Bioplastic Packaging Market Overview: Growth & Projections (2025–2034)

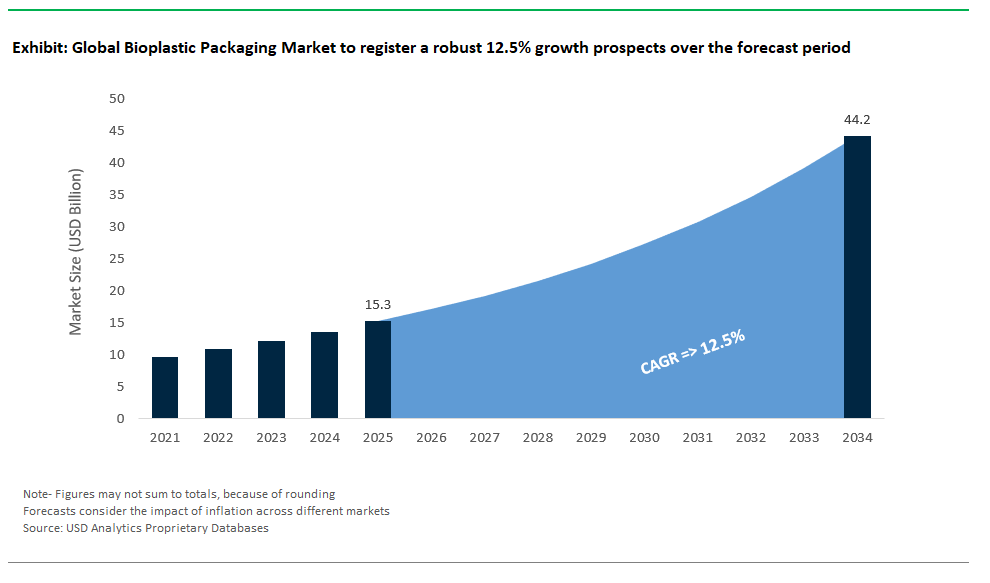

The Global Bioplastic Packaging Market is set to achieve robust expansion between 2025 and 2034, driven by mounting environmental regulations, surging demand for renewable packaging, and innovation across the packaging value chain. Industry forecasts project the global bioplastic packaging market to rise from USD 15.3 billion in 2025 to USD 44.2 billion by 2034, reflecting a strong CAGR of 12.5%. Growth is fueled by the widespread shift to sustainable packaging alternatives across food and beverages, consumer goods, pharmaceuticals, and industrial sectors, as well as advancements in both flexible and rigid packaging formats.

Leveraging the proprietary insights of USDAnalytics, the latest edition delivers a comprehensive evaluation and strategic outlook for the global bioplastic packaging market, monitoring trends and competitive moves in more than 25 countries and profiling leading packaging manufacturers By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others), By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others), By Packaging (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others).

This report provides a comprehensive analysis of the global bioplastic packaging market, uncovering the disruptive trends and next-generation technologies that are redefining packaging sustainability through 2034. It offers in-depth insights into raw material selection, packaging design evolution, and the commercialization of new bioplastic films and rigid formats. The study assesses the strategies of market leaders, details the regulatory drivers influencing packaging innovation, and highlights investments in production scale-up and brand collaboration. With granular segmentation by polymer type, packaging format, and end-use industry, this report equips manufacturers, suppliers, investors, and policy stakeholders with the intelligence needed to capture growth opportunities and advance sustainable packaging leadership worldwide.

Bioplastic Packaging Market Analysis: Trends, Innovation & Growth Drivers

The global bioplastic packaging market is experiencing transformative momentum as regulatory mandates, brand sustainability commitments, and technological breakthroughs converge to propel adoption across diverse packaging applications. Once confined to niche sustainability segments, bioplastic packaging is now scaling into mainstream markets, driven by significant investments, rapid technological advancement, and rising consumer demand for eco-friendly materials.

Product Innovation: Meeting Diverse Packaging Demands with Bioplastics

New product launches show how bioplastics are evolving to serve diverse and complex packaging needs, offering both sustainability and high performance. Amcor’s AmPrima™ PE Plus, a recyclable film with 30% bio-based content, is designed for snacks and frozen foods, providing a sustainable option that works within existing recycling systems, a key advantage for brands facing strict regulations. BASF’s ecovio® F2340, a compostable mulch film, doubles as biodegradable crop packaging, demonstrating how bioplastics are expanding beyond consumer goods into agricultural uses. Meanwhile, Mondi’s FunctionalBarrier Paper, a PLA-free recyclable solution for confectionery, reflects rising demand for paper-based packaging that ensures product protection while simplifying recycling processes.

Capacity Expansions: Signaling Confidence & Scaling for Mainstream Adoption

Rising demand for bioplastic packaging is reflected in aggressive capacity expansions worldwide, aimed at reducing costs through economies of scale and securing supply for large brand-owner contracts.

- TotalEnergies Corbion’s expansion of Luminy® PLA production to 250,000 tonnes per year in Thailand positions the company to serve surging demand in food and beverage applications across Asia and globally.

- Braskem’s 20% capacity boost for sugarcane-derived bio-PE, targeted at cosmetic bottles for brands like L'Oréal, underscores how personal care brands are integrating bio-based plastics into packaging portfolios to meet consumer sustainability expectations.

- Danimer Scientific’s commissioning of an 80,000-tonne PHA plant in Kentucky signals a major leap forward in domestic production of compostable resins, critical for meeting regulatory mandates like those emerging in U.S. states and major retailers’ sustainable packaging pledges.

