Bioplastics Market Size & Growth Forecasts

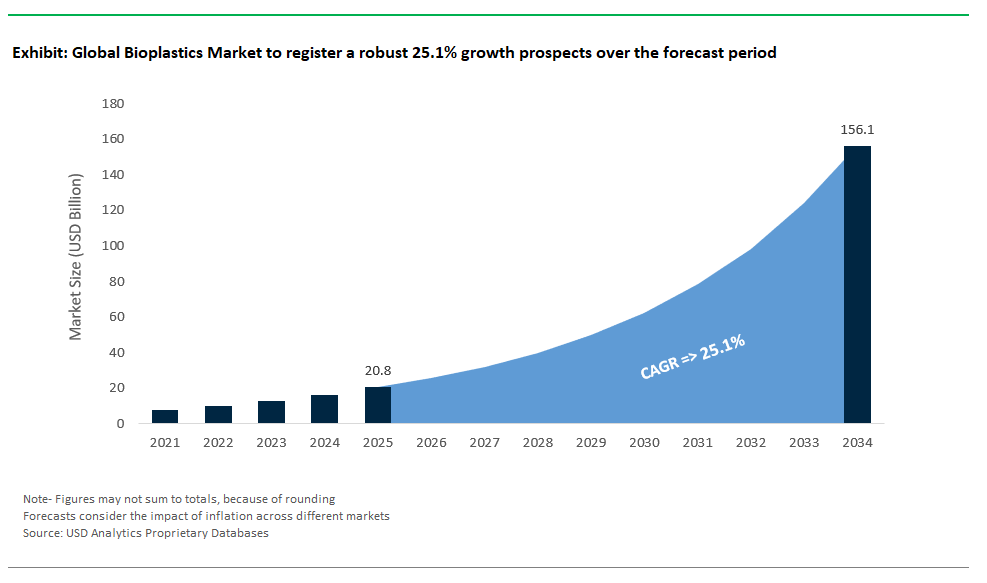

The Global Bioplastics Market is undergoing a dramatic transformation between 2025 and 2034, powered by the rapid shift from conventional plastics to sustainable, renewable alternatives across diverse end-use industries. Market analysts forecast a remarkable expansion at a CAGR of 25.1%, with the global bioplastics market expected to soar from USD 20.8 billion in 2025 to a staggering USD 156.1 billion by 2034. This exceptional growth trajectory is being driven by robust regulatory support, accelerating consumer demand for green materials, technological breakthroughs in polymer science, and the widespread adoption of bioplastics in packaging, medical, automotive, and textile applications.

Drawing on proprietary intelligence from USDAnalytics, the latest edition offers a rigorous evaluation and future outlook for the global bioplastics market, profiling developments in over 25 countries and examining the strategies of more than 20 leading companies By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others), By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others), By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others).

This report provides a comprehensive analysis of the global bioplastics market, delving into the trends and innovations reshaping the sector through 2034. It offers in-depth coverage of both biodegradable and non-biodegradable plastics, uncovers the impact of raw material diversification, and highlights ambitious investments and pioneering projects led by global manufacturers. The study explores competitive positioning and strategic alliances, assesses evolving regulatory landscapes, and analyzes the commercialization of breakthrough production technologies. With detailed market segmentation by polymer type, raw material, end-use industry, and geography, this report delivers actionable insights for manufacturers, suppliers, investors, and policymakers aiming to leverage bioplastics as a catalyst for sustainable industry transformation worldwide.

Bioplastics Market Analysis: Trends, Innovations & Capacity Expansion

The global bioplastics market is at a pivotal juncture, characterized by accelerating technological advances, substantial capacity expansions, and regulatory mandates that are redefining the competitive landscape and spurring adoption across diverse industries. Recent developments reflect the market’s evolution from niche sustainable applications to mainstream industrial and consumer segments, with a strong emphasis on environmental performance and circular economy principles.

Product Launches Expand Functional Applications

BASF’s launch of ecovio® M2351, a marine-biodegradable bioplastic for fishing gear, demonstrates how bioplastics are being engineered to solve environmental challenges such as marine litter, a critical issue driving regulatory and societal pressure, with the global marine biodegradable plastics market projected to grow significantly due to such innovations. Danimer Scientific’s introduction of Nodax™ PHA-based coffee capsules certified for home composting highlights the growing demand for sustainable consumer goods with convenient end-of-life solutions, aligning with consumer expectations for plastic alternatives that seamlessly integrate into daily life. Mitsubishi Chemical’s BioPBS™ FZ91, designed for flexible food packaging, further underscores how bioplastics are achieving technical standards required in sensitive applications, expanding market penetration in food contact materials where performance and regulatory compliance are non-negotiable.

Capacity Expansions Reflect Industry Confidence and Demand

Several significant capacity expansions signal robust confidence in the market’s long-term growth potential and reflect efforts to reduce production costs through economies of scale.

