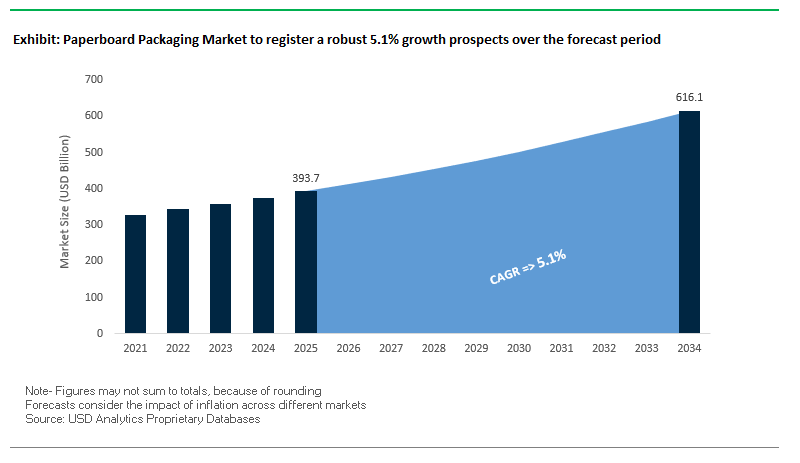

Paperboard Packaging Market Set to Expand from $393.7 Billion in 2025 to $616 Billion by 2034 with 5.1% CAGR Driven by E-Commerce and Sustainability

The Global Paperboard Packaging Market is poised for steady growth, increasing from $393.7 billion in 2025 to $616 billion by 2034, at a CAGR of 5.1%, fueled by rising demand from e-commerce, D2C channels, and sustainability-driven packaging needs. Paperboard packaging—including corrugated boxes, folding cartons, flexible paper bags, and liquid packaging plays a critical role in product protection, transportation, and branding across multiple industries, from food and beverages to personal care and industrial goods.

Key Insights for Industry Professionals:

- E-Commerce and D2C Expansion: The surge in online shopping has created a massive need for lightweight, durable, and customizable packaging that can withstand parcel shipping while enhancing brand visibility.

- Sustainability and Circular Economy Adoption: Companies are shifting toward renewable and recyclable fibers, driven by government regulations, corporate sustainability initiatives, and consumer preference for eco-friendly packaging.

- Functional and Aesthetic Innovation: Paperboard is engineered with high-quality print surfaces and moisture/grease-resistant coatings, enabling premium graphics and enhanced functionality.

- Automation and Supply Chain Optimization: New designs focus on lightweight boards and innovative structures compatible with high-speed automated packing lines, reducing material usage and logistics costs.

- Material Innovation for High-Performance Applications: Focused R&D is driving durable, cost-effective, and sustainable paperboard solutions to replace plastics in a wide range of sectors.

Strategic Moves and Product Innovations Illustrate Industry Commitment to Sustainability and Market Consolidation

The Paperboard Packaging Industry is highly dynamic, with significant strategic developments shaping growth, sustainability, and innovation. In August 2025, Graphic Packaging International introduced the PaperSeal® Pressed MAP Tray, emphasizing the broader trend of fiber-based alternatives to plastics in packaging. During the same month, International Paper announced a $1.5 billion sale of its Global Cellulose Fibers business and a $250 million investment in its Riverdale mill to convert a paper machine for containerboard production, reinforcing its focus on core sustainable packaging operations.

In July 2025, Smurfit Westrock reported capacity adjustments in the U.S. and Germany to optimize its footprint, while ReMA included paper cups in its recycled materials classification, advancing industry-wide circularity initiatives. April 2025 marked the completion of International Paper’s $9.9 billion acquisition of DS Smith, significantly expanding its European market presence and strengthening its sustainable packaging portfolio.

