Sustainability and Smart Packaging Propel the Beverage Packaging Market to USD 294.9 Billion by 2034

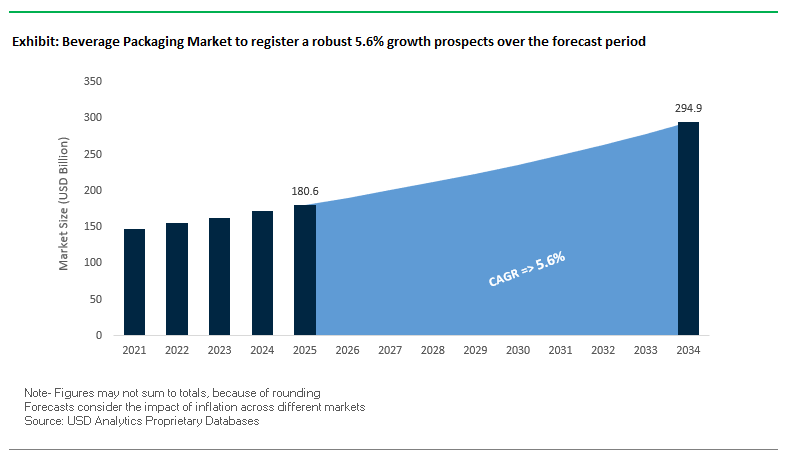

The global beverage packaging market is projected to grow from USD 180.6 billion in 2025 to USD 294.9 billion by 2034, registering a CAGR of 5.6%. This expansion is strongly driven by the shift toward sustainable packaging formats, particularly aluminum cans, cartons, and recycled-content plastics. Beverage companies are increasingly under regulatory and consumer pressure to reduce their environmental footprint, with industry leaders reporting recycled content levels of up to 70% in global production, and setting ambitious goals for 2030 and beyond.

Equally transformative is the rise of smart and connected packaging, where technologies such as QR codes, NFC tags, and AR-based storytelling are reshaping consumer engagement. Packaging is no longer just a protective container but a digital interface that enhances transparency, loyalty, and brand storytelling. Furthermore, food waste reduction through active packaging is becoming a critical growth driver, with innovations designed to extend shelf life and ensure quality during transit.

Key Insights for Industry Professionals

- Recyclability as a growth driver: Circular economy strategies dominate investment priorities.

- Smart packaging adoption: IoT-enabled labels and AR-driven engagement enhance consumer loyalty.

- Aluminum can surge: Infinitely recyclable and lightweight, cans are preferred for RTDs, beer, and premium waters.

- Food waste solutions: Active and intelligent packaging improves shelf life and quality assurance.

Strategic Mergers, Recycling Innovations, and Packaging Redesigns Reshape Beverage Packaging

The beverage packaging industry is evolving rapidly through mergers, investments, and packaging innovations. In August 2025, Smurfit WestRock debuted in New York and London following its merger, establishing itself as a dominant player in corrugated and paper-based beverage packaging. That same month, SIG received APR recognition for its recycle-ready bag-in-box package for wine, marking a step forward in circular packaging.

In July 2025, International Paper completed its acquisition of DS Smith, creating a new global leader in sustainable paper-based packaging solutions, while Novelis announced capacity expansion at its Alabama facility to meet strong demand for aluminum beverage packaging sheets. In April 2025, Coca-Cola unveiled plans to launch a cane sugar-based variant in the U.S., requiring a redefined packaging and labeling strategy to align with consumer expectations for natural and sustainable offerings.

Earlier initiatives have also reinforced market momentum. Ahlstrom (March 2025) expanded its LamiBak portfolio for beverage pouches, while Connecticut’s redemption rate (January 2025) jumped 21% due to deposit-return system reforms. In October 2024, Tetra Pak partnered with a dairy brand to introduce a plant-based carton derived from sugarcane polymers, further embedding sustainability in beverage packaging.

Transformative Trends and Lucrative Opportunities Shaping the Global Beverage Packaging Market

Strategic Capacity Expansion for Monomaterial PET and rPET Bottles

A major trend in the beverage packaging market is the rapid expansion of monomaterial PET and recycled PET (rPET) bottles, driven by regulatory mandates and corporate sustainability commitments. Leading beverage companies are investing heavily in production capabilities to meet recyclability targets and circular economy goals. For instance, PepsiCo reported a 5% reduction in virgin plastic use and 15% recycled content in key packaging markets between 2023 and 2024. Similarly, Coca-Cola Hellenic Bottling Company announced that in 2024, nearly 30 of its markets offered beverages in 100% rPET bottles, excluding labels and caps. Nestlé has pledged to use at least 25% rPET in EU plastic bottles by 2025, aiming to prevent any packaging from reaching landfills or oceans. Companies are also redesigning packaging for enhanced recyclability, such as shifting bottle colors to align with local recycling standards or using partial-bottle wrap labels. These investments in monomaterial PET and rPET are transforming the market by aligning sustainability with functional, high-quality beverage packaging.

