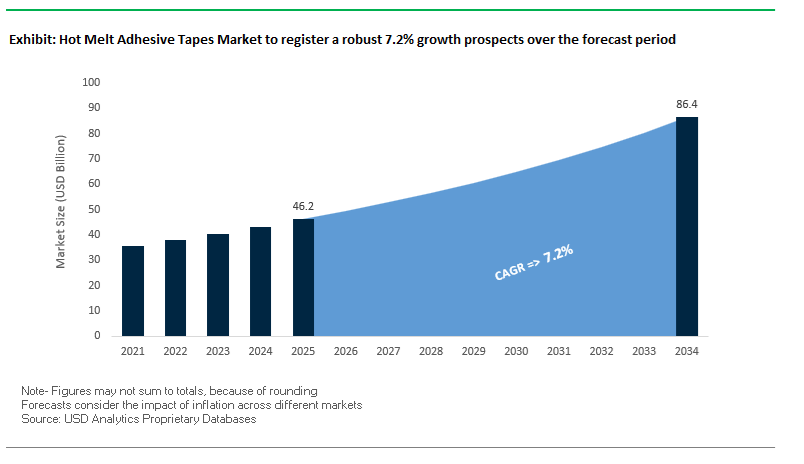

The Global Hot Melt Adhesive Tapes Market is projected to expand from USD 46.2 billion in 2025 to USD 86.4 billion by 2034, advancing at a CAGR of 7.2%, as instant-bonding solutions become fundamental to automated manufacturing and packaging modernization. Growth is structurally driven by the replacement of liquid adhesives, mechanical fastening, and solvent-based systems with hot melt pressure-sensitive adhesive (HMPSA) tapes that deliver immediate tack, predictable performance, and clean processing. In automotive interiors, high-speed packaging, construction assembly, and electronics manufacturing, HMPSA tapes are specified to support shorter takt times, consistent bond-line quality, and VOC-free operations, aligning adhesive selection directly with throughput, labor efficiency, and regulatory compliance.

Leading manufacturers such as 3M, tesa SE, Nitto Denko, Avery Dennison Performance Tapes, and Saint-Gobain are advancing polyolefin-, polyamide-, and hybrid HMPSA platforms optimized for heat resistance, creep control, and substrate versatility. Automotive applications represent a structurally important demand layer, particularly in interior trims, headliners, wire harness routing, and panel bonding, where tapes are routinely required to meet Shear Adhesion Fail Temperature (SAFT) thresholds exceeding 104°C (220°F). The transition to electric vehicles and lightweight composite structures is reinforcing this shift, with polyolefin and polyamide hot melt tapes increasingly specified for their resistance to vibration, fuels, oils, and thermal cycling—conditions that rapidly degrade conventional rubber-based systems.

Packaging and industrial assembly are reinforcing adoption through process economics rather than incremental performance gains. Packaging converters are accelerating the shift toward polyolefin-based hot melt tapes due to their fast cooling behavior, energy efficiency, and compatibility with recyclable material streams, supporting ESG objectives and VOC reduction mandates. In electronics and appliance manufacturing, polyamide hot melt tapes—including established platforms such as 3M™ 3789—are gaining traction where open times approaching 50 seconds are required to balance placement flexibility with rapid set and long-term thermal durability. Across automated carton sealing, metal fabrication, and composite assembly lines, the defining advantage of hot melt adhesive tapes remains instant set without solvent evaporation, enabling higher line speeds, reduced rework, and predictable bond performance.

The global hot melt adhesive tapes market is experiencing dynamic evolution through technological advancements, sustainability investments, and application diversification. In September 2025, Avery Dennison Performance Tapes expanded its Volt Tough portfolio, introducing pressure-sensitive adhesive (PSA) tapes engineered to prevent electrical arcing in EV batteries, directly addressing the insulation challenges in high-voltage architectures. This advancement demonstrates how adhesive innovation underpins EV battery safety and efficiency.

