Market Overview: Food Cans Market to Reach $33.8 Billion by 2034 at 3.6% CAGR

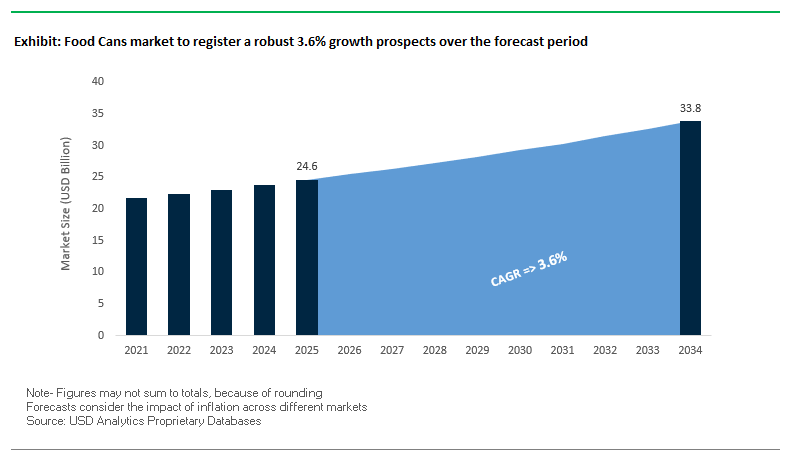

The global food cans market is projected to expand from $24.6 billion in 2025 to $33.8 billion by 2034, registering a steady CAGR of 3.6%. Food cans remain one of the most reliable packaging formats due to their superior barrier properties, extended shelf life, and unique recyclability advantages. For industry professionals and buyers, critical questions include: How will sustainability and recycling commitments reshape procurement strategies? What role will lightweighting and advanced coatings play in reducing costs? And how will cans maintain their competitive edge against flexible and paper-based packaging alternatives?

Key Insights for stakeholders:

- High Recyclability Advantage: Both steel and aluminum cans can be infinitely recycled. Aluminum food cans contain on average 71% recycled content, while steel cans achieve a 58% recycling rate in the U.S.

- Food Waste Reduction Role: Shelf life of canned foods exceeds 40 years in some cases, eliminating cold-chain dependency and reducing food loss.

- Lightweighting Efficiency: Modern steel cans are 40% lighter than three decades ago, lowering raw material use and cutting logistics emissions.

- Nutrient Preservation: The retort sterilization process maintains food safety and nutrient levels without artificial preservatives, supporting consumer trust in canned goods.

Market Analysis: Recent Developments in the Global Food Cans Industry

The food cans industry is evolving under competitive pressures from flexible packaging while sustaining relevance through innovation, capacity expansion, and product diversification.

In August 2025, Amcor reported strong fiscal Q4 2025 results, projecting further growth in fiscal 2026. Although not a direct food can manufacturer, its flexible packaging solutions compete strongly with cans, highlighting cross-material pressures. In July 2025, two significant M&A activities reshaped the packaging landscape: Smurfit Kappa and WestRock finalized their merger, forming Smurfit WestRock, a sustainability-driven global giant, while International Paper completed a $9.9 billion acquisition of DS Smith, strengthening fiber-based packaging competition against cans.

On the product front, canned food launches remain robust. In March 2025, The Bull Brand introduced three new canned mince meals Bolognaise Mince, Chilli Mince, and Savoury Mince catering to the convenience segment. Around the same time, Conagra Brands invested in its Dresden, Ontario facility, adding a dedicated production line for its Ro-Tel canned tomato brand, reinforcing confidence in long-term canned food demand.

Further developments underscore category diversification. Bisto launched a new gravy in February 2025, likely sold in cans or jars, demonstrating the packaging’s relevance in sauces. In December 2024, Oman’s state-backed Simak launched its canned tuna line with over 100 million annual can capacity, strengthening its domestic and export presence. Meanwhile, Mondi’s January 2025 win of 10 WorldStar Awards in flexible packaging highlights the innovative momentum of can alternatives.