- TotalEnergies Corbion’s doubling of Luminy® PLA production in Thailand to 250,000 tonnes per year cements PLA’s position as one of the most scalable and versatile bioplastics, suitable for both rigid and flexible applications.

- Braskem’s $87 million investment to expand sugarcane-based bio-PE capacity by 30% reflects the rising demand for drop-in solutions compatible with existing recycling infrastructure, critical for brand owners seeking to meet sustainability targets without overhauling production processes.

- NatureWorks’ opening of its second Ingeo™ PLA plant in Thailand not only expands supply but strategically positions the company closer to key Asian markets where consumption of sustainable materials is growing fastest.

Strategic Alliances and M&A Drive Consolidation and Technological Integration

The bioplastics sector is experiencing significant consolidation and partnership activity as players seek to secure feedstock supply, integrate new technologies, and strengthen market positioning.

- The merger of Novamont and Versalis to form MATER-BIOPOLYMERS establishes Europe’s largest bioplastics producer, positioning the new entity to capitalize on EU regulatory tailwinds and demand for regionally sourced sustainable materials.

- Cargill’s partnership with Helm AG to build a $300 million PLA plant in Iowa underscores the drive for localized production capacity in North America, tapping into abundant agricultural feedstocks and responding to regional policy incentives.

- Solvay’s acquisition of BioAmber’s biosuccinic acid technology enhances its portfolio for bio-based polyesters, signaling how chemical companies are increasingly investing upstream in critical bio-based monomers.

Policy changes worldwide are accelerating market adoption. The EU’s Packaging and Packaging Waste Regulation requires 65% biobased content in packaging by 2040, setting clear industry targets. India’s ban on single-use plastics is boosting demand for alternatives like PHA and PLA, although challenges remain around costs and infrastructure. In the U.S., the BioPreferred Program’s $500 million funding push reflects government support for sustainable procurement, creating opportunities for bioplastics producers.

Technological Advances Enhance Bioplastics Performance

Innovation continues to tackle key challenges in biodegradability and feedstock diversity. MIT has developed enzyme-embedded PLA that biodegrades in soil within 48 hours, potentially revolutionizing single-use plastics. The Fraunhofer Institute’s work on bioplastics from rice husks for automotive parts demonstrates how waste streams can feed into high-performance bioplastics, reinforcing circular economy goals.

Sustainability Efforts Strengthen Market Positioning

Sustainability remains central to the bioplastics industry’s value proposition. Neste’s creation of 100% bio-based polypropylene with 85% lower CO₂ emissions versus fossil-based PP shows bioplastics’ viability in large-volume applications. LanzaTech’s work turning steel mill emissions into bioplastics highlights how industrial waste can become valuable, sustainable materials, connecting bioplastics to broader decarbonization strategies.

Bioplastics Market Dynamics: Regulatory Waves and Growth Opportunities

Trend: Regulatory Tsunami Accelerates Bioplastics Adoption Globally

The bioplastics industry is undergoing rapid change as governments worldwide enforce strict regulations to boost sustainable plastics use. In the European Union, the 2024 Packaging and Packaging Waste Regulation (PPWR) promotes bio-based materials and sets high targets for recyclability and recycled content, impacting over 27,000 companies and imposing fines of up to 4% of global revenue for non-compliance. In the U.S., California’s SB 54 requires all plastics to be compostable or recyclable by 2032. Globally, 38 countries have banned single-use plastics since 2023, fueling a robust 12% CAGR in bioplastics adoption, according to UNEP.

Industry players are scaling up to meet these demands. In Europe, TotalEnergies and Novamont have grown their bioplastics capacity by 45% over the past year, focusing on PLA and PHA to comply with new laws. In the U.S., Danimer and NatureWorks have increased production by 30% through SB 54-compliant innovations. Meanwhile, India has witnessed a 60% jump in bioplastics capacity, led by firms like Futerro and local companies introducing new compostable packaging approved by FSSAI.

This global regulatory push is driving not just compliance but also innovation, investment, and new partnerships across the bioplastics market. As businesses adapt to evolving standards, integrating bio-based and compostable solutions is becoming essential for packaging, consumer goods, and food service sectors. Strong policies and active enforcement are positioning bioplastics as the future of sustainable supply chains and products.

Opportunity: Marine-Degradable PHA Unlocks Growth in APAC Coastal Economies

Marine-degradable polyhydroxyalkanoates (PHA) present a significant growth opportunity in Asia-Pacific’s bioplastics market, especially for coastal economies facing severe plastic pollution. Countries like Indonesia, the Philippines, and Thailand contribute 86% of ocean-bound plastic waste, yet under 5% of coastal regions currently use certified marine-degradable plastics. This gap stems from higher costs, limited awareness, and insufficient recycling infrastructure for these innovative materials. PHA, certified by TÜV Austria OK Marine, fully degrades in seawater within 90 days, making it ideal for applications such as fishing gear, food packaging, and coastal infrastructure.

