Market Overview: Global Metal Cans Industry Insights and Growth Outlook

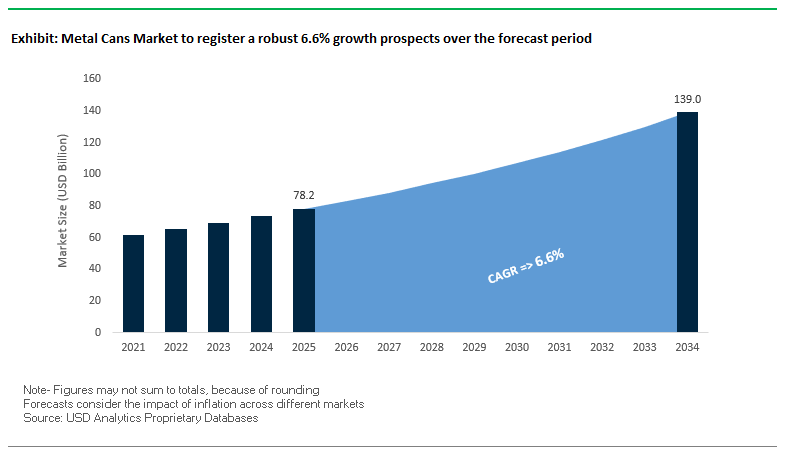

The global metal cans market is projected to reach $78.2 billion in 2025 and expand to $139 billion by 2034, registering a strong CAGR of 6.6%. Metal cans remain a cornerstone of the global packaging industry, valued for their infinite recyclability, superior barrier properties, and ability to preserve food and beverages without preservatives. Industry professionals recognize metal cans as not only a packaging solution but also a critical enabler of sustainability, product safety, and consumer trust. For brands, the choice of metal packaging is increasingly driven by circular economy principles and the demand for high-quality, eco-friendly solutions.

The industry is being reshaped by four major forces: the recyclability advantage of aluminum and steel, the dominance of beverages as the largest end-use sector, the continued role of cans in food preservation, and the shift towards lightweighting and advanced digital printing. These trends collectively highlight why metal cans remain indispensable for both global and regional packaging ecosystems.

Key Insights for Industry Professionals:

- Infinite recyclability: Aluminum and steel cans can be recycled indefinitely without quality loss, making them the most sustainable packaging formats.

- Beverage dominance: Rising consumption of craft beer, carbonated soft drinks, and energy drinks drives a large portion of market demand.

- Food preservation leader: Metal cans extend shelf life naturally, avoiding artificial preservatives, which is vital in global food supply chains.

- Lightweighting and smart design: Advanced manufacturing enables ultra-light cans and premium digital printing, meeting both sustainability and marketing goals.

Market Analysis: Recent Developments Shaping the Global Metal Cans Industry

The metal cans market has seen significant restructuring, expansion, and sustainability-focused initiatives between 2024 and 2025, reflecting a sector in transition. In August 2025, Ball Corporation divested part of its joint venture stake in Saudi Arabia to sharpen its focus on core businesses, while Crown Holdings received SBTi validation for its net-zero targets, reinforcing its decarbonization leadership. That same month, Crown also reported a strong 19% rise in earnings per share, showcasing the profitability of its Americas beverage division.

In July 2025, the Ardagh Group announced a recapitalization deal involving a debt-for-equity swap of over $4 billion, a major move to deleverage its balance sheet. Silgan Holdings, also in July, reported steady second-quarter results and continued its shareholder-focused approach with consistent dividend increases. Additionally, Crown Holdings revealed expansion plans in Brazil (May 2025) with a high-speed beverage can line at its Ponta Grossa plant, targeting demand growth in Latin America.

Sustainability remains a central narrative across players. Trivium Packaging in April 2025 reported a 2% reduction in Scope 1 and 2 emissions in its 2024 Sustainability Report, underlining progress toward its net-zero 2050 pledge. Earlier, in January 2025, CPMC Holdings exited the Hong Kong Stock Exchange after being acquired by Huarui Fengquan Development, a consolidation move in the Chinese market. Going further back, in May 2024, Sonoco Products Company announced its plan to acquire Eviosys, signaling deeper competition across food and aerosol packaging categories.

