Market Overview: Sustainability and Digitalization Reshape Cosmetic Bottles Packaging Market Valued at $33.9 Billion in 2025

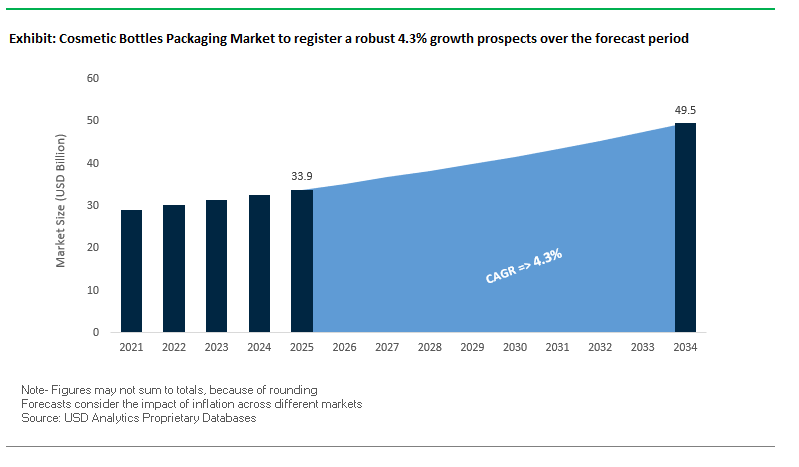

The Global Cosmetic Bottles Packaging Market is valued at USD 33.9 billion in 2025 and is forecasted to reach USD 49.5 billion by 2034, expanding at a CAGR of 4.3%. This growth trajectory is not merely volume-driven; it reflects a structural transformation in packaging strategies as the sector navigates sustainability compliance, e-commerce logistics, and shifting consumer behavior.

Packaging is no longer a downstream afterthought; it has become a strategic lever for brand equity and regulatory alignment. With 70%+ of Western consumers actively preferring recyclable or reusable formats, procurement and innovation teams are under pressure to prioritize PCR plastics, lightweight glass, and refill systems. Meanwhile, carbon-reduction commitments are steering material sourcing and manufacturing investments toward bio-based polymers and electrified glass furnaces.

Key Insights for Industry Stakeholders

- MV (2025): USD 33.9 Billion | MV (2034): USD 49.5 Billion | CAGR: 4.3%

- Consumer-driven mandates: Growing refusal of single-use plastics, favoring PCR and refill models.

- E-commerce imperatives: Structural integrity and ISTA-6 certified durability gaining importance.

- Luxury repositioning: Decorative sustainable glass becoming a competitive differentiator.

- Corporate sustainability pledges: Publicly declared 2026–2030 goals accelerating material transitions.

- Investment trend: Rising capex in mono-material lines, PCR infrastructure, and low-carbon furnaces.

Market Analysis: Strategic Shifts and Innovation Waves in 2025

The year 2025 is proving decisive, with a clustering of investments, partnerships, and material transitions that indicate a maturing sustainability agenda.

In August 2025, a leading U.S.–European packaging firm announced a dedicated mono-material PET line, signaling an industry-wide move toward recyclability compliance. By July 2025, a European prestige skincare house rolled out refillable glass bottles with recyclable pods, reinforcing the premium sector’s alignment with EU directives on circular packaging.

North America has emphasized lightweight sustainability solutions. In June 2025, a U.S.-based D2C player launched serums in 100% PCR aluminum bottles, combining recyclability with logistics efficiency. In May 2025, an Asian cosmetics manufacturer bridged digital and physical channels with smart bottles integrating QR codes and AR product tutorials, a development reflecting the intersection of packaging and consumer engagement platforms.

M&A also underscores strategic repositioning. In April 2025, a luxury packaging supplier acquired a glass decorator to secure in-house finishing capabilities for high-margin customization. Regulatory compliance accelerated shifts further: in February 2025, a multinational CPG major committed to converting its shampoo and conditioner portfolios in North America and Europe to recycled HDPE, anticipating tightening plastic bans. Meanwhile, January 2025 saw a dual emphasis on applicator-integrated bottles by indie brands and low-carbon glass production through electrified melting furnaces in Europe.

