Market Overview: Luxury Packaging Industry Growth Driven by Cosmetics, Sustainability, and Rigid Boxes

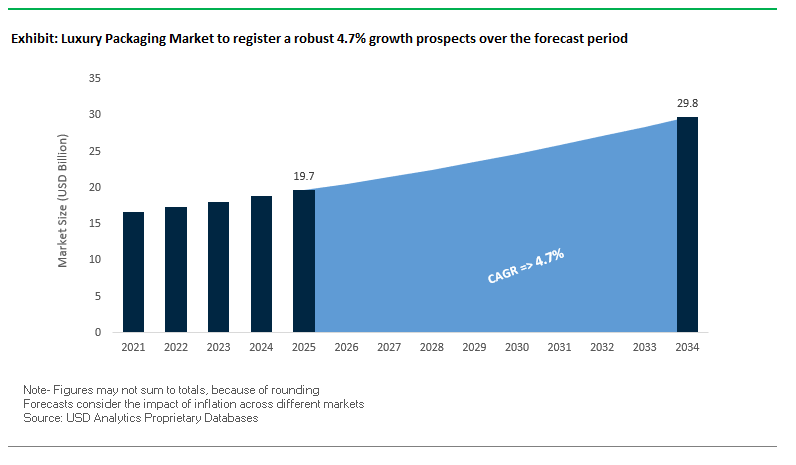

The Luxury Packaging Market is projected to reach $19.7 billion in 2025 and expand to $29.8 billion by 2034, reflecting a CAGR of 4.7%. This steady growth is driven by strong demand from the cosmetics and fragrance sector, which remains the largest consumer of premium rigid boxes and specialty paperboard packaging. The sector’s focus on brand differentiation, protection of high-value goods, and elevated unboxing experiences positions luxury packaging as a critical component of consumer engagement strategies.

Rigid boxes continue to dominate due to their durability, premium aesthetics, and customization capabilities. Techniques such as embossing, foil stamping, and specialty coatings enhance consumer perception of value, reinforcing their use in high-end markets. At the same time, sustainability has become a premium appeal factor, with 43% of global consumers in 2025 willing to pay more for eco-friendly packaging. This growing trend is reshaping innovation strategies, as brands transition toward recyclable, reusable, and biodegradable luxury formats.

The rise of e-commerce luxury retail has also influenced packaging investments. Brands are increasingly designing packaging not just for protection but also for unboxing experiences, which are amplified on social media and serve as marketing tools. The balance between aesthetics, sustainability, and brand storytelling will define the industry’s direction in the next decade.

Key Insights for Industry Professionals

- Cosmetics and fragrances dominate: This segment accounts for a major share of demand due to branding and product protection needs.

- Rigid boxes lead growth: Valued for durability, customization, and consumer appeal.

- Sustainability is a premium driver: 43% of consumers are willing to pay extra for sustainable luxury packaging.

- E-commerce boosts innovation: Memorable unboxing experiences are now vital for luxury brand differentiation.

Market Analysis: Strategic Developments Transforming Luxury Packaging

The global luxury packaging market is undergoing a phase of consolidation, material innovation, and strategic partnerships aimed at meeting consumer expectations for sustainability and premium aesthetics.

In September 2025, Mondi showcased its FunctionalBarrier Paper Ultimate at Fachpack, an ultra-high-barrier paper designed to replace plastic and aluminum in high-end food and cosmetics packaging. Just a month earlier, in August 2025, Smurfit Kappa and WestRock finalized their merger to form Smurfit WestRock, creating a new paper-based packaging powerhouse with enhanced capacity for luxury markets. Mondi also introduced Ad/Vantage Smooth Brown Semi Extensible paper in August 2025, combining strength with a premium appearance.

Earlier in June 2025, Mondi highlighted sustainable premium papers at Édition Spéciale by LUXE PACK Paris, emphasizing recyclable solutions for luxury goods. In April 2025, DS Smith partnered with TPV Automotive to develop plastic-free, eco-friendly packaging for BMW car wheel carriers, signaling the industry’s push into new luxury segments.

Strategic mergers also reshaped the competitive landscape. In February 2025, Smurfit Kappa and WestRock completed their $12.7 billion merger, while in October 2024, International Paper and DS Smith secured shareholder approval for their $7.2 billion merger, forming a stronger global leader in sustainable luxury packaging.

