Returnable Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Returnable Packaging Market Set to Reach $236.9 Billion by 2034 Driven by Cost-Efficiency and Sustainability Initiatives

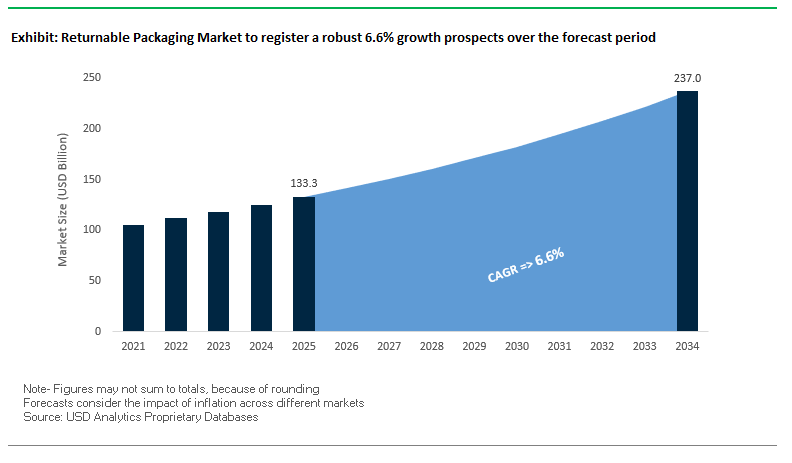

The global returnable packaging market is projected to grow from $133.3 billion in 2025 to $236.9 billion by 2034, registering a CAGR of 6.6%. The market expansion is fueled by increasing adoption of reusable transport packaging, reusable plastic containers (RPCs), and closed-loop logistics systems. Organizations across food & beverage, retail, and industrial sectors are embracing returnable packaging to reduce operational costs, lower carbon emissions, and improve supply chain efficiency.

Key Insights for industry professionals and buyers:

- Cost-Efficiency Over Time: Initial investments are offset within 12–18 months, with reusable packaging proving up to 60% more cost-effective than single-use alternatives over the product lifecycle.

- Reduction in Solid Waste: A single reusable plastic container can replace hundreds of disposable boxes, significantly minimizing landfill waste.

- Lower Carbon Footprint: Reuse and elimination of single-use waste can reduce CO2 emissions by up to 50% over a product's service life.

- Increased Supply Chain Efficiency: Standardized, durable RTP dimensions enable automated handling, minimizing product damage and optimizing logistics.

- Sustainability and Innovation: Companies are increasingly integrating recyclable materials, automated tracking, and closed-loop systems, enhancing both environmental and operational performance.

Returnable packaging is not only a cost-saving operational tool but also a critical sustainability solution, aligning with modern environmental mandates and brand responsibility goals.

Market Analysis: Strategic Partnerships and Automation Are Redefining Global Returnable Packaging Efficiency

The returnable packaging market is witnessing significant advancements in automation, sustainability, and distribution partnerships. In August 2025, Rehrig Pacific Company partnered with AutoStore, becoming its official bin manufacturing partner for the U.S., marking a key step in integrating warehouse automation with reusable packaging solutions. The same month, the Flexible Plastic Fund (FPF) and SUEZ Recycling and Recovery UK released the FlexCollect report, offering insights into integrating flexible packaging into recycling schemes, which could influence the adoption of refillable pouches in RPP systems.

Sustainability continues to drive market evolution. In June 2025, Schoeller Allibert partnered with Transoplast in the Netherlands to expand distribution, while Mondi launched sustainable packaging solutions for the pet food industry, demonstrating functional, environmentally aligned RRP applications. In March 2025, Schoeller Allibert had its near-term science-based emissions reduction targets validated by the SBTi, underscoring the commitment to carbon reduction and circular economy principles.

Technological and operational innovations also define market growth. In April 2025, SSI SCHAEFER completed a semi-automated warehouse for Rossmann in Hungary, highlighting a growing trend toward optimized intralogistics for retail. Earlier, in October 2024, Schoeller Allibert appointed a new CFO, reflecting strategic leadership shifts in major market players. The Smurfit Kappa and WestRock merger in September 2024 further expanded the geographic reach and sustainability capabilities of returnable and sustainable packaging solutions worldwide.