Key Trends and Strategic Opportunities Shaping the Metal Cans Market

Accelerated Investment in High-Speed, Small-Batch Digital Printing Capabilities

The metal cans market is undergoing a major transformation as brand owners prioritize limited-edition runs, seasonal designs, and hyper-personalized packaging campaigns. This shift is fueling strong investments in digital printing technologies, enabling mass customization without the inefficiencies of traditional lithographic processes. Unlike lithography, which requires costly plates and weeks of setup, digital printing provides cost-effective short runs and on-demand production, making it a game changer for beverage and personal care packaging.

A leading digital printing equipment manufacturer emphasizes that the cost per unit with digital printing remains stable regardless of print volume, making it viable for runs below 100,000 units where lithography becomes uneconomical. The ability to produce cans within a single day versus the two to three weeks required for conventional methods significantly accelerates product launches. Case studies, such as Ball Corporation’s 2023 personalized can project, highlight how variable data printing and event-specific customization boost consumer engagement by transforming packaging into a direct marketing channel. This trend underscores how digital printing is no longer an experimental niche but a mainstream investment priority for canmakers worldwide.

Transition to Next-Generation, Non-BPA and Varnish-Free Linings

Global regulators are mandating the shift to BPA-free and varnish-free internal linings, pushing can manufacturers to overhaul coating technologies. The European Food Safety Authority (EFSA) has reduced the tolerable daily intake of BPA to just 0.2 nanograms/kg body weight—a level 20,000 times lower than before—leading to the EU Commission Regulation (EU) 2024/3190, which bans BPA in food contact applications. This is forcing manufacturers across Europe, North America, and Asia to accelerate the adoption of BPA non-intent (BPA-NI) coatings.

Industry leaders are taking proactive steps. AkzoNobel confirmed in mid-2025 that BPA phase-out must be completed by July 2026, while PPG launched its new BPA-NI coating, Hoba Pro 2848, in February 2025, tailored for aluminum bottles and recognized at the 2025 ADF Innovation Awards. The push extends beyond BPA to avoid “regrettable substitutions,” eliminating other chemicals of concern such as styrene and formaldehyde. By combining regulatory compliance with consumer safety assurance, next-generation linings are becoming the new standard, reshaping both food and beverage can manufacturing globally.

Development of Lightweighting and Advanced Alloys for Sustainability Goals

Sustainability remains a critical growth driver, and lightweighting innovations in can design and alloys are creating strong opportunities for manufacturers. Advances in materials science have already reduced the thickness of can bodies from 0.42mm in the 1970s to 0.254mm today, representing a 39.5% reduction. Even a 0.01mm decrease saves millions in material costs for large-scale producers.

This lightweighting trend extends to can ends, where aluminum thickness has decreased from 0.39mm to 0.24mm, and diameter reductions further minimize metal use. Simultaneously, new high-strength aluminum and advanced high-strength steels (AHSS) are being developed to maintain integrity while using less material. These alloys offer greater tensile strength and formability, enabling thinner walls without compromising performance. As brand owners set ambitious carbon reduction targets, manufacturers who lead in lightweighting and advanced alloys will gain a competitive edge in sustainable metal packaging solutions.

Integration of Smart Packaging Features for Enhanced Traceability and Consumer Engagement

The convergence of packaging and digital technology is transforming metal cans from passive containers into interactive, traceable, and consumer-centric platforms. Smart packaging innovations, such as NFC chips, QR codes, and RFID technology, are enabling unit-level traceability, regulatory compliance, and real-time consumer engagement.

Encrypted NFC chips, as highlighted by a packaging technology provider, can increase consumer engagement by 30% while offering instant authentication against counterfeiting. RFID systems improve supply chain efficiency by allowing bulk scanning without line-of-sight, addressing compliance requirements under regulations like the U.S. Drug Supply Chain Security Act (DSCSA). On the consumer side, QR codes and NFC tags are increasingly used by beverage brands to deliver nutritional information, promotional campaigns, and even augmented reality experiences, making the can itself a gateway to digital interaction. By embedding these features, manufacturers not only safeguard product authenticity but also create valuable data-driven engagement opportunities for brands.

Competitive Landscape: Key Companies in the Global Metal Cans Market

The competitive environment in the metal cans market is defined by global leaders with strong portfolios in beverage, food, and aerosol packaging. These companies are competing through sustainability commitments, new product innovation, recapitalization strategies, and regional expansions. Below are the leading players shaping the global industry.