Key Trends and Opportunities Shaping the Luxury Packaging Market

Strategic Integration of Certified Sustainable and Traceable Materials

Luxury packaging is undergoing a strategic transformation as brands embrace rigorously certified, sustainable materials to align with ESG mandates and consumer expectations. Forest Stewardship Council (FSC)-certified paperboards are becoming the norm, guaranteeing responsible forest management and circularity. For instance, Burberry’s use of FSC-certified paper made from recycled coffee cups underscores the sector’s shift toward verifiable eco-materials, reinforcing its pledge to eliminate unnecessary plastic by 2025. In parallel, the adoption of bio-acetates and recycled metals is accelerating, with sustainability-driven innovators like Stella McCartney pioneering bio-acetate eyewear sourced from renewable wood pulp. This trend is not merely a marketing tactic but a structural response to demand from high-net-worth consumers who value traceability. A recent global survey found that 76% of consumers consider independent certification crucial in sustainability claims, pushing luxury brands to disclose their entire material sourcing journey. As packaging becomes an extension of brand integrity, verifiable transparency is shaping competitive differentiation in the global luxury packaging market.

Adoption of Connected Packaging for Hybrid Digital-Physical Experiences

Luxury packaging is evolving into an interactive brand platform through the integration of NFC chips, QR codes, and RFID tags. These technologies address counterfeiting a pervasive problem in luxury goods by allowing consumers to authenticate products instantly with their smartphones. Beyond security, connected packaging enables immersive storytelling. A luxury fragrance brand, for instance, can use a QR code to unlock digital experiences that narrate the perfumer’s creative journey or offer exclusive loyalty rewards. This hybrid model bridges physical and digital engagement, creating a “persistent touchpoint” that extends far beyond the initial unboxing. Additionally, connected packaging enhances supply chain visibility, enabling brands to track high-value inventory in real time and ensure compliance with storage and handling standards. As experiential luxury becomes a dominant consumer preference, the integration of connected packaging is solidifying its role as both a safeguard and an engagement tool in high-end markets.

Development of Advanced, Plastic-Free Barrier Coatings for Luxury Packaging

The push for plastic-free luxury packaging is creating a high-value opportunity for bio-based, recyclable coatings that meet the dual requirements of performance and sustainability. Luxury brands face regulatory deadlines under the EU’s Packaging and Packaging Waste Regulation (PPWR), which mandates recyclability at scale by 2035. In response, material innovators are scaling new barrier solutions. Xampla’s “Morro” pea-protein material exemplifies this innovation, offering oxygen and moisture resistance without compromising recyclability. Similarly, H.B. Fuller’s water-based grease- and moisture-resistant coatings showcase how sustainable technology can be adapted to rigid luxury boxes and wraps. These coatings eliminate the need for plastic laminates while preserving the tactile and visual aesthetics essential to luxury packaging. The challenge and opportunity lies in closing the performance gap with traditional plastic while delivering compostable, circular-ready materials. For brands, adopting plastic-free barrier coatings enhances both compliance and consumer perception, making it a critical growth driver.

Expansion of Reusable and Multi-Functional Secondary Packaging Systems

Luxury brands are redefining packaging as part of the product experience itself by designing secondary packaging rigid boxes, decorative shells, and cases with reuse and functionality in mind. Refillable systems are gaining traction: Estée Lauder targets 75–100% of its packaging to align with the “5 Rs” (Recyclable, Refillable, Reusable, Recycled, or Recoverable), while Le Labo and Bobbi Brown lead with refillable fragrance and skincare programs. Reusable packaging also functions as a collectible: a luxury perfume box can double as a jewelry container, extending its lifecycle and reinforcing brand value. Environmental benefits are tangible; Estée Lauder’s life cycle assessment revealed that refillable fragrance packaging reduces emissions and water consumption by 20% after the first purchase. This shift transforms packaging from single-use waste into a durable, functional asset that supports circularity while deepening consumer loyalty. As premium buyers increasingly demand sustainable luxury, reusable packaging systems are set to dominate future market strategies.

Competitive Landscape: Leading Companies in Global Luxury Packaging Market

The luxury packaging industry is highly consolidated, with multinational players expanding through mergers, acquisitions, and innovation in sustainable materials. Companies are leveraging vertical integration and premium design capabilities to strengthen their positions in cosmetics, fragrances, and luxury goods packaging.

Smurfit WestRock: A New Global Leader in Paper-Based Luxury Packaging

Formed in 2025 through the merger of Smurfit Kappa and WestRock, Smurfit WestRock is now one of the largest paper-based packaging companies globally. Its portfolio spans rigid boxes, folding cartons, and specialty containers tailored for premium cosmetics and luxury products. With full vertical integration from forest management to design and recycling the company ensures sustainability and quality control. Its bespoke luxury gift boxes and corrugated e-commerce solutions highlight its strength in enhancing unboxing experiences.

International Paper: Expanding Global Reach with DS Smith Merger

International Paper is a leading provider of fiber-based packaging materials. Its late 2024 acquisition of DS Smith expanded its footprint across Europe and North America, creating a global leader in sustainable packaging. The company is innovating with ultra-lightweight and translucent papers designed to replace plastics in luxury applications. Its strategy is centered on sustainable premium papers that deliver both functionality and brand aesthetics for luxury packaging.

