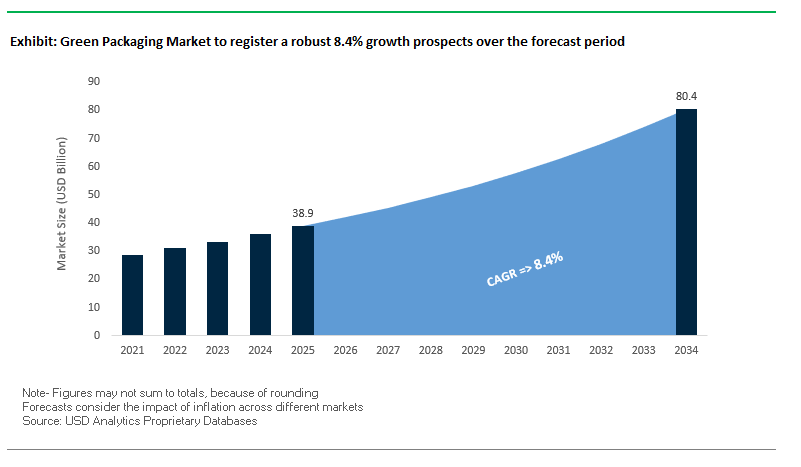

Market Overview: Green Packaging Valued at $38.9 Billion in 2025; On Track for $80.4 Billion by 2034

The Global Green Packaging Market is valued at USD 38.9 billion in 2025 and projected to reach USD 80.4 billion by 2034, expanding at a robust CAGR of 8.4%. No longer a niche sustainability play, green packaging has become a core lever of corporate strategy and brand differentiation spanning recyclable plastics, biodegradable materials, paper-based formats, rPET, and reusable/refill systems. The market is being reshaped by 100% reusable/recyclable/compostable targets by 2025, fast-growing e-commerce and last-mile logistics, and the operational push toward mono-material packaging that fits existing recovery infrastructure. For procurement and R&D teams, design choices now balance carbon intensity, sortability, barrier performance, and end-of-life economics, not just cost per unit.

Key Insights for industry professionals

- 2025 corporate pledges (100% reusable/recyclable/compostable) are pulling through large-scale material transitions.

- Recyclability outranks biodegradability in consumer purchase drivers across major markets.

- E-commerce durability + lightweighting now co-optimize damage rates, freight cost, and carbon.

- Mono-material structures accelerate MRF sortability and true circularity at scale.

- Refill/reuse pilots are moving from boutique to mainstream in personal care and beverages.

Market Analysis: Recent Developments Signaling Scale-Up of Circular Packaging (2025)

August 2025 saw a leading flexible converter launch PFAS-free, industrially compostable food pouches for the ready-to-eat segment evidence that chemical safety and end-of-life design are converging in food packaging. In July 2025, a global consumer brand partnered with a tier-one manufacturer on urban refill pilots for personal care SKUs, explicitly targeting single-use plastic reduction. That same month, trade coverage flagged a sharp rise in M&A within flexible green packaging, as strategics acquire niche technologies (barrier papers, solvent-free laminations, bio-based resins) to accelerate roadmaps.

Momentum continued into June 2025, when Mondi and a pet-nutrition partner launched a fully recyclable mono-material pouch, underscoring the shift away from multi-layer, hard-to-recycle laminates. In May 2025, a top packaging firm introduced a paper-based barrier film for snacks to displace legacy multi-polymer stacks while maintaining grease/oxygen protection. April 2025 brought a major beverage company’s rPET commitment live with a Southeast Asia bottling site producing 100% rPET, cutting regional footprint and virgin resin use. Policy and funding are also aligning: March 2025 delivered state-backed R&D support for bio-polymers and biodegradables in a key EU market, while January 2025 marked Huhtamaki’s fifth consecutive EcoVadis Gold, reinforcing investor confidence in credible ESG execution.

Collectively, these milestones chart a clear direction: scale manufacturing of circular substrates (rPET, mono-PE/PP, barrier papers), elimination of PFAS and legacy chemistries, rapid refill/reuse experimentation, and public-private funding for bio-based pathways. For category leaders, the competitive edge lies in owning design-for-recycling IP, LCAs proving total-cost-of-sustainability, and retail-tested e-commerce durability (ISTA-6).

