ACS Applied Materials & Interfaces study validated bio-acrylic PSAs achieving over 50 N/inch peel adhesion, equating to conventional petroleum-based products. The convergence of industrial innovation and scientific validation cements bio-based acrylic PSAs as the new frontier in sustainable adhesives.

The concept of debonding-on-demand has emerged as a key technological trend enabling recyclability, reworkability, and material recovery, all essential pillars of a circular economy. By integrating stimuli-responsive polymer networks into acrylic PSAs, manufacturers are designing adhesives that can selectively release bonds upon exposure to heat, light, or chemical triggers, facilitating easy disassembly or recycling.

BASF’s 2023 circular economy pilot with a European packaging consortium achieved over 95% purity in PET label separation using its reversible PSA, directly addressing recycling contamination challenges. Similarly, 3M’s “Reworkable Acrylic Adhesives,” capable of reducing bond strength by over 90% after exposure to 80°C, have become crucial for electronics rework and repair. tesa SE’s “60952” acrylic adhesive tape, engineered for temporary automotive applications with clean removal after a heat trigger, reduces solvent cleaning by 70%, improving process sustainability and reducing VOC emissions.

The innovation push is also supported by national R&D funding, notably, Germany’s BMBF €45 million “Circular Adhesives” initiative, which is pioneering photo-reversible acrylic polymers for future PSA applications.

As global renewable energy infrastructure scales up, particularly in thin-film photovoltaic (PV) manufacturing, acrylic PSAs are emerging as indispensable materials for encapsulation and lamination processes. These applications require adhesives that are optically clear, UV-resistant, and stable under prolonged outdoor exposure areas where acrylic PSAs excel due to their balance of adhesion, clarity, and processability.

Mitsubishi Chemical’s $100 million expansion for high-performance films and adhesives in 2023, specifically targeting thin-film solar encapsulation, exemplifies the strategic alignment of adhesive technology with clean energy growth. NREL’s accelerated weathering tests further validated UV-stable acrylic PSAs that retained over 95% transmittance and 90% adhesive strength after 2,000 hours of testing, ensuring long-term photovoltaic efficiency.

Heliatek’s 2023 adoption of solvent-free, low-temperature curing acrylic PSAs (<70°C processing) for organic photovoltaic lamination underscores the material’s role in sensitive OPV fabrication. The is complemented by the U.S. DOE’s SunShot 2030 initiative, which earmarked $20 million to advance new adhesive materials that lower the balance-of-system costs for solar modules. These advancements highlight how acrylic PSAs are evolving from traditional bonding agents into high-value materials critical to sustainable energy infrastructure, bridging performance, optical quality, and durability in solar technologies.

The emergence of wearable electronics, medical sensors, and flexible consumer devices is creating high-value opportunities for acrylic PSAs engineered with unique combinations of stretchability, biocompatibility, and conductivity. These “smart adhesives” serve as both mechanical and functional interfaces between flexible substrates and components, making them central to the miniaturization and comfort requirements of next-generation devices.

DuPont’s $200 million investment into electronic materials production capacity in 2022 signaled strong confidence in conformable and conductive PSA technologies. A 2023 Nature Electronics study introduced a liquid-metal-infused acrylic PSA maintaining electrical conductivity at up to 300% strain, a game-changer for motion-based wearable sensors. Meanwhile, Apple’s patented “Biocompatible, Moisture-Vapor Permeable Acrylic Adhesive” with an MVTR exceeding 500 g/m²/day demonstrates the industry’s pivot toward skin-friendly, long-wear solutions in consumer wearables.

Nitto Denko’s SECAR® thermally conductive acrylic PSA, boasting a thermal conductivity of 3.0 W/mK, addresses the pressing challenge of heat dissipation in compact electronics — a critical bottleneck in high-density device design.