Returnable Packaging Market: Trends and Opportunities Driving Circular Logistics

Strategic Expansion of Pooling Systems for Cross-Industry Standardization

The returnable packaging market is undergoing a major transformation through the scaling of pooling systems, which allow companies to share standardized pallets, crates, and containers instead of managing their own assets. Leaders such as CHEP and Tosca have pioneered this model, with CHEP’s “Share & Reuse” network eliminating capital expenditure on assets while reducing hidden costs like the return transport of empties. This not only lowers operating costs but also enables companies to redirect focus toward core business operations. Beyond economics, pooling aligns directly with upcoming European Union Packaging and Packaging Waste Regulation (PPWR) targets, which require 40% of EU packaging to be reusable by 2030. Standardized pooling systems are seen as the most efficient way for industries to meet these requirements across food, beverage, retail, and industrial supply chains. By combining regulatory compliance with cost efficiency, pooling models are becoming a cornerstone of circular packaging strategies globally.

Integration of IoT and RFID for Asset Visibility and Lifecycle Management

Another transformative trend is the widespread adoption of IoT and RFID technologies to improve asset visibility and reduce losses in returnable packaging systems. The CPCON Group’s 2025 report highlights that while pallet loss rates can reach as high as 15%, RFID tracking has proven to reduce this to just 1% in supermarket chains—a dramatic improvement in circular asset retention. Beyond minimizing shrinkage, IoT-enabled solutions provide real-time lifecycle data on pallets, crates, and containers. A 2025 research paper emphasized that these technologies can achieve inventory accuracy levels above 99%, enabling automation of data collection, reducing shipping errors, and improving reverse logistics efficiency. Furthermore, route optimization based on IoT data reduces empty miles and lowers transportation emissions. As companies seek to cut costs, comply with regulations, and achieve ESG targets, digitally enabled asset management is becoming an indispensable component of the returnable packaging value chain.

Development of Lightweight, High-Strength Composite Materials

The weight and durability of returnable assets remain key barriers to efficiency, creating opportunities for composite material innovation. Traditional wooden and plastic pallets add significant weight to shipments, increasing transport-related emissions and costs. Research from AIMPLAS highlights fiber-reinforced polymer composites that deliver superior strength-to-weight ratios, significantly reducing asset weight while maintaining robustness. Lightweight pallets and containers not only reduce fuel consumption but also improve load efficiency across long-haul supply chains. At the same time, new high-strength plastics and composites are improving durability. According to CDF Corporation, innovations in lightweight yet damage-resistant materials extend the lifecycle of containers and crates, lowering replacement rates and reinforcing circularity. By combining lower transportation emissions with enhanced asset longevity, these materials represent a key opportunity for sustainable growth in returnable packaging.

Expansion into B2C Reusable Packaging Models and Reverse Logistics

While business-to-business (B2B) returnable systems are mature, the business-to-consumer (B2C) segment remains an untapped growth opportunity. With the surge of e-commerce, single-use packaging has become a critical environmental challenge, creating strong demand for consumer-friendly reusable models. A 2025 LUT University thesis on sustainable reverse logistics noted that scalable B2C reuse will require dedicated systems including consumer incentives, convenient drop-off points, and streamlined collection logistics. Supporting this, the Government of the Netherlands reported that return models with automated collection machines, neighborhood drop-off hubs, and financial incentives substantially boost consumer participation rates. These strategies make reusables more appealing than disposables, closing the loop on packaging used in online retail and last-mile delivery. For brands and retailers, investing in B2C reusable packaging not only addresses waste but also strengthens sustainability credentials and consumer loyalty.

Competitive Landscape: Leading Players Are Driving Sustainability, Automation, and Cost-Optimization in Returnable Packaging

The returnable packaging industry is highly competitive, with top companies focusing on reducing carbon footprints, improving supply chain efficiency, and delivering high-value reusable solutions. Market leaders are investing in automation, sustainable materials, and integrated service models to differentiate themselves.

Schoeller Allibert: Driving Sustainability and Strategic Distribution Partnerships in Reusable Packaging

Schoeller Allibert manufactures returnable plastic crates, foldable large containers (FLCs), pallets, and dollies for multiple industries, including automotive, food & beverage, and retail. In June 2025, it partnered with Transoplast as a Platinum Partner in the Netherlands, expanding its European distribution network. The company has earned an EcoVadis gold rating and had its science-based emissions targets validated by the SBTi. Its solutions optimize logistics, reduce waste, and enhance sustainability across global supply chains.