Key Trends and Emerging Opportunities Shaping the Green Packaging Market Landscape

Legislative Mandates Driving Mono-Material and Recyclable Packaging Design

The green packaging market is witnessing a significant shift driven by regulatory frameworks such as Extended Producer Responsibility (EPR) laws and plastic taxes. FMCG companies are redesigning packaging structures to comply with these mandates, prioritizing mono-material, recyclable packaging in existing polyethylene (PE) and polypropylene (PP) recycling streams. The European Union's Packaging and Packaging Waste Regulation (PPWR) requires all Member States to implement EPR schemes by 2024, introducing modulated fees for non-recyclable packaging, thereby incentivizing brands to adopt circular packaging solutions. Additionally, the EU plastic tax and similar national levies in the UK and Spain further escalate the financial benefits of using recyclable materials. Reports from Europen indicate that these mandates are reshaping corporate packaging strategies, shifting focus from aesthetics and shelf life to designing packaging that is optimized for recyclability and minimizes environmental impact, positioning brands as compliant and sustainability-focused leaders in the green packaging domain.

Strategic Investment in Advanced Polymer Recycling Infrastructure

A parallel trend in the green packaging market is the substantial investment by major chemical and packaging corporations into advanced recycling facilities. Unlike mechanical recycling, chemical recycling breaks down plastics to their molecular building blocks, producing virgin-quality recycled polymers suitable for sensitive applications like food-contact packaging. Dow’s equity investment in Xycle for a chemical recycling plant at the Port of Rotterdam, with a 21-kiloton annual processing capacity, exemplifies this global trend. Similarly, Ester Industries’ ₹1,600 crore project in Gujarat, India, highlights the regional expansion of advanced recycling to convert polyester textile waste into virgin-quality PET resin. Technologies like pyrolysis enable the production of high-purity feedstock from multi-layer films, crucial for creating circular, food-grade packaging streams and reducing dependence on virgin plastics, driving sustainable supply chain integration.

Development of High-Barrier, Bio-Based Coatings for Paper Packaging

There is a clear market opportunity in developing bio-based, compostable, and recyclable barrier coatings to replace polyethylene (PE) and PFAS coatings in paper-based packaging. Such innovations unlock potential for paperboard use in liquid and grease-resistant applications like beverages, soups, and fast food packaging. Smart Planet Technologies’ EarthCoating-Bio, combining bio-based PLA with a mineral blend, reduces plastic content by up to 51% while being industrially compostable and recyclable. Similarly, Omya’s EarthGuard and EarthWrap coatings are designed for full repulpability, addressing a critical barrier for paper adoption. This trend directly responds to environmental scrutiny of PFAS chemicals and fossil-fuel-based PE, driving demand for sustainable, food-safe, high-barrier coatings that support circular packaging solutions across the green packaging market.

Integration of Digital Watermarks for Precision Recycling

Digital watermarking technologies, such as HolyGrail 2.0, represent a transformative opportunity to enhance material recovery facility (MRF) efficiency and produce high-value recycled streams. By embedding digital watermarks in packaging, combined with near-infrared (NIR) detection, sorting accuracy reaches up to 99%, with a 95% ejection rate for specific polymers. This precision allows manufacturers to generate food-grade recycled PET (rPET) or polypropylene (rPP) feedstock suitable for reuse in packaging, facilitating compliance with EPR requirements and advancing circular economy goals. Additionally, digital watermarks enable traceability and align with the EU’s upcoming Digital Product Passport (DPP), offering a platform for packaging producers to provide end-of-life information while integrating consumer and regulatory transparency, thereby driving adoption of digital-enabled green packaging solutions globally.

Competitive Landscape: System Integrators and Material Innovators Setting the Pace

A concentrated set of players is executing at scale across fiber systems, flexible mono-materials, rPET loops, and refillable formats. Differentiation hinges on material science depth, circular infrastructure partnerships, and verified ESG performance.

Huhtamaki: Fiber-first circularity with executable ESG

Overview: Huhtamaki positions itself as a first-choice sustainable packaging supplier via its “Blue Loop” circularity strategy and science-based climate targets. It pairs fiber molding and flexible mono-material know-how with credible ESG reporting.

Recent launches include recyclable/compostable ice-cream solutions and ProDairy™ single-coated paper cups (<10% plastic) that improve recyclability. The portfolio spans fiber-based trays, molded fiber, and flexible structures designed for curbside compatibility and lower CO₂e. Global manufacturing depth, continuous water/energy efficiency programs, and multi-region customer support make Huhtamaki a resilient partner for brands scaling retail-ready fiber formats and plastic reduction without compromising barrier needs.

Amcor: Scale synergies and mono-material flexible leadership

Overview: Amcor is executing a dual play of material innovation and M&A integration, targeting high-circularity formats and PCR content.