PHA production capacity in Asia-Pacific is expected to jump from 50,000 tonnes in 2024 to 500,000 tonnes by 2030, fueled by over $2 billion in investments from sources like the Asian Development Bank and the EU Green Deal. Costs are dropping as production scales up and sugarcane waste becomes a key feedstock, reducing prices from $4,200 to $2,800 per tonne by 2030. Market penetration for PHA in fishing gear alone is projected to grow from 8% to 45%, driven by policies such as Thailand’s 2025 fishing net replacement plan and Indonesia’s tax breaks for marine-degradable plastics.

Governments and financial institutions are actively supporting this shift. Thailand has established a $300 million fund for PHA R&D, Indonesia offers tax holidays for plant investments, and the Asian Development Bank has committed $500 million to ASEAN coastal waste management. Together, these initiatives position marine-degradable PHA as a cornerstone of sustainable plastics in APAC, offering environmental benefits and strong commercial potential for the bioplastics industry.

Bioplastics Market Competitive Landscape Highlighting Key Global Manufacturers

The global bioplastics market is experiencing accelerated growth in 2024 as sustainability mandates, carbon reduction goals, and consumer demand push industries to transition away from fossil-based plastics. From bio-based polyesters and polyolefins to innovative compostable materials like PLA and PHA, major producers are scaling capacities, investing in new technologies, and securing strategic partnerships across diverse sectors, including automotive, packaging, and consumer goods. The competitive landscape reflects a dynamic race to capture market share in this booming sector, as companies blend sustainability with performance to reshape global plastic supply chains.

NatureWorks: PLA Bioplastics Leadership & Applications

NatureWorks (USA) remains a leader in the PLA bioplastics space, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In February 2025, the company launched Ingeo™ 3D300, its fastest and highest-quality 3D printing grade, and in March 2025, it introduced Ingeo™ Extend for BOPLA films, further expanding its portfolio into high-performance applications like additive manufacturing and flexible packaging. NatureWorks continues to explore opportunities in durable goods and automotive markets, leveraging PLA's properties for high-performance applications beyond traditional packaging.

TotalEnergies Corbion: PLA Innovation & Capacity Expansion

TotalEnergies Corbion (Netherlands/France) has emerged as a key innovator in PLA bioplastics, with its Luminy® PLA range produced at a 75,000 tonnes per year facility in Thailand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion. TotalEnergies Corbion is actively engaged in R&D to enhance PLA's properties and expand its applicability, and with its existing production footprint, it is well-positioned to capitalize on the growing demand for bioplastics in Asian markets.

Braskem: Bio-based PE/EVA Dominance & Market Diversification

Braskem (Brazil) stands as the world’s largest producer of bio-based polyethylene, with its green ethylene plant reaching a capacity of 275,000 tonnes per year as of May 2025, following a significant 37% expansion. In October 2024, Braskem formed a joint venture with SCG Chemicals to establish a bio-ethylene project in Thailand, which will utilize bio-ethanol from sustainably sourced sugarcane, reinforcing its commitment to diversifying sustainable feedstocks and expanding global supply chains. Braskem’s I’m green™ bio-based polyethylene is widely recognized for its carbon-negative footprint (highlighted in 2023), strengthening its position as a leading sustainable alternative in packaging, consumer goods, and industrial applications globally.

Novamont: Compostable Bioplastics Innovation & Integration

Novamont (Italy) continues to drive innovation in compostable bioplastics through its Mater-Bi® product line. Following its acquisition by Versalis in October 2023, it now operates as a highly integrated entity in the bioplastics sector, leveraging substantial capacities for its compostable materials. The acquisition of BioBag Group in 2023 significantly broadened its reach in sustainable packaging solutions, particularly in compostable bags and films across Europe. Novamont remains focused on sustainable feedstock sourcing and cost efficiency, including through the valorization of waste-stream feedstocks, to enhance its competitive edge.

Mitsubishi Chemical: Advancements in Bio-based Engineering Plastics

Mitsubishi Chemical (Japan) is making notable strides in bio-based engineering plastics and polymers, including its collaboration on BioPBS production with a capacity of 20,000 tonnes per year, and is continually expanding its product offerings. The company actively leverages bio-based engineering plastics like DURABIO™, a bio-based polycarbonate, for diverse applications including eyewear, automotive components (e.g., Honda motorcycle bodywork and windshields in late 2024), and other high-value consumer and industrial goods, showcasing its push into high-performance markets. Mitsubishi Chemical aims to significantly increase its bio-based and recycled content across its product portfolio by 2030, aligning its business strategy with global sustainability goals and increasing demand for bio-based alternatives in performance applications.

