Biopolymers Market Overview: Growth Drivers, Trends & Outlook 2025-2034

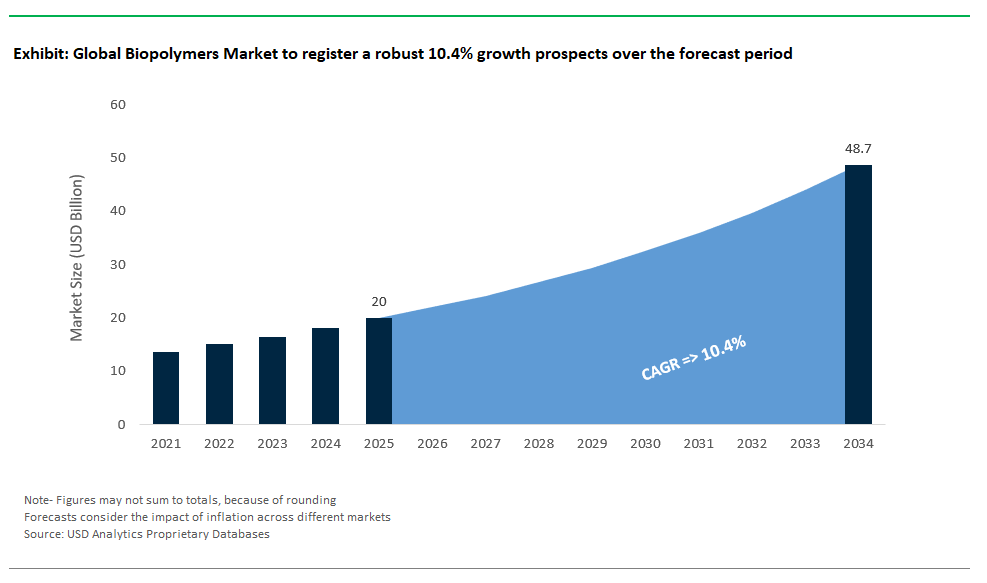

The Global Biopolymers Market is rapidly advancing between 2025 and 2034, fueled by the worldwide transition toward sustainable materials across packaging, consumer goods, automotive, textiles, agriculture, and construction sectors. Analysts project the market to expand at a compelling CAGR of 10.4%, with the global biopolymers market poised to reach USD 48.7 billion by 2034, rising from USD 20 billion in 2025. This acceleration is propelled by intensifying regulations on conventional plastics, surging consumer preference for eco-friendly solutions, and breakthrough innovations in both biodegradable and non-biodegradable polymer technologies.

Leveraging proprietary research from USDAnalytics, the latest edition provides a thorough evaluation and future outlook for the global biopolymers market, mapping developments across 25+ countries and profiling more than 20 prominent companies By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others), By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others), By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others), By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others), By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others).

This report provides a comprehensive analysis of the global biopolymers market, delving into the forces transforming the industry through 2034. It delivers in-depth coverage of technological advancements across both biodegradable and non-biodegradable polymers, evaluates large-scale investments, and highlights pioneering projects shaping future supply chains. The study examines competitive strategies among market leaders, details key regulatory trends influencing industry adoption, and explores the impact of new feedstocks and innovative production technologies. With dedicated insights on market segmentation by polymer type, end-user, technology, and feedstock, the report offers actionable intelligence for manufacturers, suppliers, investors, and policymakers seeking to capitalize on the expanding role of biopolymers in driving sustainable transformation across global value chains.

Biopolymers Market Analysis: Trends, Innovations & Capacity Expansion

The global biopolymers market is undergoing significant transformation, propelled by regulatory mandates, rapid technological innovation, and aggressive capacity expansions that are reshaping both supply and demand dynamics. Recent activities across product launches, capacity growth, strategic alliances, and sustainability initiatives collectively underscore the industry’s pivot toward scalability and diversified applications, particularly as sustainability pressures intensify worldwide.

Product Innovation & Application Horizons

Product launches over the past two years have underscored how biopolymers are penetrating increasingly specialized end-use segments. NatureWorks’ introduction of Ingeo™ biopolymer tailored for 3D printing filaments exemplifies the shift toward high-performance applications such as automotive prototyping, reflecting the market’s move beyond conventional packaging uses into engineering and industrial domains. Similarly, BASF’s release of ecovio® F4010 for compostable agricultural mulch films speaks to the critical role biopolymers play in sustainable agriculture, driven by regulatory restrictions on conventional plastics in soil applications. Danimer Scientific’s marine-degradable PHA-based biopolymer further illustrates the market’s responsiveness to global concerns about marine litter and single-use plastics, positioning biopolymers as essential solutions in environmentally sensitive applications.

Capacity Expansions Driving Market Growth

Substantial capacity expansions signal strong confidence in long-term market growth and the need for economies of scale to reduce production costs.