Trends and Opportunities Reshaping the Food Cans Market

Regulatory Scrutiny and Material Substitution Away from BPA and Beyond

The food cans market is experiencing a seismic shift as regulatory bodies across the globe impose strict limits on bisphenol-A (BPA) and other synthetic compounds used in food-contact linings. The European Union took the lead in January 2025, implementing a ban on BPA in food packaging following the European Food Safety Authority’s 2023 reassessment, which reduced the acceptable daily intake of BPA by a staggering 20,000-fold. With a transition period lasting until July 2026, manufacturers are under immense pressure to redesign lining technologies at scale.

Corporates are already realigning to comply with these mandates. For example, a leading global canning company disclosed in its 2025 sustainability report that it is phasing out BPA linings and expects the majority of its products to feature alternative coatings by the end of the year. This transition has catalyzed rapid investment into polyester-based, acrylic, and oleoresinous non-epoxy coatings, all of which aim to replicate the protective performance of legacy epoxy systems. The urgency is not driven by consumer preference alone but by compliance requirements and reputational risk, making material substitution a central pillar of competitive strategy in the global food cans market.

Lightweighting and Supply Chain Optimization Through Advanced Manufacturing

Another defining trend is the industry-wide focus on lightweighting as manufacturers attempt to balance rising costs of steel, aluminum, and energy with sustainability goals. According to the Can Manufacturers Institute, steel food cans have been made 40% lighter over the past three decades through continuous engineering innovations. This not only lowers raw material usage but also reduces carbon emissions across logistics by requiring less fuel for transport.

The adoption of recycled feedstock further compounds these benefits. Data shows that producing a can from recycled steel consumes 75% less energy compared to virgin steel, which makes recycling and lightweighting complementary levers of efficiency. In 2024, Toyo Seikan announced the launch of Japan’s lightest aluminum DI (double-integrated) can, achieved with its proprietary Compression Bottom Reform (CBR) technology. This development shaved 2 grams per can from its 350ml and 500ml formats, cutting greenhouse gas emissions by around 9% per unit. These engineering breakthroughs demonstrate how precision manufacturing not only improves performance but also delivers measurable environmental and financial returns across the food cans supply chain.

Development and Scaling of Bio-Based and Polymer-Free Can Linings

The global regulatory clampdown on synthetic chemicals is creating a high-value opportunity for the development of bio-based and polymer-free linings that provide effective corrosion resistance while ensuring full compliance with food-contact safety standards. Early pilot programs indicate significant momentum. For instance, a major packaging solutions provider recently announced a collaboration with a bio-materials startup to engineer a plant-based lining derived from agricultural by-products. Designed to provide robust shelf-life protection, this innovation underscores the potential for scaling natural alternatives to synthetic coatings.

Academic research further supports this trajectory. Studies highlight the promise of combining natural fibers with bio-based adhesives to achieve barrier properties comparable to epoxy-based linings. Additionally, research into ceramic-based inert coatings is opening new avenues for creating polymer-free alternatives with zero risk of migration into food. Companies that succeed in scaling these solutions will establish a first-mover advantage in the premium, sustainability-driven food packaging segment, which is increasingly valued by both regulators and environmentally conscious consumers.

Integration of Digital Technologies for Enhanced Traceability and Consumer Engagement

The digitalization of food cans is an emerging frontier where packaging becomes an active data interface rather than a passive container. The conductive properties of metal make it a natural platform for embedding digital watermarks, QR codes, RFID, and even NFC chips. This transformation supports multiple value drivers supply chain transparency, anti-counterfeiting, and consumer engagement.