Amcor: Sustainable Packaging Solutions with Bioplastics

Amcor (Switzerland) is significantly influencing the bioplastics packaging sector by actively integrating bio-based polyethylene into its packaging solutions. The company has strategically partnered with Paboco’s paper bottle alliance to develop bioplastic barriers for sustainable bottle solutions, blending the advantages of paper and bio-based polymers. With an ambitious target of achieving 100% recyclable or reusable packaging by 2025, Amcor is positioning itself as a leader in sustainable packaging innovations. While considerable progress has been made, particularly in rigid packaging, the company, like others, faces ongoing challenges in transforming certain complex flexible packaging structures to meet this ambitious goal fully.

Market Share and Segmentation Analysis of the Global Bioplastics Market

By Type: Biodegradable Plastics Dominate, Non-Biodegradable Bioplastics Maintain Steady Growth

In 2025, biodegradable plastics leads the market with a 53.7% share, propelled by stringent regulations such as the EU Single-Use Plastics Directive and mounting demand for sustainable packaging solutions. These materials, including PLA, PHA, PBAT, PBS, and starch blends, are rapidly adopted for their compostability and reduced environmental impact. Meanwhile, non-biodegradable bioplastics (such as Bio-PE and Bio-PET) continue to grow steadily with a CAGR of 26.2% supported by high-profile applications from brands like Coca-Cola’s PlantBottle and increased interest from FMCG brands aiming for partial fossil-free content in their packaging.

By Raw Material: Sugarcane and Corn Starch Lead, Algae and Lignin Emerge as Fastest-Growing Feedstocks

Algae and lignin are the fastest-growing feedstocks with a CAGR of 26.1%, as industry innovators tap into their potential for next-generation, high-performance bioplastics. Waste streams are also gaining traction, reflecting a broader shift toward circular economy models and resource efficiency. Sugarcane and corn starch remain the dominant raw materials, jointly accounting for over 50% of the market in 2025. Their use in producing both biodegradable and non-biodegradable bioplastics (such as PLA and Bio-PET) is supported by well-established supply chains and processing technologies.

By End-Use Industry: Packaging Commands Market Share, Healthcare and Automotive Accelerate Adoption

Packaging is the largest end-use segment, capturing 58.1% of bioplastics demand in 2025. The boom in food, beverage, and e-commerce packaging solutions is fueled by regulatory mandates, consumer sustainability awareness, and retailer initiatives. Healthcare and automotive are the fastest-growing end-use industries, as bio-based materials enable lightweight, safe, and sustainable solutions for surgical implants, interiors, and technical parts. The textiles segment is also on the rise, leveraging bio-based fibers like PLA for environmentally conscious apparel and home textiles.

.png)

Germany Leading Bioplastics Technology and Policy for Automotive, Packaging, and Marine Solutions

Germany continues to shape the global bioplastics landscape with unparalleled R&D investment, innovation, and policy momentum. With over €2.1 billion in public and private bioplastics R&D, the nation hosts a powerful ecosystem led by the Fraunhofer Institute, whose marine-degradable PHA demonstrates significantly accelerated breakdown under composting conditions, even achieving substantial depolymerization in days in controlled environments, addressing plastic pollution at its source. Automotive manufacturers like BMW now incorporate BASF’s Ecovio® bioplastics into interior parts, meeting both sustainability targets and demanding performance requirements. Südzucker’s transparent PLA films are widely adopted across Europe’s food packaging sector, reflecting German leadership in safe, compostable food contact materials. In 2024, Siemens revolutionized compounding with AI-driven bioplastic plants, reducing waste and improving process efficiency. At the policy level, Germany, in line with the EU’s Packaging and Packaging Waste Regulation (PPWR), continues its proactive stance towards the 2030 target, where all packaging must be recyclable, and specific categories must be compostable, creating an urgent and lucrative opportunity for bioplastic manufacturers. A notable 2025 development sees increased collaboration between German chemical giants and smaller bio-startup firms, focusing on commercializing new bio-based polymers for rigid packaging applications, spurred by the PPWR's upcoming recycled content targets for plastic packaging starting January 1, 2030. Germany’s industrial integration, regulatory certainty, and technology-first approach make it the epicenter of bioplastics innovation and commercial adoption in Europe.

United States Fastest-Growing Bioplastics Market with Major Investments and Regulatory Push

The United States is witnessing exponential growth in the bioplastics industry, propelled by a surge in public funding, scale-up investments, and landmark policy initiatives. With $1.8 billion in Department of Energy funding supporting PHA and PLA scaling, plus Danimer Scientific's substantial investments, including its ongoing PHA scale-up efforts at its Kentucky facility and a significant $700 million project for a new PHA plant in Georgia, the US is quickly transitioning from pilot projects to industrial-scale production. PLA is a major focus, powering high-temperature 3D printing filaments from NatureWorks, while Tepha’s PHA is revolutionizing medical applications such as surgical meshes, resorbable sutures, and implants. Regulatory drivers such as California’s SB 54, which requires 100% of single-use packaging and plastic food service ware to be recyclable or compostable by 2032, are forcing brands and converters to accelerate bioplastic adoption in consumer packaging, food service, and beyond. A key 2025 development includes the full operationalization of several new bioplastics production lines in the Midwest, significantly boosting domestic capacity for both PLA and PHA, alongside an anticipated announcement of new federal grants targeting sustainable aviation fuels that also leverage biopolymer technologies. The American bioplastics market is marked by fast-moving R&D, commercialization partnerships, and strong alignment between federal policy and private sector goals, making it the world’s most dynamic environment for bioplastic innovation and uptake.

