Market Overview: Recycling Leadership and Evolving Packaging Preferences

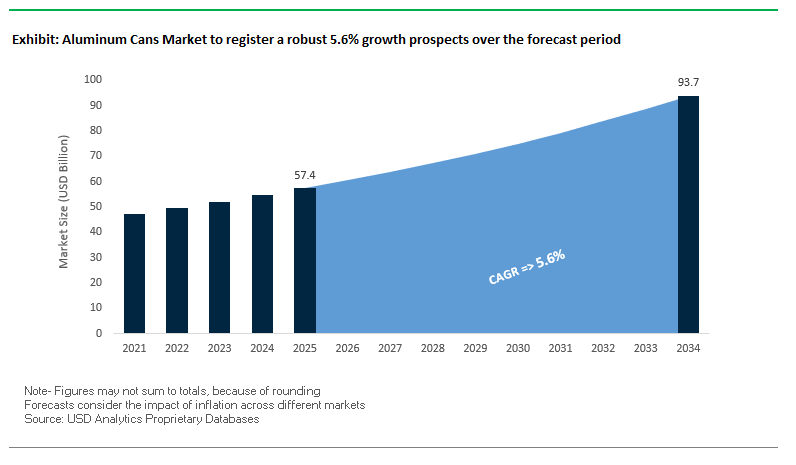

The global aluminum cans market is projected to reach USD 57.4 billion in 2025 and expand to USD 93.7 billion by 2034, reflecting a healthy CAGR of 5.6%. This growth is supported by aluminum’s unique recyclability advantages, widespread adoption across beverage and food industries, and consumer-driven demand for sustainable, lightweight, and visually appealing packaging formats.

Aluminum cans remain a dominant choice due to their 70%+ recycling rate in developed regions, aligning with sustainability mandates and helping reduce reliance on primary aluminum production, which is highly energy-intensive. The 2-piece aluminum can remains the industry standard, driven by manufacturing efficiency, cost savings, and suitability for high-speed production lines. The rise of premium and craft beverages, such as craft beer, seltzers, and energy drinks, has further positioned aluminum cans as the preferred packaging solution, owing to their ability to protect flavor and extend shelf life by blocking light and oxygen. Additionally, the shift toward smaller formats, including slim and sleek cans, is shaping consumer preferences in the RTD cocktail, coffee, and energy drink segments, combining convenience with strong retail branding.

Key Insights for Industry Professionals:

- 70%+ recyclability rates make aluminum a cornerstone of the circular economy.

- 2-piece can technology dominates global production due to efficiency and speed.

- Premium and craft beverage launches increasingly choose aluminum for product quality preservation.

- Smaller formats drive growth, with slim designs gaining traction in energy drinks and RTD cocktails.

Market Analysis: Strategic Expansions and Sustainability-Driven Innovations

The aluminum cans market is undergoing significant transformation through expansions, sustainability initiatives, and acquisitions. In August 2025, Ball Corporation divested part of its Saudi Arabia joint venture, focusing resources on core global operations. Meanwhile, Crown Holdings reported strong Q2 2025 results with rising beverage and food can demand in North America and Europe, reflecting resilient consumption patterns.

In June 2025, CANPACK committed over $110 million to expand its Polish facility, boosting output by approximately one billion cans annually to serve European beverage companies. Earlier, in May 2025, Ball Corporation received four EMBANEWS Awards for sustainable packaging innovation, emphasizing its leadership in eco-friendly materials. Similarly, in March 2025, Toyo Seikan began producing Japan’s lightest aluminum can body, reducing raw material use and lowering carbon impact.

Partnership strategies also play a critical role. In February 2025, Core Cans partnered with Can-One USA, enabling large-scale aluminum can shipments from a new Nashua facility. Consolidation continues as well, with Ball Corporation acquiring Alucan in November 2024 to expand into aluminum aerosols and bottles. Complementing these moves, Toyo Seikan launched its EcoEnd™ in July 2024, cutting lid-related emissions by 40%, highlighting the importance of next-generation design.