- Braskem invested to boost sugarcane-based bio-PE output by 30% in 2023 as part of a larger US$377 million investment, underscoring bio-based polyolefins’ growing appeal as drop-in replacements for fossil-based plastics.

- TotalEnergies Corbion inaugurated a 75,000-tonne/year PLA facility in Rayong, Thailand, in 2019 and announced plans for a second 100,000-tonne/year plant in France, reflecting significant scaling of Luminy® PLA production.

These expansions not only meet rising global demand but strategically position producers closer to feedstock sources and emerging regional markets in Asia.

M&A and Strategic Partnerships Shaping Biopolymer Landscape

Strategic collaborations and M&A are consolidating market leadership and technology portfolios.

- Solvay’s acquisition of BioAmber’s biosuccinic acid technology strengthens its foothold in bio-based monomers critical for diverse biopolymer formulations, signaling the growing importance of upstream integration in securing supply chains.

- Versalis’s acquisition of Novamont has created a highly integrated group within the European bioplastics industry, leveraging Novamont’s MATER-BI bioplastic and enhancing competitive positioning in key European markets governed by stringent sustainability regulations.

- The Cargill-Helm AG joint venture to establish a new bio-based 1,4-butanediol (BDO) plant in Iowa reflects North America’s drive to localize biopolymer precursor production amid increasing policy support, while also tapping into local agricultural feedstocks.

Policy & Regulatory Catalysts for Biopolymer Adoption

Regulatory frameworks continue to be a significant catalyst for biopolymers adoption. The European Union’s enforcement of the Single-Use Plastics Directive (SUPD), by restricting certain conventional single-use plastics, is compelling packaging producers to explore and integrate sustainable alternatives, including biopolymers, especially in applications where mechanical recycling is challenging or limited. In the U.S., the ongoing BioPreferred Program reflects the growing federal commitment to biobased procurement, providing crucial market signals for private investment and accelerating commercialization across sectors from packaging to consumer goods.

Technological Advancements Enhancing Biopolymer Performance

The market’s technological frontier is advancing rapidly, addressing key limitations in biodegradation rates and feedstock diversity. Research into enzyme-enhanced PLA degradation, such as the work being explored at institutions like MIT, aims to significantly reduce decomposition times, which could dramatically expand PLA’s usability in single-use applications and overcome challenges related to composting infrastructure compatibility. Fraunhofer Institute’s success in producing bio-based polyamides from food waste introduces an innovative pathway for integrating circular economy principles into biopolymer manufacturing, potentially reducing raw material costs and environmental impact.

Sustainability Initiatives Reinforcing Green Credentials

Sustainability remains the biopolymers market’s core value proposition, further strengthened by initiatives such as Neste’s bio-naphtha production, achieving up to 85% lower CO₂ emissions versus fossil-derived alternatives. Similarly, LanzaTech’s scaling of carbon-capture-derived biopolymers demonstrates how industrial emissions can become feedstocks for sustainable polymers, creating a compelling narrative of carbon circularity. These initiatives not only support climate targets but also appeal to brand owners seeking low-carbon materials to meet ESG commitments.

Biopolymers Market Dynamics: Opportunities & Circular Economy Trends

Trend: Circular Economy Integration Accelerates Sustainable Growth in Biopolymers

The global biopolymers market is rapidly shifting as the circular economy becomes a priority for industries and regulators. Leading FMCG players like Unilever and Nestlé have embraced closed-loop biopolymer systems, helping divert 12 million tonnes of waste from landfills by 2024. By 2027, the EU Circular Economy Action Plan aims for a 90% biopolymer collection rate for recycling or composting. Analysts forecast that circular practices could cut virgin biopolymer production costs by up to 25% by 2030, giving early adopters a strong competitive edge.

Technology is central to this transition. Companies like Danone and Carbios are running commercial enzymatic recycling plants, achieving 95% material recovery at capacities up to 5,000 tonnes annually. In parallel, AI-driven sorting systems from Veolia and Suez are lowering contamination rates by 40%, boosting the quality and value of recycled biopolymers. Together, these innovations highlight how circular economy integration and advanced recycling technologies are reshaping the biopolymers industry worldwide.

Opportunity: Enzymatic Recycling Infrastructure Unlocks High-Value Growth in Biopolymers

Scaling up enzymatic recycling offers a significant opportunity for the global biopolymers market. Currently, fewer than 15% of recycling facilities can process biopolymers, despite enzymatic depolymerization outperforming traditional methods. This advanced technology can handle up to 100,000 tonnes annually, double the capacity of mechanical recycling, and uses 60% less energy, according to Fraunhofer UMSICHT. Global enzymatic recycling capacity is expected to rise sharply from 35,000 tonnes in 2024 to 500,000 tonnes by 2030. At the same time, costs could drop from $1,200 to $650 per tonne, while carbon savings may nearly double to 5.8 tonnes of CO₂ equivalent per tonne recycled.