Key Trends and Emerging Opportunities Shaping the Cosmetic Bottles Packaging Market

Mandated Incorporation of Post-Consumer Recycled (PCR) Content

Regulatory mandates are increasingly driving cosmetic brands to adopt post-consumer recycled (PCR) materials in packaging. Legislations like Washington State’s Department of Ecology law require minimum PCR content in personal care packaging 15% by 2025, 25% by 2028, and 50% by 2031 providing a phased compliance roadmap for suppliers. Similarly, California’s Plastic Recycling Act (SB 54) enforces 15–50% PCR standards for beverage bottles, directly impacting material sourcing for cosmetic bottles. Industry leaders, including PepsiCo, have leveraged this market pull to secure reliable PCR supply chains. However, the surge in demand for PCR resin also drives a price premium, often 2–3 times higher than virgin materials, affecting packaging budgets and compelling brands to adopt more efficient sourcing and production strategies.

Strategic Investment in Refillable and Reusable Packaging Systems

Luxury and mainstream cosmetic brands are moving toward durable, refillable bottles, transforming primary packaging into a long-term brand asset. L’Oréal has invested in refillable skincare and fragrance bottles, complemented by in-store and direct-to-consumer refill logistics. High-end brands like Kjaer Weis exemplify how refillable, metal-based containers strengthen brand identity, creating a premium consumer experience. Retail programs such as Lush’s in-store refill stations encourage closed-loop reuse, fostering loyalty while reducing single-use waste. Fenty Beauty’s refillable foundation bottles demonstrate how this approach can enhance repeat purchases and long-term engagement, positioning refillable packaging as both a sustainability and strategic brand initiative.

Development of Advanced Monomaterial and Barrier Solutions

A critical opportunity exists in creating high-performance monomaterial bottles that maintain product integrity while enhancing recyclability. Companies like SML are developing MDO-PE barrier films to replace multi-material laminates, incorporating thin EVOH layers for oxygen and moisture protection. Mondi Group’s mono-material StandUpPouch and BASF-Siegwerk’s mono-PE solutions demonstrate scalable applications for sensitive formulations, achieving oxygen transmission rates (OTR) below 0.1 cc/m²/day. Taghleef Industries’ EXTENDO® PP solutions further improve recyclability, ensuring bottles can enter existing recycling streams without compromising barrier performance. These innovations address a long-standing industry challenge: combining high-barrier functionality with environmental compliance.

Integration of Digital (Smart) Packaging for Authentication and Engagement

Smart packaging technologies provide a transformative opportunity for cosmetics brands to combat counterfeiting and enhance consumer engagement. NFC chips embedded in luxury bottles allow instant product authentication, helping protect brands from counterfeit losses estimated in billions. RFID tags enable real-time supply chain visibility, preventing diversion and identifying potential sources of counterfeit products. QR-code-enabled Digital Product Passports (DPPs), aligned with the EU Eco-design for Sustainable Products Regulation (ESPR), offer consumers verified insights into materials, sustainability credentials, and recycling guidance. Beyond authentication, smart packaging allows brands to deliver tutorials, personalized skincare recommendations, and loyalty programs, converting traditional bottles into interactive digital platforms that strengthen brand-consumer connections.

Competitive Landscape: Leading Companies Driving the Next Era of Cosmetic Bottles Packaging

The global competitive field is consolidating around companies that combine materials science expertise, sustainability credentials, and global supply chain reach. Innovation pipelines are increasingly tied to regulatory alignment and luxury brand customization, shaping the future of cosmetic bottles packaging.

Gerresheimer AG: Bio-Based Plastics and Renewable Energy Commitments

Gerresheimer is scaling beyond its pharmaceutical roots, leveraging deep glass and plastic expertise for cosmetics. Its BioPack sugarcane-based bottles target body care clients seeking renewable alternatives. With over 40 facilities, Gerresheimer’s strengths lie in technical glass mastery and decorative finishes, while its 2030 pledge to halve CO2 emissions and source 100% renewable power positions it as a sustainability frontrunner.

AptarGroup, Inc.: Dispensing Systems Optimized for E-Commerce

Aptar continues to dominate in dispensing technologies while embedding sustainability. Its 2025 introduction of the HDP all-plastic pump addresses recyclability concerns without compromising dosage precision. The company also invested in a European ISTA-6 testing lab, a direct response to e-commerce packaging performance demands. Aptar’s trajectory reinforces its circular economy strategy mono-materials, refill models, and global scale.

