Polymer Innovation, Controlled Drug Delivery, and Regulatory Shifts Driving Stable Growth

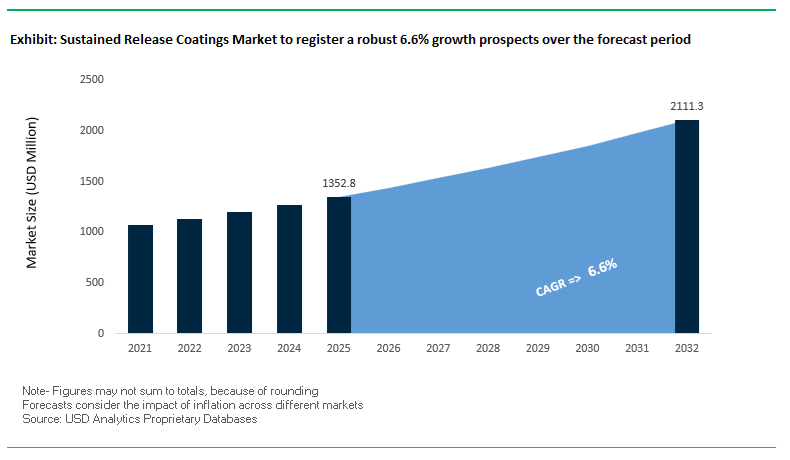

The global Sustained Release Coatings Market is expanding steadily, supported by increasing demand for controlled drug delivery systems, improved patient compliance, and advanced pharmaceutical formulations. The market was valued at $1,352.8 million in 2025 and is projected to reach $2,116.1 million by 2032, growing at a CAGR of 6.6% during 2025–2032. This growth is primarily driven by the pharmaceutical industry’s shift toward once-daily dosing, targeted drug release, and enhanced bioavailability, particularly in chronic disease management such as cardiovascular, diabetes, and central nervous system disorders.

A core structural driver is the rising use of polymer-based coating technologies, including ethylcellulose, hypromellose (HPMC), polyvinyl alcohol (PVA), and alginates, which enable precise control over drug release kinetics. These coatings form barrier layers around active pharmaceutical ingredients (APIs), allowing for gradual diffusion or delayed dissolution, thereby optimizing therapeutic outcomes and reducing side effects. The increasing adoption of plant-based and bio-derived excipients is further shaping the market, aligning with regulatory and sustainability preferences.

Another significant growth factor is the integration of multi-functional coating systems that combine sustained release with moisture protection, light shielding, and anti-counterfeiting features. As pharmaceutical products become more complex and high-value, manufacturers are prioritizing coatings that ensure stability, safety, and product integrity throughout the supply chain. Additionally, the rise of personalized medicine and complex drug formulations is driving demand for customizable coating solutions capable of delivering precise release profiles.

Regulatory changes are also playing a pivotal role, particularly in Europe and North America, where restrictions on materials such as Titanium Dioxide (TiO₂) are accelerating innovation in alternative coating systems. This is pushing manufacturers toward high-opacity, compliant formulations that maintain performance without relying on restricted substances.

Market Analysis: Pharma Portfolio Consolidation, Functional Packaging Integration, and Polymer Supply Chain Expansion Reshaping Market Dynamics

The sustained release coatings market is undergoing significant transformation driven by strategic acquisitions, supply chain optimization, and innovation in polymer chemistry and functional packaging systems. In March 2026, Roquette launched its “Shift & Lead” strategy following the acquisition of IFF Pharma Solutions, positioning itself as a global leader in plant-based excipients and sustained-release coating materials. This move integrates critical polymers such as ethylcellulose and hypromellose, strengthening Roquette’s ability to deliver advanced controlled-release solutions at scale.

The July 2025 divestiture of IFF’s Pharma Solutions business to Roquette represents a major consolidation event, transferring globally recognized brands such as ETHOCEL™ and METHOCEL™, which are foundational to sustained-release coating technologies. This acquisition significantly enhances Roquette’s R&D capabilities and global manufacturing footprint.