Following its April 2025 combination with Berry Global, Amcor broadened access to material science, blown-film, and forming technologies to speed PCR/rPCR adoption and recyclable mono-PE/PP platforms. Partnerships (e.g., with European specialists) yielded recyclable pouches cutting plastic up to ~80% versus legacy formats. Amcor’s emphasis on design-for-recycling, e-commerce-certified pouches, and food-grade PCR positions it to serve global CPGs seeking rapid, compliant portfolio transitions.

Mondi: Paper-based barriers and “sustainable by designOverview: Mondi’s MAP2030 targets make 100% of packaging reusable/recyclable/compostable by 2025, enabled by expertise across paper and flexible plastics.

Innovations range from paper mailers for e-commerce to mono-material liquid pouches and FunctionalBarrier Papers that replace plastic in many food applications. Mondi’s dual-material mastery enables data-driven substrate selection paper where feasible, recyclable plastics where required to balance barrier, machinability, and recyclability. Collaborations like the fully recyclable pet-food pouch (June 2025) exemplify commercialization at scale.

Tetra Pak: Decarbonizing aseptic with renewable layers

Overview: Tetra Pak aims to deliver the world’s most sustainable food package, maximizing renewable/recycled content while enabling ambient logistics.

Programs to replace fossil-based plastic layers with fiber are progressing alongside partner work with leading paperboard suppliers. The core aseptic carton already leverages FSC-certified boards; Tetra Recart® markets a significantly lower carbon footprint than cans for shelf-stable foods. Tetra Pak’s role as a system integrator (filling lines + materials + collection partnerships) is pivotal to end-to-end circularity.

Smurfit Kappa: Corrugated scale for e-commerce and retail-ready

Overview: Post-combination with WestRock, Smurfit Kappa is a global corrugated powerhouse with closed-loop fiber systems.

Investments target Retail-/Shelf-Ready Packaging and high-graphic boxes that elevate brand experience while staying recyclable and lightweight. A new U.S. corrugated plant expands North American capacity. Circular strength comes from integrated recycled paper mills, enabling lighter, stronger board grades with verified recovery rates ideal for e-commerce, perishables, and omni-channel fulfillment.

DS Smith: Circular design that replaces problem plastics

Overview: DS Smith’s strategy “Redefining Packaging for a Changing World” prioritizes circular design, recyclability, and fiber loop durability.

Its target to remove 1 billion pieces of problem plastic by 2025 guides innovations such as ECO Bowl (plastic-reduced trays) and collaborations on Hydropol™ (biodegradable laminate alternatives). With 700+ designers and integrated recycling operations, DS Smith designs mono-material fiber solutions that flow through municipal systems while maintaining machinability and shelf presence.

Green Packaging Market Share Insights

Paper and Paperboard Dominate Market Share by Material in the Green Packaging Industry

Paper and paperboard command the largest share of the green packaging industry at around 45%, underscoring their position as the most established and scalable sustainable material. Their dominance is supported by extensive recycling infrastructure, strong consumer preference for fiber-based solutions, and regulatory mandates that target reductions in single-use plastics. Corrugated boxes for e-commerce, paper-based foodservice clamshells, and cartons for dry goods are now default choices in both developed and emerging markets. Key innovations, such as water-based and PFAS-free barrier coatings, are expanding their suitability for applications traditionally reserved for plastic, such as greasy foods, dairy products, and beverages. Plastic retains about 25% share, but primarily through recycled polymers like rPET and rHDPE, demonstrating that the “green” value lies in circularity rather than virgin use. Bio-based polymers (PLA, PHA), while smaller in volume, represent the innovation frontier and are projected to grow rapidly as composting infrastructure improves. Glass and metals remain stable, niche categories, positioned for premium products and benefiting from their infinite recyclability and high post-consumer recovery rates.

Food and Beverages Drive the Largest Share by End-Use Industry in the Green Packaging Market

Food and beverages dominate the green packaging industry with an estimated 55% market share, making them the most influential sector in shaping material innovation and adoption. This share is driven by the sheer volume of single-use items in foodservice, packaged beverages, and grocery distribution, which are under intense scrutiny from regulators and consumers alike. Bans on polystyrene and single-use plastics in regions such as the EU and parts of North America are accelerating the transition to compostable clamshells, rPET beverage bottles, and recyclable aluminum cans. Consumer goods, holding around 20% share, are the second-largest driver, propelled by e-commerce packaging that demands lightweight yet durable recycled fiberboard and mono-material designs to enhance recyclability. Cosmetics and personal care adopt green packaging as a premium branding tool, leveraging glass jars, recycled plastics, and bio-based containers to appeal to eco-conscious consumers. Pharmaceuticals remain conservative due to stringent safety requirements but are gradually adopting recycled-content secondary packaging. Industrial applications, though smaller, highlight efficiency-driven sustainability initiatives, particularly reusable and bulk shipping systems that reduce total material throughput.

