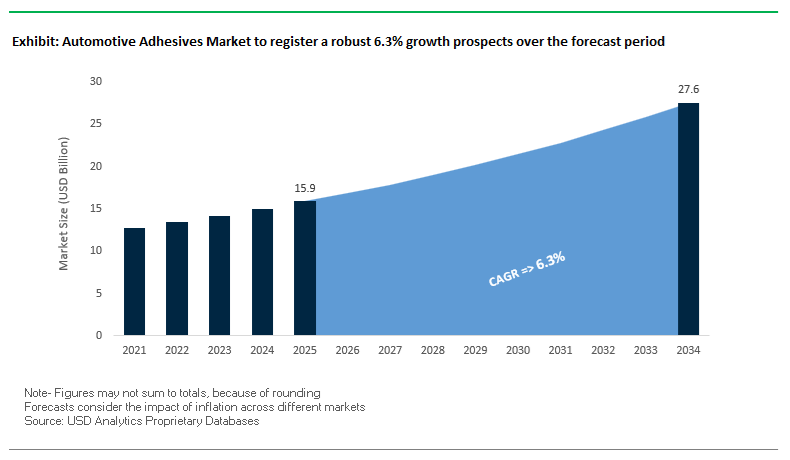

The global automotive adhesives market is projected to expand from USD 15.9 billion in 2025 to USD 27.6 billion by 2034, advancing at a 6.3% CAGR, as vehicle manufacturers fundamentally redesign platforms around electrification, mixed-material body structures, and adhesive-first assembly strategies. Adhesives are no longer auxiliary joining materials; they have become structural, safety-critical enablers replacing welding, riveting, and mechanical fastening across body-in-white (BIW), closures, battery systems, and vehicle interiors.

A central driver is the shift toward multi-material vehicle architectures, where advanced high-strength steel, aluminum, composites, and polymers must be joined without inducing corrosion, stress concentrations, or fatigue failure. Structural epoxy adhesives allow OEMs to reduce weld points by up to 45% per assembly, while simultaneously improving load distribution and enabling vehicle weight reductions exceeding 15% when combined with thinner-gauge materials. This substitution directly supports lightweighting mandates, crash performance targets, and extended vehicle durability.

Electrification further amplifies adhesive demand. In battery electric vehicles, adhesives and sealants perform multiple critical functions simultaneously—structural bonding, thermal management, electrical insulation, and environmental sealing. Silicone-based thermal gap fillers with thermal conductivity in the 2.5–4.0 W/mK range are increasingly specified within battery enclosures to manage heat dissipation, mitigate thermal runaway risk, and maintain pack integrity over long service lives. Adhesive-based battery assembly also reduces mechanical fasteners, supporting automation and improving pack stiffness.

Beyond structure and batteries, adhesives address systemic vehicle performance challenges introduced by lightweight design. Galvanic isolation adhesives and tapes prevent electrochemical corrosion between dissimilar metals such as steel and aluminum, a key failure risk in modern BIW designs. Liquid-applied sound dampeners (LASD) and elastomeric sealants further enhance vehicle refinement, reducing cabin noise by up to 5 dB, a particularly important attribute for electric and premium vehicles where powertrain noise is minimal.

From a manufacturing standpoint, the market is shaped by process substitution and throughput gains. Heat-curing polyurethane adhesives achieve handling strength in under 30 minutes, enabling faster takt times and compatibility with high-volume automated production lines. Simultaneously, OEMs are accelerating adoption of low-VOC, REACH-compliant, and recyclable adhesive formulations, aligning bonding technologies with global sustainability targets and regulatory frameworks.

The global automotive adhesives industry is rapidly evolving toward sustainability, efficiency, and e-mobility alignment. In September 2025, Henkel AG & Co. KGaA unveiled a sustainable packaging innovation with its new recyclable cardboard cartridges, reducing plastic waste by over 51% across its adhesives and sealants portfolio. This development underscores Henkel’s commitment to sustainable adhesive systems and its effort to reduce lifecycle emissions across automotive supply chains.