Policy support and new investments are driving this shift. The EU’s €2 billion Green Deal fund targets enzymatic recycling projects, and the US Inflation Reduction Act offers tax credits of up to $85 per tonne for carbon-negative initiatives. These incentives are speeding up commercialization, making enzymatic recycling a crucial growth driver for sustainability and competitiveness in the biopolymers industry, provided that technological and infrastructure challenges are addressed.

Competitive Landscape of the Global Biopolymer Market

The global biopolymer market is experiencing strong momentum in 2024, driven by increasing regulatory pressures, corporate sustainability goals, and consumer demand for eco-friendly alternatives to conventional plastics. Leading players are scaling capacities, forming strategic partnerships, and diversifying applications beyond traditional packaging into automotive, electronics, textiles, and consumer goods. From PLA and PHA to bio-based PE, PET, and innovative starch blends, the competitive landscape is marked by technological innovation, significant capital investments, and expanding global footprints. As the biopolymer industry transitions from niche applications to mainstream markets, companies are positioning themselves to capture growing opportunities in the shift toward sustainable materials.

NatureWorks: PLA Biopolymer Leadership & Applications

NatureWorks (PLA) has firmly established itself as a global leader in PLA biopolymers, with its new 75,000 tonnes per year Thailand plant nearing completion. NatureWorks' Ingeo biopolymers are increasingly adopted in durable applications, including areas like consumer goods and electronics, demonstrating PLA's evolving role beyond traditional packaging.

TotalEnergies Corbion: PLA Innovation and Capacity Expansion

TotalEnergies Corbion (PLA) continues to drive innovation in PLA technology, operating a 75,000 tonnes per year Luminy® PLA plant in Thailand, with plans for a second 100,000 tonnes per year facility in France to further expand its production capacity. TotalEnergies Corbion is actively investing in R&D and innovation, as evidenced by its patenting activities, to expand the use of its Luminy® PLA into high-performance and durable applications such as automotive and electronics, signaling a strategic pivot beyond its established base in flexible packaging and single-use products.

Danimer Scientific: PHA Biopolymers & Market Challenges

Danimer Scientific (PHA) had been a significant player in advancing polyhydroxyalkanoate (PHA) biopolymers, with efforts focused on commercialization and scaling its Kentucky facility. However, in a major development, Danimer Scientific filed for bankruptcy in March 2025 and is currently undergoing an orderly wind-down of its operations. In Q1 2024, Danimer secured its first commercial order for a 20-million-pound cutlery award, marking a crucial step in PHA’s path toward widespread market adoption in specific applications.

Kaneka Corporation: PHA-PHBH™ Advancements & Strategic Collaborations

Kaneka Corporation (PHA-PHBH™) is a significant player in the PHA segment, focusing on its proprietary PHBH™ biopolymer, with capacity already reaching 20,000 tonnes per year following an expansion completed by January 2024. The company is expecting to start full-scale operations at its 15,000-ton demonstration plant in FY2025. Kaneka’s collaboration with Suntory to produce biodegradable beverage bottles underscores the increasing role of biopolymers in mainstream consumer applications, positioning Kaneka as a key innovator in sustainable materials.

Braskem: Bio-based PE/EVA Dominance & Market Diversification

Braskem (Bio-based PE/EVA) remains a global leader in bio-based polyethylene production, with its green ethylene plant reaching a capacity of 275,000 tonnes per year as of May 2025. The company reported a significant 46% year-on-year increase in its recurring EBITDA in 2024 compared to 2023, reflecting strong performance across its portfolio, including biopolymers. The company has recently completed a 37% expansion of its green ethylene production capacity in Brazil by May 2025, bringing it to 275,000 tonnes per year, consolidating its dominance in bio-based polyolefins. Braskem’s launch of “Waxymer,” a new line of bio-based waxes for the cosmetics industry in 2024, demonstrates its strategy to diversify biopolymer applications beyond traditional packaging into high-value consumer products.

Biopolymers Market Share and Segmentation Analysis

By Biodegradable Polymers: Polylactic Acid (PLA) Leads, PHA Emerges as Fastest-Growing Segment

In 2025, PLA commands a 24.6% market share, establishing itself as the top biodegradable polymer thanks to its widespread adoption in packaging and textiles. Its advantages include excellent clarity, compostability, and compatibility with existing manufacturing lines. PHA stands out as the fastest-growing polymer with a CAGR of 10.2% due to its superior biodegradability and versatility, finding rapid uptake in single-use, food service, and medical applications. Meanwhile, PBAT and PBS are making steady gains in flexible packaging, while starch blends and cellulose-based polymers continue to expand in foodservice and agriculture, supported by increasing demand for compostable and renewable materials.