In October 2025, Nitto Denko Corporation launched thermal conductive tapes (TCTs) with >3.0 W/m·K conductivity, optimized for high-power electronics and data centers, signifying the convergence of adhesive technology and thermal management. Simultaneously, tesa SE (August 2025) announced a major investment in Europe to scale solvent-free acrylic and bio-based hot melt adhesive tapes, meeting ESG and carbon reduction objectives for sustainable packaging manufacturers.

The automotive segment remains a strong driver of innovation. 3M Company (July 2025) introduced low-VOC hot melt adhesives for interior applications, ensuring compliance with global air quality and EHS standards. This was followed by Bostik’s Moisture Cured PSA (MCPSA) release in May 2025, tailored for construction and exterior sealing. These solutions provide enhanced adhesion to low surface energy materials like PVC, with outstanding humidity resistance, critical for building envelopes and facade systems.

In March 2025, an Asian manufacturer secured a public infrastructure contract to supply flame-resistant hot melt tapes for mass transit wiring and insulation, highlighting safety’s growing importance in adhesive design. Meanwhile, Avery Dennison’s Cold Tough™ series (January 2025) redefined cold-weather adhesion, maintaining peel and shear strength below freezing—a breakthrough for cold chain logistics and outdoor construction.

Strategic integrations are also reshaping the supply chain. In November 2024, a European specialty chemicals company acquired a U.S.-based renewable tackifier producer, securing a bio-based raw material supply for sustainable hot melt tape formulations. At the same time, 3M’s October 2024 unveiling of robotic applicator systems showcased automation’s critical role in achieving precision coating and consistent tape performance across complex assembly lines.

The rise of heat-sensitive materials in packaging, consumer electronics, and automotive interiors is driving the innovation of hot melt adhesive tapes that bond effectively at significantly lower temperatures while maintaining exceptional heat resistance post-application. The shift toward low-temperature hot melt systems minimizes the risk of substrate warping, delamination, and discoloration, all while delivering superior adhesion and energy efficiency during production.

Recent advances in Reactive Polyurethane (PUR) Hot Melt Adhesives have expanded application temperatures as low as 50°C to 70°C (122°F–158°F), compared to the traditional 150°C range. At these reduced temperatures, these formulations initially behave as pressure-sensitive adhesives (PSAs) and subsequently undergo moisture-induced cross-linking, developing high-strength, heat-resistant bonds capable of enduring up to 150°C (302°F) service conditions. The hybrid bonding mechanism allows manufacturers to work with delicate polymer films, foams, and coated fabrics that were previously incompatible with conventional high-heat adhesives.

Leading adhesive manufacturers have capitalized on the innovation by introducing specialized low-temperature hot melt lines for film-to-foam lamination in automotive interiors, particularly for door panels, dashboards, and acoustic insulation materials. These systems can reduce application temperatures by up to 40%, enabling improved material safety, reduced energy use, and faster process throughput. For OEMs and tier suppliers in automotive and packaging, the strategic benefit lies in balancing sustainability, operational efficiency, and superior bonding performance, making low-temperature hot melts a defining technology in modern manufacturing environments.

The transition toward eco-friendly adhesive chemistries and recyclable substrates is redefining how hot melt adhesive tapes are formulated and deployed, especially within packaging, labeling, and logistics applications. Environmental regulations limiting volatile organic compounds (VOCs) and corporate sustainability initiatives are pushing adhesive developers to engineer bio-based, compostable, and recyclable hot melt tapes that align with the circular economy model.

A major advancement was reported by a specialty chemicals company that achieved 85% bio-based content in a new hot melt adhesive formulation for paper-based packaging applications. The product was certified industrially compostable, decomposing fully within 180 days—a significant milestone in reducing landfill accumulation and supporting eco-conscious packaging trends. In parallel, the industry is witnessing rapid adoption of post-consumer recycled (PCR) materials, such as rPET film backings made from up to 90% recycled polyethylene terephthalate. These sustainable substrates complement high-performance hot melt layers while maintaining mechanical strength and adhesive reliability.