Supply chain and distribution optimization are also key focus areas. Evonik’s February 2026 restructuring of its North American distribution network improves access to specialized additives used in pharmaceutical coatings, ensuring consistent supply and enhanced technical support for manufacturers.

Material innovation is being driven by regulatory compliance and sustainability demands. Colorcon’s Opadry® Titanium Dioxide-free coating system (2024–2025 update) provides high-opacity, light-protective coatings for sustained-release tablets, addressing regulatory uncertainty while maintaining processing efficiency. Additionally, BASF’s January 2026 strategic divestments allow the company to focus on high-value nutrition and care additives, including advanced materials for controlled-release applications.

Functional packaging integration is emerging as a critical differentiator. Colorcon’s HAT®-B Handy Active Tube expansion (2026) and its earlier acquisition of a functional packaging business (January 2024) enable a “full system” approach, combining coating technologies with moisture-control packaging to preserve drug stability and release profiles throughout the product lifecycle.

Upstream supply chain investments are also strengthening market resilience. Shin-Etsu Chemical’s multi-billion-dollar investment in PVC and caustic soda production (2025–2026) secures the availability of key intermediates required for cellulose-based polymers, ensuring stable production of sustained-release coating materials.

Innovation is also extending into anti-counterfeiting and smart coating technologies. BASF’s “Driving the Proxy” pigment innovations (October 2025), while initially developed for automotive applications, are being adapted for pharmaceutical coatings to create visually complex, difficult-to-replicate surfaces, enhancing drug security.

Leadership changes are further accelerating strategic execution. Roquette’s appointment of Thierry Fournier as CEO (July 2025) underscores the company’s commitment to rapidly commercializing next-generation sustained-release polymers and strengthening its position in high-growth pharmaceutical segments.

Market Trend: USP <1790> and USP <790> Revisions Elevate Precision Requirements for Functional Coating Uniformity

The sustained release coatings industry is entering a phase of heightened precision control as the United States Pharmacopeia strengthens guidance on coating uniformity in solid oral dosage forms. The evolving alignment between USP <1790> and USP <790> reflects a shift from purely visual inspection toward quantitative performance validation of functional coatings, particularly in preventing dose dumping in sustained release formulations. Advanced dissolution studies conducted in 2026 demonstrate that even minor deviations in coating thickness, as low as 5 microns, can induce a 15% to 20% variation in drug release kinetics, specifically impacting T80% parameters. This level of sensitivity is driving the adoption of high-resolution spray monitoring systems and real-time process analytical technologies within coating operations. Additionally, under updated Quality by Design frameworks, manufacturers are required to maintain a weight gain variation coefficient below 2% across large-scale batches, often exceeding 500 kilograms. This benchmark enforces strict inter-tablet uniformity, particularly for high-potency active pharmaceutical ingredients where dosing precision is critical. As regulatory expectations converge toward quantitative reproducibility and process control, coating uniformity is becoming a defining quality attribute in sustained release drug delivery systems.

Market Trend: FDA 2026 Guidance Reclassifies Functional Coating Defects as Critical Quality Failures

The U.S. Food and Drug Administration’s updated guidance on quality attribute monitoring is significantly increasing scrutiny on functional coating integrity in sustained release products. Defects that were previously categorized as cosmetic, such as pinholes, cracking, and delamination, are now formally recognized as critical quality failures due to their direct impact on drug release profiles and therapeutic efficacy. Under 2026 inspection protocols, a defect rate as low as 0.5% within a batch can trigger an Official Action Indicated classification, reflecting the agency’s zero-tolerance approach to risks associated with premature drug exposure. This regulatory tightening is compelling manufacturers to enhance in-process inspection technologies, including automated vision systems and defect detection algorithms capable of identifying sub-millimeter irregularities. Furthermore, the FDA has introduced more stringent stability requirements, mandating that the mean dissolution time of sustained release products must not deviate by more than 10% over a 24-month accelerated aging period under conditions of 40°C and 75% relative humidity. These requirements emphasize the need for robust polymer film formation and long-term structural stability, particularly in formulations sensitive to environmental conditions. As compliance thresholds tighten, defect minimization and stability assurance are becoming central pillars of sustained release coating development.