Acrylic Pressure Sensitive Adhesives (PSA) Market Share Insights

The water-based (emulsion) acrylic pressure sensitive adhesives (PSAs) segment dominates the global acrylic PSA industry, commanding an estimated 48% market share in 2025. This leadership is attributed to the superior environmental and regulatory profile of water-based technologies, which align with the global transition toward sustainable, low-VOC, and non-toxic adhesive formulations. Their versatility across diverse substrates and compatibility with paper, film, and foil materials make them indispensable in packaging, tapes, and label applications. Furthermore, as global manufacturers increasingly focus on REACH and EPA-compliant materials, water-based acrylic PSAs have become the default formulation for both industrial and consumer markets. Technological improvements in polymer emulsification, tackifier dispersion, and surfactant-free systems have significantly enhanced the performance of these adhesives. The combination of cost-effectiveness, safety, and sustainability continues to ensure their dominance in volume-driven industries such as packaging, construction, and consumer goods.

The hot-melt acrylic PSA segment, accounting for approximately 22% of the market, is recognized as the fastest-growing category within the global industry. These formulations uniquely integrate the instant bonding, clean application, and high-speed convertibility of traditional hot-melts with the aging resistance, UV stability, and chemical resilience of acrylic systems. As a result, they are rapidly gaining preference in high-speed labeling lines, tapes for packaging logistics, and automotive applications where productivity and durability are critical. The expansion of the e-commerce and logistics sectors, combined with the growing automation of packaging operations, is a major catalyst for adoption. Additionally, advancements in reactive hot-melt polymer chemistry are enabling new formulations that outperform solvent-based systems while maintaining recyclability.

While solvent-based and radiation-cured acrylic PSAs occupy smaller market shares, they play a pivotal role in high-performance, niche applications. Solvent-based PSAs continue to serve industries that demand exceptional initial tack, moisture resistance, and adhesion to challenging substrates like low-surface-energy plastics, automotive composites, and specialty films. However, their market share is gradually declining due to environmental regulations on volatile organic compounds (VOCs) and the rising efficiency of cleaner alternatives. Meanwhile, radiation-cured (UV/EB) acrylic PSAs are gaining traction in electronics, medical devices, and precision assembly due to their controlled curing kinetics, solvent-free nature, and high optical clarity.

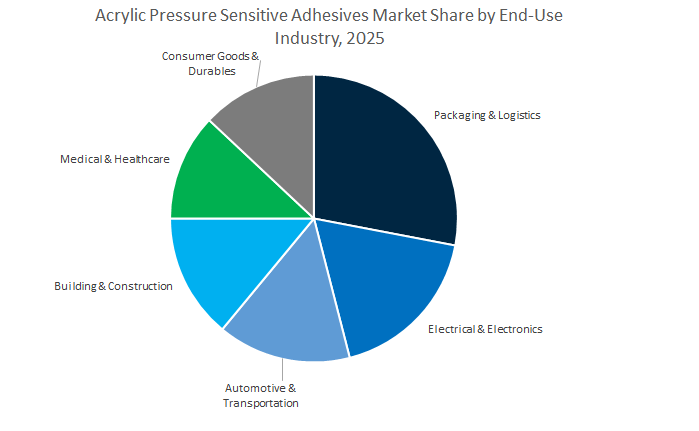

The packaging and logistics segment leads the global acrylic PSA market, capturing approximately 28% share in 2025, driven by the explosive rise in e-commerce, flexible packaging, and high-speed labeling applications. The packaging industry’s shift toward sustainable, water-based adhesive solutions has created strong demand for acrylic PSAs due to their clarity, durability, and compatibility with recycled substrates. These adhesives are integral to the production of pressure-sensitive tapes, carton sealing labels, and product identification films. Furthermore, as companies emphasize sustainable packaging design, the adoption of bio-based and solvent-free PSAs is accelerating. The convergence of automation, high-speed converting technology, and environmental compliance ensures that packaging and logistics will continue to be the volume backbone of the acrylic PSA industry.