The dual focus on bio-content enhancement and recyclability has reshaped tape construction methodologies. Leading packaging tape manufacturers are producing fully recyclable hot melt adhesive tapes suitable for integration into mono-material packaging systems, addressing the compatibility challenges associated with recycling mixed materials. As major FMCG brands accelerate their commitment to plastic reduction and carbon-neutral packaging, the demand for sustainable hot melt adhesive tapes is expected to surge across both industrial and consumer packaging value chains.

The rapid electrification of mobility presents one of the most lucrative frontiers for the Hot Melt Adhesive Tapes Market, particularly in battery module assembly, thermal management, and safety insulation applications. Adhesive tapes are critical for achieving dielectric protection, flame retardancy, vibration dampening, and efficient thermal conduction—all essential in the design of modern lithium-ion and solid-state EV batteries.

Recent technical advances have introduced high-conductivity acrylic adhesive tapes with thermal conductivities up to 2.0 W/mK, specifically tailored for bonding battery cells to cooling elements. The ensures optimal thermal regulation between 20°C and 35°C, preventing overheating and maintaining uniform cell performance. Concurrently, hot melt polyamide adhesives are being utilized for battery encapsulation to improve mechanical integrity and dielectric isolation, effectively minimizing the risk of short-circuiting and thermal runaway in high-density modules.

Manufacturers are leveraging these material innovations to serve the needs of EV battery OEMs, where chemical resistance, flame retardancy, and thermal management are non-negotiable. The expansion of gigafactory-scale production in Europe, North America, and Asia-Pacific is further amplifying demand for thermally stable, high-strength hot melt tapes. As the EV industry races toward lighter, safer, and more efficient architectures, hot melt adhesive tapes will remain a key enabler in achieving sustainable, high-performance battery assembly.

The explosive growth of e-commerce and automated logistics infrastructure is driving an unprecedented need for high-speed, machine-compatible hot melt adhesive tapes that can perform reliably under rapid sealing and variable environmental conditions. In automated fulfillment centers, where packaging lines exceed speeds of 100 boxes per minute, the adhesive’s set time, flexibility, and adhesion uniformity are critical performance factors.

Metallocene-based hot melt tapes have emerged as the preferred solution for modern carton-sealing systems. Their ultra-fast set time (under 1 second) ensures precise sealing even at extremely high line speeds, while maintaining strong tack and peel performance. The enables consistent packaging throughput and reduced downtime in automated operations. Additionally, their stable viscosity and controlled rheology make them ideal for robotic spray or extrusion systems, ensuring minimal clogging and uniform film deposition.

A real-world case study from the logistics sector reported that switching to high-performance hot melt tapes formulated for recycled corrugated substrates reduced sealing failure rates by 15% compared to standard pressure-sensitive acrylic tapes. The improvement is particularly valuable given the widespread use of low-quality recycled board in e-commerce, which often presents surface irregularities and dust contamination. These advantages establish hot melt adhesive tapes as a mission-critical component in achieving packaging line efficiency, sustainability compliance, and reduced material waste in the booming global e-commerce supply chain.