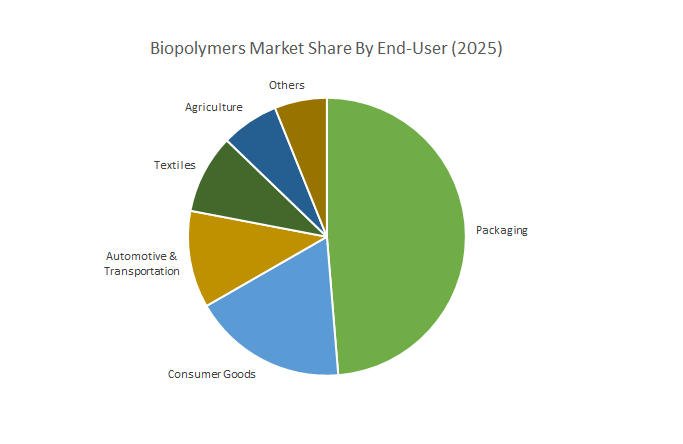

End-User Industry: Packaging Dominates, Automotive Accelerates Adoption

Packaging remains the dominant end-user, accounting for 48.7% of total biopolymer demand in 2025. The surge is driven by food and beverage brands seeking sustainable alternatives to conventional plastics, and by tightening global regulations on single-use packaging. The automotive and transportation sector is a standout for rapid growth, with biopolymers increasingly featured in lightweight vehicle interiors and structural components, reflecting the industry’s focus on fuel efficiency and eco-friendly design. Textiles and agriculture are also expanding, leveraging biopolymer-based solutions for compostable fabrics and biodegradable mulch films.

By Technology: Fermentation Dominates Production, Genetic Engineering Fuels Future Growth

Fermentation technologies lead biopolymer production, representing 39.6% of the market in 2025. This method’s scalability and cost efficiency have made it the go-to approach for producing PLA and PHA from renewable biomass. Genetic and metabolic engineering is the fastest-growing technology segment with a CAGR of 11.3% enabling customized polymer properties and higher yields, especially for high-value applications in packaging, healthcare, and specialty materials. Chemical synthesis remains essential, supporting PBAT and PBS output for flexible packaging and technical industrial uses.

United States Spearheading Biopolymers Innovation with Massive Investment and Regulatory Momentum

The United States continues to lead the global biopolymers industry through a powerful combination of government funding, world-class R&D, and high-profile commercialization. Federal investment surpassing $2.1 billion (2021–2024) from agencies such as the DOE and USDA has catalyzed rapid innovation in both feedstocks and end-use applications. Danimer Scientific's substantial investments, including its ongoing PHA scale-up efforts at its Kentucky facility and a significant $700 million project for a new PHA plant in Georgia, highlight the accelerating shift from lab-scale breakthroughs to full industrial capacity. The US is also home to PLA leaders like NatureWorks, whose materials power the fast-growing 3D printing sector, while companies such as Tepha Inc. are pioneering the use of PHA for high-value medical implants and bioresorbable sutures. In recent years, major brands like PepsiCo and Mars Wrigley have been piloting and investing in snack packaging made from plant-based and compostable materials like PHA, signaling a wider trend of major brands moving toward fully compostable, plant-based solutions. California’s landmark SB 54 law, which requires 100% of single-use packaging and plastic food service ware to be recyclable or compostable by 2032, is significantly pushing manufacturers and retailers nationwide to ramp up sustainable materials adoption, with brands required to enroll with Producer Responsibility Organizations by July 1, 2025, and submit their 2024 packaging data by August 31, 2025. These regulatory and investment dynamics, coupled with an active startup ecosystem, ensure the US will remain a global epicenter for biopolymer innovation and industrial scaling.

Germany Leading Europe’s Circular Biopolymers Economy with Industrial Integration and R&D

Germany stands as Europe’s industrial biotechnology powerhouse, renowned for translating advanced materials science into scalable, market-ready solutions for the circular economy. The Fraunhofer Institute’s breakthrough in enzyme-depolymerizable PLA, which demonstrates significantly accelerated breakdown under composting conditions, even achieving substantial depolymerization in days in controlled environments, sets a new benchmark for true circularity in plastics. The country’s biopolymers sector also benefits significantly from EU Horizon Europe funding, with substantial investments in bioeconomy and sustainable polymer R&D across the EU that directly fuel German innovation and commercialization. German industry is already deploying high-performance PBAT/PLA blends such as BASF’s Ecovio® in compostable films, food service packaging, and retail bags, while Covestro’s bio-based PUR is making inroads in automotive interiors and furniture. Siemens’ recent partnership with BASF for AI-optimized biopolymer production demonstrates the integration of digitalization and sustainability. In 2025, Germany continues to prepare for the full implementation of the EU’s Packaging and Packaging Waste Regulation (PPWR), which will ban non-recyclable plastics by 2030, further driving rapid adoption of compostable and recyclable biopolymers throughout manufacturing. These combined efforts cement Germany’s role as an R&D and production hub for circular biopolymer solutions.