In the same month, Huntsman Advanced Materials launched a new generation of ARALDITE® epoxy adhesives that are BPA- and CMR-free, addressing stringent EU worker safety standards while maintaining the high structural integrity expected in aerospace-grade and automotive applications. These next-generation adhesives reflect the industry’s shift toward safer chemistries and high-performance bonding for lightweight structures and EV enclosures.

In May 2025, PPG Industries reinforced its position in the EV adhesives market, highlighting a portfolio of thermal interface and fire-protection materials designed for battery pack assembly and module safety. The company’s emphasis on electric mobility materials demonstrates how adhesives are integral to EV design, safety, and performance. Similarly, Saint-Gobain’s product expansion (January 2025) diversified its adhesive range for structural and semi-structural bonding, catering to applications from panel bonding to battery enclosure sealing.

Strategic M&A and policy changes are shaping the competitive landscape. In October 2024, a global chemical conglomerate completed the acquisition of a European Thermal Interface Material (TIM) specialist, integrating high-conductivity EV gap fillers into its automotive adhesive portfolio. Meanwhile, EU End-of-Life Vehicle (ELV) directives (August 2024) are driving the development of debondable adhesive technologies, ensuring easier material separation and recyclability during vehicle dismantling—a major advancement for the circular automotive economy.

Technological progress continues to accelerate production efficiency. In July 2024, a leading adhesive manufacturer unveiled a fast-curing structural epoxy capable of reaching 90% of ultimate shear strength within 10 minutes at 170°C, significantly improving Body Shop throughput and takt time. Further, Henkel’s $30 million investment (June 2024) in its Brandon, South Dakota facility solidified its role as the North American hub for mobility adhesives, reinforcing global supply chain resilience and thermal management capacity for EV production.

The global transition toward lightweighting and mixed-material architectures—especially in Electric Vehicles (EVs) burdened by heavy battery systems—has established structural adhesives as a cornerstone of Body-in-White (BIW) design. Automakers are leveraging these high-performance adhesives to reduce vehicle weight, enhance crash performance, and extend lifecycle durability.

Leading suppliers have engineered two-part structural epoxy adhesives that achieve tensile lap-shear strengths exceeding 20 MPa on e-coated aluminum substrates at 23 °C and retain over 70% of their strength after 14 days of Cataplasma exposure—a rigorous humidity and heat resistance test. These adhesives maintain mechanical integrity over a 15-year vehicle lifespan, meeting the crash-worthiness standards of EV platforms.

The integration of adhesives alongside traditional joining techniques (e.g., weld-bonding) has been shown to boost fatigue resistance, increase joint stiffness, and enhance impact energy absorption. Studies across leading OEMs report that combining Advanced High-Strength Steel (AHSS) and aluminum with adhesives results in a 15–25% improvement in fatigue life, directly contributing to superior crash safety and structural longevity.

Automotive manufacturers are deploying non-conductive structural isolation tapes to address galvanic corrosion—a major issue when bonding dissimilar metals. These advanced tapes deliver both bonding strength and electrical insulation, allowing seamless integration of aluminum and steel in BIW applications while ensuring long-term corrosion protection under severe environmental exposure.

As the automotive landscape electrifies, Battery Electric Vehicles (BEVs) are redefining adhesive performance requirements—demanding formulations that combine structural bonding, thermal management, and fire resistance within compact, high-energy battery systems.

State-of-the-art thermally conductive adhesives (TCAs) deliver thermal conductivity up to 3.8 W/m·K, ensuring efficient heat transfer from lithium-ion cells to cooling systems. These adhesives are also UL 94 V-0 rated, guaranteeing flame retardancy that extinguishes fire within 10 seconds—an essential safety feature in EV battery modules.