Albéa Group: PCR Tubes and Refill Ecosystems for Scalable Sustainability

Albéa is aligning with clients’ carbon reduction targets through PCR- and bio-based cosmetic tubes, refill pods, and low-carbon packaging launches in 2025. The company offers a full-service model from design through manufacturing, enabling technical and branding synergies. Its positioning as a responsible packaging partner makes it integral for multinational beauty houses facing EU circularity deadlines.

Verescence: Luxury Glass Innovation Through Proprietary Technologies

Verescence commands the luxury glass segment, fusing artisanal heritage with proprietary innovations such as SCULPT’in technology, enabling unique internal bottle structures. Its lightweighting initiatives reduce raw material use without aesthetic compromise. The company’s 4R&D framework (Reduce, Reuse, Recycle, Replace, Disrupt) underpins its strategic orientation, with refillable flacons and recycled glass integration resonating strongly with luxury fragrance houses.

Libo Cosmetics Co., Ltd.: Customization and PCR Integration for Indie and Mid-Tier Brands

Libo Cosmetics differentiates through end-to-end R&D-to-manufacturing in Taiwan, offering agile customization for skincare and color cosmetics. Its 2025 WEConnect International certification strengthened its global supplier profile. Libo’s eco-friendly series, built around PCR materials and refillables, aligns particularly well with indie beauty and mid-tier brands that emphasize both sustainability and personalization.

Cosmetic Bottles Packaging Market Share Insights

Dispensing Bottles Lead Market Share by Product Type in Cosmetic Bottles Packaging Industry

Dispensing bottles dominate the cosmetic bottles packaging market with a commanding 40% share, underscoring their role as the functional backbone of hair care, body care, and mass skincare products. Their prevalence is tied to high-volume categories such as shampoos, conditioners, lotions, and shower gels, which require reliable, hygienic, and user-friendly dispensing systems. PET and HDPE remain the leading substrates due to durability and recyclability, but sustainability trends are reshaping the segment: mono-material pumps, reduced resin designs, and PCR (post-consumer recycled) integration are increasingly common. Innovation in precision dispensing such as scalp applicator tips and controlled pumps for viscous formulations further strengthens this segment’s dominance. Their ability to combine cost-efficiency with functionality makes dispensing bottles the workhorse of the beauty industry, balancing consumer convenience with brand identity.

Skin Care Dominates Market Share by Application in Cosmetic Bottles Industry

Skincare products represent 45% of the cosmetic bottles market, driven by the sheer breadth and innovation intensity of this category. From mass-market moisturizers to luxury serums, skincare requires a diverse packaging portfolio spanning dispensing pumps, airless bottles, and droppers. Rising consumer demand for active-rich formulations such as retinol, vitamin C, and peptides makes packaging integrity critical, pushing adoption of airless systems and UV-protected materials. The premiumization of skincare, coupled with the global "skinification" trend where beauty overlaps with health and wellness, ensures packaging must serve both functional and branding roles. Multinational giants like L’Oréal, Estée Lauder, and Shiseido are heavily investing in sustainable skincare packaging, including refillable bottle systems and PCR integration, amplifying the segment’s market share. Skincare remains the industry’s anchor application, dictating material selection, design trends, and regulatory compliance across the cosmetic bottles market.

United States: Sustainability Regulations and Pharmaceutical Packaging Drive Cosmetic Bottles Market

The U.S. cosmetic bottles packaging market is advancing rapidly due to a combination of stringent environmental regulations, sustainability initiatives, and pharmaceutical demand. States such as California are implementing laws like the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), which accelerate the shift toward recyclable, reusable, and PFAS-free cosmetic packaging. The U.S. Environmental Protection Agency (EPA) has also updated its rulemaking agenda to regulate PFAS in packaging, driving cosmetic brands to launch safer, eco-friendly bottles. Sustainability-focused companies like Amcor plc are pioneering recyclable solutions such as the AmSky Blister System, and extending innovations to cosmetic bottles that avoid PVC and aluminum while offering higher recyclability.