Integration of Smart Packaging Technologies for Consumer Engagement and Traceability

The adoption of smart packaging technologies is accelerating in the beverage sector, enabling real-time traceability, anti-counterfeiting measures, and consumer engagement. Brands like Nestlé integrate QR codes on products like Zoégas coffee, providing detailed information on origin, processing, and sustainability. Coca-Cola leverages a “Sip and Scan” system to engage consumers with interactive rewards. The incorporation of NFC tags and IoT-enabled sensors enhances authenticity, particularly for premium beverages, by providing security that is harder to replicate than traditional labels. Beyond marketing, these technologies facilitate monitoring of freshness, temperature, and humidity for perishable beverages such as juices and dairy alternatives. This integration not only reduces food waste but also strengthens brand-consumer connections and supports data-driven insights into consumption behavior, positioning smart packaging as a key differentiator in the global beverage market.

Development of Paper-Based Barrier Solutions for Non-Carbonated Beverages

The success of paper-based bottles for carbonated drinks has unlocked opportunities for high-barrier paper solutions suitable for non-carbonated beverages, including juices, dairy alternatives, and RTD coffee. Technical challenges focus on developing coatings and multi-layer films that maintain oxygen and moisture barriers without compromising recyclability. Companies like Diageo have trialed paper-based bottles for Johnnie Walker, evaluating supply chain performance and scalability. Collaborative initiatives such as the Bottle Collective, led by PulPac and PA Consulting, aim to optimize barrier properties and production methods, targeting mainstream adoption by 2026. With increasing regulatory pressure and consumer demand for plastic reduction, the development of paper-based barrier packaging represents a significant growth avenue in sustainable beverage packaging.

Adoption of Lightweighting and Advanced Design to Reduce Material Use

Lightweighting and innovative bottle design are emerging opportunities to reduce material consumption, transportation emissions, and overall carbon footprint. Glass manufacturers such as Ardagh Group have reduced the weight of standard bottles by up to 40% over the past 15 years, creating containers that retain durability while minimizing material use. Advanced engineering software ensures optimal weight distribution, preserving strength and design aesthetics. Reduced weight allows more bottles per shipment, cutting fuel consumption and transportation costs, and directly supporting Scope 3 emissions reduction targets. In addition to sustainability, lightweighting offers clear cost savings on materials, creating a dual benefit for profitability and environmental impact. This trend positions optimized bottle design as a strategic lever for beverage companies aiming to combine efficiency, sustainability, and brand differentiation.

Global Leaders Compete with Aluminum, Carton, Glass, and Flexible Packaging Innovations

The competitive landscape of the global beverage packaging market is marked by intense rivalry among companies leveraging sustainability, material innovation, and digital engagement as their growth strategies.

Amcor plc: Repositioning Through Portfolio Optimization

Amcor remains a leader in flexible and rigid plastic packaging, offering PET bottles, closures, and flexible pouches for beverages. After acquiring Berry Global, the company is considering divesting its North American beverage business to refocus on its core growth segments. Key innovations include its Secure Flip tamper-evident closures and PET bottles with high post-consumer recycled content, reinforcing its commitment to 100% recyclable or reusable packaging by 2025.

Crown Holdings, Inc.: Expanding Can-making Capacity Globally

Crown dominates in aluminum beverage cans and steel food cans, catering to beer, soft drinks, energy drinks, and RTDs. To meet growing demand, Crown is adding new two-piece aluminum can lines worldwide. Its SuperEnd technology and 360 End full-can opening feature highlight its technical leadership and customer loyalty, while its strategy focuses on sustainability and footprint reduction.

Ball Corporation: Leading the Aluminum Beverage Can Revolution

Ball is a pioneer in lightweight, infinitely recyclable aluminum cans, supplying beverage giants with formats ranging from standard 12-ounce to slim RTD-ready cans. Its sustainability focus is evident in its partnership with PepsiCo to launch a can with 90% recycled content. With innovation targeting premium categories such as RTD cocktails and functional beverages, Ball strengthens its role as the global leader in aluminum beverage packaging.

Tetra Pak International S.A.: Innovating with Renewable Cartons

Tetra Pak leads in aseptic carton packaging for milk, juices, and plant-based beverages. In recent years, it earned EcoVadis Platinum rating, underscoring its sustainability leadership. Its strategy centers on food safety, renewable materials, and carbon reduction, while expanding partnerships such as its 2024 plant-based carton initiative with a European dairy brand. Tetra Pak continues to set benchmarks in renewable and recyclable beverage cartons.