Earlier innovations include Billerud’s heat-sealable fossil-free paper (March 2025), Mondi’s sustainability report highlighting 87% of revenue from reusable, recyclable, or compostable products (March 2025), and the Smurfit Kappa-WestRock merger completed in November 2024, creating a new global leader in corrugated and sack packaging.

Trends and Opportunities Shaping the Paperboard Packaging Market

Unprecedented Capacity Expansion Driven by Plastic Substitution Mandates

The paperboard packaging market is undergoing historic capacity expansion as global legislation forces a structural shift away from single-use plastics. Regulatory frameworks such as the European Union’s Packaging and Packaging Waste Regulation (PPWR) and the EU plastics tax, effective since 2021, impose financial penalties on non-recycled plastic packaging, driving brands to adopt recyclable paperboard alternatives at scale. This legislative restructuring is fueling unprecedented capital investments across the paperboard sector. Sappi North America, for instance, announced a landmark $500 million investment at its Somerset Mill in Maine. Completed in late 2025, the project doubled the mill’s solid bleached sulfate (SBS) paperboard output to 470,000 metric tons annually, positioning the company as a key supplier for high-performance sustainable packaging.

At the national level, similar investments are reshaping supply capacity. In India, where a ban on single-use plastics has been enforced since July 2022, paper manufacturers such as Andhra Paper and Satia Industries are committing significant capital to expansion. Andhra Paper is upgrading its Paper Machine-3 to add 60,000 tons annually, while Satia Industries has earmarked INR 4–4.5 billion ($48–54 million) over FY26–FY27 to increase production by 10%. This expansion is directly tied to surging domestic demand created by compliance-driven bans. On the corporate side, Amazon’s replacement of 99.7% of its plastic padded mailers with recyclable paper mailers exemplifies how e-commerce giants are driving demand shocks across the value chain. Combined with legislative bans, corporate commitments to ESG and plastic elimination are restructuring procurement strategies and accelerating the shift to paperboard packaging.

Strategic Adoption of Advanced Barrier Coatings for Functional Performance

Another transformative trend in the paperboard packaging market is the strategic adoption of high-performance barrier coatings that extend the applicability of paper-based formats. Traditionally limited by vulnerability to moisture, grease, and gas transmission, paperboard is now being enhanced with innovative, recyclable coatings. Academic research demonstrates the potential of water-based alkali-soluble resin (ASR) coatings that can be easily separated during repulping, ensuring compatibility with recycling infrastructure. These technologies make coated paperboard fully recyclable without compromising performance.

Commercial players are also leading with new mineral-based resin coatings, which act as “drop-in replacements” for traditional plastics. With up to 51% mineral content, these coatings behave like clay in recycling mills, facilitating fiber recovery and ensuring compliance with circularity targets. In the food sector, new formulations are solving the moisture and grease barrier challenge. Patents highlight water-based emulsions combining synthetic rubber latex and wax that create strong waterproof and grease-resistant layers while retaining recyclability. These innovations open paperboard packaging to frozen food, ready-to-eat meals, and greasy snack applications previously dominated by multi-material laminates. By enabling paperboard to replace complex plastic structures, barrier coatings are not just improving performance—they are redefining its role in high-demand, high-regulation packaging markets.

Commercialization of Molded Fiber for Expanded Applications

The commercialization of molded fiber represents one of the most promising opportunities in the paperboard packaging market. Moving beyond egg cartons and protective trays, molded fiber is being scaled as a replacement for expanded polystyrene (EPS) and Styrofoam in electronics packaging. Thermoformed molded fiber inserts can be custom-engineered to secure smartphones, laptops, and accessories, offering both shock absorption and sustainability. With premium electronics brands under pressure to reduce plastic use, molded fiber provides a compelling alternative that combines protection, brand image, and eco-friendly credentials.