Hot Melt Adhesive Tapes Market Share Insights, 2025-2034

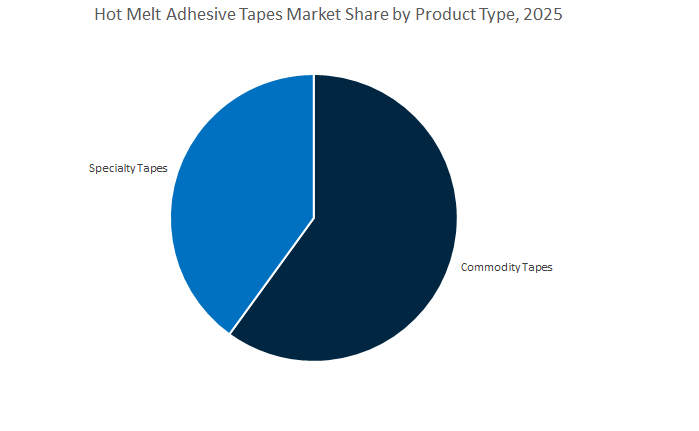

Commodity hot melt adhesive tapes dominate the global market with a projected 58.6% share in 2025, driven by their ubiquitous use across packaging, shipping, logistics, and general industrial applications. Their high-volume consumption is supported by the explosive growth in e-commerce and global trade, which fuels continuous demand for cost-efficient, reliable bonding and sealing solutions. These tapes are typically based on ethylene-vinyl acetate (EVA), rubber, or polyolefin hot melts, optimized for instant tack, peel adhesion, and long-term holding power across corrugated boxes, films, and flexible substrates. Their scalability and adaptability across manual, semi-automated, and automated packaging lines make them indispensable in fast-moving consumer goods (FMCG), electronics packaging, and retail distribution.

On the other hand, specialty hot melt adhesive tapes—accounting for 41.4% of the market—represent the value and innovation segment, serving demanding applications across automotive assembly, electronics, aerospace, and construction. These include double-sided, heat-activated, and conductive tapes that deliver superior temperature resistance, dielectric insulation, and precise bonding for complex substrates. Growth is being driven by miniaturization, lightweighting, and automation trends, which require advanced adhesive tapes capable of replacing mechanical fasteners while maintaining high reliability under dynamic stress.

Manual application methods retain the largest share of the global hot melt adhesive tapes market, estimated at 45.9% in 2025, due to their widespread use in small-to-medium enterprises, repair shops, and customized packaging operations. Manual application remains preferred where adaptability, operator precision, and versatility are valued over throughput. SMEs across logistics, retail, and maintenance sectors rely on manual dispensers and handheld applicators for cost-effective sealing and bundling solutions.

However, the machine and automated application segments are transforming the industry landscape. Machine application—employed in mid-speed production lines for automotive, appliance, and electronics manufacturing—supports consistent adhesive laydown, minimal waste, and repeatable bond quality. Meanwhile, automated systems represent the fastest-growing segment, propelled by the shift toward Industry 4.0 manufacturing, robotics integration, and high-speed packaging automation. These systems enable real-time adhesive dispensing control, inline curing, and precision placement, substantially improving operational efficiency. As manufacturers pursue productivity, labor reduction, and quality assurance, automated tape application is becoming integral to next-generation smart factories, especially in electronics, automotive, and flexible packaging.

The hot melt adhesive tapes market is highly consolidated, led by major global players—3M Company, tesa SE, Avery Dennison Corporation, Bostik (Arkema Group), and Nitto Denko Corporation—each leveraging distinct technological strengths across industrial bonding, thermal management, EV, and packaging applications. Their strategies emphasize low-VOC compliance, automation integration, and sustainability-driven chemistry reformulation.

3M stands as a global leader in hot melt adhesives (HMAs), delivering polyamide and polyolefin formulations with shear strength above 500 psi, essential for structural bonding and high-speed production lines. Its flagship Scotch-Weld™ series provides fast-setting 100% solid resins, minimizing fixturing time and enabling rapid assembly in metal fabrication and packaging automation. The firm’s continuous investment in low-temperature melt adhesives (121°C/250°F) expands applications in heat-sensitive plastics and foams, enhancing safety and process adaptability in automotive interiors and consumer goods.

tesa SE continues to redefine the European adhesive tape landscape, with 20% of its portfolio developed within the last five years, underscoring its innovation pace. The company produces ultra-thin double-sided tapes (≤3 µm) for smartphone displays and microelectronics, leveraging UV-curable and solvent-free hot melt formulations. Its strong sustainability focus includes replacing solvent-based technologies with bio-acrylic and hot melt systems, drastically reducing CO₂ emissions. For industrial converters, tesa offers film and transfer tapes optimized for LSE substrates, ensuring high productivity and minimal waste in precision assembly.