Strategic Partnerships & M&A: Accelerating Bioplastic Packaging Market Development

Strategic collaborations and acquisitions are playing a pivotal role in scaling bioplastic packaging solutions and bringing new materials to market.

- Tetra Pak’s partnership with Corbion to develop PHA-based aseptic beverage cartons demonstrates how biopolymers are moving into demanding applications that require precise barrier properties, thermal stability, and regulatory approvals.

- Sealed Air’s acquisition of AFP Advanced Food Products to expand PHA-based tray production for retail giants like Walmart and Costco reflects the drive toward sustainable alternatives in high-volume food packaging segments.

- Novamont and Evertis’ collaboration on bio-based PET trays, already distributed across Carrefour stores in the EU, illustrates the commercialization of bio-based solutions that meet existing performance standards while delivering significant sustainability gains.

Regulatory Landscape: Driving Global Bioplastics Adoption in Packaging

Global policies are shifting from voluntary goals to strict mandates, driving rapid change in packaging material choices. The EU’s Packaging and Packaging Waste Regulation (PPWR) is forcing brands to adopt sustainable materials by setting ambitious targets, like requiring 65% recycled content for certain plastic packaging by 2040, and promoting bio-based plastics. The European Commission plans to review the progress of bio-based packaging technologies by 2028, potentially introducing new targets. In India, the ban on single-use plastics is pushing brands toward sustainable alternatives, showing how emerging markets are also driving bioplastics growth. Meanwhile, California’s SB 54 law mandates that all packaging be recyclable or compostable by 2032, creating significant opportunities for bioplastics in North America.

Technological Advances: Boosting Bioplastic Packaging Performance & Usability

Innovations are overcoming traditional limitations of bioplastics, making them suitable for more demanding applications. The Fraunhofer Institute has developed cellulose nanofiber (CNF)-PLA composites with excellent oxygen-barrier properties, crucial for extending the shelf life of oxygen-sensitive food products and competing with conventional multilayer films. The University of Cambridge’s pH-sensitive bioplastic labels change color when food spoils, introducing smart packaging that improves food safety and engages consumers. While these breakthroughs show strong potential, scaling production and reducing costs to match conventional plastics remain key challenges.

Brand Commitments: Shaping Market Shifts Towards Sustainable Packaging

Major brands are playing a pivotal role in shaping the bioplastics market. Nestlé is adopting sustainable packaging strategies, such as using recycled plastic for KitKat wrappers and sugarcane-derived bio-PE for lids and scoops in its nutrition products, balancing sustainability with recyclability for mass-market applications. Unilever is testing PHA-based ice cream tubs for Ben & Jerry’s in Europe, showing how bioplastics are becoming a competitive edge in premium markets where sustainability is a key consumer priority.

Bioplastic Packaging Industry Dynamics: Key Trends & Opportunities

Trend: Regulatory Tsunami Accelerating Global Bioplastic Adoption in Packaging

The global bioplastic packaging industry is undergoing rapid change as tough new regulations drive a shift toward sustainable packaging. The European Union’s 2024 Packaging and Packaging Waste Regulation (PPWR) sets ambitious targets for recycled content, promotes bio-based plastics, and mandates compostable packaging in certain categories by 2028. These rules impact over 27,000 companies, with fines reaching up to 4% of global revenue for non-compliance. Similarly, California’s SB 54 requires all packaging to be recyclable or compostable by 2032, along with a 25% cut in plastic packaging and a 65% recycling rate for single-use plastics, imposing penalties of up to $50,000 per day for violations. In Asia-Pacific, single-use plastic bans in India and Thailand, enacted in 2023, are driving strong demand for bioplastic alternatives and reshaping regional markets. These regulatory pressures are forcing brands worldwide to redesign products and supply chains quickly.

In response, major corporations are investing in bioplastics and sustainable packaging solutions. PepsiCo is targeting 97% reusable, recyclable, or compostable packaging by 2030 and reducing virgin plastic use. Unilever is restructuring supply chains and participating in projects like the UK’s Smart Sustainable Plastic Packaging initiative, which focuses on new recycling technologies for materials such as food-grade polypropylene. These efforts signal a fundamental shift in the packaging industry, where sustainability, compliance, and innovation are now key competitive factors.

Opportunity: Carbon-Negative PHA from Methane Capture & New Market Potential

A major growth opportunity in the bioplastic packaging market lies in carbon-negative polyhydroxyalkanoates (PHA) produced from captured methane. Breakthrough technologies are converting methane from landfills and agriculture, a greenhouse gas 25 times more potent than CO₂, into high-performance bioplastics. These processes can result in bioplastics with a net-negative carbon footprint, depending on the feedstock and technology used.

Governments are backing this innovation with strong incentives. The U.S. offers a 45Q tax credit of $85 per tonne of CO₂ sequestered for carbon capture projects, while the EU’s Innovation Fund provides significant grants for low-carbon technologies, including methane-to-plastic solutions. Brazil is also emerging as a key player, with companies like Braskem producing bio-based plastics from sugarcane ethanol and exploring methane-derived pathways using agricultural waste like sugarcane bagasse.

These financial incentives, coupled with rising demand for climate-positive packaging, position carbon-negative PHA as a crucial opportunity for future growth and sustainability in the global bioplastic packaging industry.