Technological adoption in the U.S. packaging industry is also noteworthy. Under the Drug Supply Chain Security Act (DSCSA), manufacturers are incorporating RFID tags, barcodes, and advanced traceability features to prevent counterfeiting and enhance product safety. This aligns with the increasing pharmaceutical demand for secure and tamper-evident cosmetic bottles, especially as home-based treatments for chronic diseases rise. Corporate initiatives from players like Placon, which launched inert trays for food and cosmetics, highlight the growing trend toward functional, transparent, and sustainable bottle designs. Together, regulatory mandates, pharmaceutical applications, and sustainability pressures are shaping a highly competitive U.S. market.

Germany: EU Packaging Regulations and Circular Economy Fuel Cosmetic Bottles Innovation

The German cosmetic bottles packaging market is heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR 2025), which requires all packaging to be fully recyclable by 2030. Germany’s strong commitment to a circular economy, supported by the Packaging Act (Verpackungsgesetz), ensures that producers are responsible for the entire lifecycle of their packaging. This framework incentivizes cosmetic bottle manufacturers to develop eco-friendly, recyclable, and bio-based packaging solutions.

Innovation is a defining feature of Germany’s cosmetic packaging sector. Manufacturers are embedding oxygen-barrier labels with unique device identification (UDI) to improve stability for sensitive products and ensure compliance with EU Medical Device Regulation (MDR). Companies like Gerresheimer AG are leading the sustainability push with new launches, such as glass jars paired with bio-based forewood closures, reflecting a trend toward premium sustainable packaging in cosmetics. With growing consumer awareness and strong governmental mandates, Germany is positioned as a leader in eco-conscious and technologically advanced cosmetic bottle packaging.

China: Dual Carbon Policies and E-Commerce Growth Reshape Cosmetic Bottles Packaging

China’s cosmetic bottles packaging market is undergoing transformation driven by the government’s dual carbon goal, which aims to achieve carbon peak and carbon neutrality. Policies are actively promoting eco-friendly and reusable packaging materials, reshaping how cosmetic bottles are designed and manufactured. At the same time, restrictions on non-degradable plastics have spurred demand for paper-based, laminated, and recyclable alternatives, making sustainability a core industry priority.

Technological innovation is accelerating production. Chinese manufacturers are investing in automation, AI, and 5G-enabled industrial internet systems to improve manufacturing efficiency and flexibility. The country’s booming e-commerce sector, particularly in cosmetics and personal care, is driving demand for secure, tamper-proof, and lightweight bottle packaging that can withstand long-distance shipping. Regulatory reforms, such as the 2025 announcement from the National Medical Products Administration (NMPA) requiring strict quality management systems for packaging manufacturers, are raising industry standards. China’s strong production capacity, combined with sustainability mandates and rising global exports, makes it a key hub for innovative cosmetic bottle solutions.

India: Domestic Production and Regulatory Reforms Boost Cosmetic Bottles Market

The Indian cosmetic bottles packaging market is benefitting from the government’s Make in India and Zero Effect Zero Defect initiatives, which encourage high-quality domestic production and infrastructure development. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, further enhances manufacturing capabilities, encouraging investment in standardized and eco-friendly bottle packaging solutions.

India’s regulatory landscape is also steering the market toward sustainable growth. The Plastic Waste Management (Amendment) Rules are phasing out single-use plastics, fueling demand for bio-based and recyclable cosmetic bottles. Consumer preferences are shifting as rising disposable incomes and urbanization encourage the adoption of portable, single-serve cosmetic packaging. Moreover, India’s growing pharmaceutical and healthcare industries are driving demand for secure, tamper-evident, and child-resistant bottles, which are essential for medicines, nutraceuticals, and cosmetic formulations. Combined with its abundant resources and large consumer base, India is emerging as a high-potential market for sustainable cosmetic packaging.

Brazil: Sustainability Laws and Traceability Mandates Transform Cosmetic Bottles Packaging

The Brazilian cosmetic bottles packaging market is experiencing significant change due to stringent sustainability laws. The National Solid Waste Policy (PNRS) is a central driver, promoting a circular economy and banning the import of solid waste, including plastics. These policies are encouraging manufacturers to embrace eco-friendly, reusable, and biodegradable cosmetic packaging solutions.

Brazil’s packaging sector is also adopting robotics, automation, and AI-driven quality control systems to enhance production efficiency and meet global standards. Strategic investments in new facilities are strengthening domestic capabilities, while ANVISA’s strict traceability requirements for pharmaceutical and cosmetic packaging are pushing adoption of unique identification and serialization systems. The convergence of regulatory mandates, consumer sustainability demands, and technological upgrades positions Brazil as a growing hub for durable and compliant cosmetic bottles packaging.