China: Dominating Bioplastics Production & Capacity Expansion

China stands at the forefront of bioplastics manufacturing, accounting for 65% of global output and demonstrating unrivaled capacity expansion. The nation’s annual bioplastics production now exceeds 3.2 million tons, led by industry giants like Kingfa, rapidly expanding its biodegradable plastics output, with substantial annual capacities, including for PBAT, positioning them as dominant global players, and Sinopec, with a 500,000-ton PLA facility serving textile, packaging, and agricultural markets. The Chinese government’s proactive stance is reflected in mandatory policies such as GB Standard 38507-2023 for biodegradable plastics and the ambitious 2025 regulation mandating that at least 30% of certain packaging categories be bioplastic-based. This regulatory certainty is catalyzing investment and rapid technology transfer across the value chain, from feedstocks and synthesis to compounding and downstream adoption. In 2025, several new large-scale PLA and PHA production facilities, particularly in coastal provinces, are expected to come online, further cementing China's role as the global leader in bioplastics manufacturing capacity. Furthermore, major Chinese e-commerce platforms are intensifying their push for "green packaging" in 2025, with internal targets pushing for a significant portion of their shipments to utilize compostable or recyclable bioplastic packaging. China’s dominance is also visible in its rapid commercialization, with major brands and retailers shifting to bioplastics packaging to meet both domestic and global demand. The country’s scale, policy discipline, and production agility ensure its ongoing global leadership in bioplastics.

Netherlands: Pioneering Circular Bioplastics Economy

The Netherlands is recognized as Europe’s circular economy model, blending advanced bioplastics innovation with rapid commercialization in consumer brands and healthcare. Avantium’s PEF, a 100% bio-based PET alternative, is a game-changer for beverage and food packaging, enabling fully renewable bottles and containers, with Avantium actively pursuing significant funding for its commercialization following a recent €10 million financing round. DSM’s Niaga® platform is pioneering fully recyclable bioplastics, supporting closed-loop manufacturing in electronics and home goods. Commercial pilots such as Heineken’s ongoing PEF bottle assessments for beer packaging and Philips’ adoption of PHA in select medical devices by 2026 show how the Netherlands is translating R&D leadership into market-ready products. The national and EU regulatory environment actively supports these initiatives, encouraging certification and sustainable sourcing. A notable 2025 development includes the launch of several new pilot projects for marine-degradable bioplastics in aquaculture and fishing industries, supported by public-private partnerships aiming to reduce marine plastic pollution. Furthermore, Dutch research institutions are leading advancements in enzymatic recycling technologies for complex bioplastic waste streams, with 2025 seeing increased funding for these initiatives. The Netherlands’ culture of innovation, corporate partnership, and circularity positions it as a critical hub for bioplastics breakthroughs in Europe and beyond.

Japan Advancing High-Performance Bioplastics for Electronics, Packaging, and Consumer Goods in Asia

Japan’s bioplastics industry is defined by its focus on specialty, high-performance materials, driven by both market demand and robust government support. Mitsubishi Chemical’s BioPBS™ stands out for its heat resistance up to 120°C, making it the material of choice for hot food packaging, beverage lids, and disposable utensils. Toray is driving innovation in PLA films for flexible electronics and smart packaging, supporting the country’s advanced manufacturing sector. Consumer electronics giant Sony has pledged to use 100% bioplastic packaging by 2027, accelerating market growth and downstream adoption. Backed by a $300 million Green Innovation Fund from METI, Japan’s public and private sectors are working together to bring bioplastics into mainstream consumer goods, automotive, and electronics markets. In 2025, Japanese government initiatives are set to provide enhanced subsidies for companies investing in domestic production of high-performance biopolymers for the automotive sector, aiming to secure supply chains. Additionally, leading Japanese consumer goods manufacturers are anticipated to announce expanded use of bio-based plastics in their product lines, particularly for personal care and household items, driven by the government’s 2025 targets and initiatives encouraging increased biopolymer use. This strategic blend of technical excellence, forward-thinking policy, and strong brand engagement ensures Japan’s continued leadership in high-value, next-generation bioplastics.