Ball Corporation Expands Core Aluminum Packaging Focus

Ball Corporation remains a global leader in recyclable aluminum cans for beverages, home, and personal care applications. In August 2025, the company divested part of its Saudi joint venture stake to streamline operations. With a 4.1% global shipment increase in Q2 2025, Ball continues to deliver growth. Its ReAl alloy cans, featuring high recycled content and lower carbon footprints, reinforce its sustainability leadership. Ball’s 2030 goals target a 16% Scope 3 emissions reduction and 100% renewable electricity across global sites.

Crown Holdings Strengthens Net-Zero Commitments

Crown Holdings operates in 39 countries with a wide range of aluminum and steel cans. In August 2025, it secured SBTi validation for its net-zero targets, marking a milestone in sustainability. The company also reported a 9% increase in segment income in Q2 2025, supported by its strong Americas Beverage business. Its Twentyby30 program is a comprehensive sustainability initiative, addressing environmental, social, and governance dimensions while creating long-term shareholder value.

Ardagh Group Pursues Recapitalization Strategy

Ardagh Metal Packaging (AMP), part of Ardagh Group, is a major global supplier of recyclable beverage and aerosol cans. In July 2025, Ardagh announced a recapitalization deal worth over $4 billion to cut debt through a debt-for-equity swap. With strong 34% EBITDA growth in the Americas, AMP is aligning its focus on lightweighting and efficiency-driven technologies. Its diversified product portfolio ensures growth in energy drinks, sparkling water, and non-alcoholic beverages.

Silgan Holdings Builds Strength in Food and Pet Food Cans

Silgan Holdings is a leading supplier of rigid packaging, with a strong foothold in food and pet food metal containers in North America and Europe. In July 2025, Silgan reported robust Q2 results, complemented by a steady dividend increase in August 2025. The company emphasizes a dual strategy of organic growth and acquisitions, ensuring it serves both human and pet food markets effectively. Its breadth of product offerings reinforces resilience across consumer segments.

Trivium Packaging Advances Circular Economy Strategy

Trivium Packaging supplies metal food, beverage, and aerosol cans, with sustainability at the core of its growth strategy. In April 2025, it released its 2024 Sustainability Report, highlighting progress on its net-zero 2050 roadmap. Impressively, 47% of its 2024 revenue came from eco-designed products, underlining the rising customer demand for circular solutions. Trivium continues to drive innovation through lightweighting and design support services, helping brands align with sustainability and performance goals.

Metal Cans Market Share Insights

Two-Piece Cans Hold the Largest Share by Type in the Metal Cans Industry

Two-piece cans represent 78% of the global metal cans market, underscoring their position as the industry standard for both food and beverage applications. Their dominance is rooted in the drawn and wall-ironed (DWI) manufacturing process, which produces a seamless can body that reduces leakage risks, enhances pressure resistance, and cuts raw material usage. This method is particularly critical in aluminum beverage cans, which dominate soft drinks, beer, energy drinks, and increasingly, canned water and ready-to-drink cocktails. The two-piece format also plays a growing role in steel food cans, where its reduced seamwork ensures durability under retort sterilization. Continuous investments in lightweighting technology and advanced BPA-NI (bisphenol-A non-intent) coatings have further cemented its position, aligning with regulatory compliance and sustainability initiatives.

Food and Beverage Companies Drive Market Share by End-User in the Metal Cans Industry

Food and beverage companies account for 85% of metal can consumption, making them the undisputed foundation of the industry. The beverage segment primarily relies on aluminum two-piece cans due to their infinite recyclability, superior chillability, and consumer preference for convenience packaging. At the same time, food companies heavily depend on steel cans for fruits, vegetables, soups, seafood, and pet food, leveraging the can’s ability to preserve freshness and nutrients without refrigeration for extended periods. The surge in plant-based beverages, premium RTD cocktails, and canned wines has expanded beverage can usage, while food categories continue to benefit from growing demand for long-shelf-life and pantry-stable products. As major FMCG brands pursue circular economy goals, their commitment to higher post-consumer recycled (PCR) content and lightweight steel/aluminum cans further reinforces their role as the primary end-users shaping innovation and sustainability direction in the global metal cans market.

United States Metal Cans Market Strengthened by Sustainability Regulations and Lightweighting Innovations

The U.S. metal cans market is heavily influenced by strict EPA and DOT regulations, as well as state-level initiatives like California’s Extended Producer Responsibility (EPR) laws, which push manufacturers toward highly recyclable aluminum and steel solutions. Regulatory focus on sustainability and recyclability is shaping the industry, making lightweight aluminum cans and steel containers essential for compliance. The Aluminum Association highlights that aluminum beverage cans contain an average of 71% recycled content, making them one of the most eco-friendly packaging solutions.