Advancements in wet press and thermoforming technologies are enabling molded fiber to achieve smooth finishes and fine details, making it suitable for high-end cosmetics and premium consumer goods. This evolution transforms molded fiber from a utilitarian material to a premium packaging component that enhances the unboxing experience. Furthermore, molded fiber delivers logistical advantages—it is lightweight, stackable, and reduces freight costs and emissions compared to bulkier plastic foams. By combining cost efficiency with sustainability and functionality, molded fiber is set to expand its share across both protective and premium packaging categories.

Integration of Digital Watermarking for Intelligent Recycling

Digital watermarking is emerging as a breakthrough opportunity to enhance recyclability and compliance in the paperboard packaging market. The HolyGrail 2.0 initiative, which conducted large-scale industrial trials in Germany from August to December 2024, demonstrated over 90% detection efficiency while processing significant volumes of household packaging waste. This confirms the scalability of watermarking as a sorting technology for real-world recycling systems.

The key advantage lies in its granularity. Watermarks allow sorting equipment to distinguish between food-grade and non-food-grade paperboard, as well as between different barrier coatings. This ensures high-purity recycling streams capable of being reprocessed into food-contact packaging—an area of increasing regulatory scrutiny. Beyond operational benefits, digital watermarking supports compliance with Extended Producer Responsibility (EPR) frameworks by providing brands with verifiable, real-time data on packaging recovery and recycling performance. This transparency allows companies to meet sustainability commitments, prove regulatory compliance, and strengthen consumer trust. As governments tighten circular economy targets, watermarking offers a critical opportunity to close the loop for paperboard packaging.

Leading Paperboard Packaging Companies Drive Sustainable Innovation and Global Scale

The Global Paperboard Packaging Market is dominated by major players leveraging materials science expertise, manufacturing scale, and sustainability initiatives to deliver innovative solutions across food, e-commerce, and industrial applications.

Smurfit Westrock plc Combines Scale and Expertise to Lead Global Paperboard Packaging Innovation

Smurfit Westrock, formed from the Smurfit Kappa-WestRock merger, has over 500 converting operations and 62 mills across 40 countries. In July 2025, it reported Adjusted EBITDA of $752 million in North America. The company provides corrugated containers, folding cartons, and specialty packaging, focusing on renewable and recyclable materials and circular economy-driven solutions.

International Paper Company Focuses on Strategic Transformation to Enhance Sustainable Packaging Operations

International Paper is a global leader in fiber-based packaging, with extensive mills and converting plants. In August 2025, it sold its Global Cellulose Fibers business and invested $250 million in containerboard production. The company offers corrugated boxes, containerboard, and bleached paperboard and is committed to achieving an advantaged cost position while enhancing customer experience and sustainability.

Graphic Packaging International, LLC Advances Fiber-Based Packaging and Operational Sustainability

Graphic Packaging specializes in consumer packaging and paperboard solutions, with a vertically integrated model. Its 2024 Impact Report (July 2025) highlighted replacing 1 billion plastic packages with paperboard alternatives. Offerings include folding cartons, paperboard cups, and flexible packaging, aligned with Vision 2030 for innovation, circularity, and operational excellence.

Mondi Group Drives High-Barrier and Sustainable Paper Packaging Solutions Globally

Mondi excels in paper-based and plastic-based packaging, providing corrugated packaging, sack kraft paper, and flexible solutions. In August 2025, production of FunctionalBarrier Paper Ultimate ramped up, and the March 2025 sustainability report confirmed 87% of revenue from reusable, recyclable, or compostable products. The company emphasizes MAP2030 for circularity, climate action, and workforce empowerment.

Stora Enso Oyj Champions Renewable Packaging and Circular Bioeconomy Leadership

Stora Enso integrates forestry and high-performance packaging production, providing folding boxboard, liquid packaging board, and containerboard. In April 2025, it reorganized to focus on renewable packaging, achieving a 53% reduction in Scope 1 & 2 emissions by 2024. The company emphasizes circular bioeconomy principles and replacing fossil-based materials.