Market Opportunity: Aqueous Ethylcellulose Dispersions Drive Sustainable and High-Precision Multiparticulate Coating Systems

Aqueous ethylcellulose dispersions are emerging as a leading solution in sustained release coating technologies, particularly for multiparticulate dosage forms such as pellets and granules. The shift away from solvent-based coating systems is being driven by both environmental regulations and the need to eliminate residual solvent risks in pharmaceutical manufacturing. Aqueous systems enable a reduction in coating process times by 30% to 40% in fluidized bed equipment, provided that post-coating curing conditions, typically around 60°C for two hours, are carefully controlled to ensure film coalescence and stability. These dispersions are particularly effective for coating small particles in the 200 to 500 micron range, delivering uniform barrier layers that maintain drug loading efficiencies above 95% while supporting controlled release profiles extending up to 24 hours. From a sustainability perspective, the elimination of organic solvents such as ethanol and isopropanol results in a 90% reduction in volatile organic compound emissions, aligning with evolving environmental compliance requirements in pharmaceutical production. As manufacturers seek to balance performance, scalability, and regulatory compliance, aqueous ethylcellulose coatings are becoming a cornerstone technology in advanced sustained release formulations.

Market Opportunity: pH-Independent Sustained Release Coatings Enhance Bioavailability for Weakly Basic Drug Molecules

The development of pH-independent sustained release coatings is addressing a critical challenge in drug delivery for weakly basic compounds, which exhibit variable solubility across the gastrointestinal tract. These coatings utilize optimized combinations of permeable and non-permeable polymers, such as ammonium methacrylate copolymers and ethylcellulose-hydroxypropyl methylcellulose blends, to maintain consistent drug diffusion regardless of environmental pH. In 2026, advanced formulations demonstrate release rate variability of less than 8% across a pH range of 1.2 to 6.8, ensuring stable therapeutic performance in diverse patient populations, including those undergoing proton pump inhibitor therapy. This stability in dissolution kinetics translates into improved pharmacokinetic profiles, with reductions in peak-to-trough concentration ratios of up to 35%, thereby minimizing side effects associated with rapid drug absorption. Precise control over polymer ratios allows formulators to fine-tune lag times within a tolerance of plus or minus 15 minutes, enabling targeted release profiles tailored to specific therapeutic needs. As the pharmaceutical industry continues to focus on patient-centric drug delivery and bioavailability optimization, pH-independent coating systems represent a significant innovation opportunity within the sustained release coatings market.

Sustained Release Coatings Market Share and Segmentation Insights: Dominance of Acrylic Polymer Systems and Pharmaceutical End-Use Applications

By Polymer Material Type: Acrylic Polymers and Copolymers Leading with 38% Share Driven by Controlled Drug Release Efficiency

Acrylic polymers and copolymers accounted for 38% of the sustained release coatings market share in 2025, establishing them as the leading material segment due to their superior pH-independent drug release capabilities. Widely used grades such as Eudragit® enable consistent controlled release across varying gastrointestinal conditions, making them indispensable in oral solid dosage formulations. The segment is further strengthened by increasing demand from generic pharmaceutical manufacturers, particularly as patent expirations accelerate global generic drug production. Acrylic-based sustained release coatings offer proven reliability in both matrix and reservoir drug delivery systems, supporting annual growth exceeding 6%. This positions acrylic polymers as a cornerstone in advanced drug delivery coatings and pharmaceutical excipient technologies.

By End-User Industry: Pharmaceutical Sector Capturing 74% Share Amid Rising Demand for Controlled-Release Drug Delivery Systems

The pharmaceutical industry dominated the sustained release coatings market in 2025, capturing a substantial 74% share, driven by the widespread adoption of controlled-release drug delivery systems. More than 60% of newly approved drugs targeting chronic conditions such as diabetes, hypertension, and central nervous system disorders incorporate sustained release coatings to enhance patient compliance and reduce dosing frequency. Additionally, the industry is transitioning toward multiparticulate drug delivery systems, including coated pellets and beads, which require highly precise spray-coating technologies using acrylic and cellulosic polymers. This shift is significantly boosting demand for high-performance sustained release coating materials, reinforcing the pharmaceutical sector’s leadership in the global market.