Recent trials highlight how smart packaging can enable real-time traceability, allowing stakeholders to track a can’s journey across the supply chain and monitor conditions such as temperature or storage. Brands are leveraging unique QR codes to combat counterfeiting while simultaneously offering consumers interactive experiences such as sustainability information, product provenance, and recycling instructions. A 2025 logistics case study demonstrated how these technologies provide end-to-end visibility and reduce inefficiencies in distribution. As digital packaging ecosystems expand, food cans are uniquely positioned to become a bridge between brands and consumers, aligning with global sustainability targets while driving customer trust and loyalty.

Competitive Landscape: Global Leaders in the Food Cans Market

The food cans industry is led by multinational corporations with strong capabilities in metal packaging, coatings technology, and global manufacturing networks. Their focus is on lightweighting, recyclability, and customer-specific innovations to sustain growth.

Ball Corporation Championing Infinitely Recyclable Aluminum Solutions

Ball Corporation is a global leader in aluminum packaging, including food cans, aerosols, and specialty metal containers. Its innovation strategy revolves around lightweighting technologies and reinforcing aluminum’s “infinitely recyclable” positioning. With a strong global manufacturing presence across the Americas, Europe, and Asia, Ball supports food and beverage companies with sustainable, cost-effective solutions.

Crown Holdings, Inc. Innovating BPA-Free Coatings and Shaped Can Formats

Crown Holdings offers a wide range of steel and aluminum food cans, with expertise in internal coatings and tamper-evidence technologies. The company is recognized for pioneering BPA-free protective coatings and continuously advancing lightweight can-making technologies. Its portfolio includes traditional round cans as well as modern, rectangular and specialty-shaped containers that enhance shelf appeal and product differentiation.

Ardagh Group S.A. Expanding Global Footprint in Food and Beverage Packaging

Ardagh Group specializes in both glass and metal packaging, with food cans being a core business within its steel and aluminum divisions. The company operates across Europe, North America, and South America, investing in upgraded production lines to improve efficiency and product quality. Its strategy emphasizes sustainable partnerships with major food brands, providing easy-open ends and convenience features that align with consumer expectations.

Can-Pack S.A. Driving Regional Growth with Lithographic Printing Excellence

Can-Pack, headquartered in Poland, is a prominent producer of aluminum and steel food cans with a strong presence in Europe, the Middle East, and Africa. The company invests heavily in capacity expansion and sustainability, offering lightweight, recyclable cans. Known for its high-quality lithographic printing, Can-Pack enables brands to stand out with vibrant, customized designs, supporting differentiation in competitive food categories.

Silgan Holdings Inc. Specializing in Easy-Open and Peel-Off Can Innovations

Silgan Holdings is a major U.S.-based manufacturer of rigid packaging, with a strong portfolio in steel and aluminum food containers. Its key innovations include easy-open and peel-off can ends, enhancing consumer convenience and safety. Silgan has expanded through acquisitions to broaden its customer base and deepen expertise in food cans. Its products serve diverse categories such as fruits, vegetables, seafood, sauces, and pet food, making it a versatile leader in the segment.

Food Cans Market Share Insights

Two-Piece Cans Dominate Market Share by Can Type in Food Cans

In 2025, two-piece cans capture 70% of the food cans market, establishing themselves as the efficiency standard due to lightweight construction, material savings, and seamless integrity that reduces leakage risk. Their widespread adoption in fruits, vegetables, and ready-to-drink beverages is reinforced by lower production costs and compatibility with high-speed manufacturing lines. Two-piece cans also excel in withstanding carbonation and high-pressure processing, securing dominance in beverage and processed food packaging. Three-piece cans maintain a strong minority share, holding relevance in high-temperature retort applications such as pet food, soups, and dense proteins where their strength and ability to withstand extreme heat and pressure remain unmatched. Their steel composition provides durability for heavy or bulky products, ensuring continued reliance in specific categories despite broader industry migration toward two-piece formats. This segmentation illustrates how two-piece cans lead on efficiency and scalability, while three-piece cans retain strength-driven niches.