Rehrig Pacific Company: Integrating Reusable Packaging with Automated Warehouse Solutions

Rehrig Pacific produces sustainable pallets, crates, and roll-out carts. Its August 2025 partnership with AutoStore underscores its move into automated warehouse solutions. The company recently launched a 100% recyclable GMA Rackable Plastic Pallet with integrated monitoring for temperature, shock, and vibration, crucial for safe transport. Its products are widely used in beverage, dairy, and retail industries, supporting direct store delivery (DSD) operations.

Myers Industries, Inc.: Leveraging Rotational Molding Expertise for Durable Returnable Solutions

Myers Industries offers reusable bulk containers, pallets, and other durable plastic solutions. The company’s Focused Transformation program streamlines operations, with plans in July 2025 to optimize production facilities. Its rotational molding expertise ensures long-lasting, high-performance packaging suitable for industrial and consumer applications, improving supply chain efficiency and waste reduction.

SSI SCHAEFER: Pioneering Automated Logistics Solutions for Returnable Packaging

SSI SCHAEFER provides automated storage and retrieval systems, conveyors, and AGVs essential for robust returnable packaging operations. In April 2025, it completed a semi-automated warehouse for Rossmann, highlighting optimized intralogistics in retail. Its circular economy strategy and technologies like SSI LOGIMAT® Vertical Lift Module enhance efficiency, reduce costs, and support sustainable packaging operations across industries.

Nefab AB: Offering Customized Returnable Packaging Solutions through Global Integration

Nefab, now part of DS Smith, specializes in reusable packaging for automotive, telecom, and industrial sectors. Its engineering and design capabilities ensure products are protected and returnable throughout the supply chain. Nefab’s global network and full-service solution approach allow complex supply chains to operate efficiently, reinforcing its position as a key provider of optimized, sustainable returnable packaging solutions.

Returnable Packaging Market Share Insights, 2025-2034

Pallets dominate Market Share by Product Type in the Returnable Packaging market

Pallets hold the largest share at around 40%, cementing their position as the backbone of global logistics in the returnable packaging industry. Their dominance stems from standardization and durability, with plastic and metal pallets increasingly replacing traditional wooden models in high-turnover supply chains. Pooling systems such as CHEP and Loscam allow companies to outsource asset management, while closed-loop models in automotive and FMCG ensure pallets circulate between suppliers and manufacturers without waste. Crates & totes follow closely with 25%, acting as the workhorses of parts handling and just-in-time production lines, especially in automotive and electronics. Intermediate bulk containers (IBCs) secure 15%, favored for liquid and granular bulk transfer in chemicals, food, and pharma where efficiency, safety, and reusability are paramount. Drums & barrels contribute 12%, vital for hazardous and high-value goods where container strength and certification outweigh cost. Collapsible bins, though holding just 8%, are gaining traction as space-saving assets, minimizing return freight costs by collapsing up to 80%. This segmentation underscores how pallets dominate through scale and universality, while niche product types thrive by addressing sector-specific efficiency and regulatory needs.

Automotive leads Market Share by End-Use Industry in the Returnable Packaging market

The automotive industry commands the largest share at 30%, reflecting its status as the earliest and most sophisticated adopter of returnable packaging. Just-in-time (JIT) manufacturing models demand specialized crates, pallets, and totes that guarantee seamless flow of components with zero tolerance for damage or delay. Food & beverages follow with 25%, where reusable plastic crates (RPCs) dominate fresh produce, meat, and bakery logistics due to their washability, hygiene compliance, and shelf-life extension benefits. E-commerce & retail represent 20% of share, rapidly scaling returnable systems for back-of-store replenishment, fulfillment centers, and pilot programs in last-mile delivery where closed-loop tote systems are being tested. Consumer goods account for 10%, deploying returnables in upstream logistics for electronics, household goods, and non-perishables to reduce costs and damage rates. Healthcare & pharmaceuticals contribute 8%, driven by stringent regulatory requirements that necessitate validated washing, sterilization, and traceability for transport of sensitive medical devices and supplies. Chemicals hold 7%, where returnable IBCs and UN-certified drums provide safety, compliance, and lifecycle management for hazardous materials. Collectively, these industry dynamics confirm that automotive and food & beverage remain the primary drivers, while e-commerce is emerging as the fastest-growth end-user pushing innovation in reverse logistics and tracking technologies.