Leading manufacturers are investing heavily in developing thermally resilient epoxies and polyurethanes that provide flexibility, high peel strength, and superior thermal shock resistance—allowing the adhesive to absorb volume changes caused by cell expansion during charge-discharge cycles. The combination of mechanical toughness and elasticity ensures long-term thermal and mechanical stability under aggressive operational stresses.

In addition to bonding, specialized flame-retardant foams and potting compounds are being integrated within BEV battery packs. These materials prevent thermal runaway propagation—a critical safety concern—by acting as thermal barriers that isolate failing cells from adjacent modules.

Adhesive innovation in the EV sector directly impacts battery efficiency, safety, and manufacturability, positioning next-generation BEV adhesives as a pivotal enabler of energy density optimization and battery longevity in electric mobility.

Market Opportunity 1: Enabling the Manufacturing of Gigacast Vehicle Subframes

The Gigacasting revolution—a manufacturing breakthrough involving single-piece aluminum castings for vehicle underbodies—is reshaping adhesive application in automotive production. As manufacturers like Tesla, Volvo, and Toyota scale Gigacasting for mass production, the need for high-performance structural adhesives capable of bonding massive, high-tolerance cast components is skyrocketing.

Gigacasting reduces the number of structural components from over 170 individual parts to a single casting, dramatically cutting assembly time and weld points. The consolidation shifts adhesive demand toward nodal bonding, where adhesives strengthen connections between large aluminum castings and steel modules—critical junctions in EV architectures.

New adhesive injection systems designed for Gigacasting applications are enabling fast-fill, high-viscosity two-component (2K) adhesives to be precisely applied into deep joint cavities with automated accuracy. These formulations exhibit non-sag properties, superior gap-filling capability, and high-elongation resilience to withstand the differential expansion between aluminum castings and surrounding materials.

Adopting advanced sealants and adhesives in Gigacasting improves chassis stiffness, load distribution, and crash resistance, while reducing overall vehicle weight by up to 20–30 kg per assembly. The result is greater range efficiency in EVs and a clear cost advantage for OEMs through faster, automated production cycles.

Market Opportunity 2: Development of Sustainable and Circular Adhesive Solutions

The global shift toward circular automotive manufacturing and end-of-life vehicle recovery is driving innovation in sustainable, debondable, and bio-based adhesive systems. As automakers face stringent recycling quotas under the EU Battery Passport and Extended Producer Responsibility (EPR) frameworks, the development of recyclable and bio-circular adhesives is becoming both a regulatory necessity and a market opportunity.

The European Commission’s upcoming battery recycling mandates require that all high-voltage EV batteries be designed for repairability and material recovery. The is accelerating demand for debonding-on-demand adhesives, which enable clean, non-destructive disassembly of bonded components such as battery modules, pack housings, and structural composites—directly reducing waste and manufacturing costs.

The European BiDebA Project (Biobased Debondable Adhesives) exemplifies the innovation frontier. Its research focuses on bio-based polymers that can be triggered by heat, induction, or chemical activation to safely release bonded joints, allowing for efficient material separation during recycling or remanufacturing. The reversible bonding capability directly supports circularity by extending product life cycles and minimizing landfill waste.

Sustainable adhesives formulated with renewable raw materials (e.g., plant-based polyols, starch-derived resins) are gaining traction, with some structural adhesive systems containing up to 30% bio-based content. These eco-friendly formulations not only meet low-VOC standards but also contribute to automakers’ Scope 3 emission reduction targets, reinforcing their sustainability credentials.