Bioplastics Market Report Scope

Bioplastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20.8 Billion

|

|

Market Size (2034)

|

$156.1 Billion

|

|

Market Growth Rate

|

25.1%

|

|

Segments

|

By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others), By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others), By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others), By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (US), BASF SE (Germany), Novamont S.p.A. (Italy), Braskem S.A. (Brazil), TotalEnergies Corbion, Mitsubishi Chemical Group Corporation (Japan), Eastman Chemical Company (U.S.), Arkema S.A. (France), Versalis S.p.A. (Italy), Toray Industries Inc. (Japan), Danimer Scientific (US), CJ Biomaterials Inc. (South Korea), Plantic Technologies Limited (Australia), Avantium (Netherlands), RWDC Industries (U.S./Singapore), Biome Bioplastics (UK), FKuR Kunststoff GmbH (Germany), Green Dot Bioplastics (U.S.), KANEKA Corporation (Japan), Total-Corbion PLA (Netherlands/France), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioplastics Market Segmentation

By Non-Biodegradable Plastics

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Bio-Polypropylene (Bio-PP)

- Bio-Polyamides (Bio-PA)

- Polyethylene Furanoate (PEF)

- Others

By Biodegradable Plastics

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS) & Co-Polymers (PBSA)

- Starch Blends / Thermoplastic Starch (TPS)

- Polycaprolactone (PCL)

- Cellulose-based Plastics

- Others

By Raw Material

- Sugarcane

- Corn Starch

- Cellulose

- Vegetable Oils

- Lignin

- Algae

- Waste Streams

- Methane / Biogas

- Others

By End-Use Industry

- Packaging

- Consumer Goods

- Automotive & Transportation

- Textiles

- Agriculture & Horticulture

- Building & Construction

- Medical & Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Bioplastics Market

- NatureWorks LLC (US)

- BASF SE (Germany)

- Novamont S.p.A. (Italy)

- Braskem S.A. (Brazil)

- TotalEnergies Corbion

- Mitsubishi Chemical Group Corporation (Japan)

- Eastman Chemical Company (US)

- Arkema S.A. (France)

- Versalis S.p.A. (Italy)

- Toray Industries Inc. (Japan)

- Danimer Scientific (US)

- CJ Biomaterials Inc. (South Korea)

- Plantic Technologies Limited (Australia)

- Avantium (Netherlands)

- RWDC Industries (U.S./Singapore)

- Biome Bioplastics (UK)

- FKuR Kunststoff GmbH (Germany)

- Green Dot Bioplastics (US)

- KANEKA Corporation (Japan)

- Total-Corbion PLA (Netherlands/France)

* List Not Exhaustive

Methodology

The Global Bioplastics Market 2025–2034 report is built on rigorous primary and secondary research, including direct interviews with industry stakeholders across the bioplastics value chain—from manufacturers and raw material suppliers to technology innovators and end-user industries—to capture insights on trends, technological advancements, capacity expansions, regulatory changes, and strategic developments. Secondary research incorporates analysis of industry publications, patents, regulatory documents, company filings, sustainability reports, and trade data to validate and enrich primary insights. Market sizing was derived using top-down and bottom-up approaches, factoring in production capacities, consumption trends, raw material flows, and regulatory adoption rates across more than 25 countries. Data integrity was ensured through meticulous triangulation and cross-validation, with proprietary analytics from USDAnalytics providing deeper perspectives on competitive dynamics, market scenarios, and emerging growth drivers, resulting in a comprehensive and actionable assessment of the global bioplastics landscape.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Polymer Type (Biodegradable: PLA, PHA, PBAT, PBS, TPS, etc.; Non-Biodegradable: Bio-PE, Bio-PET, Bio-PP, Bio-PA, PEF, etc.), Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane/Biogas, Others), and End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others).

- Competitive Landscape: Profiles and strategies of 20+ leading companies, innovators, and technology developers active in the global bioplastics industry.

- Trends & Disruptions: In-depth examination of regulatory frameworks, technological breakthroughs, marine-degradable bioplastics, enzymatic recycling, sustainability initiatives, and circular economy integration.

- Industry Dynamics: Comprehensive analysis of market drivers, challenges, investment flows, feedstock trends, sustainability imperatives, and commercialization strategies shaping the bioplastics market through 2034.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Narrative insights, detailed data tables, and visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & Company Profiles

- Regulatory Landscape & Emerging Policy Tracker

- Executive Summary & Key Analyst Insights

- Custom Queries/Analyst Support Post Sale

Table of Contents for Bioplastics Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Bioplastics Market Size & Growth Forecasts (2025-2034)