Bioplastic Packaging Market Competitive Landscape and Key Industry Players

The global bioplastic packaging industry is surging in 2024, fueled by rising demand for sustainable alternatives to fossil-based plastics amid tightening regulations, brand sustainability pledges, and shifting consumer preferences. From compostable solutions and bio-based polyolefins to innovative enzymatic recycling technologies, leading players are investing in capacity expansions, novel materials, and strategic partnerships. The competitive landscape reflects a dynamic market where bioplastic packaging is rapidly moving beyond niche applications into high-volume, mainstream markets across food, beverages, cosmetics, and fashion.

NatureWorks: Leading PLA-Based Packaging Solutions

NatureWorks remains a cornerstone of PLA-based packaging solutions, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability. This solution integrates Ingeo™ PLA biopolymer in the rigid capsule body, nonwoven filter, and multi-layer top lidding. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. NatureWorks continues to play a pivotal role in transitioning brands toward compostable alternatives, solidifying its position as a leader in renewable and high-performance packaging materials.

Braskem: Global Leader in Bio-based Polyethylene for Packaging

Braskem is firmly established as the global leader in bio-based polyethylene for packaging applications. Its green ethylene plant reached a capacity of 275,000 tonnes per year as of May 2025, following a significant 37% expansion. In October 2024, Braskem formed a joint venture with SCG Chemicals to establish a bio-ethylene project in Thailand, which will utilize bio-ethanol from sustainably sourced sugarcane, reinforcing its commitment to diversifying sustainable feedstocks and expanding global supply chains. Braskem’s I’m green™ PE is widely recognized for its carbon-negative footprint, strengthening its position as a leading sustainable alternative in packaging, consumer goods, and industrial applications globally. The company recently completed its first sale of circular PE (produced via chemical recycling) in South America, further diversifying its sustainable offerings for packaging.

Novamont: Pioneering Compostable Packaging with Mater-Bi® Technology

Novamont has carved out a leadership position in compostable packaging with its Mater-Bi® technology, widely used for compostable bags and agricultural films. Following its acquisition of BioBag Group in 2023, Novamont significantly expanded its influence in the compostable packaging market. Novamont remains a key innovator focused on sustainable feedstock sourcing and cost efficiency to enhance its competitiveness and appeal to brands seeking sustainable yet economically viable packaging solutions.

TIPA: Transforming Flexible Packaging with Home-Compostable Solutions

TIPA, based in Israel, is transforming the flexible packaging industry with home-compostable solutions that combine sustainability and premium performance. Renowned for offering compostable alternatives to traditional flexible plastics, TIPA is rapidly expanding as more brands pursue packaging that preserves product quality and brand image while aligning with environmental goals.

Carbios: Advancing Enzymatic Recycling for Bioplastic Packaging

Carbios (France) stands out for its pioneering work in the enzymatic recycling of PET, offering a circular solution for bioplastic packaging. In May 2024, Carbios announced its biorecycling plant is under construction in Longlaville, France, with operations expected to deliver significant quantities to customers in 2026 and a target annual capacity of 50,000 tonnes. In a significant development in May 2025, Carbios signed its first multi-year biorecycled PET sales contracts with L'Oréal and L'Occitane en Provence. The company’s long-standing partnerships with global giants like L’Oréal, Nestlé Waters, PepsiCo, and Suntory Beverage & Food Europe through its consortium underscore the market’s strong interest in enzymatic recycling as a viable path to achieving closed-loop packaging systems and reducing plastic waste.

BASF: Expanding Bioplastic Footprint with Ecovio® & Circular Solutions

BASF (Germany) continues to advance its bioplastic footprint with ecovio®, a PBAT/PLA blend used extensively in certified compostable bags and flexible packaging. In February 2024, BASF launched its ChemCycling™ initiative in the US, processing feedstock from plastic waste at its Port Arthur, TX facility to produce ISCC+ certified advanced recycled building blocks, further aligning its portfolio with circular economy principles by converting plastic waste into new packaging resins. BASF continues to demonstrate how global reach and advanced chemical innovation are propelling bioplastics into diverse and high-demand markets worldwide. Looking ahead to K 2025 (October 2025), BASF plans to showcase its commitment to #OurPlasticsJourney, highlighting a reduced Product Carbon Footprint (rPCF) portfolio and the use of biomass balance approach for biopolymers like ecovio® and ecoflex® BMB, further reinforcing its sustainable packaging solutions.

Bioplastic Packaging Market Share & Segmentation Analysis

By Packaging Type: Flexible Packaging Leads the Market, Rigid Packaging Maintains Strong Demand

In 2025, flexible packaging dominates the bioplastic packaging landscape with a 58.6% market share, reflecting strong demand for pouches, films, and wraps in food, beverages, and e-commerce. The segment’s growth is propelled by the rise of single-serve convenience, online grocery, and sustainable snack packaging. Rigid packaging remains a substantial segment, supporting robust demand for bioplastic bottles, trays, and clamshells, particularly in food service and ready-to-eat applications. Notably, flexible packaging is the fastest-growing segment with a CAGR of 13.6%, driven by its adaptability across industries and rapid consumer adoption.

.png)

By End-Use Industry: Food & Beverages Dominate, Pharmaceutical Packaging Grows Fastest

Food & beverages is the dominant industry of bioplastic packaging demand in 2025, with fresh produce, snacks, and beverage brands rapidly shifting to bioplastics to meet consumer expectations and regulatory standards for sustainable packaging. Pharmaceutical packaging is the fastest-growing end-use sector with a CAGR of 13.2%, fueled by the adoption of PLA and PHA in biodegradable blister packs, pill containers, and advanced drug delivery systems. Consumer goods, including cosmetics and electronics, are also expanding their use of bioplastic wraps and containers, aligning with global sustainability trends.