Ardagh Group S.A.: Strengthening Glass Packaging Sustainability

Ardagh remains a powerhouse in glass bottles and metal cans for beverages, focusing on premium wine, beer, and spirits packaging. In 2024, it formed a joint venture with Verdant BioGlass to enhance recycled content in glass bottles, aligning with consumer and regulatory sustainability goals. With its strong manufacturing expertise and innovation in high-quality glass packaging, Ardagh reinforces its competitive edge in premium beverage segments.

Beverage Packaging Market Share Insights

Bottles Lead Market Share by Product Type in Beverage Packaging

Bottles dominate with 40% share of the beverage packaging market, making them the most versatile and consumer-preferred format. PET bottles remain the backbone of bottled water and carbonated soft drinks due to lightweighting innovations, resealability, and compatibility with high-speed filling lines. Glass bottles continue to hold importance in premium segments like wine and spirits, offering superior product perception and shelf appeal. Although cans are gaining momentum as a sustainable alternative, bottles’ adaptability across categories from functional beverages to sports drinks keeps them at the forefront. Ongoing investments in recycled PET (rPET) and tethered caps to meet regulatory and environmental standards reinforce bottles’ leadership as the primary choice for mass-market and premium beverages alike.

Non-Alcoholic Beverages Dominate Market Share by Application in Beverage Packaging

Non-alcoholic beverages account for 75% of beverage packaging demand, driven by the massive global consumption of bottled water, carbonated soft drinks, juices, and ready-to-drink teas and coffees. The segment’s dominance reflects both its scale and innovation intensity: packaging suppliers continuously optimize formats for lightweighting, extended shelf-life, and higher recycled content integration. With rising health consciousness, demand for functional beverages and plant-based drinks further accelerates growth in PET bottles, aseptic cartons, and flexible pouches. While alcoholic beverages remain a high-value niche characterized by premium packaging tied to brand identity, the daily consumption volumes and distribution scale of non-alcoholic beverages make this segment the foundation of the global beverage packaging industry.

United States Beverage Packaging Market Driven by EPR Laws, Smart Bottles, and Sustainable Materials

The United States beverage packaging market is shaped by a complex regulatory landscape where the U.S. Food and Drug Administration (FDA) enforces strict material safety standards and state-level Extended Producer Responsibility (EPR) laws increasingly dictate recycling obligations. States such as Oregon and Colorado are requiring beverage companies to fund and manage recycling systems, accelerating adoption of recyclable and reusable packaging. Major corporations are responding with investments in sustainable packaging innovation. PepsiCo has rolled out 100% recycled PET (rPET) bottles globally, while Coca-Cola has pioneered smart beverage bottles in the U.S. using NFC tags to provide consumers with recycling information and interactive engagement, showcasing how technology enhances both compliance and consumer experience.

The U.S. beverage packaging market also reflects broader sustainability trends, with a strong push toward reusable, recyclable, and lightweight formats. The Association of Plastic Recyclers (APR) has certified leading designs for recyclability, driving industry-wide adoption. Demand is particularly robust in the single-serve and ready-to-drink (RTD) beverage segment, where aluminum cans and rPET bottles are gaining popularity for functional beverages, water, and low-calorie sodas. Minimalist design trends, combined with innovations like paper-based multi-pack wraps and lightweight bottles, highlight the U.S. as a leader in sustainable and smart packaging solutions tailored to evolving consumer preferences.

Germany Beverage Packaging Market Strengthened by EU PPWR and Circular Economy Leadership

Germany’s beverage packaging market is tightly regulated under the EU Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be recyclable by 2030. Adding to this, Germany introduced a Single-Use Plastics levy in 2024, with payments commencing in 2025, covering beverage containers up to three liters. The Packaging Act (VerpackG) further strengthens producer responsibility, compelling beverage companies to design packaging compatible with recycling streams and to actively support collection and recovery systems. These policies are positioning Germany as a model for sustainable beverage packaging within Europe.

Technological innovation is accelerating, with companies introducing new substrates such as grass paper, high-strength recycled fibers, lightweight glass, and metal containers to reduce environmental impact. The beer, wine, and carbonated soft drink segments are particularly strong, supported by Germany’s well-established bottle reuse and recycling systems. International investments in European beverage can production, such as Chinese-owned CPMC Holdings’ new plant in Hungary, highlight Europe’s attractiveness, with Germany serving as a central hub due to its regulatory alignment and recycling infrastructure. Overall, Germany continues to lead in circular economy-driven packaging innovation while preserving its deep-rooted beverage culture.