2.1. Introduction to Bioplastics

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Robust Regulatory Support

2.3.2. Accelerating Consumer Demand for Green Materials

2.3.3. Technological Breakthroughs in Polymer Science

2.3.4. Widespread Adoption Across Key Applications

2.4. Market Challenges and Restraints

3. Bioplastics Market Analysis: Trends, Innovations & Capacity Expansion

3.1. Product Launches Expand Functional Applications

3.1.1. Marine-Biodegradable Bioplastics for Fishing Gear (BASF ecovio® M2351)

3.1.2. PHA-based Home Compostable Coffee Capsules (Danimer Scientific Nodax™)

3.1.3. Flexible Food Packaging Solutions (Mitsubishi Chemical BioPBS™ FZ91)

3.2. Capacity Expansions Reflect Industry Confidence and Demand

3.2.1. TotalEnergies Corbion: Doubling Luminy® PLA Production

3.2.2. Braskem: Expansion of Sugarcane-based Bio-PE Capacity

3.2.3. NatureWorks: Opening of Second Ingeo™ PLA Plant in Thailand

3.3. Strategic Alliances and M&A Drive Consolidation and Technological Integration

3.3.1. Merger of Novamont and Versalis to Form MATER-BIOPOLYMERS

3.3.2. Cargill’s Partnership with Helm AG for PLA Plant

3.3.3. Solvay’s Acquisition of BioAmber’s Biosuccinic Acid Technology

3.4. Policy and Regulatory Shifts Accelerating Market Adoption

3.4.1. EU’s Packaging and Packaging Waste Regulation (PPWR)

3.4.2. India’s Ban on Single-Use Plastics

3.4.3. U.S. BioPreferred Program Funding Push

3.5. Technological Advances Enhance Bioplastics Performance

3.5.1. Enzyme-Embedded PLA for Rapid Biodegradation (MIT)

3.5.2. Bioplastics from Rice Husks for Automotive Parts (Fraunhofer Institute)

3.6. Sustainability Efforts Strengthen Market Positioning

3.6.1. Neste’s 100% Bio-based Polypropylene with Lower CO₂ Emissions

3.6.2. LanzaTech’s Carbon-Capture-Derived Bioplastics

4. Bioplastics Market Dynamics: Regulatory Waves and Growth Opportunities

4.1. Trend: Regulatory Tsunami Accelerates Bioplastics Adoption Globally

4.1.1. European Union’s 2024 Packaging and Packaging Waste Regulation (PPWR)

4.1.2. California’s SB 54 Requirements for Plastics

4.1.3. Global Single-Use Plastics Bans and Bioplastics CAGR

4.1.4. Capacity Scale-up by Leading Players (TotalEnergies, Novamont, Danimer, NatureWorks, Futerro)

4.2. Opportunity: Marine-Degradable PHA Unlocks Growth in APAC Coastal Economies

4.2.1. Addressing Plastic Pollution in Asia-Pacific Coastal Regions

4.2.2. PHA Degradation Characteristics and Applications

4.2.3. PHA Production Capacity Projections and Cost Reductions

4.2.4. Policy Support and Investments in PHA (Thailand, Indonesia, ADB)

5. Competitive Landscape of the Global Bioplastics Market

5.1. Key Players and Market Competition Overview

5.2. Company Profiles & Strategies

5.2.1. NatureWorks: PLA Bioplastics Leadership & Applications

5.2.2. TotalEnergies Corbion: PLA Innovation & Capacity Expansion

5.2.3. Braskem: Bio-based PE/EVA Dominance & Market Diversification

5.2.4. Novamont: Compostable Bioplastics Innovation & Integration

5.2.5. Mitsubishi Chemical: Advancements in Bio-based Engineering Plastics

5.2.6. Amcor: Sustainable Packaging Solutions with Bioplastics

5.2.7. Other Key Players

6. Bioplastics Market Share & Segmentation Analysis (2021- 2034)

6.1. By Type: Biodegradable Plastics vs. Non-Biodegradable Bioplastics

6.1.1. Biodegradable Plastics Market Share & Drivers (PLA, PHA, PBAT, PBS, Starch Blends)

6.1.2. Non-Biodegradable Bioplastics Growth & Applications (Bio-PE, Bio-PET)

6.2. By Raw Material: Leading and Emerging Feedstocks

6.2.1. Sugarcane and Corn Starch: Dominant Raw Materials

6.2.2. Algae and Lignin: Fastest-Growing Feedstocks

6.2.3. Waste Streams: Gaining Traction in Circular Economy Models

6.2.4. Cellulose, Vegetable Oils, Methane/Biogas, Others

6.3. By End-Use Industry: Dominance and Accelerated Adoption

6.3.1. Packaging: Largest Segment and Demand Drivers

6.3.2. Healthcare and Automotive: Fastest-Growing End-Use Industries

6.3.3. Textiles

6.3.4. Agriculture & Horticulture

6.3.5. Building & Construction

6.3.6. Consumer Goods

6.3.7. Others

7. Geographic Analysis: Bioplastics Market Outlook by Country (2021- 2034)

7.1. North America

7.1.1. United States: Fastest-Growing Bioplastics Market with Major Investments and Regulatory Push

7.1.2. Canada: Steady Growth Driven by Sustainable Packaging Demand and Polysaccharide Dominance

7.1.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.2. Europe

7.2.1. Germany: Leading Bioplastics Technology and Policy for Automotive, Packaging, and Marine Solutions

7.2.2. UK: Strong Growth Driven by Packaging Sector and Environmental Awareness

7.2.3. France: Increasing Adoption Driven by Stringent Regulations and Innovative Material Development

7.2.4. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.5. Italy: High Growth Trajectory with Increasing Adoption in Packaging and Textile Applications