Germany Accelerating Bioplastic Packaging Innovation and Investment for EU Circular Economy

Germany is emerging as a powerhouse in the global bioplastic packaging industry, blending robust production capacity, policy leadership, and pioneering product development. In 2024, the nation's bioplastic production capacity contributed significantly to Europe's total of approximately 670,000 tons, with the broader European bioplastics market projected to grow at an 18% CAGR from 2025-2030. Major brands like BASF are driving innovation through products such as “Ecoflex,” a PBAT resin certified for compostable food packaging and now widely adopted across Europe. Germany’s substantial federal investment in bioeconomy initiatives, exceeding €2 billion, underpins the country’s continued leadership in R&D, infrastructure, and commercial rollout of advanced bioplastic materials. New policy measures, notably the EU’s Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025 and will apply from August 2026, mandate that all packaging must be recyclable by 2030, with specific compostability requirements for certain formats and bans on non-recyclable plastics. This dramatically accelerates industry transformation. Siemens’ AI-optimized production for PHA-based pouches demonstrates how digitalization and sustainability converge in German industry. In 2025, German material suppliers are actively launching new flexible film grades specifically designed for improved recyclability and compostability, targeting the food packaging sector to help brands comply with upcoming PPWR requirements. Furthermore, several German research consortia are receiving increased funding to develop advanced sorting technologies for bioplastic waste, crucial for achieving circularity goals. These advances make Germany the technology and regulatory anchor for the biopolymer packaging sector, influencing product design, process innovation, and sustainability standards worldwide.

United States Leading Bioplastic Packaging Growth with Large-Scale Production and Regulatory Momentum

The United States is the fastest-growing market for bioplastic packaging, backed by large-scale investments, technological leadership, and a powerful policy shift toward circular materials. Production in 2024 saw significant growth, with the North American region accounting for approximately 20% of global bioplastic production capacity. NatureWorks, the nation’s flagship producer, expanded its Nebraska PLA plant, maintaining a significant capacity (over 140,000 tons/year), supporting widespread adoption in food packaging and foodservice applications. Danimer Scientific’s FDA-approved PHA is enabling new compostable solutions for both rigid and flexible packaging, with growing use in quick-service restaurants and brand packaging. The regulatory landscape is also rapidly evolving: California’s SB 54 mandates that all packaging in the state be 100% recyclable or compostable by 2032, setting a new national benchmark. In 2025, several states are considering or finalizing legislation mirroring California's SB 54, indicating a broader federal push towards harmonized bioplastic packaging standards. Major consumer brands with significant U.S. operations are announcing new packaging pilot programs featuring advanced bioplastics, with some committing to public reporting of their bioplastic usage percentages by year-end to demonstrate sustainability progress. As the U.S. government and private sector invest further in capacity and scale, the country is poised to drive both innovation and global market growth in bioplastic packaging.

China Dominating Global Bioplastic Packaging Supply and Driving Rapid Market Growth

China leads the world in bioplastic packaging production, accounting for approximately 45% of global bioplastics production capacity in 2024, projected for continued high growth. Major players such as Kingfa (with significant PBAT capacities aimed at meeting growing global demand) and Sinopec (actively expanding its large-scale biodegradable plastic production) are scaling output to meet both domestic and global demand. China’s stringent “plastic ban” policies, phasing out non-degradable packaging across retail, e-commerce, and foodservice, have driven unprecedented adoption of certified bioplastic solutions. Local authorities enforce these transitions through standards such as GB Standard 38507-2023, ensuring product safety and compostability. A key development in 2025 is the full implementation of nationwide bans on certain single-use non-degradable plastics across major e-commerce and retail sectors, leading to a surge in demand for certified compostable and biodegradable packaging solutions. Several large-scale bioplastic manufacturing complexes are expected to commence full commercial operations in 2025, further solidifying China's dominance in global supply. China’s combination of massive production capacity, policy enforcement, and cost-competitive materials is making it the preferred sourcing hub for multinational brands seeking scalable and sustainable packaging options.

Italy Advancing Compostable Bioplastic Packaging for Food, Retail, and Agriculture

Italy remains a pioneer and major supplier of compostable bioplastic packaging in Europe, with its compostable packaging market valued at USD 148 billion in 2024 and projected to grow at a CAGR of 19.19% from 2025 to 2032. Novamont’s Mater-Bi is the mandated standard for Italian produce bags, widely adopted by retailers and foodservice operators. The nation’s policy environment supports rapid bioplastics deployment, with a strong network of industrial composting plants (over 100 nationwide) ensuring end-of-life treatment infrastructure and compliance. In 2025, Italian regional governments are launching new initiatives to incentivize local businesses, especially small and medium enterprises (SMEs), to switch to certified compostable packaging for fresh produce and prepared foods, leveraging Italy's advanced composting infrastructure. There is also an increased focus on developing home-compostable packaging solutions for niche food markets, driven by consumer demand. Italy’s focus on home compostable, certified, and high-performance packaging solutions makes it a benchmark market for circularity and food safety in the EU bioplastics landscape.