Avery Dennison delivers one of the most comprehensive Pressure-Sensitive Adhesive (PSA) portfolios, addressing performance-critical needs in automotive, medical, and construction sectors. Its Core Series™ Portfolio simplifies industrial selection, spanning rubber-based to high-performance hot melt systems. In EV manufacturing, Avery Dennison’s specialized PSA tapes enable battery cell wrapping, NVH damping, and insulation. The Cold Tough™ line, launched in January 2025, offers superior low-temperature performance for roofing and exterior applications, expanding the brand’s dominance in both industrial and specialty adhesive markets.

Bostik combines Arkema’s polymer chemistry expertise with market-driven innovation in Hot Melt Pressure Sensitive Adhesives (HMPSA). Its fast-set systems dominate the disposable hygiene market, ensuring bonding reliability in baby care and medical applications. The company’s Silyl Modified Polymer (SMP) and high-tack HMPSA technologies deliver excellent adhesion to LSE plastics and coated materials, vital for construction sealing and assembly lines. With 100% solids formulations, Bostik minimizes curing time, optimizing productivity in high-speed tape manufacturing.

Nitto Denko is a leader in functional hot melt adhesive tapes for electrical, electronic, and automotive sectors. Its advanced thermal conductive tapes (>3.0 W/m·K) are crucial for battery pack and semiconductor assembly, offering flame resistance and insulation under extreme conditions. The company’s innovation in Fiber PSA technology—combining non-woven flexibility with hot melt adhesion—positions it at the forefront of next-gen display and flexible electronics manufacturing. Nitto’s adhesive tapes withstand temperatures up to 200°C (392°F), ensuring reliability in automotive wire harnesses and industrial protection systems.

China dominates the global hot melt adhesive tapes market due to its unparalleled manufacturing scale, strong e-commerce ecosystem, and government policies supporting low-emission adhesive technologies. The country's booming packaging and logistics sectors, coupled with rapid industrial expansion, have positioned it as the largest producer and consumer of hot melt adhesive materials globally.

Zhuhai Yongsheng, a subsidiary of Dongjiang Environmental, has notably expanded its hot melt adhesive pellet processing capacity from 3–5 tons/day to 15–18 tons/day, reinforcing China's dominance in adhesive materials manufacturing. The scale-up supports both domestic industrial consumption and export-oriented demand for packaging and construction adhesives. In R&D, local researchers have introduced a photoanionic curing system for Pressure Sensitive Adhesives (PSAs) that achieves full curing under UV exposure in just two hours, enhancing production efficiency and energy savings for electronic and industrial applications.

China’s semiconductor and electronics industries are increasingly adopting high-temperature-resistant PSAs that can withstand up to 220°C, making them ideal for temporary bonding during semiconductor packaging and precision electronics assembly. Additionally, government-backed environmental policies from the 12th Five-Year Plan continue to incentivize low-VOC and solvent-free adhesive systems, encouraging domestic firms to switch to more sustainable hot melt solutions.

The hygiene products sector is another major growth engine, with SBS/SIS-based hot melts widely used in diapers and adult care products. The adhesives provide elasticity and softness, critical for consumer comfort. Combined, The factors make China the epicenter for high-volume, sustainable, and technology-driven production in the global hot melt adhesive tapes landscape.

The U.S. hot melt adhesive tapes industry is a pioneer in advanced formulations, precision applications, and sustainability-led product innovation. As a mature market with strong regulatory oversight, U.S. manufacturers are focusing on low-emission, recyclable, and water-resistant hot melt adhesive solutions for diverse industrial end-uses.