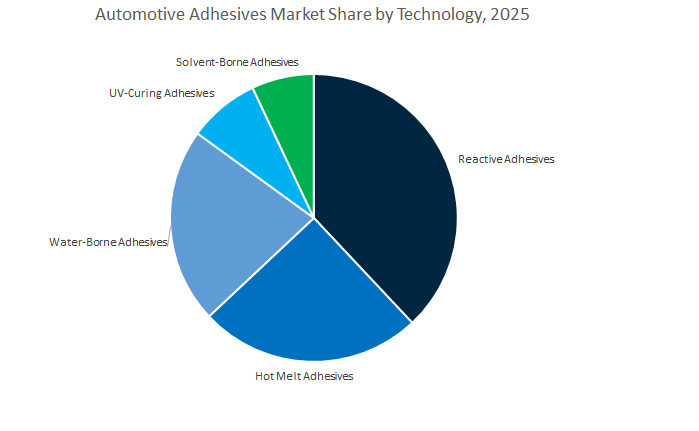

Automotive Adhesives Market Share Insights, 2025-2034

The reactive adhesives segment dominates the global automotive adhesives industry, holding an estimated 38% market share in 2025. Its dominance is attributed to the exceptional performance, strength, and durability these formulations deliver in demanding automotive environments. Reactive systems—primarily epoxies, polyurethanes (PU), and acrylics—are indispensable for structural and semi-structural applications, including Body-in-White (BIW) assemblies, glazing, and electric vehicle (EV) battery modules. These adhesives cure through chemical reactions that create strong, permanent bonds capable of withstanding high mechanical loads, thermal cycling, and chemical exposure. In an era of lightweight vehicle architectures, reactive adhesives enable OEMs to bond dissimilar materials such as aluminum, composites, and high-strength steel, supporting both fuel economy and crash performance. The widespread shift toward EV platforms has further expanded the role of reactive adhesives, particularly in battery pack structural bonding, gap filling, and vibration damping. Their superior fatigue resistance and structural reliability make them essential for extending vehicle life and safety, solidifying this segment’s position as the technological backbone of modern automotive manufacturing.

The hot melt adhesives segment, projected to account for approximately 25 percent of the 2025 market, is expanding rapidly due to its speed, efficiency, and compatibility with automated automotive manufacturing. Solvent-free hot melts based on polyolefin, EVA, and reactive PUR chemistries offer instant tack, fast set times, and clean processing for high-speed assembly operations, supporting applications such as interior and trim bonding, seat and carpet lamination, wire harness attachment, and weatherstrip sealing. The rise of reactive PUR hot melts, which combine thermoplastic processing with thermoset-level strength, is further enhancing adoption in both interior and semi-structural bonding. Hot melts also enable VOC-free production and align with Industry 4.0 through robotic dispensing integration, positioning PUR-based systems as one of the fastest-growing technologies in automotive adhesives. In parallel, the water-borne adhesives segment maintains a strong, stable position driven by sustainability requirements and environmental compliance. Acrylic and polyurethane dispersions play a central role in interior bonding applications including headliners, seats, door panels, and carpets, supported by their low VOC emissions, non-flammability, and suitability for occupant-facing cabin environments. Ongoing advances in crosslinking and polymer dispersion technologies have improved their heat and humidity resistance, reinforcing their role as a sustainable, regulatory-compliant alternative as automakers pursue carbon neutrality and broader ESG commitments.

The UV-curing adhesives segment, though smaller in scale, is becoming increasingly essential for precision automotive applications that require rapid curing, high optical clarity, and exceptional bonding accuracy. These formulations are widely used in lighting assemblies, sensor modules, camera systems, and decorative components, benefiting from on-demand UV polymerization that enables near-instant curing and high throughput in automated production environments. Their excellent adhesion to plastics, glass, and metals, combined with low shrinkage and transparent finishes, makes them particularly valuable in headlamp and taillight lens bonding as well as in ADAS and autonomous driving systems where LiDAR, radar, and optical sensors demand reliable, optically clear bonding. As automotive electronics grow more advanced, UV-curing adhesives are positioned for sustained double-digit growth driven by miniaturization, lightweighting, and high-performance bonding needs. In contrast, the solvent-borne adhesives segment represents a declining but still relevant niche, maintaining use in legacy production lines and aftermarket applications that require immediate high tack, strong water resistance, and fast drying. Despite regulatory pressures reducing their prevalence, solvent-based systems remain valued in specific scenarios where robustness and ease of application are essential.