Netherlands Advancing Bioplastic Innovation and Commercial Scale for Circular Packaging

The Netherlands has established itself as a European innovation hub for bioplastic packaging, specializing in plant-based and recyclable solutions. Production is estimated at around 100,000 tons per year in 2024, anchored by global leaders such as Avantium and Corbion. Avantium’s new PEF plant, supported by EU grants, which completed construction in 2024 and is targeting first commercial production in 2025, marks the world’s first commercial-scale deployment of this bio-PET alternative, offering dramatic improvements in oxygen barrier and shelf life for food and beverage packaging. The EU Single-Use Plastics (SUP) Directive and national policies are accelerating brand and retailer adoption of certified bioplastics, with the Netherlands providing a model for innovation, certification, and closed-loop circularity in packaging supply chains. A key 2025 development sees Dutch research institutions and industry consortia focusing on optimizing the sorting and recycling of multi-material bioplastic packaging, aiming to establish viable closed-loop systems. Furthermore, several major Dutch retail chains are expanding their "bring-your-own-container" initiatives and offering more pre-packaged products in refillable or certified compostable bioplastic options, driven by the SUP Directive's reduction targets.

Thailand Leading ASEAN in Bioplastic Packaging Production and Export

Thailand is rapidly becoming the leading ASEAN supplier of bioplastic packaging, with production reaching around 400,000 tons annually and a dominant export position across Asia-Pacific. The industry focuses primarily on PLA and PBS grades, with PTT MCC Biochem providing advanced solutions for global brands such as Unilever and Nestlé. Supported by the government’s BCG (Bio-Circular-Green) Economy policy and a $1 billion fund dedicated to bioplastics, Thailand’s industry is scaling capacity, expanding export markets, and strengthening its role as a regional production hub for sustainable packaging. In 2025, Thailand is actively seeking foreign direct investment in large-scale bioplastic feedstock production facilities, particularly for sugarcane-based ethanol, to further enhance its competitive advantage as an export hub. There is also increased emphasis on developing bioplastic packaging for the rapidly growing e-commerce sector within ASEAN, with collaborations between Thai manufacturers and regional online retailers.

Brazil Pioneering Sugarcane-Based Bioplastics and Expanding Global Partnerships

Brazil continues to lead South America’s bioplastic packaging industry, producing around 150,000 tons per year in 2024, with a strong emphasis on sugarcane-based polyethylene (bio-PE). Braskem remains the global leader in this field, supplying bio-PE for major international beverage brands such as Coca-Cola. Recent partnerships, including a joint venture with SCG to expand bio-polyethylene production in Thailand and commercialize bio-based PE using EtE EverGreen™ technology, are boosting Brazil’s presence in global packaging supply chains. The “Plastic Free Amazon” initiative and growing demand for sustainable materials in food and beverage make Brazil a rising force in bioplastic innovation and environmental stewardship. A key 2025 development for Brazil involves accelerated R&D into converting other agricultural residues, beyond sugarcane, into advanced bioplastics, aiming to diversify feedstock sources and create new revenue streams for rural communities. Braskem is also anticipated to announce further capacity expansions for its bio-PE lines to meet increasing global demand from brands committed to reducing their carbon footprint.

India Driving High-Growth Bioplastic Packaging for Food and Retail Applications

India is emerging as a fast-growing market for bioplastic packaging, with production exceeding 100,000 tons in 2024 and an impressive CAGR of 30%. The market is focused on starch- and PLA-based solutions for retail, foodservice, and e-commerce packaging. Key players like Reliance have launched pilot plants for bio-PET, and new EPR (Extended Producer Responsibility) credits for bioplastic adoption are accelerating investments from major brands and packaging suppliers. With government support for sustainable materials and the rollout of national plastic waste bans, India is on a strong trajectory to become a leading market for scalable, certified bioplastic packaging. In 2025, India is intensifying efforts to establish a robust framework for certified compostable packaging, including clear labeling guidelines and a nationwide network of industrial composting facilities, to facilitate widespread adoption. Major Indian food delivery platforms are also expected to scale up their use of bioplastic packaging for meal deliveries, driven by consumer preference for sustainable options and government incentives.

Bioplastic Packaging Market Report Scope

Bioplastic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.3 Billion

|

|

Market Size (2034)

|

$44.2 Billion

|

|

Market Growth Rate

|

12.5%

|

|

Segments

|

By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others), By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others), By Packaging (Flexible Packaging, Rigid Packaging, B End-Use Industry, Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (U.S.), Novamont S.p.A. (Italy), Braskem S.A. (Brazil), BASF SE (Germany), TotalEnergies Corbion (Netherlands/France), Danimer Scientific (U.S.), Mitsubishi Chemical Group Corporation (Japan), Avantium (Netherlands), CJ Biomaterials Inc. (South Korea), Plantic Technologies Limited (Australia), Amcor Plc (Australia/U.S.), Mondi Group (Austria/UK), Sealed Air Corporation (U.S.), Alpla Group (Austria), Constantia Flexibles (Austria), Huhtamaki Oyj (Finland), Tetra Pak (Switzerland), Crown Holdings Inc. (U.S.), International Paper (U.S.), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bioplastic Packaging Market Segmentation

By Non-Biodegradable Plastics for Packaging

- Bio-Polyethylene (Bio-PE)

- Bio-Polyethylene Terephthalate (Bio-PET)

- Bio-Polypropylene (Bio-PP)

- Polyethylene Furanoate (PEF)

- Bio-Polyamides (Bio-PA)

- Others

By Biodegradable Plastics for Packaging

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Polybutylene Adipate Terephthalate (PBAT)

- Starch Blends / Thermoplastic Starch (TPS)

- Polybutylene Succinate (PBS) & Copolymers (PBSA)

- Cellulose-based Films

- Polycaprolactone (PCL)