Emerging Trends and Growth Opportunities in the Aluminum Cans Market

Accelerated Adoption of Lightweighting and Advanced Alloys to Mitigate Cost and Supply Volatility

One of the most defining trends in the aluminum cans market is the rapid push toward lightweighting and advanced alloy development. With aluminum prices subject to global market volatility and supply chain disruptions, manufacturers are innovating to reduce the amount of metal used per unit while maintaining durability and performance. Leading companies are achieving material reductions of up to 12–15% per can, which translates into significant cost savings and enhanced transportation efficiency. Beyond cost considerations, these strategies directly contribute to sustainability goals by lowering carbon emissions associated with raw material extraction and processing. In June 2025, Novelis and DRT Holdings unveiled a “uni-alloy” beverage can end initiative, designed to enable up to 99% recycled content while cutting the carbon footprint by more than 50%. This innovation also ensures compatibility with high-speed filling operations that can exceed 2,000 cans per minute, addressing operational efficiency while supporting the industry’s broader sustainability transformation.

Strategic Backward Integration and Investment in Closed-Loop Recycling Systems

Aluminum can producers are moving aggressively into backward integration and closed-loop recycling systems to secure reliable, high-quality recycled content. Recycling aluminum consumes 95% less energy than producing virgin aluminum, making it a cornerstone of industry decarbonization. Novelis, part of the Aditya Birla Group, recycles more than 82 billion cans annually and aims to push its products to 75% recycled content by 2030. Parallel to this, Ball Corporation has launched its “Toward a Perfect Circle” vision, which focuses on circularity through infrastructure investment and collaboration with recycling technology partners like TOMRA. Sustainability certifications are becoming central to market credibility, with Crown Holdings and Ball’s beverage division both achieving Aluminum Stewardship Initiative (ASI) certifications in 2025. These moves strengthen the value chain’s resilience, demonstrate alignment with global ESG standards, and enhance consumer confidence in the recyclability of aluminum cans.

Expansion into New Beverage Categories Beyond Traditional Soft Drinks and Beer

A critical opportunity for aluminum can manufacturers lies in diversifying beyond legacy segments such as beer and carbonated soft drinks. The format’s durability, portability, and eco-friendly credentials are driving its adoption in wine, spirits, ready-to-drink (RTD) cocktails, and functional beverages. In 2024, canned RTD cocktails dominated the segment with a 78.3% revenue share, reflecting consumer preference for convenience and premium branding opportunities. Cans also offer technical advantages for wine producers by protecting against light and oxygen exposure, which preserves quality. The single-serve format further reduces waste and appeals to younger demographics seeking sustainable and stylish packaging. Additionally, cans provide a unique creative platform for premium brands to use vibrant, artistic labels that stand out on shelves, helping products in emerging beverage categories capture consumer attention and market share.

Deployment of Digital Printing and Smart Can Technologies for Enhanced Engagement

The convergence of packaging and digital technology is opening a new frontier for aluminum can innovation. Digital printing enables beverage brands to rapidly design limited-edition runs, seasonal graphics, and personalized cans without the high setup costs of traditional methods. This agility supports hyper-local marketing campaigns and strengthens consumer engagement. At the same time, smart can technologies, including QR codes and NFC tags, are transforming cans into interactive media channels. By scanning a can, consumers can access exclusive brand content, loyalty programs, or product origin data. For environmentally conscious buyers, transparency features allow them to trace the can’s recycling journey, reinforcing trust in sustainability claims. This fusion of digital interactivity and eco-transparency turns the aluminum can from a static container into a dynamic marketing platform, making it a high-potential opportunity for beverage brands seeking differentiation in competitive markets.

Competitive Landscape: Leading Companies Driving the Global Aluminum Cans Market

The competitive environment in the aluminum cans industry is defined by multinational corporations that combine global production capacity, advanced technologies, and sustainability commitments to maintain leadership.

Ball Corporation: Driving Sustainable Aluminum Packaging Expansion

Ball Corporation remains a leader in beverage and aerosol packaging. Following its Alucan acquisition in November 2024, the company expanded into sustainable aluminum bottle and aerosol technologies. In August 2025, Ball optimized its portfolio by selling part of its Saudi Arabia joint venture. Its strategy centers on sustainability, digital transformation, and renewable energy adoption, aiming to achieve ambitious 2030 circular economy goals while exploring new markets for aluminum cups and smart packaging.