China Scaling Biopolymers Production and Adoption for Textiles, Agriculture, and E-Commerce

China has established itself as the world’s biopolymer mass production powerhouse, driven by over $3 billion in state-backed investments since 2023. Leading companies such as Kingfa Science are rapidly expanding their biodegradable plastics output, with substantial annual capacities, including for PBAT, positioning them as dominant global players. A new wave of plants is accelerating the supply of PLA, PBS, and other next-generation biopolymers. Key Chinese applications include PLA for textiles (Zhejiang Hisun), PBS for agricultural mulch and biodegradable films (Sinopec), and an expanding role in flexible packaging and single-use products. E-commerce giants like Alibaba are driving rapid downstream adoption through ambitious targets and initiatives to integrate sustainable packaging, including biodegradable options, across a significant portion of their shipments by 2025, to reshape packaging logistics across Asia. China is also implementing strict regulatory standards, with new and updated national standards for biodegradable plastics raising the bar for compostability, safety, and market entry. With escalating investments and proactive government policies, China is poised to become the dominant global exporter and innovation hub for biopolymer materials across diverse sectors.

Netherlands Pioneering Circular Biopolymer Commercialization and Marine-Degradable Solutions

The Netherlands is at the vanguard of Europe’s circular economy transition, leveraging strong public and private investment to drive breakthrough commercialization of advanced biopolymers. Avantium’s active pursuit of significant funding, following a recent €10 million financing to secure short-term liquidity, for PEF (plant-based PET alternative) commercialization highlights the country’s leadership in next-generation bottle and packaging materials. Dutch companies are also advancing marine-degradable PHA with key players innovating for ocean-safe single-use products, while DSM’s bio-based polyamides power electronics and automotive applications with lower carbon footprints. The Netherlands is a hub for R&D on PEF bottles, which are now being piloted by Heineken for beer packaging with ongoing assessments and potential future rollout. In 2025, the Netherlands continues to be a key proponent of the expansion of the EU Single-Use Plastics Directive to include biopolymer certification, reinforcing the demand for traceability and proven end-of-life performance, further solidifying its role as a leading testbed for circular biopolymer solutions. These factors position the Netherlands as a leader in circular biopolymers, sustainable packaging, and cross-sector applications in the EU.

Japan Driving High-Performance and Marine-Degradable Biopolymer Adoption in Industry

Japan’s biopolymers industry is marked by a focus on high-performance, specialty materials and strong regulatory support for sustainable transformation. Backed by a $200 million Green Innovation Fund from METI, Japanese research institutes and companies such as Mitsubishi Chemical have pioneered products like BioPBS™, a heat-resistant biopolyester suitable for demanding food service and packaging applications. Toray’s PLA films for flexible electronics and Kaneka’s marine-degradable PHBH for fishing nets illustrate the country’s commitment to both innovation and environmental stewardship. Consumer goods leaders, including Sony, have adopted sugarcane-based PET for packaging, supporting a broader move toward renewable content in retail and electronics. The government’s upcoming 2025 targets and initiatives encouraging increased biopolymer use in consumer goods will further accelerate adoption, making Japan a prime market for advanced, sustainable, and functional biopolymers in Asia. In 2025, Japanese companies like Braskem (through its Tokyo office) are also actively expanding their bio-based polyethylene offerings in the Japanese market, aligning with the country's carbon neutrality goals. Japan’s unique combination of high-tech manufacturing, stringent regulation, and R&D investment ensures continued global relevance and market growth for biopolymers.

Biopolymers Market Report Scope

Biopolymers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$20 Billion

|

|

Market Size (2034)

|

$48.7 Billion

|

|

Market Growth Rate

|

10.4%

|

|

Segments

|

By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others), By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS - Thermoplastic Starch), Polycaprolactone (PCL), Cellulose-based Polymers (e.g., Cellulose Acetate), Others), By End-user (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others), By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others), By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (US), Novamont S.p.A. (Italy), BASF SE (Germany), Braskem S.A. (Brazil), TotalEnergies Corbion (Netherlands), Mitsubishi Chemical Group Corporation (Japan), Eastman Chemical Company (U.S.), Arkema S.A. (France), Versalis S.p.A. (Italy), BioLogiQ Inc. (U.S.), Danimer Scientific (U.S.), Polymateria Ltd. (UK), Plantic Technologies Limited (Australia), PTT MCC Biochem Company Limited, Total-Corbion PLA, KANEKA Corporation (Japan), and Others

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biopolymers Market Segmentation

By Non-Biodegradable Polymers

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Bio-Polypropylene (Bio-PP)

- Bio-Polyamides (Bio-PA)