- Others

By Packaging

- Flexible Packaging

- Films

- Bags

- Pouches & Sachets

- Wraps & Lidding Films

- Rigid Packaging

- Bottles & Jars

- Trays & Containers

- Clamshells

- Cups

- Lids & Caps

- Blister Packs & Clamshells

B End-Use Industry

- Food & Beverages

- Consumer Goods

- Industrial Packaging

- Pharmaceutical Packaging

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Bioplastic Packaging Industry

- NatureWorks LLC (US)

- Novamont S.p.A. (Italy)

- Braskem S.A. (Brazil)

- BASF SE (Germany)

- TotalEnergies Corbion (Netherlands/France)

- Danimer Scientific (US)

- Mitsubishi Chemical Group Corporation (Japan)

- Avantium (Netherlands)

- CJ Biomaterials Inc. (South Korea)

- Plantic Technologies Limited (Australia)

- Amcor Plc (Australia/U.S.)

- Mondi Group (Austria/UK)

- Sealed Air Corporation (US)

- Alpla Group (Austria)

- Constantia Flexibles (Austria)

- Huhtamaki Oyj (Finland)

- Tetra Pak (Switzerland)

- Crown Holdings Inc. (US)

- International Paper (US)

*List not Exhaustive

Methodology

The Global Bioplastic Packaging Market 2025–2034 report is developed through an integrated research approach combining extensive primary and secondary research. Primary insights were collected via interviews with packaging manufacturers, bioplastic producers, technology innovators, and sustainability leaders to understand trends, capacity developments, regulatory impacts, and strategic market shifts. Secondary research drew from scientific literature, patents, regulatory updates, company disclosures, sustainability reports, and trade data to validate and enhance primary findings. Market sizing was conducted through both top-down and bottom-up modeling, factoring in production capacities, consumption trends, technology penetration, and regulatory adoption across more than 25 countries. All data was rigorously cross-verified and triangulated to ensure accuracy and consistency. Proprietary analytics from USDAnalytics added deeper layers of insight into competitive dynamics, emerging technologies, and scenario-based forecasts, delivering a robust, actionable perspective on the evolving bioplastic packaging landscape.

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by Polymer Type (Biodegradable: PLA, PHA, PBAT, PBS, TPS, etc.; Non-Biodegradable: Bio-PE, Bio-PET, Bio-PP, PEF, Bio-PA, etc.), Packaging Type (Flexible Packaging: films, bags, pouches, wraps, lidding films; Rigid Packaging: bottles, trays, containers, clamshells, cups, lids, blister packs), and End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others).

- Competitive Landscape: Profiles and strategies of 20+ leading companies, material innovators, and packaging converters in the bioplastic packaging space.

- Trends & Disruptions: Deep dive into regulatory frameworks, capacity expansions, smart packaging innovations, carbon-negative bioplastics, sustainability initiatives, and circular economy integration.

- Industry Dynamics: Analysis of market drivers, challenges, investment trends, feedstock innovations, technological breakthroughs, and evolving brand strategies shaping the market through 2034.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Comprehensive narrative insights, data tables, charts, and visualizations.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & Company Profiles

- Regulatory Landscape & Emerging Policy Tracker

- Executive Summary & Key Analyst Insights

- Custom Queries/Analyst Support Post Sale

Table of Contents

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Bioplastic Packaging Market Overview: Growth & Projections (2025–2034)

2.1. Introduction to Bioplastic Packaging

2.2. Market Valuation and Growth Projections (2025-2034)

2.2.1. Historical Market Size (2021-2024)

2.2.2. Current Market Size (2025)

2.2.3. Forecasted Market Size and CAGR (2025-2034)

2.3. Key Market Drivers

2.3.1. Mounting Environmental Regulations

2.3.2. Surging Demand for Renewable Packaging

2.3.3. Innovation Across the Packaging Value Chain

2.3.4. Widespread Shift to Sustainable Packaging Alternatives

2.4. Market Challenges and Restraints

3. Bioplastic Packaging Market Analysis: Trends, Innovation & Growth Drivers

3.1. Product Innovation: Meeting Diverse Packaging Demands with Bioplastics

3.1.1. Recyclable PE Packaging with Bio-Based Content (Amcor AmPrima™ PE Plus)

3.1.2. Compostable Mulch Film for Crop Packaging (BASF ecovio® F2340)

3.1.3. PLA-Free Recyclable Paper for Confectionery (Mondi FunctionalBarrier Paper)

3.2. Capacity Expansions: Signaling Confidence & Scaling for Mainstream Adoption

3.2.1. TotalEnergies Corbion: Expanding Luminy® PLA Production

3.2.2. Braskem: Boosting Sugarcane-Derived Bio-PE Capacity

3.2.3. Danimer Scientific: Commissioning of PHA Plant in Kentucky

3.3. Strategic Partnerships & M&A: Accelerating Bioplastic Packaging Market Development

3.3.1. Tetra Pak’s Partnership with Corbion for PHA-Based Aseptic Beverage Cartons

3.3.2. Sealed Air’s Acquisition of AFP Advanced Food Products for PHA-Based Trays

3.3.3. Novamont and Evertis’ Collaboration on Bio-Based PET Trays

3.4. Regulatory Landscape: Driving Global Bioplastics Adoption in Packaging

3.4.1. EU’s Packaging and Packaging Waste Regulation (PPWR)

3.4.2. India’s Ban on Single-Use Plastics

3.4.3. California’s SB 54 Law for Packaging Recyclability/Compostability

3.5. Technological Advances: Boosting Bioplastic Packaging Performance & Usability

3.5.1. Cellulose Nanofiber (CNF)-PLA Composites for Oxygen Barrier (Fraunhofer Institute)

3.5.2. pH-Sensitive Bioplastic Labels for Food Spoilage (University of Cambridge)