The Body-in-White (BIW) segment is the largest and most strategically critical application area, commanding approximately 24% of the global automotive adhesives market share in 2025. Adhesives are integral to modern BIW assembly, enabling automakers to replace welds, bolts, and rivets with lightweight, high-strength bonds that improve structural rigidity and crashworthiness. Epoxy and polyurethane-based structural adhesives are particularly vital in hem flanging, frame reinforcement, and joint sealing, ensuring durability under thermal and mechanical stress. The trend toward multi-material vehicle bodies, combining steel, aluminum, and carbon fiber, has dramatically increased the reliance on structural adhesives, as they provide uniform load distribution and corrosion protection between dissimilar substrates. Furthermore, BIW adhesives enhance noise and vibration damping (NVH) while improving overall energy absorption during impact, key attributes for meeting stringent safety and emissions standards. As OEMs continue to develop next-generation electric vehicle platforms, the importance of BIW adhesives in achieving lightweight, rigid structures will only intensify, solidifying their role as the cornerstone of modern vehicle architecture.

The interior segment, accounting for about 22% of the 2025 market share, is another major contributor to the automotive adhesives landscape. Adhesives are used extensively in trim assembly, seating, headliners, flooring, dashboard bonding, and acoustic insulation, providing not only functional adhesion but also enhanced comfort and aesthetics. The dominance of water-borne and hot melt adhesives in this segment aligns with the industry’s focus on low-VOC, low-odor, and environmentally sustainable materials. Interior bonding applications demand adhesives that offer flexibility, heat resistance, and long-term durability, while ensuring smooth finishes and resistance to delamination. The increasing integration of interior electronics, ambient lighting, and lightweight composite panels is driving the need for more advanced adhesive solutions with superior material compatibility. Moreover, the shift toward luxury and premium interiors in both ICE and EV segments has elevated the importance of adhesives that deliver noise reduction, fire retardancy, and improved tactile quality. As vehicle interiors become digital and multifunctional, adhesive systems are evolving from simple bonding agents into multi-performance materials that contribute directly to passenger comfort, design, and sustainability.

The EV battery assembly segment is the fastest-growing and most technologically transformative area of the global automotive adhesives market, driven by rising EV adoption and the need for advanced thermal interface materials, structural adhesives, vibration-damping solutions, and fire-retardant sealants that ensure battery safety, efficiency, and durability. As automakers shift to solid-state and higher-energy-density batteries, demand is increasing for silicone, epoxy, and polyurethane systems capable of withstanding extreme heat and chemical exposure. At the same time, the Powertrain and Under-the-Hood segment is transitioning from traditional ICE applications toward e-motor insulation, inverter encapsulation, and thermal management for EV power electronics, supported by high-temperature and thermally conductive adhesives. Glazing and exterior bonding applications, including windshield installation, lighting assemblies, and trim attachment, continue to rely on UV-resistant silicone and acrylic systems that provide weatherproof sealing, aerodynamic flexibility, and long-term clarity.

The automotive adhesives market is dominated by five global leaders—Henkel AG & Co. KGaA, Sika AG, Huntsman International LLC, The Dow Chemical Company, and PPG Industries, Inc. Each company combines deep chemistry expertise with regional production capabilities to serve the expanding needs of electric mobility, structural bonding, and lightweight automotive design.

Henkel leads the market with its Loctite® and Bonderite® adhesive brands, offering solutions for thermal management, structural integrity, and acoustic sealing. Its Battery Engineering Center in Düsseldorf drives R&D on injectable thermally conductive adhesives such as Loctite TLB 9300 APSi, engineered to stabilize battery temperature and prevent thermal runaway. The company’s multi-chemistry portfolio—spanning polyurethane, epoxy, and silicone systems—enables metal-to-plastic bonding across BIW, exterior trims, and EV assemblies. Henkel also pioneers water-based and renewable thermoset systems, aligning with automotive decarbonization goals.