European Union: PPWR and Reusable Packaging Mandates Reshaping Market Dynamics

The European Union returnable packaging market is undergoing a significant transformation driven by stringent regulations under the Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025. The PPWR replaces older directives and sets ambitious requirements for reuse, recyclability, and circular economy principles. One of the most impactful provisions is the establishment of reuse targets, mandating companies to offer a percentage of their products in reusable or refillable packaging, particularly in takeaway food and beverage segments. This regulatory push is expected to accelerate innovation in returnable containers, deposit systems, and multi-use packaging materials.

The EU is also promoting the widespread adoption of Deposit Return Systems (DRS) to increase collection efficiency and reduce littering. Germany leads the bloc with its reusable packaging obligation implemented in January 2023, requiring catering businesses to provide reusable alternatives at no extra cost. Complementary frameworks like the Ecodesign for Sustainable Products Regulation (ESPR), which introduces a Digital Product Passport, will further enhance transparency on material origin and compliance. Restrictions on substances such as PFAS in food-contact packaging from August 2026 are also steering innovation toward safer, sustainable materials. Collectively, these measures position Europe as a pioneer in shaping global returnable packaging standards.

United States: EPR Legislation and Circular Economy Partnerships Driving Adoption

In the United States, the returnable packaging market is gaining momentum under Extended Producer Responsibility (EPR) laws, now enacted in seven states. For example, Maryland’s EPR law mandates that Producer Responsibility Organizations (PROs) cover 90% of packaging waste management costs by 2030, a landmark step in shifting responsibility from municipalities to manufacturers. Such policies are fueling large-scale investments in packaging redesign and return systems that support closed-loop recycling and reuse models.

Technological adoption is equally pivotal. The U.S. market is witnessing the rapid use of advanced digital printing platforms, such as UV-curable and eco-solvent inks, enabling durable branding on returnable and recycled packaging substrates. Rising demand for mono-material designs and greater recycled content reflects industry efforts to simplify recycling streams. Federal funding from the Infrastructure Investment and Jobs Act is supporting the buildout of advanced recycling and manufacturing facilities. Meanwhile, partnerships with initiatives like the U.S. Plastics Pact are aligning states, companies, and NGOs toward national circular economy targets. Together, regulatory support and private innovation are reinforcing the U.S. as a dynamic hub for returnable packaging adoption.

China: Regulatory Mandates and E-Commerce Fueling Returnable Packaging Systems

The China returnable packaging market is expanding rapidly under government mandates and the explosive growth of e-commerce. Effective June 1, 2025, new regulations require express delivery companies to prioritize reusable and eco-friendly packaging, creating substantial demand for returnable boxes, crates, and circulation systems. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are spearheading regulatory frameworks under the 14th Five-Year Plan, with a focus on reducing plastic pollution and encouraging green manufacturing practices.

Major logistics providers, including JDL Express and SF Express, are already rolling out reusable circulation boxes to replace single-use cardboard. These shifts align with China’s Dual Circulation strategy, which emphasizes domestic consumption and sustainability. Community-driven programs, such as Zhejiang University’s package reuse initiative, are further embedding reuse culture at a consumer level. Additionally, government tax incentives for remanufacturing industries are encouraging investment in scalable green packaging solutions. These policies and trends highlight China’s leadership in integrating returnable packaging into its fast-growing e-commerce and logistics sectors.

India: EPR Rules and Traceability Driving Market Expansion

The India returnable packaging market is shaped by the Plastic Waste Management (Amendment) Rules, 2024, which place a strong emphasis on Extended Producer Responsibility (EPR) for manufacturers, importers, and brand owners. While MSMEs are exempted from EPR obligations, responsibility is shifted to upstream suppliers, creating an industry-wide push toward sustainable packaging design and return systems. A critical regulatory development requires that, starting July 2025, plastic products be traceable via barcodes, QR codes, or unique numbers, ensuring accountability and transparency in packaging waste management.

The market is also driven by India’s growing processed food and FMCG consumption, fueling demand for cost-efficient, reusable packaging options. Labeling standards mandate disclosure of recycled content under IS 14534: 2023, pushing companies to innovate with returnable formats in food, beverages, and dairy sectors. Parallel trends in bioplastic development from agricultural and dairy waste—including patents for ghee residue-based bioplastics—add another sustainable layer to India’s evolving packaging ecosystem. With rising consumer demand and regulatory enforcement, India is emerging as a strong growth market for refillable and returnable packaging solutions.