3.6. Brand Commitments: Shaping Market Shifts Towards Sustainable Packaging

3.6.1. Nestlé’s Sustainable Packaging Strategies for KitKat and Nutrition Products

3.6.2. Unilever’s Testing of PHA-Based Ice Cream Tubs for Ben & Jerry’s

4. Bioplastic Packaging Industry Dynamics: Key Trends & Opportunities

4.1. Trend: Regulatory Tsunami Accelerating Global Bioplastic Adoption in Packaging

4.1.1. European Union’s 2024 Packaging and Packaging Waste Regulation (PPWR)

4.1.2. California’s SB 54 Requirements and Penalties

4.1.3. Single-Use Plastic Bans in Asia-Pacific (India, Thailand)

4.1.4. Corporate Investments and Supply Chain Restructuring (PepsiCo, Unilever)

4.2. Opportunity: Carbon-Negative PHA from Methane Capture & New Market Potential

4.2.1. Methane Conversion to High-Performance Bioplastics

4.2.2. Potential for Net-Negative Carbon Footprint

4.2.3. Government Incentives (U.S. 45Q Tax Credit, EU Innovation Fund)

4.2.4. Role of Key Players (Braskem) in Methane-Derived Pathways

5. Competitive Landscape: Leading Bioplastic Packaging Manufacturers

5.1. Key Players and Market Competition Overview

5.2. Company Profiles & Strategies (Overview)

5.2.1. NatureWorks: Leading PLA-Based Packaging Solutions

5.2.2. Braskem: Global Leader in Bio-Based Polyethylene for Packaging

5.2.3. Novamont: Pioneering Compostable Packaging with Mater-Bi® Technology

5.2.4. TIPA: Transforming Flexible Packaging with Home-Compostable Solutions

5.2.5. Carbios: Advancing Enzymatic Recycling for Bioplastic Packaging

5.2.6. BASF: Expanding Bioplastic Footprint with Ecovio® & Circular Solutions

5.2.7. Other Key Players (Detailed profiles in Chapter 9)

6. Bioplastic Packaging Market Share and Segmentation Analysis

6.1. By Packaging Type

6.1.1. Flexible Packaging

6.1.1.1. Films

6.1.1.2. Bags

6.1.1.3. Pouches & Sachets

6.1.1.4. Wraps & Lidding Films

6.1.2. Rigid Packaging

6.1.2.1. Bottles & Jars

6.1.2.2. Trays & Containers

6.1.2.3. Clamshells

6.1.2.4. Cups

6.1.2.5. Lids & Caps

6.1.2.6. Blister Packs & Clamshells

6.2. By End-Use Industry

6.2.1. Food & Beverages

6.2.2. Consumer Goods

6.2.3. Industrial Packaging

6.2.4. Pharmaceutical Packaging

6.2.5. Others

6.3. By Non-Biodegradable Plastics for Packaging

6.3.1. Bio-Polyethylene (Bio-PE)

6.3.2. Bio-Polyethylene Terephthalate (Bio-PET)

6.3.3. Bio-Polypropylene (Bio-PP)

6.3.4. Polyethylene Furanoate (PEF)

6.3.5. Bio-Polyamides (Bio-PA)

6.3.6. Others

6.4. By Biodegradable Plastics for Packaging

6.4.1. Polylactic Acid (PLA)

6.4.2. Polyhydroxyalkanoates (PHA)

6.4.3. Polybutylene Adipate Terephthalate (PBAT)

6.4.4. Starch Blends / Thermoplastic Starch (TPS)

6.4.5. Polybutylene Succinate (PBS) & Copolymers (PBSA)

6.4.6. Cellulose-based Films

6.4.7. Polycaprolactone (PCL)

6.4.8. Others

7. Geographic Analysis: Bioplastic Packaging Market Outlook by Country (2021- 2034)

7.1. North America

7.1.1. United States: Leading Bioplastic Packaging Growth with Large-Scale Production and Regulatory Momentum

7.1.2. Canada: Steady Growth Driven by Sustainable Packaging Demand and Polysaccharide Dominance

7.1.3. Mexico: Rapid Expansion Fueled by Sustainable Packaging and F&B Sector Demand

7.2. Europe

7.2.1. Germany: Accelerating Bioplastic Packaging Innovation and Investment for EU Circular Economy

7.2.2. UK: Strong Growth Driven by Packaging Sector and Environmental Awareness

7.2.3. France: Increasing Adoption Driven by Stringent Regulations and Innovative Material Development

7.2.4. Spain: Significant Market Expansion Led by Polysaccharide and PLA Adoption

7.2.5. Italy: Advancing Compostable Bioplastic Packaging for Food, Retail, and Agriculture

7.2.6. Russia: Emerging Market with Growing Awareness and Demand for Eco-friendly Alternatives

7.2.7. Rest of Europe: Broad Adoption of Bio-based Biodegradables and Flexible Packaging Amidst Policy Shifts

7.2.8. Netherlands: Advancing Bioplastic Innovation and Commercial Scale for Circular Packaging

7.3. Asia Pacific

7.3.1. China: Dominating Global Bioplastic Packaging Supply and Driving Rapid Market Growth

7.3.2. Japan: Developing High-Performance Biopolymer Films for Packaging & Electronics

7.3.3. India: Driving High-Growth Bioplastic Packaging for Food and Retail Applications

7.3.4. South Korea: Advancing Sustainable Biopolymer Market with Focus on Packaging and Biomedical Applications

7.3.5. Australia: Accelerating Adoption in Packaging and Agriculture with Focus on Polysaccharides and PLA

7.3.6. Southeast Asia: Rising Demand in Flexible Packaging and Electronics, Bolstered by Government Initiatives

7.3.7. Rest of Asia: Significant Market Share and Fastest Growth Driven by Demand for Bio-based Packaging