Billerud AB Strengthens High-Performance and Sustainable Packaging Material Leadership

Billerud specializes in durable, high-printability paperboard. Its Michigan mills investment supports the Way Forward strategy, while achieving a Gold EcoVadis rating (November 2024) for sustainability. Products include fluting, liner, and cartonboard for industrial, liquid, and consumer goods, with a focus on high-performance materials and low-carbon solutions.

Paperboard Packaging Market Share Insights, 2025-2034

Corrugated Boxes Lead Market Share by Product Type in the Paperboard Packaging Industry

Corrugated boxes command 62% of the global paperboard packaging market, highlighting their role as the structural backbone of global e-commerce and logistics systems. Their dominance is fueled by strength-to-weight advantages, cost efficiency, and unparalleled stackability, making them indispensable for transporting goods across diverse supply chains. The ongoing trend of “right-weighting” reducing fiber usage while maintaining crush resistance is reshaping corrugated manufacturing, delivering both environmental benefits and lower transportation costs. Beyond functionality, corrugated packaging has evolved into a brand communication tool, with high-resolution digital printing enabling enhanced shelf appeal and traceability through QR and RFID integration. Folding cartons, holding 20% of the market, remain vital for retail point-of-sale packaging, providing superior printability and sustainability-driven innovations such as bio-based coatings and PCR fiber integration. Paperboard cups and trays, while smaller in volume, are witnessing accelerated transformation due to global bans on plastic-lined disposables, spurring investment in compostable and recyclable barrier technologies. Liquid cartons continue to offer aseptic advantages for dairy and juice packaging, though recycling infrastructure gaps and rising rPET competition temper their share. Emerging innovations in molded pulp and paperboard tubes are rapidly expanding their footprint in electronics, cosmetics, and premium beverages, positioning the “other” category as a hub of sustainable innovation. Collectively, product segmentation reveals corrugated’s unmatched scale, folding cartons’ brand-led resilience, and specialty formats’ critical role in addressing sustainability mandates.

Food & Beverages Hold the Largest Market Share by Application in the Paperboard Packaging Industry

The food and beverage sector accounts for 45% of paperboard packaging demand, underscoring its role as the industry’s anchor end-use. Paperboard’s renewable, food-safe, and customizable properties make it the preferred substrate across categories ranging from frozen foods and cereals to premium beverages and QSR takeout containers. The most critical driver is the development of functional coatings and barriers that provide grease, moisture, and oxygen resistance without undermining recyclability enabling the substitution of plastic packaging with fiber-based solutions. E-commerce and retail, with a 35% share, act as the growth engine of corrugated packaging, demanding high-performance designs that combine durability for last-mile shipping with shelf-ready branding features. Industrial goods rely on reinforced corrugated structures and multi-ply sacks to safeguard heavy machinery, chemicals, and construction materials, prioritizing performance over graphics. Healthcare and pharmaceuticals, though smaller in volume, are a high-value niche, requiring precise tamper-evidence, clean surfaces, and serialization-ready packaging aligned with global compliance frameworks. Personal care and cosmetics leverage premium folding cartons with foiling, embossing, and plastic-free barriers to create luxury unboxing experiences, while electronics and appliances depend on custom-engineered corrugated inserts and molded pulp solutions to ensure transit protection. The “other applications” category demonstrates paperboard’s adaptability, spanning automotive components, household detergents, and specialty packaging that demands oil resistance, static control, or heavy-duty performance. This segmentation illustrates how food and beverage drives volume, e-commerce and retail sustain innovation, and high-value niches elevate technical sophistication across the global paperboard packaging industry.

United States Paperboard Packaging Market Driven by FDA Regulations and Corporate Investments

The United States paperboard packaging market is undergoing rapid transformation due to regulatory action, corporate investment, and surging e-commerce demand. A pivotal driver is the FDA’s ban on PFAS in food contact materials, which has accelerated the adoption of fluorine-free and alternative barrier coatings to ensure food safety and recyclability. Companies are responding with substantial investments. For instance, WestRock announced a $140 million corrugated box plant in Pleasant Prairie, Wisconsin to expand production capabilities for the Great Lakes region, while International Paper is converting its Alabama mill with a $250 million investment to boost containerboard output.