Technological innovation in lightweighting and advanced alloys is allowing manufacturers to develop thinner-walled aluminum cans, reducing material use, shipping costs, and carbon footprints without compromising strength. Corporate initiatives further demonstrate the industry’s commitment to sustainability. For example, the Aerosol Recycling Initiative, launched by the Can Manufacturers Institute (CMI) and Household & Commercial Products Association (HCPA) with the support of 20+ companies, aims to achieve an 85% recycling rate for aerosol cans in the U.S. Meanwhile, Ball Corporation’s investment in a new aluminum end manufacturing facility in Bowling Green, Kentucky, is reinforcing supply chain resilience. Demand is particularly strong across beverage (craft beer, canned drinks) and food (soups, pet foods) segments, fueled by growth in home consumption and e-commerce-driven packaging demand.

Germany Metal Cans Market Driven by Circular Economy and Can Contouring Technologies

Germany’s metal cans market operates within the framework of the European Union’s Circular Economy Action Plan, which emphasizes recyclability and the use of high-value materials like aluminum and tinplate. This regulatory push has positioned Germany as a leader in closed-loop packaging systems, supported by one of the world’s most efficient deposit return systems that ensures high beverage can recycling rates.

German manufacturers are pioneers in can contouring technologies, creating customized and ergonomic can designs that enhance brand differentiation and consumer convenience. These innovations, coupled with the integration of recycled content, align with Germany’s strong role in the circular economy model. Demand is particularly strong in personal care and beverage applications, with aerosols and canned beverages seeing steady growth due to the country’s high per capita consumption. Germany continues to set benchmarks in sustainable packaging, advanced manufacturing, and high-quality consumer product applications within the global metal cans industry.

China Metal Cans Market Expands with Government-Led Manufacturing and Digital Printing Advances

China’s metal cans market is expanding rapidly under government-backed initiatives aimed at strengthening high-end domestic manufacturing and reducing reliance on imported packaging. In 2024, the government unveiled a plan to advance the sector, which includes fast-tracking standards for new technologies and simplifying approval processes for innovative packaging products. This has created a favorable environment for local producers and multinational FMCG companies to expand production capacity in the country.

Chinese manufacturers are increasingly investing in automation and digital printing technologies, enabling on-demand production and high-quality customization that meets the branding needs of both local and international firms. Global FMCG giants are building localized production facilities to shorten supply chains and meet the surging demand from China’s expanding consumer goods sector. Major applications include personal care, household products, and automotive care, with rising demand for disinfectants and household insecticides further boosting the need for aerosol cans. This combination of government reforms, domestic substitution, and technology-driven production is establishing China as a central hub in the global metal cans industry.

India Metal Cans Market Gains Momentum Through Make in India and Two-Piece Can Innovations

India’s metal cans market is thriving under the government’s Make in India initiative, which encourages local manufacturing and reduces dependency on imports. Favorable policies, coupled with the rapid expansion of consumer markets, are driving strong industry growth. The Indian packaging sector is embracing technological advancements, particularly in the adoption of two-piece aluminum cans that offer lightweight, safe, and consumer-friendly packaging. A notable milestone was Ball Corporation’s 2024 partnership with CavinKare to introduce retort two-piece aluminum cans for milkshakes, showcasing India’s transition toward advanced packaging solutions.

Investments in industrial parks and new production facilities are further boosting the domestic industry’s competitiveness. Applications are broadening, with strong demand from personal care products like deodorants, as well as food and beverage packaging, driven by rising disposable incomes and the expanding middle-class population. India’s market growth is fueled by a combination of technological adoption, consumer-driven demand, and supportive government initiatives, positioning it as one of the fastest-growing markets in the global metal can packaging sector.

Brazil Metal Cans Market Strengthened by Climate-Resilient Packaging and New Manufacturing Investments

The Brazilian metal cans market is shaped by regulatory oversight from Anvisa, which recently launched a national Unique Device Identifier (UDI) system impacting labeling and certification standards for aerosols. This regulatory shift is driving demand for innovative printing and labeling technologies across the packaging industry. Brazilian manufacturers are also focusing on developing cans suited to the country’s diverse climate conditions and transport challenges, with steel cans valued for rigidity and pressure resistance.