The electrical and electronics segment, with around 18% market share, represents the high-value and innovation-intensive end of the PSA industry. Acrylic PSAs are widely used in display assembly, optoelectronic components, microelectronic insulation, protective films, and other applications requiring optical clarity, low outgassing, and temperature resistance. The boom in consumer electronics, EV battery modules, and flexible displays has driven steady growth for radiation-cured and high-purity solvent-based formulations. Likewise, miniaturization and device complexity are pushing adhesive manufacturers to develop ultra-thin, precision-coated PSA films compatible with automated assembly processes. These characteristics position electronics as a critical growth catalyst for premium acrylic PSAs, where performance supersedes cost.

The automotive and construction sectors jointly represent stable and mature demand centers for acrylic PSAs. These industries rely on the durability, UV stability, and vibration resistance of acrylic adhesives for applications such as interior trims, emblems, insulation foils, and mounting tapes. The rise of lightweight vehicles, EV production, and modular construction systems is stimulating new use cases for high-bond, thermally resistant PSAs that replace mechanical fasteners. Similarly, in the building and construction sector, acrylic PSAs play a vital role in insulation sealing, window protection, and floor lamination.

The competitive landscape of the global Acrylic Pressure Sensitive Adhesives market is defined by technological leadership, sustainability-driven R&D, and deep vertical integration across automotive, packaging, medical, and electronics sectors. Major players such as 3M, Henkel, Avery Dennison, H.B. Fuller, Arkema (Bostik), and Sika AG dominate through innovation in water-based, hot-melt, and UV-curable Acrylic PSA technologies that address the industry’s demand for performance, compliance, and application versatility.

3M Company maintains a strong leadership position through its VHB™ tapes, optically clear adhesives (OCA), and medical-grade Acrylic PSAs. The company continues to expand production for high-shear, temperature-resistant acrylic foam tapes across North America and Europe to support automotive assembly and EV applications. Its cross-linking polymer expertise ensures superior UV and chemical resistance, while its innovation in medical-grade Acrylic PSAs positions 3M as a global leader in precision bonding and biocompatible adhesive systems.

Henkel offers a comprehensive portfolio under its LOCTITE® and TECHNOMELT® brands, including high-solid, water-based Acrylic PSAs and hot-melt acrylics. The company’s heavy R&D investment in bio-based adhesives and low-VOC PSA solutions reflects its commitment to sustainability. With new capital expansions across Europe, Henkel is accelerating the commercialization of solvent-free PSA technologies tailored for rigid packaging and high-speed industrial applications, reinforcing its position as a pioneer in sustainable pressure-sensitive systems.

Avery Dennison is a global frontrunner in pressure-sensitive materials (PSM) that heavily rely on emulsion and solvent-based acrylic PSA systems. Its recent acquisition of a specialized thin-film coating company enhances capabilities in optically clear Acrylic PSAs (OCAs) for advanced displays and intelligent labeling solutions. The company’s focus on durable, UV-resistant outdoor Acrylic PSAs and high-tack adhesives for challenging substrates consolidates its dominance in the labeling, packaging, and digital graphics industries.

H.B. Fuller delivers a robust range of liquid and hot-melt Acrylic PSAs catering to hygiene, medical, and packaging applications. The opening of its Asia-Pacific Water-Based PSA Technical Center underscores the company’s strategy to localize innovation and serve the region’s rapidly expanding flexible packaging and converting markets. With strong integration into medical and hygiene product value chains, Fuller’s Acrylic PSA technologies emphasize skin-friendliness, consistent adhesion, and low residue performance.

Arkema’s Bostik division offers a diverse portfolio of acrylic and hybrid acrylic-polyurethane PSAs, including hot-melt formulations designed for multi-material bonding in electric vehicle assembly and construction. The company’s new R&D initiative focuses on developing next-generation structural Acrylic PSAs that deliver high adhesion on metals, composites, and flexible substrates. Arkema’s specialty polymer expertise ensures its PSAs provide thermal stability, chemical resistance, and performance durability under demanding operating conditions.