Innovation is also playing a major role. DS Smith introduced DryPack, a recyclable, water-resistant seafood box designed for cold chain logistics, marking a breakthrough for fiber-based packaging in food transportation. The e-commerce boom continues to be a dominant force, requiring durable corrugated mailers, inserts, and customized packaging to ensure product protection during direct-to-consumer deliveries. Combined with these trends, strategic divestments and reinvestments by leading players highlight the U.S. market’s pivot toward sustainability and high-performance solutions.

China Paperboard Packaging Market Accelerated by Plastic Reduction Policies and E-Commerce Growth

The China paperboard packaging market is strongly driven by the government’s Plastic Pollution Control Action Plan, which mandates reduced reliance on non-biodegradable plastics. This regulatory pressure is accelerating adoption of fiber-based alternatives across food, beverage, and e-commerce packaging. China’s ban and restrictions on waste paper imports have forced domestic manufacturers to enhance recycling practices and secure local raw material sources, reshaping supply chains for sustainable growth.

With e-commerce and takeaway food services expanding rapidly, the demand for cost-effective, durable, and lightweight corrugated packaging has surged. Domestic producers are making major capital investments to increase paperboard production capacity, while technological innovations in digital printing and automation are improving packaging customization, reducing waste, and optimizing large-scale production. These advancements position China as not only a high-volume producer but also a global innovator in paperboard packaging efficiency and sustainability.

Germany Paperboard Packaging Market Influenced by EU Sustainability Mandates

The Germany paperboard packaging market is closely shaped by the EU Packaging and Packaging Waste Regulation (PPWR), effective 2025, which enforces stricter recycling and waste reduction targets. Alongside this, Germany’s VerpackG law requires higher recycling rates and mandatory registration with the Central Packaging Register (ZSVR), compelling producers to deliver fully recyclable paperboard solutions.

Sustainability in supply chains is also under scrutiny due to the European Union Deforestation Regulation (EUDR), which mandates robust due diligence systems for timber sourcing by December 2025. German companies are therefore investing heavily in traceability systems and recyclable product innovation. With its strong focus on regulatory compliance, precision manufacturing, and advanced barrier technologies, Germany is solidifying its role as a benchmark for sustainable paperboard packaging in Europe.

India Paperboard Packaging Market Supported by EPR Rules and Rapid E-Commerce Growth

The India paperboard packaging market is being propelled by regulatory and economic factors. The government’s Plastic Waste Management Rules and Extended Producer Responsibility (EPR) framework have boosted demand for eco-friendly paperboard alternatives, particularly in food, retail, and logistics. In addition, the National Packaging Initiative aims to lower logistics costs, promote returnable packaging, and strengthen domestic capacity for advanced paperboard materials.

Private players are actively expanding, with domestic paper mills investing in modernization and capacity upgrades to deliver high-quality, sustainable paperboard. The e-commerce boom and food delivery expansion, led by platforms like Flipkart, Swiggy, and Zomato, are fueling demand for corrugated boxes, folding cartons, and fiber-based cushioning solutions. With government support under “Make in India” and corporate commitments to sustainability, India is emerging as a fast-growing hub for innovative and recyclable paperboard packaging solutions.

Japan Paperboard Packaging Market Driven by Plastic Waste Reduction and Green Innovation

The Japan paperboard packaging market is advancing rapidly under the government’s target to reduce plastic waste by 50% by 2030, which has positioned paperboard as a key substitute. Manufacturers are enhancing material science innovations, developing water-resistant, robust paperboard products that can effectively compete with plastics in durability and performance.