Mondi Group: Innovating with Recyclable Premium Papers

Mondi is pioneering sustainable luxury packaging solutions with specialty papers for bags, boxes, and premium cartons. In September 2025, it launched FunctionalBarrier Paper Ultimate, a recyclable alternative to plastic or aluminum for high-end food and cosmetic packaging. Mondi continues to emphasize sustainability, expanding its corrugated and solid board offering with recent acquisitions. The company’s premium materials and design focus position it as a sustainability-driven innovator in the luxury packaging market.

GPA Global: Specialist in Bespoke Luxury Packaging Solutions

GPA Global delivers fully customized luxury packaging for cosmetics, spirits, and electronics. Its global supply chain expertise and wide network of manufacturing facilities make it a preferred partner for both global brands and niche luxury labels. Its offerings include luxury gift bags, rigid boxes, and promotional packaging. GPA Global’s ability to manage small-batch projects for limited editions sets it apart, while its design expertise ensures packaging that is both innovative and sustainable.

DS Smith Plc: Redefining Luxury Packaging with Fiber-Based Solutions

DS Smith, set to merge with International Paper, continues to strengthen its luxury packaging footprint. Its offerings are made from 100% recycled paper, reinforcing its commitment to closed-loop models. The company’s strategy, “Redefining Packaging for a Changing World,” centers on eliminating plastic waste and innovating with recyclable fiber-based solutions. DS Smith’s integrated approach spanning recycling, paper production, and packaging design provides clients with consistent and sustainable luxury packaging supply.

Luxury Packaging Market Share Insights

Boxes Dominate Market Share by Packaging Type in Luxury Packaging

Boxes command the largest share of the luxury packaging industry, capturing 45% of the market in 2025. Their dominance is rooted in their central role in creating a memorable unboxing experience, a core driver of luxury brand perception. Rigid set-up boxes with magnetic closures, layered structures, and custom inserts have evolved into storytelling vehicles that elevate brand identity far beyond simple protection. Luxury houses now treat packaging as a strategic marketing expense, investing in premium materials, intricate detailing, and finishes designed to amplify the tactile and visual appeal of the product. With the rise of social media, particularly unboxing videos on Instagram and YouTube, boxes deliver disproportionate brand visibility, reinforcing their leadership in a market where consumer engagement and heritage storytelling are as critical as the product itself.

Cosmetics & Fragrances Drive Market Share by End-Use Industry in Luxury Packaging

Cosmetics and fragrances dominate the luxury packaging landscape, contributing 35% of market demand. This leadership reflects the industry’s reliance on packaging as an inseparable component of the product’s value proposition. For skincare, heavy glass jars and sculpted containers enhance perceptions of efficacy and ritual, while for fragrances, the bottle and presentation box are iconic extensions of the scent itself. Unlike other luxury categories, cosmetics and fragrances demand high-frequency replenishment, which multiplies packaging volumes and innovation cycles. The convergence of personalization, sustainability, and heritage aesthetics has further reinforced this segment’s leadership, with brands investing in refillable jars, bio-based materials, and digitally authenticated packaging. By combining high volume, strong emotional branding, and regulatory-driven material innovation, cosmetics and fragrances have established themselves as the core economic engine of the luxury packaging industry.

United States: Interactive and Sustainable Luxury Packaging Drives Consumer Engagement

The U.S. luxury packaging market is experiencing strong growth due to affluent consumer demand for aesthetically pleasing, high-performance, and eco-friendly packaging. Rising awareness of sustainability is prompting brands in cosmetics, fine foods, and spirits to adopt innovative materials and circular packaging solutions. Smart packaging technologies, including NFC (Near Field Communication) and AR (Augmented Reality), are being integrated to enhance interactive unboxing experiences, improve product authenticity verification, and deepen consumer engagement.

Sustainability remains a core market driver. Avient Corporation has expanded its recycled formulations to include grades with up to 60% ocean-bound plastic waste, reflecting the industry’s commitment to circularity. Additionally, the surge of e-commerce luxury sales is creating demand for packaging that is not only protective but also memorable and experiential, exemplified by WestRock’s layered packaging designs. Corporate initiatives, such as lightweight champagne bottles by Champagne Telmont, further demonstrate the trend toward reducing carbon emissions and promoting sustainable luxury packaging.

Germany: Regulatory Compliance and Circular Economy Leadership Shape Luxury Packaging

Germany’s luxury packaging industry is heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates fully recyclable packaging by 2030 and establishes reuse and refill targets. This stringent regulatory framework is driving demand for eco-friendly, recyclable luxury packaging solutions and shaping consumer expectations around sustainability.

German manufacturers are leveraging their leadership in the circular economy to develop high-quality packaging that combines luxury aesthetics with recycled content. Innovations include recycled glass materials, creative shapes, and eco-conscious color designs. The PPWR regulations, coupled with technological innovation in sustainable materials, are positioning Germany as a global benchmark for high-end, environmentally responsible packaging.