Sika AG integrates Acrylic PSA technology into its building and automotive tape systems, serving the construction and aftermarket segments. The company is expanding its manufacturing footprint across emerging economies, aligning with global infrastructure growth. Known for its weather-resistant and moisture-curing Acrylic PSAs, Sika’s adhesives are widely used in roofing, façade, and flooring applications, where long-term durability and environmental compliance are essential performance metrics.

China remains the epicentre of global acrylic pressure sensitive adhesive (PSA) production, propelled by an extensive manufacturing ecosystem and escalating demand across electronics, packaging, construction, and automotive sectors. The domestic electronics industry has witnessed a strong uptick in the use of optically clear acrylic adhesives (OCA), particularly for flexible displays and high-performance electronic assemblies. The advancements cater to leading technology manufacturers, enhancing display clarity, flexibility, and heat resistance.

Simultaneously, China’s infrastructure and real estate boom continues to generate large-scale applications for weather-resistant and durable acrylic PSAs, notably in facade insulation, waterproof membranes, and energy-efficient construction materials. The rapid growth of e-commerce and logistics is another defining force, fueling extensive use of acrylic-based permanent labels and carton-sealing tapes, supporting millions of daily domestic shipments.

Environmental reform remains central to China’s industrial agenda, as local manufacturers ramp up APEO-free, low-VOC acrylic emulsions to comply with stricter emission policies. Moreover, the country’s expanding EV production ecosystem integrates advanced acrylic foam tapes to achieve lightweighting, vibration damping, and noise reduction, further diversifying PSA demand. Through a combination of manufacturing scale, regulatory adaptation, and technological maturity, China continues to dominate as a high-capacity and innovation-driven hub in the global acrylic PSA landscape.

The United States acrylic PSA market is entering a new phase of sustainability-oriented innovation, marked by a surge in bio-based and solvent-free adhesive technologies. Top manufacturers are investing heavily in bio-acrylic and renewable resin formulations, aligning with national sustainability goals and major corporate ESG commitments. The initiatives are reducing dependency on petrochemical feedstocks while maintaining the shear strength, tack, and peel adhesion performance required by high-value industrial users.

In the healthcare and medical device sector, U.S. producers are driving breakthroughs in skin-safe medical-grade acrylic PSAs for wound dressings, wearable patches, and biosensor adhesion. Concurrently, the automotive industry is adopting lightweight, high-strength acrylic PSAs for bonding mixed materials like aluminum, carbon composites, and plastics—essential for the structural integrity of next-generation electric vehicles (EVs).

Ongoing R&D in optically clear adhesives (OCA) is enhancing display performance for automotive infotainment systems and consumer electronics, reinforcing the nation’s leadership in advanced materials. Moreover, a strategic push toward regionalized manufacturing—accelerated by post-2025 tariff policies and near-shoring of acrylic monomer production—is strengthening domestic supply security. With innovation extending into high-performance solvent-based PSAs for aerospace and industrial applications, the U.S. stands as a technology leader in the global transition toward sustainable, high-performance adhesive systems.

Germany continues to anchor the European acrylic PSA industry through its commitment to sustainability, precision manufacturing, and materials innovation. Strict EU environmental mandates are driving a rapid transformation toward water-based and UV-cured acrylic PSAs, particularly across automotive, construction, and industrial sectors. The advanced adhesives are prized for their low-VOC profiles, superior temperature resistance, and long-term bond stability, aligning with the EU’s Green Deal objectives.

Germany’s position as a hub for high-performance tape production is reinforced by the development of Acrylic Foam Tapes (AFT) used for structural bonding in automotive assemblies, where durability and vibration resistance are paramount. Major chemical companies headquartered in Germany continually pioneer next-generation PSA formulations designed to withstand harsh chemical and thermal environments. Moreover, the country’s machinery engineering excellence supports innovation in high-speed precision coating equipment—optimizing the production efficiency of hot-melt and emulsion-based acrylic PSAs.