Corporate investments remain strong, with both domestic and international players expanding their footprint. For instance, Crown Holdings, Inc. announced a new beverage can plant in Rio Verde, signaling confidence in Brazil’s growing packaging sector. The market is particularly strong in personal care, chemical, and automotive sectors, with demand for repellents and insecticides surging due to recurring regional outbreaks. Brazil’s packaging industry demonstrates resilience and adaptability, leveraging technological advancements and foreign investment to expand its role in the global metal cans market.

Japan Metal Cans Market Focused on Precision Manufacturing and Bag-on-Valve Packaging Innovations

Japan’s metal cans industry is anchored in its precision manufacturing excellence, with leading companies like Toyo Seikan producing high-performance tinplate and aluminum cans that meet stringent safety and quality standards. The industry is tightly regulated by the Pharmaceuticals and Medical Devices Agency (PMDA), which enforces strict packaging safety rules. A May 2025 amendment to the Pharmaceuticals and Medical Devices Act aims to improve the stability of pharmaceutical and medical device supply chains, directly impacting the demand for high-quality aerosol and specialty cans.

The Japanese market is pivoting toward specialty and value-added packaging solutions, focusing on thin-walled, high-finish cans for cosmetics and pharmaceuticals. There is also growing adoption of Bag-on-Valve (BoV) technology, which separates the product from the propellant, extending shelf life and enabling wider applications in food, cosmetics, and pharmaceuticals. This reflects Japan’s dedication to technological innovation, functional packaging solutions, and high-value product markets, reinforcing its global reputation as a leader in advanced packaging systems.

Metal Cans Market Report Scope

Metal Cans Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$78.2 Billion

|

|

Market Size (2034)

|

$139 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Material (Aluminum, Steel & Tinplate), By Type (2-Piece Cans, 3-Piece Cans), By Application (Food & Beverage, Personal Care & Cosmetics, Pharmaceuticals & Healthcare, Automotive & Industrial, Others), By End-User (Food & Beverage Companies, Pharmaceutical Companies, Personal Care Product Manufacturers, Chemical & Industrial Product Manufacturers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Crown Holdings, Inc., Ardagh Group S.A., Trivium Packaging, Toyo Seikan Group Holdings, Ltd., Silgan Holdings Inc., Can-Pack S.A., Nampak Ltd., Sonoco Products Company, CPMC Holdings Limited, Mauser Packaging Solutions, Colep Packaging, DS Containers, Inc., Exal Corporation, Hindustan Tin Works Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Cans Market Segmentation

By Material

- Aluminum

- Steel & Tinplate

By Type

- 2-Piece Cans

- 3-Piece Cans

By Application

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceuticals & Healthcare

- Automotive & Industrial

- Others

By End-User

- Food & Beverage Companies

- Pharmaceutical Companies

- Personal Care Product Manufacturers

- Chemical & Industrial Product Manufacturers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Metal Cans Market

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- Trivium Packaging

- Toyo Seikan Group Holdings, Ltd.

- Silgan Holdings Inc.

- Can-Pack S.A.

- Nampak Ltd.

- Sonoco Products Company

- CPMC Holdings Limited

- Mauser Packaging Solutions

- Colep Packaging

- DS Containers, Inc.

- Exal Corporation

- Hindustan Tin Works Ltd.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-dimensional research methodology to analyze the global Metal Cans Market, combining both primary and secondary research to ensure accuracy and actionable insights for industry professionals. Primary research involves interviews with key executives, packaging engineers, and supply chain specialists from leading companies such as Ball Corporation, Crown Holdings, and Ardagh Group, capturing qualitative insights on technological adoption, sustainability initiatives, and market trends. Secondary research sources include company annual reports, regulatory publications, trade journals, and authoritative databases to track historical performance, investment activities, and competitive strategies. The analysis integrates regional market dynamics across the United States, Europe, China, India, Brazil, and Japan, focusing on regulatory frameworks, consumer preferences, and production innovations such as lightweighting, digital printing, and BPA-free coatings. USDAnalytics also leverages advanced modeling techniques to forecast market growth, assess the impact of strategic initiatives like the Twentyby30 program, and quantify the influence of end-user segments such as food and beverage, personal care, and pharmaceuticals. By triangulating multiple data sources and validating findings through expert consultations, USDAnalytics delivers a comprehensive, reliable, and forward-looking perspective on the metal cans market that enables stakeholders to make informed decisions on investments, technology adoption, and sustainability strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.