Fruits and Vegetables Lead Market Share by Application in Food Cans

By application, fruits and vegetables account for 30% of the food cans market in 2025, securing their leadership as pantry staples globally. Consumers value affordability, shelf life, and year-round availability, while canning ensures nutritional retention and food security. Pet food at 25% emerges as the high-value growth engine, with 3-piece retort cans providing durability, sterility, and premium perception for wet pet food, aligning with the premiumization trend in pet care. Meat, poultry, and seafood remain critical users, leveraging cans’ hermetic seals to prevent spoilage in protein-rich foods. Soups, sauces, and dressings form a stable demand base, though flexible pouches and tubs are encroaching in convenience segments. Ready meals, once a significant category, are now a declining niche as microwavable trays and pouches offer easier preparation and disposal. End-use share distribution highlights how cans sustain dominance in core pantry items and pet food while facing competitive pressure in ready meals and single-serve formats.

United States: Advancing BPA-Free, Sustainable, and E-Commerce-Ready Food Cans

The U.S. food cans market is being driven by a strong focus on sustainability and recycling, with initiatives from the Aluminum Association and Can Manufacturers Institute promoting the nearly infinite recyclability of aluminum and steel cans. Consumer demand for safer packaging has accelerated the adoption of BPA-free linings and coatings, addressing health concerns associated with Bisphenol A while enhancing product safety. The rapid growth of e-commerce and direct-to-consumer (DTC) channels is prompting manufacturers to design lightweight, durable cans capable of withstanding shipping stress and maintaining product integrity. Additionally, the U.S. market leads in ready-to-eat and convenience foods, with canned products preferred for their long shelf life and ease of preparation, creating robust demand for innovative packaging solutions.

Germany: Leading Circular Economy Practices and High-Quality Metal Can Production

Germany’s food cans market is defined by stringent regulations emphasizing food safety and quality, aligning with both national and EU standards. The market is at the forefront of Europe’s circular economy, driving initiatives for high recycling rates and using recycled materials in metal can production. Companies are investing in advanced manufacturing processes to produce lightweight, durable, and recyclable cans. Furthermore, there is increasing demand for cans catering to new applications, such as organic and health-conscious foods, reflecting shifting consumer preferences and regulatory support for sustainable production.

China: Regulatory Compliance and Expansive Production Capacity Fuel Market Growth

China’s food cans industry is guided by comprehensive regulations on food contact materials, ensuring product safety and compliance. The country holds a dominant position in global production and exports of metal cans, supported by its extensive manufacturing infrastructure. Rising domestic demand, fueled by growth in processed and ready-to-eat foods, is a key driver as urbanization increases the need for convenient, safe, and attractively packaged food products. This combination of regulatory compliance, massive production capacity, and strong domestic consumption is propelling China’s food cans market forward.

India: Domestic Manufacturing Growth and Expanding Modern Retail Channels

India’s food cans market is experiencing rapid growth under the government’s “Make in India” initiative and liberal FDI policies in the food processing sector, attracting global players and boosting local manufacturing. Expansion of the food processing industry, supported by infrastructure development from the Ministry of Food Processing Industries (MoFPI), provides a solid foundation for innovation in food cans. The market is also shaped by the growth of modern retail and e-commerce platforms, driving demand for lightweight, durable packaging solutions capable of protecting products during shipping and handling.

Brazil: Sustainable Supply Chains and Innovation Driving Market Demand

Brazil’s food cans industry is increasingly focused on sustainability, with new platforms tracking supply chain environmental and social metrics to improve sourcing practices. The rapid growth of e-commerce is driving demand for convenient, protective packaging solutions, with a focus on flexible and lightweight designs that reduce material use and shipping costs. Innovation in new applications, such as plant-based yogurt products, is encouraging investment in metal can technology to support product development and expand market use.