Japanese companies like Oji Holdings and Nippon Paper are leading in fiber-based material development and sustainable coatings, ensuring both printability and barrier functionality. Additionally, digital tools such as QR codes and RFID tags are being integrated into packaging for traceability and consumer engagement, turning packaging into a value-added branding tool. With its focus on premium quality, design excellence, and sustainable material innovation, Japan continues to set high standards in the global paperboard packaging industry.

United Kingdom Paperboard Packaging Market Strengthened by Plastic Packaging Tax and E-Commerce Demand

The United Kingdom paperboard packaging market has gained strong momentum due to the Plastic Packaging Tax, which applies to packaging with less than 30% recycled plastic content. This regulation provides a direct financial incentive for businesses to transition to paperboard alternatives.

The UK’s robust e-commerce and subscription box sector is fueling demand for corrugated and rigid paperboard packaging, particularly for retail, food, and premium goods. Local manufacturers are focusing on glue-free packaging innovations, including interlocking tab designs that enhance recyclability and assembly efficiency. With growing consumer preference for luxury goods packaging enhanced with embossing, foiling, and high-quality printing, the UK market demonstrates a blend of sustainability and premium branding appeal, reinforcing its position as a leading innovator in European paperboard packaging.

Paperboard Packaging Market Report Scope

Paperboard Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$393.7 Billion

|

|

Market Size (2034)

|

$616 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Corrugated Boxes, Folding Cartons, Liquid Cartons, Paperboard Cups & Trays, Other Product Types), By Material Grade (CRB, CUK, SBS, URB, Containerboard), By Application (Food & Beverages, E-commerce & Retail, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Industrial Goods, Electronics & Appliances, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group, DS Smith Plc, Oji Holdings Corporation, Mondi Group, Stora Enso Oyj, Graphic Packaging Holding Company, Packaging Corporation of America, Nippon Paper Industries Co., Ltd., Sonoco Products Company, Amcor Plc, BillerudKorsnäs AB, Huhtamäki Oyj, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paperboard Packaging Market Segmentation

By Product Type

- Corrugated Boxes

- Folding Cartons

- Liquid Cartons

- Paperboard Cups & Trays

- Other Product Types

By Material Grade

- CRB

- CUK

- SBS

- URB

- Containerboard

By Application

- Food & Beverages

- E-commerce & Retail

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Goods

- Electronics & Appliances

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paperboard Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Oji Holdings Corporation

- Mondi Group

- Stora Enso Oyj

- Graphic Packaging Holding Company

- Packaging Corporation of America

- Nippon Paper Industries Co., Ltd.

- Sonoco Products Company

- Amcor Plc

- BillerudKorsnäs AB

- Huhtamäki Oyj

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-dimensional research methodology to provide an authoritative assessment of the global Paperboard Packaging Market. Our approach integrates both primary and secondary research to ensure accuracy, reliability, and actionable insights for industry stakeholders. Primary research includes structured interviews with senior executives, product managers, and R&D heads across leading packaging manufacturers such as International Paper, WestRock, Smurfit Kappa, and Mondi Group, enabling firsthand perspectives on market trends, sustainability initiatives, and technological innovations. Secondary research encompasses the systematic review of company annual reports, press releases, regulatory filings, industry publications, and government databases to capture historical and projected market developments. Quantitative analysis leverages advanced modeling techniques, including CAGR calculations, market sizing, and segmentation by product type, material grade, application, and end-use industry. Our methodology also emphasizes regional market dynamics, accounting for country-specific regulatory frameworks, e-commerce penetration, and sustainability mandates in markets such as the U.S., China, Germany, India, Japan, and the U.K. By combining qualitative insights with rigorous data analytics, USDAnalytics delivers a robust market forecast, highlighting strategic growth opportunities, competitive intelligence, and emerging technological trends in paperboard packaging, thereby providing industry professionals with a comprehensive tool for informed decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.