Crown Holdings, Inc.: Strengthening Beverage Can Leadership in North America and Europe

Crown Holdings is a key global supplier of aluminum beverage, food, and aerosol cans. In July 2025, it reported robust financial growth, including a 6% sales increase in its Americas beverage segment, supported by strong demand. Earlier, in 2024, Crown expanded European capacity with a new two-line plant in Peterborough, UK, strengthening its regional presence. Crown’s diverse product range and global manufacturing footprint make it a reliable partner for consumer goods companies worldwide.

Ardagh Group S.A.: Investing in Low-Carbon Aluminum Can Solutions

Ardagh Group, through its Ardagh Metal Packaging (AMP) division, is a top producer of aluminum beverage cans for major brands. Its sustainability strategy was showcased at BrauBeviale in November 2024, emphasizing low-carbon materials and renewable energy integration. With significant investments in Virtual Power Purchase Agreements (VPPAs), Ardagh is reducing emissions while delivering high-performance cans to breweries, soft drink manufacturers, and energy drink brands globally.

CANPACK S.A.: Expanding Capacity and Sustainability Commitments

CANPACK has built a strong position as a global producer of aluminum cans, glass bottles, and flexible packaging. In June 2025, it invested over $110 million in Poland to expand production by one billion cans per year. CANPACK’s 2024 Sustainability Report highlighted achievements such as 100% renewable electricity across plants and higher recycled content in cans. With 27 production facilities in 16 countries, serving customers in 100 markets, CANPACK is a global growth leader with strong sustainability credentials.

Envases Group: Diversifying into Premium Aluminum Bottles and Specialty Cans

Envases Group is a global aluminum packaging specialist with a focus on beverage cans and premium aluminum bottles for cosmetics, spirits, and specialty beverages. Its 2024 Sustainability Report detailed climate action progress and alignment with EU sustainability directives. Recent expansion includes a new Texas facility to boost North American capacity. Envases’ ability to deliver customized, high-finish aluminum packaging makes it a key supplier in niche premium markets.

Aluminum Cans Market Share Insights

Beverage Cans Dominate Aluminum Cans Market Share by Product Type

Beverage cans account for nearly 80% of the aluminum cans market in 2025, cementing their position as the undisputed leader. Their dominance is powered by the global consumption of carbonated soft drinks, beer, energy drinks, and the rising popularity of canned wine and ready-to-drink (RTD) cocktails. Aluminum cans provide exceptional barrier properties, ensuring carbonation and flavor retention, while also being lightweight and infinitely recyclable—attributes that align perfectly with sustainability-driven consumer and regulatory preferences. Aerosol cans form a high-value niche, sustained by innovation in bag-on-valve (BOV) systems, particularly in personal care and household products. Food cans, though limited compared to steel alternatives, retain strategic importance for premium and non-reactive packaging applications such as seafood and specialty foods. Smaller shares are held by emerging “other applications” including pharmaceuticals and industrial uses, showcasing aluminum’s versatility in niche sectors. Beverage cans’ overwhelming market share demonstrates how sustainability, performance, and evolving consumer lifestyles converge to make them the primary growth driver in the aluminum can industry.

Food & Beverages Lead Aluminum Cans Market Share by End-Use Industry

The food & beverages sector represents 88% of the aluminum cans market, underscoring the category’s absolute dominance. Within this segment, beverage packaging accounts for the vast majority, with aluminum cans serving as the global standard for brewers, soda manufacturers, and emerging RTD beverage players. Their recyclability and consumer appeal as a sustainable alternative to plastic bottles make them indispensable. The food portion, though smaller, includes applications in pet food, coffee, and nutritional supplements, where premium positioning benefits from aluminum’s protective and branding advantages. Cosmetics & personal care follow as the fastest-growing end-use, driven by aerosol packaging for dry shampoos, hairsprays, and skincare mousses, where aluminum’s premium image and shatterproof safety are key. Pharmaceuticals and healthcare rely on aluminum in highly regulated niches such as inhalers and medical sprays, while chemicals and industrial uses (e.g., lubricants, paints) represent stable, specialized demand. The dominance of beverages highlights aluminum’s central role in mass-market consumption, while growth in cosmetics underscores its evolution into premium lifestyle categories.