Sika AG dominates in elastic structural bonding and load-bearing sealants, catering to commercial vehicles, EVs, and next-gen lightweight assemblies. Its Sikaflex® and SikaForce® product lines integrate Silane-Terminated Polymer (STP) technology, combining polyurethane durability with enhanced environmental compliance. The Sika® Booster system accelerates 1K PU curing, shortening assembly times for large body panels. Its SikaForce® 803 L45 adhesives enable primerless bonding of composites, a key advantage in EV and specialty vehicle production. By replacing mechanical fasteners, Sika helps OEMs achieve superior fatigue resistance and corrosion protection.

Huntsman’s ARALDITE® epoxy and ARATHANE® polyurethane adhesives deliver unmatched structural reliability in buses, rail, and lightweight automotive applications. The company’s BPA-free, CMR-free adhesive range (launched September 2025) represents a major milestone in safe industrial chemistry. Its composite bonding systems maintain mechanical strength under high fatigue conditions, ideal for CFRP-to-metal applications. Huntsman also incorporates Post-Consumer Recycled (PCR) packaging, cutting CO₂ emissions by up to 36%, showcasing its commitment to sustainable manufacturing and regulatory compliance.

Dow is a key innovator in silicone and fluorosilicone adhesives, offering advanced DOWSIL™ and SILASTIC™ systems for sealing, NVH dampening, and heat resistance. Its adhesives ensure UV and ozone stability up to 200°C, critical for engine bay and powertrain sealing. Dow’s sealants minimize squeaks and rattles, enhancing NVH performance and cabin comfort. With excellent dielectric properties, these materials protect sensors, actuators, and electronic modules in EVs. Dow’s focus on thermal management and electronic insulation strengthens its leadership in electric mobility adhesive solutions.

PPG Industries combines its adhesive technologies with its coatings portfolio, creating integrated solutions across BIW, Paint Shop, and Final Assembly. Products such as CORABOND® and REVOFORM® reduce panel flutter and vibration, while TOTALSEAL® polyurethane adhesives enhance structural integrity in metal–composite bonding. Its 4 Wet Sealer Technology simplifies paint shop processes, cutting cycle times and improving energy efficiency. PPG’s EV-oriented adhesives are tailored for battery encapsulation and module sealing, reinforcing its role in EV structural and safety applications.

China remains the epicenter of global automotive adhesive innovation, particularly due to its dominance in electric vehicle (EV) production and giga-factory expansion. Leading domestic manufacturers are investing heavily in one-component epoxy structural adhesives that provide enhanced thermal conductivity and mechanical strength for battery cell-to-module and module-to-pack assembly. The high-performance adhesives are specifically engineered for high-speed, automated production environments in China’s massive EV manufacturing ecosystem.

In late 2024, a global adhesives producer completed its third Asia-Pacific technical center expansion in Shanghai, focusing on fast-curing, high-toughness epoxy formulations optimized for robotic application lines. The adoption of Polyurethane (PU) hot-melt adhesives in vehicle interior lamination is also increasing, supporting lightweight, durable, and aesthetically refined cabin assembly for domestic OEMs.

The New Energy Vehicle (NEV) Development Plan continues to set stringent standards for vehicle crash performance, leading to wider replacement of spot welding with toughened structural adhesives in Body-in-White (BiW) applications. Moreover, Chinese EV manufacturers are utilizing reactive hot-melt adhesives (RHM) for headlamp assembly, improving thermal cycling resistance and moisture durability — a crucial step for high-speed production lines.

Germany continues to lead Europe in advanced adhesive R&D for premium vehicle manufacturing, with a strong emphasis on lightweight construction, acoustic comfort, and sustainability compliance. German specialty chemical companies are developing next-generation polyurethane (PU) glass bonding adhesives that enable primerless, fast-processing applications, aligning with European crash safety standards and high-speed automated assembly.