In the construction industry, energy efficiency initiatives are amplifying demand for specialized acrylic bonding systems that improve sealing and insulation in building envelopes. The cohesive blend of engineering sophistication, sustainability focus, and R&D leadership keeps Germany at the forefront of high-performance PSA innovation in Europe.

Japan’s acrylic PSA industry epitomizes precision engineering and high-value technological applications, making it a global benchmark for functional and performance-driven adhesives. The nation’s expertise in microelectronics and flexible circuitry has resulted in widespread use of ultra-pure, high-clarity acrylic PSAs for complex multi-layer film bonding and flexible printed circuits. Japanese companies lead in the continuous refinement of optically clear adhesives (OCA) for display technologies, supporting the production of high-resolution OLED and LCD screens in smartphones, tablets, and automotive displays.

Beyond electronics, the automotive sector remains a pivotal end-user of high-tack, impact-resistant acrylic PSAs—essential for secure interior fastening, dashboard assembly, and safety component integration. Ongoing R&D is also focused on functional PSA formulations with enhanced thermal conductivity, electromagnetic shielding, and flame retardancy, aligning with the country’s innovation-led approach.

Japan’s strong culture of R&D collaboration between academia, automotive OEMs, and electronics manufacturers enables it to consistently push the boundaries of adhesive performance. The precision-driven ecosystem ensures Japan’s leadership in smart, multifunctional, and high-purity acrylic PSA technologies.

India’s acrylic PSA market is witnessing rapid acceleration, driven by the government’s “Make in India” initiative and the country’s expanding manufacturing base. The surge in industrial tapes, labels, and protective films demand has turned India into a promising destination for both domestic production and global export of cost-effective acrylic emulsions. The booming FMCG and e-commerce packaging sectors are key consumers, relying heavily on pressure-sensitive acrylic labels and sealing tapes that balance affordability with strong adhesion.

The country’s infrastructure growth—spanning transport networks, housing, and commercial projects—has further increased demand for weather-resistant and durable adhesive solutions suitable for concrete bonding, insulation, and protective coatings. A notable milestone includes Henkel’s new application lab in Chennai (announced in 2024, set to open by 2025), designed to strengthen regional R&D and customer collaboration. The developments highlight India’s transition from a consumption-driven to a production-oriented acrylic PSA hub, reinforcing its importance in the Asia-Pacific adhesives ecosystem.

France holds a strategic role in the European acrylic PSA industry, leveraging its deep-rooted specialty chemical expertise and innovation in UV-curable and solvent-free formulations. Major players like Arkema (Bostik) continue to advance specialty acrylic PSAs for electronics, healthcare, and high-performance industrial applications, strengthening the nation’s foothold in precision adhesive technologies.

The aerospace and defense sectors represent a niche but critical segment, utilizing high-durability acrylic PSAs for non-structural bonding in aircraft interiors, where fire resistance, weight reduction, and durability are key performance indicators. Simultaneously, France’s commitment to green chemistry is reshaping its PSA production base, encouraging solvent-free and compliant formulations to meet EU environmental standards. With its blend of chemical innovation and advanced industrial design, France remains a key European hub for next-generation acrylic PSA systems.

South Korea is a global innovation leader in the acrylic PSA industry, driven by its dominance in OLED and QLED display manufacturing. The country’s electronics giants consistently demand high-specification Optically Clear Adhesives (OCA) that offer optical precision, durability, and chemical resistance. The segment has experienced double-digit growth as display technologies advance toward flexible, foldable, and ultra-thin formats.

Beyond electronics, electric vehicle (EV) battery production is an emerging catalyst for South Korea’s acrylic PSA growth. The adhesives play a pivotal role in battery insulation, component protection, and thermal management, enabling safer and more reliable EV architectures. With its robust R&D infrastructure and export-driven manufacturing model, South Korea continues to reinforce its global position as a technology-intensive hub for advanced PSA applications.