United States: Sustainability and Lightweight Aluminum Cans Drive Market Expansion

The U.S. aluminum cans market is experiencing strong growth driven by evolving consumer preferences for sustainable, convenient, and single-serve packaging, particularly in the beverage sector. The trend toward eco-friendly packaging is highlighted by the Can Manufacturers Institute (CMI), which reports that the average aluminum can contains 71% recycled content and can be recycled into a new can in under 60 days.

Technological advancements are reshaping the market, with companies like Crown Holdings leading the push for ultra-lightweight can designs, reducing material usage by 10% while maintaining structural integrity. Investments in recycling infrastructure aim to increase recovery rates to 70% by 2030 and 90% by 2050, ensuring long-term feedstock security. Additionally, regulatory developments, such as the removal of fill-size barriers by the U.S. Alcohol and Tobacco Tax and Trade Bureau in 2025, are expanding aluminum can usage in the premium wine and spirits market, creating significant growth opportunities.

Germany: Circular Economy and High-Recycling Rates Fuel Market Leadership

Germany’s aluminum cans market is heavily influenced by its stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), which promotes eco-friendly and fully recyclable packaging. The country boasts one of the highest aluminum can recycling rates in Europe at 99%, driven by robust deposit return systems and strong consumer participation.

Technological innovations are supporting sustainability, with European smelters such as Constellium and Novelis harmonizing alloy specifications to allow cans with up to 100% recycled content, thereby significantly reducing carbon emissions. The implementation of governmental mandates under the PPWR, including waste reduction targets and recyclability improvements, further strengthens Germany’s position as a leading hub for environmentally responsible aluminum can production.

China: Industrial Growth and Government Initiatives Accelerate Aluminum Can Demand

China’s aluminum cans market is benefiting from rapid industrialization and expansion in the beverage and e-commerce sectors, creating high demand for durable and reliable packaging solutions. The government’s 2025–2027 Action Plan focuses on resource security, green development, and technological innovation, with targets including 15 million tonnes of recycled aluminum output and stricter energy efficiency and environmental standards.

Technological advancements such as AI-driven automation and 5G-integrated industrial internet optimize production efficiency and flexible manufacturing. Sustainability is a central driver, with the dual carbon goals of carbon peak and carbon neutrality aligning the industry with national carbon trading programs by 2025. Companies are increasingly monetizing sustainability performance by purchasing carbon credits, reflecting a strong integration of eco-conscious practices in aluminum can production.

India: Rising Beverage Consumption and Recycling Infrastructure Boost Market

India’s aluminum cans market is propelled by the rapid expansion of the food and beverage sectors, driven by rising disposable incomes, urbanization, and a growing preference for ready-to-drink (RTD) beverages among younger consumers. Strategic investments, such as Ball Corporation’s expansion of aluminum can facilities, are enhancing production capacity to meet rising demand.

Sustainability initiatives are a key driver, with the Plastic Waste Management (Amendment) Rules encouraging the shift from single-use plastics to reusable and recyclable alternatives. India maintains a high aluminum can recycling rate of approximately 85%, demonstrating effective infrastructure and strong public awareness, positioning the country as a rapidly growing and environmentally responsible aluminum can market.

Brazil: Record Recycling Rates and Strategic Investments Strengthen Market

Brazil’s aluminum cans industry is shaped by stringent legislation restricting single-use plastics under the National Solid Waste Policy, driving the adoption of durable, reusable packaging. Technological advancements, including robotics and AI-driven quality control, are enabling sophisticated production processes, from automated sorting to defect detection, enhancing efficiency and accuracy.

Sustainability is a hallmark of the Brazilian market, with the country achieving the highest aluminum can recycling rate globally at 97.3%, according to the Brazilian Aluminium Manufacturers Association. Significant strategic investments, such as Canpack Group’s new facility in Minas Gerais with a 1.3 billion can annual capacity, are set to commence operations by 2024, reflecting continued market growth and innovation in high-quality aluminum can production.