7.4. South America

7.4.1. Brazil: Pioneering Sugarcane-Based Bioplastics and Expanding Global Partnerships

7.4.2. Argentina: Emerging Market with Potential in Electrical & Electronics and Biodegradable Applications

7.4.3. Rest of South America: Increasing Adoption of PLA and PHA in Sustainable Packaging Solutions

7.5. Middle East and Africa

7.5.1. Saudi Arabia: Developing Market for Lignin-based Biopolymers in Construction and Agriculture

7.5.2. UAE: Rapidly Growing Demand for Sustainable Packaging and Consumer Goods

7.5.3. Rest of Middle East: Expanding Market for Bioplastics in Packaging and Electrical & Electronics Sectors

7.5.4. South Africa: Growing Adoption of Biopolymers in Electrical & Electronics and Packaging

7.5.5. Egypt: Increasing Focus on Bioplastic Multi-Layer Films for Food Packaging and Delivery Services

7.5.6. Rest of Africa: Rising Demand for Eco-Friendly Plastics, Particularly in Packaging Industry

8. Bioplastic Packaging Market Size Outlook by Region (2025-2034)

8.1. North America Bioplastic Packaging Market Size Outlook to 2034

8.1.1. By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others)

8.1.2. By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others)

8.1.3. By Packaging (Flexible Packaging, Rigid Packaging)

8.1.4. By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

8.2. Europe Bioplastic Packaging Market Size Outlook to 2034

8.2.1. By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others)

8.2.2. By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others)

8.2.3. By Packaging (Flexible Packaging, Rigid Packaging)

8.2.4. By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

8.3. Asia Pacific Bioplastic Packaging Market Size Outlook to 2034

8.3.1. By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others)

8.3.2. By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others)

8.3.3. By Packaging (Flexible Packaging, Rigid Packaging)

8.3.4. By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

8.4. South America Bioplastic Packaging Market Size Outlook to 2034

8.4.1. By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others)

8.4.2. By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others)

8.4.3. By Packaging (Flexible Packaging, Rigid Packaging)

8.4.4. By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

8.5. Middle East and Africa Bioplastic Packaging Market Size Outlook to 2034

8.5.1. By Non-Biodegradable Plastics for Packaging (Bio-Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), Bio-Polypropylene (Bio-PP), Polyethylene Furanoate (PEF), Bio-Polyamides (Bio-PA), Others)

8.5.2. By Biodegradable Plastics for Packaging (Polylactic Acid (PLA), Polyhydroxyalkanoates (PHA), Polybutylene Adipate Terephthalate (PBAT), Starch Blends / Thermoplastic Starch (TPS), Polybutylene Succinate (PBS) & Copolymers (PBSA), Cellulose-based Films, Polycaprolactone (PCL), Others)

8.5.3. By Packaging (Flexible Packaging, Rigid Packaging)

8.5.4. By End-Use Industry (Food & Beverages, Consumer Goods, Industrial Packaging, Pharmaceutical Packaging, Others)

9. Company Profiles: Leading Players in the Bioplastic Packaging Industry

9.1. NatureWorks LLC (US)

9.2. Novamont S.p.A. (Italy)

9.3. Braskem S.A. (Brazil)

9.4. BASF SE (Germany)

9.5. TotalEnergies Corbion (Netherlands/France)

9.6. Danimer Scientific (US)

9.7. Mitsubishi Chemical Group Corporation (Japan)

9.8. Avantium (Netherlands)

9.9. CJ Biomaterials Inc. (South Korea)

9.10. Plantic Technologies Limited (Australia)

9.11. Amcor Plc (Australia/U.S.)

9.12. Mondi Group (Austria/UK)

9.13. Sealed Air Corporation (US)

9.14. Alpla Group (Austria)

9.15. Constantia Flexibles (Austria)

9.16. Huhtamaki Oyj (Finland)

9.17. Tetra Pak (Switzerland)

9.18. Crown Holdings Inc. (US)

9.19. International Paper (US)

10. Research Methodology

10.1. Data Collection Approach (Primary & Secondary Research)

10.2. Market Sizing and Forecasting Model

10.3. Data Validation and Triangulation

10.4. Proprietary Intelligence & Tools (USDAnalytics)

11. Report Scope & Deliverables

11.1. Report Scope

11.1.1. Geographic Coverage

11.1.2. Market Segmentation

11.1.3. Competitive Landscape Assessment

11.1.4. Key Trends & Disruptions

11.1.5. Industry Dynamics

11.1.6. Historic and Forecast Data Range

11.2. Deliverables

11.2.1. Full Market Research Report (PDF, Excel)

11.2.2. Country-Level Forecasts & Analysis

11.2.3. Segment-wise Revenue Projections

11.2.4. Competitive Benchmarking & Company Profiles

11.2.5. Regulatory Landscape & Emerging Policy Tracker

11.2.6. Executive Summary & Key Analyst Insights

11.2.7. Custom Queries/Analyst Support Post Sale

12. Disclaimer