The German automotive sector is a pioneer in multi-material bonding, using two-component epoxy systems for joining aluminum and carbon fiber reinforced plastics (CFRP) to reduce vehicle mass without compromising structural integrity. In parallel, REACH regulation compliance has driven a rapid transition to low-VOC, waterborne adhesives in interior components such as dashboards and door panels, ensuring reduced cabin emissions and improved sustainability.

In early 2025, a major global adhesive manufacturer launched a state-of-the-art Automotive Application Center near Stuttgart, enabling real-time validation of structural bonding processes, dispensing precision, and thermal cure optimization. The advancements position Germany as the benchmark market for premium adhesives in luxury EV and hybrid platforms.

The U.S. automotive adhesives industry is undergoing a major expansion driven by domestic EV gigafactory construction and federal manufacturing incentives. Major adhesive producers have announced new capital investments to boost the supply of thermal conductive adhesives (TCA) and specialty gasketing materials essential for EV battery pack assembly and thermal management.

The North American market is seeing a strong shift toward acrylic-based structural adhesives for composite and plastic bonding in Light Commercial Vehicles (LCVs) and pickup trucks, replacing rivets and welds for improved fatigue resistance and assembly efficiency. In academia, recent research breakthroughs in self-healing epoxy systems are laying the foundation for adhesives that automatically repair micro-cracks in battery enclosure joints, improving lifecycle durability.

Furthermore, federal and state policies promoting domestic EV production are stimulating demand for high-elongation, crash-resistant adhesives that enhance occupant safety in large-format EV battery trays. Concurrently, U.S. adhesive companies are pursuing sustainability-focused R&D for low-VOC, solvent-free formulations to meet EPA 2025 emission standards, particularly in interior and trim adhesives.

Japan’s automotive adhesives market is defined by its technological precision and focus on electronic integration, supporting the nation’s leadership in hybrid and fuel cell vehicle (FCV) technology. Japanese adhesive manufacturers are at the forefront of ultra-fast-curing urethane adhesives, specifically designed for ADAS (Advanced Driver Assistance Systems) sensors, camera modules, and compact electronic components, addressing increasing miniaturization in modern vehicles.

Local companies are also innovating in acoustic damping technologies, developing elastomeric liquid-applied sound dampeners (LASD) that improve Noise, Vibration, and Harshness (NVH) control in hybrid and EV interiors. Key automotive OEMs are adopting reactive silicone sealants for high-temperature applications, including fuel cell stack sealing and thermal management systems, leveraging their superior chemical resistance and durability.

The advancements reflect Japan’s continuous pursuit of lightweighting and interior comfort in alignment with its high-efficiency, low-emission vehicle roadmap.

South Korea’s automotive adhesives sector is scaling rapidly in alignment with its dominance in EV platform exports. Large chemical conglomerates are investing in two-component polyurethane (PU) and epoxy adhesives for modular vehicle assembly, catering to global OEMs transitioning to battery-electric architectures.

Manufacturers are also innovating light-curing adhesives that enhance production efficiency for interior and exterior plastic components, enabling faster cycle times and reduced energy consumption in automated lines. A growing area of specialization is the development of fire-retardant and intumescent epoxy adhesives, designed to provide thermal runaway protection for high-energy battery packs.

With strong government support for R&D collaborations between tape, sealant, and adhesive producers, South Korea is advancing its capabilities in high-durability silicone sealants and lightweight bonding systems, reinforcing its reputation as a global EV adhesive technology hub.

Mexico’s growing role as a North American automotive manufacturing hub continues to boost the demand for cost-effective, high-volume automotive adhesives. The influx of global OEM investments in central and northern Mexico has led to a surge in locally sourced hot-melt adhesives for carpet, trim, and interior component bonding across major assembly lines.

A significant portion of vehicles produced in Mexico utilize butyl rubber sealants for Body-in-White (BIW) joint sealing, ensuring superior water, dust, and noise insulation—key requirements for export quality assurance. In addition, global adhesive suppliers have expanded converting and slitting operations within Mexico to streamline supply to the USMCA automotive corridor, reducing cross-border logistics complexity.