Japan: Advanced Recycling and Lightweighting Innovations Propel Market

Japan’s aluminum cans market is anchored by advanced recycling systems and regulatory support, including the Plastic Resource Circulation Act, which underpins circular production practices. The industry is increasingly incorporating bio-based materials, such as Spiber’s Brewed Protein™, into packaging solutions, enhancing sustainability credentials.

Innovation in functionality is driving market differentiation, with companies like Suntory pioneering ultra-lightweight aluminum cans to minimize resource use while maintaining usability. These developments, combined with Japan’s strong focus on sustainable materials and advanced recycling practices, position the country as a global leader in environmentally friendly and technologically advanced aluminum can production.

Aluminum Cans Market Report Scope

Aluminum Cans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$57.4 Billion

|

|

Market Size (2034)

|

$93.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Food Cans, Beverage Cans, Aerosol Cans, Other Applications), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Chemicals, Other Industries), By Can Type (Two-piece Cans, Three-piece Cans)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., CANPACK Group, Silgan Holdings Inc., Toyo Seikan Group Holdings Ltd., Novelis Inc., Trivium Packaging, CPMC Holdings Ltd., Hindustan Tin Works Ltd., Massilly Group, Exal Corporation, Sonoco Products Company, Showa Aluminum Can Corporation, Kian Joo Can Factory Berhad

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aluminum Cans Market Segmentation

By Product Type

- Food Cans

- Beverage Cans

- Aerosol Cans

- Other Applications

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Chemicals

- Other Industries

By Can Type

- Two-piece Cans

- Three-piece Cans

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aluminum Cans Market

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- CANPACK Group

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings Ltd.

- Novelis Inc.

- Trivium Packaging

- CPMC Holdings Ltd.

- Hindustan Tin Works Ltd.

- Massilly Group

- Exal Corporation

- Sonoco Products Company

- Showa Aluminum Can Corporation

- Kian Joo Can Factory Berhad

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global aluminum cans market, capturing breakthroughs in sustainability, lightweighting innovations, advanced alloy development, and digital engagement technologies. The analysis reviews evolving packaging preferences driven by rising demand for premium beverages, RTD cocktails, and functional drinks, alongside efficiency improvements in two-piece can manufacturing and closed-loop recycling systems. It highlights key growth drivers, including regulatory support for circular economy practices, eco-conscious consumer behavior, and strategic expansions by leading players such as Ball Corporation, Crown Holdings, and CANPACK. This report is an essential resource for industry professionals, investors, and manufacturers seeking actionable insights on market dynamics, competitive strategies, regional developments, and technological advancements. By integrating historical data, recent developments, and long-term forecasts, the report offers a comprehensive perspective on product types, end-use industries, and can technologies, enabling stakeholders to identify growth opportunities, optimize supply chains, and leverage sustainability and innovation as competitive advantages.

Scope Highlights:

- Segmentation: By Product Type (Food Cans, Beverage Cans, Aerosol Cans, Other Applications), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Chemicals, Other Industries), By Can Type (Two-piece Cans, Three-piece Cans)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies, including Ball Corporation, Crown Holdings, Ardagh Group, CANPACK, Silgan Holdings, Toyo Seikan, and Novelis

Methodology

USDAnalytics employed a rigorous research methodology combining primary interviews, secondary data, and quantitative modeling to provide a precise and actionable overview of the aluminum cans market. Primary research involved consultations with manufacturers, distributors, beverage companies, and sustainability experts to understand trends in lightweighting, recycling, alloy innovation, and market adoption of premium and craft beverages. Secondary research included corporate filings, regulatory frameworks, patent databases, and trade publications to validate market size, competitive positioning, and technological innovations. Market sizing and forecasting were conducted using historical trends, consumption patterns, and projected growth drivers across product types, end-use industries, and regional markets. Qualitative analysis focused on digital printing, smart can technologies, and circular economy initiatives, while quantitative assessment addressed production capacities, market shares, and financial performance of key players. The methodology ensures robust insights for strategic decision-making and investment planning in a rapidly evolving, sustainability-driven aluminum cans market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.