- Others

By Biodegradable Polymers

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Polybutylene Succinate (PBS)

- Starch Blends (TPS - Thermoplastic Starch)

- Polycaprolactone (PCL)

- Cellulose-based Polymers (e.g., Cellulose Acetate)

- Others

By End-user

- Packaging

- Consumer Goods

- Automotive and Transportation

- Textiles

- Agriculture and Horticulture

- Building & Construction

- Others

By Technology

- Fermentation

- Chemical Synthesis

- Direct Extraction/Processing

- Genetic Engineering/Metabolic Engineering

- Others

By Feedstock

- Sugarcane

- Corn Starch

- Cellulose

- Vegetable Oils

- Lignin

- Algae

- Waste Streams

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Southeast Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Global Biopolymers Market

- NatureWorks LLC (US)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- Braskem S.A. (Brazil)

- TotalEnergies Corbion (Netherlands)

- Mitsubishi Chemical Group Corporation (Japan)

- Eastman Chemical Company (US)

- Arkema S.A. (France)

- Versalis S.p.A. (Italy)

- BioLogiQ Inc. (US)

- Danimer Scientific (US)

- Polymateria Ltd. (UK)

- Plantic Technologies Limited (Australia)

- PTT MCC Biochem Company Limited

- Total-Corbion PLA

- KANEKA Corporation (Japan)

* List Not Exhaustive

Methodology

The Global Biopolymers Market 2025–2034 report is built on a combination of primary and secondary research, including direct interviews with industry experts, executives, and technology developers across biopolymer manufacturers, end-user sectors, and supply chain participants to gather firsthand insights on market dynamics, innovations, and strategic developments. Secondary research drew from scientific publications, regulatory documents, patents, company reports, and sustainability disclosures to validate findings and track capacity expansions, technological progress, and regulatory changes. Market estimates were developed through both top-down and bottom-up modeling, factoring in production capacities, demand patterns, feedstock availability, and regulatory adoption rates across over 25 countries. Data was rigorously cross-checked and triangulated to ensure accuracy and consistency, while proprietary intelligence from USDAnalytics supported deeper analysis of competitive positioning, regional shifts, and emerging technologies, delivering a robust and actionable assessment of the biopolymers landscape.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Polymer Type (Biodegradable: PLA, PHA, PBAT, PBS, etc.; Non-Biodegradable: Bio-PE, Bio-PET, Bio-PP, Bio-PA), End-User Industry (Packaging, Consumer Goods, Automotive & Transportation, Textiles, Agriculture & Horticulture, Building & Construction, Others), Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic/Metabolic Engineering, Others), and Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others).

- Competitive Landscape: Profiles and strategies of 20+ leading companies, technology developers, and emerging innovators across the biopolymer value chain.

- Trends & Disruptions: In-depth analysis of regulatory frameworks, capacity expansions, marine-degradable innovations, enzymatic recycling, sustainability initiatives, and circular economy integration.

- Industry Dynamics: Coverage of market drivers, challenges, investment trends, feedstock supply shifts, sustainability impacts, and technological breakthroughs shaping the market through 2034.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Comprehensive narrative analysis, data tables, charts, and visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & Company Profiles

- Regulatory Landscape & Emerging Policy Tracker

- Executive Summary & Key Analyst Insights

- Custom Queries/Analyst Support Post Sale

Table of Contents

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Biopolymers Market Overview: Growth Drivers, Trends & Outlook (2025-2034)

2.1. Introduction to Biopolymers

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Intensifying Regulations on Conventional Plastics