A major North American producer recently launched water-resistant hot melt adhesive tapes, targeting industries that require high humidity tolerance, such as construction, marine, and outdoor packaging. Another leading U.S. manufacturer introduced a new generation of high-performance hot melt tapes engineered for industrial bonding, flexible packaging, and labeling applications, offering superior peel adhesion and cohesive strength even under variable temperature conditions.

In the electronics sector, reactive hot melt adhesives (RHMAs) are gaining traction for smartphones, smartwatches, and wearables, as they combine heat resistance, chemical stability, and moisture protection. The trend is complemented by automotive OEMs increasingly integrating reactive polyolefin-based hot melts, which simplify vehicle disassembly for recycling, directly aligning with U.S. circular economy mandates and end-of-life vehicle directives.

Furthermore, a global chemical company has expanded its Sparta, Wisconsin manufacturing plant, adding capacity for strapping tapes and acrylic adhesives, catering to the healthcare and industrial sectors.

Germany stands at the forefront of European hot melt adhesive technology, driven by its engineering precision, environmental stewardship, and focus on dual-cure and specialty adhesive systems. The German market’s growth is fueled by increasing applications in technical textiles, furniture manufacturing, and industrial lamination, supported by a strong network of chemical innovation and sustainable material sourcing.

A notable development comes from a German specialty chemical firm that patented a dual-cure polyurethane hot melt adhesive—a breakthrough formulation that combines silane-modified acrylates and isocyanate crosslinking to deliver exceptional chemical and heat resistance. The advanced chemistry is particularly advantageous for technical textile lamination, providing durability against washing cycles, thermal exposure, and chemical stress in industrial and automotive fabrics.

German manufacturers are also advancing polyolefin (PO) hot melt adhesives, prized for their high heat resistance and fast setting time, which are essential for furniture applications, especially in kitchen and modular cabinetry. On the sustainability front, European producers are integrating bio-refinery-sourced renewable waxes and resins into adhesive formulations to reduce CO₂ emissions and the fossil dependency of traditional petrochemical hot melts.

The balance of technological innovation and environmental compliance positions Germany as a global reference point for sustainable adhesive production, aligned with the European Green Deal and circular economy objectives. The nation’s continuous push toward non-isocyanate and low-VOC technologies makes it a leader in next-generation eco-efficient hot melt adhesive systems.

Japan’s hot melt adhesive tapes industry is defined by precision engineering, advanced material science, and long-term innovation in specialty formulations. With an emphasis on electronics miniaturization and high-spec automotive assembly, Japanese manufacturers continue to deliver cutting-edge adhesive solutions with unmatched performance and reliability.

Industry giants such as Nitto Denko Corporation and LINTEC Corporation are driving R&D advancements in pressure-sensitive and thermally stable hot melts, tailored for complex electronic device assembly, optical bonding, and automotive component manufacturing. Japanese firms emphasize dielectric strength, electrical insulation, and low-outgassing properties, crucial for the high reliability required in next-generation consumer electronics.

R&D initiatives are also targeting high-temperature and oxidation-resistant hot melts, supporting automotive electrification and hybrid vehicle manufacturing. The adhesives maintain structural integrity in thermal cycling environments, making them ideal for battery pack sealing, under-hood electronics, and advanced EV sensor systems.

The country’s manufacturing excellence and focus on precision dispensing technologies ensure consistent adhesive application, reducing material waste while maintaining micro-scale accuracy. Japan’s unique blend of technological depth, quality assurance, and innovation in polymer science keeps it at the forefront of high-performance hot melt adhesive development across Asia-Pacific.