Japan: Plastic Resource Circulation Strategy Accelerating Refillable Packaging

The Japan returnable packaging market is guided by the government’s Plastic Resource Circulation Strategy, which mandates that by 2025 all plastic goods and packaging must be reusable or recyclable. This ambitious roadmap is reinforced by targets to double renewable material usage by 2030 and enforce stricter waste sorting at collection points to boost efficiency. As part of this shift, leading companies like Shiseido and Tokiwa Cosmetics are pioneering refillable and reusable packaging formats in the personal care and beauty sector, launching refill systems for creams, serums, and foundations.

Japanese companies are also advancing innovative paper-based barrier materials, such as Nippon Paper Industries’ SHIELDPLUS, which prevents oxygen and odor transmission while remaining recyclable. This aligns with Japan’s broader circular economy goals that emphasize compostable and easily recyclable materials. The country’s emphasis on combining technological innovation with consumer convenience ensures it remains a leading market for premium returnable packaging solutions in both consumer goods and industrial applications.

Brazil: Reverse Logistics and Solid Waste Policy Reinforcing Market Growth

In Brazil, the returnable packaging market is closely tied to regulatory and policy initiatives, particularly the National Solid Waste Policy (PNRS), which mandates responsible waste management, reuse, and recycling. The government is actively promoting reverse logistics systems, requiring producers to take responsibility for post-consumer collection and recycling, which directly strengthens demand for returnable packaging models.

With Law No. 15,088 (January 2025) banning imports of various solid wastes—including plastics, glass, and paper—Brazil is prioritizing domestic recycling and reuse solutions. This restriction is pushing local industries to invest in more sustainable and circular packaging practices. The overarching goal is to curb solid waste generation, increase packaging reuse, and promote sustainable consumption models. These measures, combined with growing corporate commitments, ensure that Brazil continues to scale adoption of returnable packaging systems across retail, FMCG, and logistics sectors.

Returnable Packaging Market Report Scope

Returnable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$133.3 Billion

|

|

Market Size (2034)

|

$236.9 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material (Plastics, Wood, Metal, Glass, Paper & Paperboard), By Product Type (Pallets, Crates & Totes, Drums & Barrels, IBCs, Collapsible Bins), By End-Use Industry (Automotive, Food & Beverages, Consumer Goods, E-commerce & Retail, Healthcare & Pharmaceuticals, Chemicals), By Circulation Model (Closed-Loop Systems, Open-Loop Systems, Pooling Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Returnable Packaging Market Segmentation

By Material

- Plastics

- Wood

- Metal

- Glass

- Paper & Paperboard

By Product Type

- Pallets

- Crates & Totes

- Drums & Barrels

- IBCs

- Collapsible Bins

By End-Use Industry

- Automotive

- Food & Beverages

- Consumer Goods

- E-commerce & Retail

- Healthcare & Pharmaceuticals

- Chemicals

By Circulation Model

- Closed-Loop Systems

- Open-Loop Systems

- Pooling Services

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Returnable Packaging Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to deliver precise, actionable insights into the global returnable packaging market, combining extensive secondary research with targeted primary inputs. Our approach begins with the collection of verified data from company filings, government reports, trade journals, sustainability disclosures, and industry publications to identify trends in reusable packaging, pooling systems, and closed-loop logistics. Primary research includes interviews with packaging manufacturers, logistics providers, retailers, and end-users across food & beverage, automotive, e-commerce, and industrial sectors to understand operational efficiency gains, sustainability metrics, and adoption challenges. USDAnalytics leverages quantitative modeling to forecast market growth, incorporating factors such as material innovation, asset lifecycle management, regulatory impact (EPR, PPWR, and Plastic Waste Management rules), and technological trends including IoT and RFID-enabled tracking. Regional market dynamics, mergers and acquisitions, and strategic partnerships are analyzed to evaluate competitive positioning and investment opportunities. The methodology emphasizes cost-benefit analysis, carbon footprint reduction, and supply chain optimization, ensuring that insights support strategic decision-making for industry professionals seeking to capitalize on the expanding global returnable packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.