Acrylic Pressure Sensitive Adhesives Market Report Scope

Acrylic Pressure Sensitive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.3 Billion

|

|

Market Size (2034)

|

$33.5 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Technology (Water-based (Emulsion) Acrylic PSAs, Solvent-based Acrylic PSAs, Hot-Melt Acrylic PSAs, Radiation Cured Acrylic PSAs (UV/EB)), By Product Type (Tapes (Single & Double-Sided), Labels & Tags, Graphic Films (Window films, Signage), Others), By End-Use Industry (Packaging & Logistics, Automotive & Transportation, Building & Construction, Electrical & Electronics, Medical & Healthcare, Consumer Goods & Durables), By Chemistry (Butyl Acrylate-based PSAs, 2-Ethylhexyl Acrylate-based PSAs, Functional Acrylates

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M, H.B. Fuller Company, Avery Dennison Corporation, Arkema S.A. (Bostik), Sika AG, Dow, Wacker Chemie AG, Tesa SE (Beiersdorf Group), LG Chem, Nitto Denko Corporation, DIC Corporation, LINTEC Corporation, Ashland Inc., Soken Chemical & Engineering Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology

- Water-based (Emulsion) Acrylic PSAs

- Solvent-based Acrylic PSAs

- Hot-Melt Acrylic PSAs

- Radiation Cured Acrylic PSAs (UV/EB)

By Product Type

- Tapes (Single & Double-Sided)

- Labels & Tags

- Graphic Films (Window films, Signage)

- Other Applications (Protective Films, Medical, etc.)

By End-Use Industry

- Packaging & Logistics

- Automotive & Transportation

- Building & Construction

- Electrical & Electronics

- Medical & Healthcare

- Consumer Goods & Durables

By Chemistry (Acrylic Monomer Type)

- Butyl Acrylate-based PSAs

- 2-Ethylhexyl Acrylate-based PSAs

- Functional Acrylates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M

- H.B. Fuller Company

- Avery Dennison Corporation

- Arkema S.A. (Bostik)

- Sika AG

- Dow

- Wacker Chemie AG

- Tesa SE (Beiersdorf Group)

- LG Chem

- Nitto Denko Corporation

- DIC Corporation

- LINTEC Corporation

- Ashland Inc.

- Soken Chemical & Engineering Co., Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the Global Acrylic Pressure Sensitive Adhesives industry’s demand inflection driven by low-VOC adoption, EV/lightweighting use cases, and high-purity electronics applications; it consolidates breakthroughs in bio-acrylic monomers, hot-melt acrylics, UV/EB curing, debond-on-demand chemistries, and optically clear PSA systems into decision-ready insights. Produced by USDAnalytics, the study delivers analysis reviews of technology migration (solvent → water/hot-melt/UV), performance benchmarks (shear, peel, heat/UV stability), and regulatory catalysts shaping procurement and specification choices across tapes, labels, films, and medical wearables. It highlights capacity moves, M&A, and regionalization strategies that are redefining cost curves and service models, and maps price sensitivities to feedstock and compliance variables. By translating technical advances into commercial impact, this report is an essential resource for executives, product managers, and procurement leaders aligning portfolio roadmaps to sustainability, convertibility, and throughput KPIs.

Scope Highlights

- By Technology/Formulation: Water-based (Emulsion) Acrylic PSAs; Solvent-based; Hot-Melt Acrylic PSAs; Radiation-Cured (UV/EB).

- By Product/Application: Tapes (single & double-sided); Labels & Tags; Graphic Films (window films, signage); Other Applications (protective films, medical, etc.).

- By End-Use Industry: Packaging & Logistics; Automotive & Transportation; Building & Construction; Electrical & Electronics; Medical & Healthcare; Consumer Goods & Durables.

- By Chemistry: Butyl-acrylate-based; 2-Ethylhexyl-acrylate-based; Functional Acrylates.

- .

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies (e.g., Henkel, 3M, Avery Dennison, H.B. Fuller, Arkema/Bostik, Sika, Dow, Wacker, tesa, LG Chem, Nitto, DIC, LINTEC, Ashland, Soken Chemical).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.