Hot Melt Adhesive Tapes Market Report Scope

Hot Melt Adhesive Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$46.2 Billion

|

|

Market Size (2034)

|

$86.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Adhesive Resin Type (Rubber-based, Acrylic-based, Silicone-based, Ethylene-Vinyl Acetate, Styrenic Block Copolymers, Hot-Melt Polyurethane Adhesive, Amorphous Poly Alpha Olefin, Others), By Backing Material (Polypropylene, Polyethylene Terephthalate/Polyester, Paper, Cloth/Fabric, Polyvinyl Chloride, Foam, Foil, Others), By Product Type (Commodity Tapes, Specialty Tapes), By Application Method (Manual Application, Machine Application, Automated Systems), By End-User Industry (Packaging, Automotive and Transportation, Building and Construction, Electrical and Electronics, Consumer Goods and DIY, Healthcare and Hygiene, Woodworking and Furniture, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Avery Dennison Corporation, tesa SE, Sika AG, Jowat SE, Arkema Group, Intertape Polymer Group Inc., Nitto Denko Corporation, LINTEC Corporation, Scapa Group Plc, Shurtape Technologies, LLC, ExxonMobil Corporation, Dow Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Adhesive Resin Type

- Rubber-based

- Acrylic-based

- Silicone-based

- Ethylene-Vinyl Acetate

- Styrenic Block Copolymers

- Hot-Melt Polyurethane Adhesive

- Amorphous Poly Alpha Olefin

- Others

By Backing Material

- Polypropylene

- Polyethylene Terephthalate/Polyester

- Paper

- Cloth/Fabric

- Polyvinyl Chloride

- Foam

- Foil

- Others

By Product Type

- Commodity Tapes

- Specialty Tapes

By Application Method

- Manual Application

- Machine Application

- Automated Systems

By End-User Industry

- Packaging

- Automotive and Transportation

- Building and Construction

- Electrical and Electronics

- Consumer Goods and DIY

- Healthcare and Hygiene

- Woodworking and Furniture

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Avery Dennison Corporation

- tesa SE

- Sika AG

- Jowat SE

- Arkema Group

- Intertape Polymer Group Inc.

- Nitto Denko Corporation

- LINTEC Corporation

- Scapa Group Plc

- Shurtape Technologies, LLC

- ExxonMobil Corporation

- Dow Inc.

*- List not Exhaustive

Research Coverage

Built for packaging, automotive, construction, and electronics decision-makers, the USDAnalytics study on the Hot Melt Adhesive Tapes Market delivers an executive-to-engineering view of where hot-melt pressure-sensitive technologies win on speed, line uptime, and multi-substrate adhesion. Specifically, this report investigates how resin choices, backing architectures, and application methods translate into bond reliability across LSE plastics, metals, foams, and recycled boards; tracks breakthroughs in low-temperature application systems, thermal-conductive tapes, and bio-based/recyclable constructions; analysis reviews regulatory and ESG momentum alongside automation-ready dispensing and robotics; and highlights the implications for EV battery safety, high-speed e-commerce packaging, and precision electronics assembly. Designed to de-risk specifications and capex decisions, this report is an essential resource for CTOs, procurement leaders, converters, and process engineers who need evidence-backed guidance on performance, compliance, and total cost of ownership, etc……

Scope Highlights

Segmentation

- By Adhesive Resin Type: Rubber-based; Acrylic-based; Silicone-based; Ethylene-Vinyl Acetate; Styrenic Block Copolymers; Hot-Melt Polyurethane Adhesive; Amorphous Poly Alpha Olefin; Others

- By Backing Material: Polypropylene; Polyethylene Terephthalate/Polyester; Paper; Cloth/Fabric; Polyvinyl Chloride; Foam; Foil; Others

- By Product Type: Commodity Tapes; Specialty Tapes

- By Application Method: Manual Application; Machine Application; Automated Systems

- By End-User Industry: Packaging; Automotive & Transportation; Building & Construction; Electrical & Electronics; Consumer Goods & DIY; Healthcare & Hygiene; Woodworking & Furniture; Others

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: 15+ company analyses/profiles included (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.