Sustained Release Coatings Market Competitive Landscape Driven by Functional Excipients and Precision Drug Delivery Technologies

The sustained release coatings market is evolving rapidly, driven by demand for controlled release drug delivery, biocompatible polymers, and solvent-free coating systems. Leading players are focusing on excipient innovation, precise kinetic control, and scalable pharmaceutical coating technologies to enhance bioavailability, patient compliance, and manufacturing efficiency.

IFF Pharma Solutions Leads Controlled Release Innovation with Advanced Cellulose Polymer Portfolio

International Flavors & Fragrances Inc. maintains a dominant position in the sustained release coatings market through its extensive portfolio of cellulose-based excipients and polyethylene oxide polymers. Its flagship products, METHOCEL™ (HPMC), ETHOCEL™ (ethylcellulose), and POLYOX™ (PEO), are widely used in matrix tablets and osmotic drug delivery systems for precise release kinetics. In 2025, the company launched the “Timing is Everything” platform to optimize dosing frequency and improve patient adherence in controlled release formulations. By early 2026, IFF advanced its excipient engineering capabilities to deliver more predictable release profiles in complex solid dosage forms. With over 70 years of expertise and a global innovation network, IFF provides customized drug delivery solutions across multiple therapeutic categories. This strong foundation reinforces its leadership in pharmaceutical excipients and sustained release technologies.

Colorcon Advances Patient-Centric and Talc-Free Film Coatings for Optimized Drug Delivery Performance

Colorcon is a key player in functional coating systems, offering comprehensive solutions for immediate, enteric, and sustained release formulations. The company’s coating technologies enhance tablet stability, appearance, and functional performance while ensuring consistent drug release profiles. In 2026, Colorcon has been at the forefront of transitioning the industry toward talc-free film coatings, aligning with evolving global regulatory and safety standards. Its strategic focus on patient-centric design includes developing coatings that improve swallowability without compromising sustained release mechanisms. Colorcon’s ready-to-use coating systems streamline pharmaceutical manufacturing by reducing preparation time and minimizing process variability. This operational efficiency and regulatory alignment position the company strongly in the global drug formulation market.

Evonik Strengthens Targeted Drug Delivery with EUDRAGIT® and Digitalized Coating Solutions

Evonik Industries AG is a leading innovator in sustained release coatings through its EUDRAGIT® polymer platform, enabling precise pH-dependent and time-controlled drug release. In 2026, Evonik optimized its North American distribution network by appointing specialized partners, enhancing supply chain resilience and technical support. Its Custom Solutions segment generated €5.4 billion in 2025, reflecting strong demand for pharmaceutical excipients and coating additives. The company excels in tailor-made polymer systems that enable targeted drug release in specific regions of the gastrointestinal tract, critical for chronic disease therapies. Evonik is also integrating digital tools to provide real-time formulation support and customer engagement. This combination of advanced polymer science and digitalization strengthens its competitive position in precision drug delivery systems.

Ashland Expands Biobased and High-Performance Rheology Modifiers for Sustainable Coating Systems

Ashland Inc. is advancing its role in the sustained release coatings market through specialty additives and rheology modifiers that enhance coating performance and sustainability. The company reported $482 million in Q2 2026 sales, with its Specialty Additives segment returning to growth driven by market share gains. Ashland’s innovation strategy emphasizes environmentally friendly solutions, including biobased defoamers (drewplus™) and low-VOC additives. In pharmaceutical applications, its natrosol™ (HEC) products are widely used to control viscosity and optimize drug release characteristics in aqueous coating systems. The company’s “globalize and innovate” strategy has accelerated R&D output and product development. This focus on sustainability and performance positions Ashland as a key supplier of advanced coating excipients.