China: Eco-Friendly Materials and M&A Activity Accelerate Luxury Packaging Growth

China’s luxury packaging market is undergoing a green transformation, driven by the government’s dual carbon goals promoting eco-friendly, reduced, and reusable packaging materials. Sustainability initiatives by brands, such as Mars Wrigley China’s 100% recycled PET packaging for its Cui Xiang Mi chocolate line, reflect the growing environmental consciousness in the luxury segment.

Technological investments, including automation, AI, and 5G-enabled industrial integration, are enhancing production efficiency and flexibility. The market is also witnessing increased mergers and acquisitions, exemplified by the Fedrigoni Group’s acquisition of Arjowiggins HKK3 Limited, strengthening the company’s footprint in Asia and expanding its portfolio of translucent papers for premium packaging. These developments underscore China’s rapidly evolving luxury packaging landscape, where sustainability, technology, and strategic growth converge.

India: Policy Support and E-Commerce Expansion Propel Sustainable Luxury Packaging

India’s luxury packaging market is benefiting from the Make in India and Zero Effect Zero Defect initiatives, which encourage quality domestic production and industrial investment. Recent taxation policies, such as the 1% Tax Collected at Source (TCS) on high-value luxury goods effective April 2025, are formalizing high-value transactions and expanding the market for premium packaging solutions.

The rapid growth of e-commerce is driving demand for affordable, protective, and visually appealing packaging for luxury items. Sustainability is a key focus, supported by government regulations like the Plastic Waste Management (Amendment) Rules, which encourage eco-friendly and reusable packaging alternatives. Together, policy support, e-commerce expansion, and sustainable innovations are establishing India as a fast-growing market for luxury packaging solutions that combine aesthetics with environmental responsibility.

Luxury Packaging Market Report Scope

Luxury Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.7 Billion

|

|

Market Size (2034)

|

$29.8 Billion

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Material Type (Paperboard, Glass, Metal, Plastic, Wood, Other Materials), By Packaging Type (Boxes, Pouches, Bags, Bottles & Containers, Other Types), By End-Use Industry (Cosmetics & Fragrances, Premium Beverages, Confectionery, Watches & Jewelry, Tobacco, Other Industries), By Printing Technology (Offset Printing, Digital Printing, Screen Printing, Flexography, Other Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, WestRock Company, Smurfit Kappa Group, DS Smith plc, Graphic Packaging Holding Company, International Paper, Mondi Group, Crown Holdings Inc., Ardagh Group, Gerresheimer AG, SGD Pharma, Verescence, Stolzle Glass Group, Waltersperger, GPA Global

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Luxury Packaging Market Segmentation

By Material Type

- Paperboard

- Glass

- Metal

- Plastic

- Wood

- Other Materials

By Packaging Type

- Boxes

- Pouches

- Bags

- Bottles & Containers

- Other Types

By End-Use Industry

- Cosmetics & Fragrances

- Premium Beverages

- Confectionery

- Watches & Jewelry

- Tobacco

- Other Industries

By Printing Technology

- Offset Printing

- Digital Printing

- Screen Printing

- Flexography

- Other Technologies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Luxury Packaging Market

- Amcor plc

- WestRock Company

- Smurfit Kappa Group

- DS Smith plc

- Graphic Packaging Holding Company

- International Paper

- Mondi Group

- Crown Holdings Inc.

- Ardagh Group

- Gerresheimer AG

- SGD Pharma

- Verescence

- Stolzle Glass Group

- Waltersperger

- GPA Global

* List Not Exhaustive

Methodology

The research methodology for the Luxury Packaging Market combines both primary and secondary data collection to ensure comprehensive and accurate insights for industry professionals. Primary research involved detailed interviews with key stakeholders, including packaging manufacturers, luxury brand executives, and sustainability experts, to assess current market trends, strategic developments, and innovation priorities. Secondary research drew from company press releases, financial statements, trade journals, industry publications, regulatory updates, and market reports to corroborate and validate findings. The study employed a top-down approach for market sizing, beginning with overall packaging market estimates and narrowing to luxury-specific segments based on material type, packaging type, end-use industry, and printing technology. Quantitative data were analyzed using statistical tools to calculate growth trends, market shares, and projections, while qualitative insights examined strategic partnerships, sustainability adoption, and technological innovations such as connected packaging and plastic-free barrier coatings. Regional analyses for key markets, including the U.S., Germany, China, and India, were incorporated to reflect regulatory impact, e-commerce penetration, and consumer behavior differences. The combination of rigorous data validation, cross-verification of company developments, and consideration of macroeconomic, technological, and environmental factors ensures an accurate and actionable overview of the global luxury packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.