7.2.6. Russia: Emerging Market with Growing Awareness and Demand for Eco-friendly Alternatives

7.2.7. Rest of Europe: Broad Adoption of Bio-based Biodegradables and Flexible Packaging Amidst Policy Shifts

7.2.8. Netherlands: Pioneering Circular Bioplastics Economy

7.3. Asia Pacific

7.3.1. China: Dominating Bioplastics Production & Capacity Expansion

7.3.2. Japan: Advancing High-Performance Bioplastics for Electronics, Packaging, and Consumer Goods in Asia

7.3.3. India: Robust Growth Fueled by Evolving Consumer Demand and Favorable Regulatory Frameworks

7.3.4. South Korea: Advancing Sustainable Biopolymer Market with Focus on Packaging and Biomedical Applications

7.3.5. Australia: Accelerating Adoption in Packaging and Agriculture with Focus on Polysaccharides and PLA

7.3.6. Southeast Asia: Rising Demand in Flexible Packaging and Electronics, Bolstered by Government Initiatives

7.3.7. Rest of Asia: Significant Market Share and Fastest Growth Driven by Demand for Bio-based Packaging

7.4. South America

7.4.1. Brazil: Leading Regional Growth with Strong Presence in Bio-PE and PHA Production

7.4.2. Argentina: Emerging Market with Potential in Electrical & Electronics and Biodegradable Applications

7.4.3. Rest of South America: Increasing Adoption of PLA and PHA in Sustainable Packaging Solutions

7.5. Middle East and Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers in Construction and Agriculture

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging and Consumer Goods

7.5.3. Rest of Middle East: Expanding Market for Bioplastics in Packaging and Electrical & Electronics Sectors

7.5.4. South Africa: Growing Adoption of Biopolymers in Electrical & Electronics and Packaging

7.5.5. Egypt: Increasing Focus on Bioplastic Multi-Layer Films for Food Packaging and Delivery Services

7.5.6. Rest of Africa: Rising Demand for Eco-Friendly Plastics, Particularly in Packaging Industry

8. Bioplastics Market Size Outlook by Region (2025-2034)

8.1. North America Bioplastics Market Size Outlook to 2034

8.1.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.1.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.1.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.1.4. By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

8.2. Europe Bioplastics Market Size Outlook to 2034

8.2.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.2.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.2.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.2.4. By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

8.3. Asia Pacific Bioplastics Market Size Outlook to 2034

8.3.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.3.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.3.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.3.4. By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

8.4. South America Bioplastics Market Size Outlook to 2034

8.4.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.4.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.4.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.4.4. By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

8.5. Middle East and Africa Bioplastics Market Size Outlook to 2034

8.5.1. By Non-Biodegradable Plastics (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Polyethylene Furanoate (PEF), Others)

8.5.2. By Biodegradable Plastics (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS) & Co-Polymers (PBSA), Starch Blends / Thermoplastic Starch (TPS), Polycaprolactone (PCL), Cellulose-based Plastics, Others)

8.5.3. By Raw Material (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Methane / Biogas, Others)

8.5.4. By End-Use Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Medical & Healthcare, Others)

9. Company Profiles: Leading Players in the Bioplastics Market

9.1. NatureWorks LLC (US)

9.2. BASF SE (Germany)

9.3. Novamont S.p.A. (Italy)

9.4. Braskem S.A. (Brazil)

9.5. TotalEnergies Corbion

9.6. Mitsubishi Chemical Group Corporation (Japan)

9.7. Eastman Chemical Company (US)

9.8. Arkema S.A. (France)

9.9. Versalis S.p.A. (Italy)

9.10. Toray Industries Inc. (Japan)

9.11. Danimer Scientific (US)

9.12. CJ Biomaterials Inc. (South Korea)

9.13. Plantic Technologies Limited (Australia)

9.14. Avantium (Netherlands)

9.15. RWDC Industries (U.S./Singapore)

9.16. Biome Bioplastics (UK)

9.17. FKuR Kunststoff GmbH (Germany)

9.18. Green Dot Bioplastics (US)

9.19. KANEKA Corporation (Japan)

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.1.1. Geographic Coverage

11.1.2. Market Segmentation

11.1.3. Competitive Landscape Assessment

11.1.4. Key Trends & Disruptions

11.1.5. Industry Dynamics

11.1.6. Historic and Forecast Data Range

11.2. Deliverables

11.2.1. Full Market Research Report (PDF, Excel)

11.2.2. Country-Level Forecasts & Analysis

11.2.3. Segment-wise Revenue Projections

11.2.4. Competitive Benchmarking & Company Profiles

11.2.5. Regulatory Landscape & Emerging Policy Tracker

11.2.6. Executive Summary & Key Analyst Insights

11.2.7. Custom Queries/Analyst Support Post Sale

12. Disclaimer