United States: EPR Laws and Technological Advancements Reshape Green Packaging Market

The U.S. green packaging market is undergoing a rapid transformation, driven by evolving regulations and technological breakthroughs. As of 2025, seven states, including Maryland and Washington, have passed Extended Producer Responsibility (EPR) laws for packaging, placing the burden of waste management directly on producers. These laws are not only reshaping supply chains but also incentivizing manufacturers to adopt recyclable and compostable packaging solutions at scale. A major trend in the U.S. sustainable packaging market is the rising adoption of paper-based and recycled materials, as they are cost-effective, widely accepted in recycling systems, and preferred by environmentally conscious consumers.

On the innovation front, AI-powered automated recycling systems are redefining efficiency by identifying, sorting, and processing materials with precision. Corporate initiatives further accelerate this growth, with companies such as Georgia-Pacific investing in water-based barrier coatings as sustainable alternatives to traditional corrugated box coatings. Additionally, the Inflation Reduction Act of 2022 continues to provide tax credits for energy-efficient upgrades, influencing corporate sustainability initiatives. With the explosive growth of e-commerce, durable, lightweight, and eco-friendly packaging is in demand, creating a fertile ground for companies that offer both protective strength and environmental responsibility.

Germany: Circular Economy Leadership and Sustainable Innovations Define the Market

Germany stands as a frontrunner in the global green packaging market, with stringent regulations shaping industry practices. The EU Packaging and Packaging Waste Regulation (PPWR), effective since February 2025, mandates that all packaging be recyclable or reusable by 2030, pushing German companies to pioneer next-generation substrates such as grass paper and high-strength recycled fibers. The Packaging Act (Verpackungsgesetz) further reinforces this shift, ensuring producers are accountable for the full life cycle of their packaging.

Sustainability commitments are evident in both retail and manufacturing. For example, Aldi introduced sour cream cups made from 30% recycled polystyrene in August 2025, a clear reflection of corporate responsibility aligning with consumer expectations. Additionally, the German Packaging Award 2025 spotlighted 14 sustainability-focused innovations, ranging from bio-based alternatives to material reduction strategies. These advancements, supported by a highly efficient recycling infrastructure, solidify Germany’s role as a global leader in circular economy-driven green packaging solutions.

China: Dual Carbon Goals and E-commerce Growth Fuel Sustainable Packaging

China’s green packaging market is being reshaped by government mandates and the booming e-commerce economy. The “dual carbon” policy, aimed at achieving carbon peak and neutrality, is a powerful driver encouraging companies to adopt eco-friendly and reusable materials. The government has tightened restrictions on non-degradable plastics, creating strong demand for paper-based packaging and alternative sustainable solutions.

Technological innovation is also central to China’s market growth, with manufacturers integrating AI, 5G, and industrial internet solutions to enhance automation and flexible production capabilities. The rapid expansion of e-commerce platforms like Alibaba and JD.com has intensified demand for customizable and durable sustainable packaging, fueling market consolidation as smaller players exit due to stricter environmental regulations. Furthermore, the “Made in China 2025” strategy aims to increase domestic content of core packaging materials to 70% by 2025, positioning China as a strategic hub for advanced green packaging innovation and supply chain dominance.

India: Regulatory Shifts and Consumer Preferences Drive Green Packaging Growth

India’s green packaging industry is gaining momentum through a mix of government initiatives, regulatory mandates, and shifting consumer behaviors. The amended Plastic Waste Management Rules, effective July 2025, now mandate on-pack barcodes or QR codes for plastic packaging to ensure traceability under Extended Producer Responsibility (EPR). This regulatory tightening is accelerating the shift toward recyclable and biodegradable packaging formats. Government-led programs like “Make in India” and “Zero Effect Zero Defect” further provide regulatory support and investment incentives, boosting domestic production capabilities.

A growing middle-class consumer base with higher disposable incomes is fueling demand for convenient, single-serve, and sustainable packaging solutions. The healthcare and pharmaceutical sectors, in particular, are driving significant growth as they increasingly require tamper-proof and eco-friendly packaging formats. Strategic industry partnerships are also shaping the sector for instance, Indorama Ventures and PepsiCo’s recycling joint venture reflects growing corporate responsibility toward circular packaging models. With rapid urbanization and expanding commercial hubs, India is emerging as one of the fastest-growing markets for green packaging in Asia.