The modernization of local facilities is driving a shift toward water-based and hot-melt adhesive technologies, aligning Mexico’s automotive adhesive market with North American sustainability and emissions standards.

Automotive Adhesives Market Report Scope

Automotive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.9 Billion

|

|

Market Size (2034)

|

$27.6 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Silicone, Polyamide/Hot Melt, Cyanoacrylate, Others), By Technology (Reactive Adhesives, Hot Melt Adhesives, Water-Borne Adhesives, Solvent-Borne Adhesives, UV-Curing Adhesives), By Application Area (Body-in-White, Glazing, Powertrain/Under the Hood, Interior, Exterior, EV Battery Assembly), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, Hybrid Electric Vehicles), By Function (Structural Adhesives, Sealants, Thermal Management Adhesives, NVH/Acoustic Damping, Assembly Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, The Dow Chemical Company, 3M Company, Arkema S.A., Huntsman International LLC, Wacker Chemie AG, Illinois Tool Works Inc., PPG Industries, Inc., Lord Corporation, Mapei S.p.A., Ashland Global Holdings Inc., Jowat SE, Hexion Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin/Chemistry Type

- Epoxy

- Polyurethane

- Acrylic

- Silicone

- Polyamide/Hot Melt

- Cyanoacrylate

- Other

By Technology

- Reactive Adhesives

- Hot Melt Adhesives

- Water-Borne Adhesives

- Solvent-Borne Adhesives

- UV-Curing Adhesives

By Application Area

- Body-in-White

- Glazing

- Powertrain/Under the Hood

- Interior

- Exterior

- EV Battery Assembly

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Electric Vehicles

- Hybrid Electric Vehicles

By Function

- Structural Adhesives

- Sealants

- Thermal Management Adhesives

- NVH/Acoustic Damping

- Assembly Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- The Dow Chemical Company

- 3M Company

- Arkema S.A.

- Huntsman International LLC

- Wacker Chemie AG

- Illinois Tool Works Inc.

- PPG Industries, Inc.

- Lord Corporation

- Mapei S.p.A.

- Ashland Global Holdings Inc.

- Jowat SE

- Hexion Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how structural epoxies, polyurethane and acrylic systems, and silicone thermal materials are reshaping Body-in-White, glazing, interior, powertrain, and EV battery assemblies. Our analysis reviews the rapid replacement of welds and rivets with high-strength, corrosion-isolating bonds; the rise of thermally conductive gap fillers for battery safety; and the move to fast-cure, low-VOC, and recyclable chemistries that compress takt times while meeting REACH/EPA/ELV expectations. It highlights primerless LSE bonding, gigacast-ready nodal adhesives, debond-on-demand concepts for circularity, and LASD/NVH solutions that lower cabin noise without mass penalties. Capturing cost-per-vehicle impacts, quality yield, and compliance risk, this report is an essential resource for engineering, procurement, and operations leaders prioritizing lightweighting, EV readiness, throughput, and sustainability roadmaps.

Scope Includes

- By Resin/Chemistry: Epoxy; Polyurethane; Acrylic; Silicone; Polyamide/Hot Melt; Cyanoacrylate; Other

- By Technology: Reactive; Hot Melt; Water-Borne; Solvent-Borne; UV-Curing

- By Application Area: Body-in-White; Glazing; Powertrain/Under-the-Hood; Interior; Exterior; EV Battery Assembly

- By Vehicle Type: Passenger Cars; Light Commercial Vehicles; Heavy Commercial Vehicles; Electric Vehicles; Hybrid Electric Vehicles

- By Function: Structural Adhesives; Sealants; Thermal Management Adhesives; NVH/Acoustic Damping; Assembly Adhesives

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historical 2021–2024 and forecasts 2025–2034.

- Companies: 15+ company analysis/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.