2.3.2. Surging Consumer Preference for Eco-Friendly Solutions

2.3.3. Breakthrough Innovations in Polymer Technologies

2.4. Market Challenges and Restraints

3. Market Analysis: Biopolymers Industry Acceleration & Innovation

3.1. Product Innovation & Application Horizons

3.1.1. Penetration into Specialized End-Use Segments (e.g., 3D Printing, Agricultural Mulch)

3.1.2. Marine-Degradable Biopolymers

3.2. Capacity Expansions Driving Market Growth

3.2.1. Braskem: Sugarcane-based Bio-PE Output Expansion

3.2.2. TotalEnergies Corbion: PLA Facility Expansions

3.3. M&A and Strategic Partnerships Shaping Biopolymer Landscape

3.3.1. Solvay’s Acquisition of BioAmber’s Technology

3.3.2. Versalis’s Acquisition of Novamont

3.3.3. Cargill-Helm AG Joint Venture

3.4. Policy & Regulatory Catalysts for Biopolymer Adoption

3.4.1. European Union’s Single-Use Plastics Directive (SUPD)

3.4.2. U.S. BioPreferred Program

3.5. Technological Advancements Enhancing Biopolymer Performance

3.5.1. Enzyme-Enhanced PLA Degradation

3.5.2. Bio-based Polyamides from Food Waste

3.6. Sustainability Initiatives Reinforcing Green Credentials

3.6.1. Neste’s Bio-Naphtha Production

3.6.2. LanzaTech’s Carbon-Capture-Derived Biopolymers

4. Market Dynamics – Biopolymers Industry: Core Trends & Opportunities

4.1. Trend: Circular Economy Integration Accelerates Sustainable Growth

4.1.1. FMCG Player Adoption of Closed-Loop Systems

4.1.2. EU Circular Economy Action Plan Targets

4.1.3. Impact on Production Costs

4.1.4. Role of Advanced Technologies (Enzymatic Recycling, AI-Driven Sorting)

4.2. Opportunity: Enzymatic Recycling Infrastructure Unlocks High-Value Growth

4.2.1. Current Recycling Capabilities vs. Enzymatic Depolymerization

4.2.2. Projected Capacity Growth and Energy Efficiency

4.2.3. Cost Reduction and Carbon Savings Potential

4.2.4. Policy Support and New Investments

5. Competitive Landscape of the Global Biopolymer Market

5.1. Key Players and Market Competition Overview

5.2. Company Profiles & Strategies

5.2.1. NatureWorks LLC: PLA Biopolymer Leadership & Applications

5.2.2. TotalEnergies Corbion: PLA Innovation and Capacity Expansion

5.2.3. Danimer Scientific: PHA Biopolymers & Market Challenges

5.2.4. Kaneka Corporation: PHA-PHBH™ Advancements & Strategic Collaborations

5.2.5. Braskem: Bio-based PE/EVA Dominance & Market Diversification

5.2.6. Other Key Players

6. Biopolymers Market Share & Segmentation Analysis (2021- 2034)

6.1. Market Share Analysis By Non-Biodegradable Polymers

6.1.1. Bio-Polyethylene (Bio-PE)

6.1.2. Bio-Polyethylene Terephthalate (Bio-PET)

6.1.3. Bio-Polypropylene (Bio-PP)

6.1.4. Bio-Polyamides (Bio-PA)

6.1.5. Others

6.2. Market Share Analysis By Biodegradable Polymers

6.2.1. Polylactic Acid (PLA): Leading Share & Advantages

6.2.2. Polyhydroxyalkanoates (PHA): Fastest Growth & Versatility

6.2.3. Polybutylene Adipate Terephthalate (PBAT)

6.2.4. Polybutylene Succinate (PBS)

6.2.5. Starch Blends (TPS - Thermoplastic Starch)

6.2.6. Polycaprolactone (PCL)

6.2.7. Cellulose-based Polymers (e.g., Cellulose Acetate)

6.2.8. Others

6.3. Market Share Analysis By End-User

6.3.1. Packaging: Dominant End-User Adoption

6.3.2. Automotive and Transportation: Rapid Growth

6.3.3. Textiles

6.3.4. Agriculture and Horticulture

6.3.5. Building & Construction

6.3.6. Consumer Goods

6.3.7. Others

6.4. Market Share Analysis By Technology

6.4.1. Fermentation: Dominant Production Method

6.4.2. Genetic Engineering/Metabolic Engineering: Fastest Growing Technology

6.4.3. Chemical Synthesis

6.4.4. Direct Extraction/Processing

6.4.5. Others

6.5. Market Share Analysis By Feedstock

6.5.1. Sugarcane

6.5.2. Corn Starch

6.5.3. Cellulose

6.5.4. Vegetable Oils

6.5.5. Lignin

6.5.6. Algae

6.5.7. Waste Streams

6.5.8. Others

7. Geographic Analysis: Biopolymers Market Outlook by Country (2021- 2034)

7.1. North America

7.1.1. United States: Spearheading Biopolymers Innovation with Massive Investment and Regulatory Momentum

7.1.2. Canada: Steady Growth Driven by Sustainable Packaging Demand and Polysaccharide Dominance

7.1.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.2. Europe

7.2.1. Germany: Leading Europe’s Circular Biopolymers Economy with Industrial Integration and R&D

7.2.2. UK: Strong Growth Driven by Packaging Sector and Environmental Awareness

7.2.3. France: Increasing Adoption Driven by Stringent Regulations and Innovative Material Development

7.2.4. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.5. Italy: High Growth Trajectory with Increasing Adoption in Packaging and Textile Applications