BASF Strengthens Polymer Supply Chain and Sustainable Chemistry for Pharmaceutical Coatings

BASF SE plays a critical role in the sustained release coatings market by supplying high-purity polymers and chemical intermediates essential for controlled release systems. Under its “Winning Ways” strategy, BASF is driving green transformation through operational efficiency and leadership restructuring in 2026. The company’s $1 billion MDI expansion in Geismar and the successful launch of the Zhanjiang Verbund site significantly enhance its global production capabilities. These investments support the growing demand for pharmaceutical coating materials in Asia-Pacific and other high-growth regions. BASF’s vertically integrated manufacturing ensures consistent quality and performance of excipients used in sustained release formulations. This strong supply chain control and sustainability focus reinforce its position as a foundational player in pharmaceutical coating technologies.

United States Leading Advanced Drug Delivery and PFAS-Free Medical Coatings Innovation

The United States dominates the sustained-release coatings market, driven by strong R&D capabilities and increasing demand for advanced drug delivery systems. Regulatory developments from the FDA (CDER, 2026) are tightening controls on excipient purity, particularly focusing on reducing residual solvents in pharmaceutical coatings, accelerating the shift toward safer formulations.

Technological advancements include AI-optimized coating thickness for 3D-printed tablets, enabling personalized drug release aligned with patient circadian rhythms. Product innovations such as stimuli-responsive pH-dependent polymers with dual-pulse release mechanisms are improving treatment outcomes for chronic diseases. Significant investments in PFAS-free coating facilities and expansion of aqueous ethylcellulose dispersion technologies are strengthening domestic production. Additionally, applications such as antimicrobial sustained-release coatings for orthopedic implants highlight the growing role of coatings in long-term therapeutic delivery.

China Advancing Regulatory Harmonization and High-Volume Generic Sustained-Release Coatings

China is rapidly evolving in the sustained-release coatings market, shifting from bulk manufacturing to high-value specialty coatings aligned with global standards. Regulatory updates such as GB 4806.10-2025 are enforcing stricter migration limits, improving safety for coatings used in pharmaceuticals, food-contact packaging, and nutraceuticals.

Government initiatives under Healthy China 2030 are boosting domestic production of sustained-release generics, particularly for chronic conditions like hypertension. Technological advancements include nano-clay reinforced polymer matrices that enhance moisture barrier performance without increasing coating thickness. Product innovations such as color-changing coatings for medication adherence are improving patient compliance. Additionally, the large-scale adoption of enteric sustained-release coatings in probiotics highlights China’s growing role in functional healthcare applications.

Germany Leading Sustainable Bio-Polymer Coatings and Precision Drug-Eluting Systems

Germany is at the forefront of the sustained-release coatings industry, driven by its focus on sustainability and precision engineering. Investments in high-automation manufacturing facilities powered by renewable energy are reducing the carbon footprint of coating production.

Technological advancements include the development of biodegradable carboxymethylcellulose (CMC) binders, offering fully bio-based alternatives without compromising mechanical performance. Product innovations such as hybrid rapid-to-sustained release coating systems are improving dosage flexibility, particularly for geriatric patients. Regulatory frameworks under EU sustainability mandates are driving the adoption of digital product passports for traceability. Key applications include drug-eluting stent coatings, where Germany leads in precision spray-coating technologies for controlled therapeutic delivery.

India Emerging as a Global Hub for Pharmaceutical Coating Manufacturing and Export

India is rapidly becoming a global powerhouse in the sustained-release coatings market, supported by strong pharmaceutical manufacturing capabilities and government incentives. Programs such as the PLI Scheme 2.0 (2026) are encouraging domestic production of key coating precursors, reducing reliance on imports.

Technological advancements include the implementation of continuous fluid-bed coating processes, significantly improving efficiency and reducing processing time. Strategic collaborations between global and domestic players are strengthening the production of ethylcellulose polymers for sustained-release formulations. Product innovations such as natural coating resins derived from plant-based materials are gaining traction in the nutraceutical sector. High-volume applications, including multi-unit particulate systems (MUPS) for diabetes treatments, highlight India’s critical role in global pharmaceutical supply chains.

Japan Driving Precision Nano-Coatings for Medical Devices and Aging Population Needs

Japan is a global leader in precision sustained-release coatings, focusing on high-quality applications in healthcare and medical devices. Technological advancements include the development of ultra-thin nanolayer coatings for pharmaceutical packaging, which incorporate sustained-release antioxidants to extend shelf life.