Japan: Premium Quality, Barrier Innovation, and Disaster-Preparedness Applications

The Japanese food cans market emphasizes high-quality production, safety, and functional innovation. Companies are at the forefront of developing advanced barrier coatings and linings to extend shelf life and ensure food safety. Japan’s unique focus on disaster preparedness also influences market demand, with shelf-stable canned products prioritized to guarantee food availability during emergencies. The combination of premium product standards, cutting-edge barrier technology, and emergency food applications positions Japan as a highly specialized and innovative market within the global food cans industry.

Food Cans Market Report Scope

Food Cans market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.6 Billion

|

|

Market Size (2034)

|

$33.8 Billion

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Material Type (Aluminum Cans, Steel Cans), By Can Type (2-Piece Cans, 3-Piece Cans), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Ready Meals, Pet Food, Soups, Sauces & Dressings, Other Applications), By Closure Type (Easy-Open Ends, Standard Ends)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings Inc., Ardagh Group S.A., CANPACK S.A., Silgan Holdings Inc., Toyo Seikan Group Holdings Ltd., Daiwa Can Company, CPM Acquisition Corp. (part of the CANPACK Group), Shandong Bohui Paper Group Co., Ltd., Massilly Group, Colep Packaging, Envases Group, Rexam PLC (part of Ball Corporation), Exal Group (part of the CANPACK Group), Kian Joo Can Factory Berhad

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Cans Market Segmentation

By Material Type

By Can Type

- 2-Piece Cans

- 3-Piece Cans

By Application

- Fruits & Vegetables

- Meat

- Poultry & Seafood

- Ready Meals

- Pet Food

- Soups

- Sauces & Dressings

- Other Applications

By Closure Type

- Easy-Open Ends

- Standard Ends

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Cans Market

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group S.A.

- CANPACK S.A.

- Silgan Holdings Inc.

- Toyo Seikan Group Holdings Ltd.

- Daiwa Can Company

- CPM Acquisition Corp. (part of the CANPACK Group)

- Shandong Bohui Paper Group Co., Ltd.

- Massilly Group

- Colep Packaging

- Envases Group

- Rexam PLC (part of Ball Corporation)

- Exal Group (part of the CANPACK Group)

- Kian Joo Can Factory Berhad

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global Food Cans Market, examining the evolving dynamics of aluminum and steel can production, advanced coating technologies, and sustainable packaging trends. The analysis reviews breakthrough developments in BPA-free linings, lightweighting innovations, and bio-based coatings, while highlighting competitive strategies from leading global players. The report highlights opportunities in digital traceability, e-commerce-ready solutions, and circular economy practices, providing critical insights into product diversification, capacity expansion, and regulatory compliance. This report is an essential resource for manufacturers, packaging suppliers, investors, and product developers seeking actionable intelligence on market growth, emerging applications, and sustainability-driven innovations, bridging historical performance data (2021–2024) with forward-looking projections (2025–2034) to guide strategic decision-making.

Scope Highlights

- Segmentation: By Material Type (Aluminum Cans, Steel Cans), By Can Type (2-Piece Cans, 3-Piece Cans), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Ready Meals, Pet Food, Soups, Sauces & Dressings, Other Applications), By Closure Type (Easy-Open Ends, Standard Ends)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis/profiles of 15+ leading companies including Ball Corporation, Crown Holdings, Ardagh Group, CANPACK, Silgan Holdings, Toyo Seikan, and others.

Methodology

USDAnalytics employs a robust research methodology combining primary and secondary sources to ensure comprehensive market coverage and reliable forecasts. Primary research involved detailed interviews with packaging manufacturers, coating specialists, food brand stakeholders, and industry consultants to capture firsthand insights on innovation, regulatory compliance, and sustainability strategies. Secondary research included in-depth review of company reports, financial statements, trade publications, patent filings, and global databases to validate trends and benchmark performance. Market sizing and forecasting were conducted using bottom-up and top-down approaches, integrating historical consumption data, production capacity, and application-specific adoption rates. Triangulation of data, scenario modeling, and competitive benchmarking were applied to ensure accuracy and deliver actionable insights into the Food Cans Market for the 2025–2034 forecast period.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.