7.2.6. Russia: Emerging Market with Growing Awareness and Demand for Eco-friendly Alternatives

7.2.7. Rest of Europe: Broad Adoption of Bio-based Biodegradables and Flexible Packaging Amidst Policy Shifts

7.2.8. Netherlands: Pioneering Circular Biopolymer Commercialization and Marine-Degradable Solutions

7.3. Asia Pacific

7.3.1. China: Scaling Biopolymers Production and Adoption for Textiles, Agriculture, and E-Commerce

7.3.2. Japan: Driving High-Performance and Marine-Degradable Biopolymer Adoption in Industry

7.3.3. India: Robust Growth Fueled by Evolving Consumer Demand and Favorable Regulatory Frameworks

7.3.4. South Korea: Advancing Sustainable Biopolymer Market with Focus on Packaging and Biomedical Applications

7.3.5. Australia: Accelerating Adoption in Packaging and Agriculture with Focus on Polysaccharides and PLA

7.3.6. Southeast Asia: Rising Demand in Flexible Packaging and Electronics, Bolstered by Government Initiatives

7.3.7. Rest of Asia: Significant Market Share and Fastest Growth Driven by Demand for Bio-based Packaging

7.4. South America

7.4.1. Brazil: Leading Regional Growth with Strong Presence in Bio-PE and PHA Production

7.4.2. Argentina: Emerging Market with Potential in Electrical & Electronics and Biodegradable Applications

7.4.3. Rest of South America: Increasing Adoption of PLA and PHA in Sustainable Packaging Solutions

7.5. Middle East and Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers in Construction and Agriculture

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging and Consumer Goods

7.5.3. Rest of Middle East: Expanding Market for Bioplastics in Packaging and Electrical & Electronics Sectors

7.5.4. South Africa: Growing Adoption of Biopolymers in Electrical & Electronics and Packaging

7.5.5. Egypt: Increasing Focus on Bioplastic Multi-Layer Films for Food Packaging and Delivery Services

7.5.6. Rest of Africa: Rising Demand for Eco-Friendly Plastics, Particularly in Packaging Industry

8. Biopolymers Market Size Outlook by Region (2025-2034)

8.1. North America Biopolymers Market Size Outlook to 2034

8.1.1. By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others)

8.1.2. By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others)

8.1.3. By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others)

8.1.4. By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others)

8.1.5. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

8.2. Europe Biopolymers Market Size Outlook to 2034

8.2.1. By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others)

8.2.2. By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others)

8.2.3. By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others)

8.2.4. By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others)

8.2.5. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

8.3. Asia Pacific Biopolymers Market Size Outlook to 2034

8.3.1. By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others)

8.3.2. By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others)

8.3.3. By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others)

8.3.4. By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others)

8.3.5. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

8.4. South America Biopolymers Market Size Outlook to 2034

8.4.1. By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others)

8.4.2. By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others)

8.4.3. By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others)

8.4.4. By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others)

8.4.5. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

8.5. Middle East and Africa Biopolymers Market Size Outlook to 2034

8.5.1. By Non-Biodegradable Polymers (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Bio-Polyamides (Bio-PA), Others)

8.5.2. By Biodegradable Polymers (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Polybutylene Succinate (PBS), Starch Blends (TPS), Polycaprolactone (PCL), Cellulose-Based Polymers, Others)

8.5.3. By End-User (Packaging, Consumer Goods, Automotive and Transportation, Textiles, Agriculture and Horticulture, Building & Construction, Others)

8.5.4. By Technology (Fermentation, Chemical Synthesis, Direct Extraction/Processing, Genetic Engineering/Metabolic Engineering, Others)

8.5.5. By Feedstock (Sugarcane, Corn Starch, Cellulose, Vegetable Oils, Lignin, Algae, Waste Streams, Others)

9. Company Profiles: Leading Players in the Biopolymers Market

9.1. NatureWorks LLC (US)

9.2. Novamont S.p.A. (Italy)

9.3. BASF SE (Germany)

9.4. Braskem S.A. (Brazil)

9.5. TotalEnergies Corbion (Netherlands)

9.6. Mitsubishi Chemical Group Corporation (Japan)

9.7. Eastman Chemical Company (US)

9.8. Arkema S.A. (France)

9.9. Versalis S.p.A. (Italy)

9.10. BioLogiQ Inc. (US)

9.11. Danimer Scientific (US)

9.12. Polymateria Ltd. (UK)

9.13. Plantic Technologies Limited (Australia)

9.14. PTT MCC Biochem Company Limited

9.15. KANEKA Corporation (Japan)

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.1.1. Geographic Coverage

11.1.2. Market Segmentation

11.1.3. Competitive Landscape Assessment

11.1.4. Key Trends & Disruptions

11.1.5. Industry Dynamics

11.1.6. Historic and Forecast Data Range

11.2. Deliverables

11.2.1. Full Market Research Report (PDF, Excel)

11.2.2. Country-Level Forecasts & Analysis

11.2.3. Segment-wise Revenue Projections

11.2.4. Competitive Benchmarking & Company Profiles

11.2.5. Regulatory Landscape & Emerging Policy Tracker

11.2.6. Executive Summary & Key Analyst Insights

11.2.7. Custom Queries/Analyst Support Post Sale

12. Disclaimer