Regulatory updates from the PMDA (2026) are enforcing stricter safety and durability testing for multi-drug coatings. Product innovations such as ultra-thin sustained-release barriers for fast-dissolving tablets are improving therapeutic efficiency while maintaining extended release profiles. Additionally, the development of piezo-responsive coatings that release drugs upon mechanical triggers is opening new opportunities in wearable medical devices. Applications in elder-care infrastructure, including antimicrobial sustained-release coatings, highlight Japan’s focus on healthcare innovation for aging populations.

Brazil Leveraging Bio-Based Chemistry for Agricultural and Veterinary Sustained-Release Coatings

Brazil is emerging as a key player in the sustained-release coatings market, leveraging its strong agricultural base and bio-chemistry expertise. Investments in innovation centers are supporting the development of bio-based surfactants and coating materials for controlled-release applications.

Technological advancements include lignin-based sustained-release coatings that provide extended nutrient delivery in agricultural applications, improving efficiency and reducing environmental impact. Product innovations such as smart biocide-releasing coatings are enhancing durability in industrial and architectural surfaces. Government initiatives like Agro-Tech 2026 are promoting the adoption of coated fertilizers to reduce nutrient loss. Additionally, Brazil’s dominance in veterinary sustained-release coatings, particularly for livestock health management, highlights its importance in global agricultural and pharmaceutical applications.

Sustained Release Coatings Market Report Scope

Sustained Release Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1352.8 Million

|

|

Market Size (2032)

|

$2116.1 Million

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Polymer Material Type (Cellulosic Derivatives, Acrylic Polymers and Copolymers, Vinyl Polymers, Polyethylene Glycol, Polysaccharides, Other Materials), By Substrate (Tablets, Capsules, Multiparticulates, Pills, Seeds and Fertilizers), By Technology (Diffusion-Controlled Systems, Erosion-Controlled Systems, Osmotic-Pump Systems, pH-Responsive, Biodegradable), By End-User Industry (Pharmaceuticals, Agriculture, Food and Nutraceuticals, Animal Health and Veterinary, Personal Care and Cosmetics), By Application Environment (In Vivo, In Vitro), By Sales Channel (Direct Sales, Contract Manufacturing Organizations, Specialized Chemical and Excipient Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Colorcon, Evonik Industries AG, BASF SE, Ashland Inc., Merck KGaA, Coating Place, Inc., Eastman Chemical Company, JRS PHARMA, Shin-Etsu Chemical Co., Ltd., Panchsheel Organics Ltd., G.M. Chemie Pvt. Ltd., Spraycel Coatings, Panacea Biotec, SPI Pharma, Nippon Soda Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sustained Release Coatings Market Segmentation

By Polymer Material Type

- Cellulosic Derivatives

- Acrylic Polymers and Copolymers

- Vinyl Polymers

- Polyethylene Glycol

- Polysaccharides

- Other Materials

By Substrate

- Tablets

- Capsules

- Multiparticulates

- Pills

- Seeds and Fertilizers

By Technology

- Diffusion-Controlled Systems

- Erosion-Controlled Systems

- Osmotic-Pump Systems

- pH-Responsive

- Biodegradable

By End-User Industry

- Pharmaceuticals

- Agriculture

- Food and Nutraceuticals

- Animal Health and Veterinary

- Personal Care and Cosmetics

By Application Environment

By Sales Channel

- Direct Sales

- Contract Manufacturing Organizations

- Specialized Chemical and Excipient Distributors

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Sustained Release Coatings Industry

- Colorcon

- Evonik Industries AG

- BASF SE

- Ashland Inc.

- Merck KGaA

- Coating Place, Inc.

- Eastman Chemical Company

- JRS PHARMA

- Shin-Etsu Chemical Co., Ltd.

- Panchsheel Organics Ltd.

- G.M. Chemie Pvt. Ltd.

- Spraycel Coatings

- Panacea Biotec

- SPI Pharma

- Nippon Soda Co., Ltd.

*- List not Exhaustive