Japan: Bio-Based Innovations and High-Performance Packaging Elevate Cosmetic Bottles Market

The Japanese cosmetic bottles packaging market is evolving through a blend of advanced recycling systems, bio-based innovations, and functional upgrades. Under the Containers and Packaging Recycling Law, businesses must contribute to recycling rigid plastics and glass, supporting a highly efficient waste management system. New regulatory updates under the Food Sanitation Act (2025) have introduced stricter migration limits for food-contact and cosmetic packaging, prompting manufacturers to enhance product safety and compliance.

Sustainability is a strong trend, with companies like LyondellBasell integrating bio-based polypropylene into packaging for brands such as Shiseido, showcasing the shift toward renewable and sustainable cosmetic bottles. Innovation in dimensional stability, deformation resistance, and high-performance functionality is allowing Japan to cater to premium cosmetic and personal care markets. By combining eco-friendly materials with precision engineering, Japan continues to set benchmarks in cosmetic bottles packaging that balances sustainability and performance.

Cosmetic Bottles Packaging Market Report Scope

Cosmetic Bottles Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.9 Billion

|

|

Market Size (2034)

|

$49.5 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Material Type (Glass, Plastic, Metal, Bioplastics), By Product Type (Dispensing Bottles, Non-Dispensing Bottles, Dropper Bottles, Airless Bottles, Roll-on Bottles), By Application (Skin Care, Hair Care, Fragrances, Nail Care, Other Applications), By Capacity (Less than 50 ml, 50–150 ml, 151–500 ml, More than 500 ml)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., AptarGroup, Inc., Gerresheimer AG, Silgan Holdings Inc., Albéa S.A., HCP Packaging, Cosmopak Corp., Quadpack, The Libo Cosmetics Company, Ltd., Verescence France, Vitro S.A.B, Lumson, DS Smith plc, Huhtamaki Oyj

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cosmetic Bottles Packaging Market Segmentation

By Material Type

- Glass

- Plastic

- Metal

- Bioplastics

By Product Type

- Dispensing Bottles

- Non-Dispensing Bottles

- Dropper Bottles

- Airless Bottles

- Roll-on Bottles

By Application

- Skin Care

- Hair Care

- Fragrances

- Nail Care

- Other Applications

By Capacity

- Less than 50 ml

- 50–150 ml

- 151–500 ml

- More than 500 ml

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cosmetic Bottles Packaging Market

- Amcor plc

- Berry Global Inc.

- AptarGroup, Inc.

- Gerresheimer AG

- Silgan Holdings Inc.

- Albéa S.A.

- HCP Packaging

- Cosmopak Corp.

- Quadpack

- The Libo Cosmetics Company, Ltd.

- Verescence France

- Vitro S.A.B

- Lumson

- DS Smith plc

- Huhtamaki Oyj

* List Not Exhaustive

Methodology

USDAnalytics conducted an extensive, multi-layered research study to analyze the global Cosmetic Bottles Packaging Market, leveraging both primary and secondary sources to ensure a data-driven, industry-relevant perspective. Primary research involved interviews with key stakeholders including packaging manufacturers, cosmetic brands, distributors, and supply chain specialists, while secondary research incorporated regulatory reports, sustainability mandates, corporate ESG disclosures, trade journals, and market press releases. The methodology focused on evaluating the impact of post-consumer recycled (PCR) content mandates, refillable and reusable packaging trends, and technological innovations such as mono-material solutions, advanced barrier films, and smart packaging integration. Market sizing, segmentation, and forecasts were derived using historical data, adoption trends across regions including the U.S., Germany, China, India, Brazil, and Japan, and application-specific demand in skincare, haircare, fragrance, and nail care. Competitive intelligence was gathered on major players like Gerresheimer AG, AptarGroup, Albéa, Verescence, and Libo Cosmetics, analyzing their sustainability initiatives, product innovations, and strategic investments in low-carbon glass, PCR integration, and refillable ecosystems. Additionally, USDAnalytics examined market drivers including regulatory compliance, e-commerce durability standards, luxury repositioning, and corporate sustainability pledges to provide actionable insights tailored for industry professionals seeking strategic growth, regulatory alignment, and product innovation intelligence.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.