Brazil: Regulatory Enforcement and Technological Investments Propel Market Expansion

The Brazilian green packaging market is evolving under strict environmental regulations and increasing demand for sustainable alternatives. The National Solid Waste Policy has created a strong legislative push against plastics, encouraging the adoption of reusable and recyclable materials. In addition, a 2025 law banning the import of solid waste, including plastics, has spurred domestic waste management innovations while reducing dependency on external waste processing.

Technological advancements such as robotics and AI in packaging processes are boosting efficiency, enabling defect detection, automated sorting, and sustainable material optimization. Major investments from companies like Klabin, which is developing high-strength papers suited for humid climates and fruit exports, highlight Brazil’s role in material innovation. Regulatory oversight from ANVISA, including traceability requirements in the food and beverage sector, further elevates demand for sustainable and serialized packaging. Together, these factors position Brazil as a critical emerging market in the global green packaging industry, especially for Latin American supply chains.

Japan: Bio-based Materials and Functional Innovation Lead Green Packaging

Japan’s green packaging market is heavily influenced by advanced recycling systems and a strong regulatory framework. Under the Containers and Packaging Recycling Law, businesses are mandated to contribute to material collection and reuse, fostering a closed-loop recycling ecosystem. A major regulatory update in May 2025 by Japan’s Ministry of Health, Labour and Welfare introduced stricter food-contact packaging standards, ensuring compliance with global benchmarks on material safety.

The market is also characterized by rapid innovation in bio-based materials and packaging functionality. Companies like Shiseido, in collaboration with LyondellBasell, are incorporating bio-based polypropylene into packaging solutions, highlighting Japan’s leadership in sustainable material adoption. At the same time, manufacturers are investing in high-performance packaging with enhanced dimensional stability and durability to meet the demands of pharmaceuticals, cosmetics, and e-commerce logistics. With the rapid rise of e-commerce, Japan’s adoption of customizable, sustainable packaging is accelerating, positioning the country as a technological leader in the Asia-Pacific green packaging landscape.

Green Packaging Market Report Scope

Green Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.9 Billion

|

|

Market Size (2034)

|

$80.4 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Material (Paper & Paperboard, Plastic, Glass, Metal, Bio-based Materials), By Packaging Type (Recycled Content Packaging, Reusable Packaging, Degradable Packaging), By End-Use Industry (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Consumer Goods, Industrial, Other End-Use Industries), By Application (Primary Packaging, Secondary Packaging, Tertiary Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, WestRock Company, Smurfit Kappa Group, Amcor plc, Mondi Group, Tetra Pak, DS Smith Plc, Ardagh Group, O-I Glass, Stora Enso, Billerud AB, Ball Corporation, Sonoco Products Company, Huhtamäki Oyj, Novolex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Green Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastic

- Glass

- Metal

- Bio-based Materials

By Packaging Type

- Recycled Content Packaging

- Reusable Packaging

- Degradable Packaging

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Cosmetics & Personal Care

- Consumer Goods

- Industrial

- Other End-Use Industries

By Application

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Green Packaging Market

- International Paper

- WestRock Company

- Smurfit Kappa Group

- Amcor plc

- Mondi Group

- Tetra Pak

- DS Smith Plc

- Ardagh Group

- O-I Glass

- Stora Enso

- Billerud AB

- Ball Corporation

- Sonoco Products Company

- Huhtamäki Oyj

- Novolex

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-faceted research methodology to deliver accurate and actionable insights into the Green Packaging Market. Our approach combines primary research, including interviews and surveys with key stakeholders such as packaging manufacturers, material suppliers, FMCG brands, and regulatory authorities, with secondary research from verified industry reports, scientific journals, government publications, and corporate disclosures. Quantitative analyses, such as market sizing, historical trend extrapolation, and CAGR computation, are complemented by qualitative assessments of technological innovations, sustainability initiatives, and regulatory impacts. We also integrate regional market intelligence to evaluate country-specific dynamics, including EPR regulations, dual carbon policies, and circular economy adoption, ensuring the research is globally relevant. Competitive benchmarking incorporates financial performance, product portfolios, mergers and acquisitions, and R&D activity to map strategic positioning. USDAnalytics further employs scenario-based modeling to assess future market trajectories, factoring in evolving consumer preferences, material innovations (rPET, bio-based polymers, mono-material solutions), and digital recycling advancements. This robust methodology ensures that stakeholders receive precise, reliable, and actionable insights for strategic planning, investment, and product development within the rapidly evolving green packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.