China Beverage Packaging Market Expands with Dual Carbon Goals, AI-Driven Efficiency, and E-Commerce Growth

China’s beverage packaging market is expanding rapidly under government initiatives aligned with the nation’s “dual carbon” goals, which restrict non-degradable plastics and promote sustainable alternatives. The “Made in China 2025” plan has further boosted domestic manufacturing capacity, encouraging local companies to substitute imports with homegrown technology and production. Regulatory reforms led by the State Administration for Market Regulation (SAMR) are updating “GB” food-contact standards to align with global safety practices, providing a framework for recyclable beverage packaging innovation.

Technological adoption is transforming operations, with manufacturers integrating automation, AI, and “5G plus industrial internet” to enhance flexible production capacity. China’s beverage packaging demand is particularly driven by the booming bottled water, fruit juice, and ready-to-drink tea industries, which require lightweight, cost-effective, and recyclable solutions. The rise of e-commerce has added pressure for durable, compact, and shipping-friendly formats, fueling demand for flexible pouches and smaller bottles. Corporate initiatives, such as PepsiCo’s transition to partial-wrap labels for Pepsi Black in China, are designed to improve recyclability while aligning with consumer expectations, making China one of the fastest-growing markets for sustainable beverage packaging.

India Beverage Packaging Market Boosted by Plastic Ban, rPET Regulations, and Rapid Consumption Growth

The beverage packaging market in India is evolving quickly due to government-led sustainability initiatives. The “Make in India” and “Zero Effect Zero Defect” missions encourage quality domestic production, while the Ministry of Environment, Forest, and Climate Change (MoEFCC) has enacted a ban on single-use plastics, creating vast opportunities for paper-based and recyclable alternatives. The Food Safety and Standards Authority of India (FSSAI) has intensified regulation, mandating 30% recycled PET content in beverage bottles starting April 2025. This requirement is driving a redesign of supply chains and catalyzing large-scale investments in food-grade rPET production.

Corporate investments are expanding capacity to meet rising demand, with Ganesha Ecopet boosting bottle-to-bottle recycling operations and UFlex Ltd. achieving U.S. FDA approval for its recycling process, marking a milestone for India’s global packaging competitiveness. The beverage packaging market is also benefiting from technological advancements, including automation and advanced barrier films that enhance shelf life and product safety. Demand is particularly strong from India’s expanding middle class, with dairy products, fruit juices, and ready-to-drink beverages fueling rapid growth. India is emerging as both a manufacturing hub and a consumer powerhouse for sustainable beverage packaging solutions.

Brazil Beverage Packaging Market Supported by ANVISA Regulations, Aluminum Recycling, and Green Innovations

Brazil’s beverage packaging market is evolving under regulatory reforms led by ANVISA, whose new risk-based pre-market control framework implemented in September 2024 impacts all food and beverage packaging. Governmental support for recycling, including the January 2025 law sanctioning solid waste imports to bolster the circular economy, is strengthening the country’s ability to process recyclable materials domestically. Brazil’s impressive aluminum recycling rate, one of the highest globally, is attracting significant investments, with CANPACK Group establishing a new beverage can plant to capitalize on robust demand.

Technological advancements in robotics and AI are improving efficiency and quality control in packaging production, enabling automated defect detection and smarter operations. Sustainability is another strong focus, with companies like Klabin pioneering recyclable innovations such as the Wicket Paper Bag. Beverage demand is particularly high in wine, fruit juice, and soy-based drink segments, fueled by the expansion of Brazil’s food processing industry. With regulatory backing, a strong recycling culture, and corporate investment in green packaging materials, Brazil is positioning itself as a leading Latin American market for sustainable beverage packaging.

Japan Beverage Packaging Market Driven by Bioplastic Roadmap, Advanced Films, and Smart Collaborations

Japan’s beverage packaging market is advancing rapidly due to its precision manufacturing culture and government-backed sustainability goals. The Ministry of Health, Labour and Welfare (MHLW) updated food-contact packaging standards in May 2025, requiring stricter compliance under the Food Sanitation Act. At the same time, Japan’s bioplastic roadmap targets mass adoption of bioplastic packaging by 2030, stimulating research and innovation in bio-based and biodegradable barrier films. Companies like Oji Holdings, Toppan, and Nippon Paper Industries are pioneering solutions that combine recyclability with advanced performance properties.

Functionality and innovation are central to Japan’s beverage packaging sector. Companies are developing high-barrier, paper-based alternatives with exceptional dimensional stability and resistance to deformation, supporting demanding applications in beverages and ready-to-drink products. Collaborations between packaging giants are fostering breakthroughs in recyclable coatings and smart packaging features, aligning with Japan’s push for circular systems. As both corporate R&D and academic research continue to deliver cutting-edge solutions, Japan remains a global leader in high-performance, eco-friendly beverage packaging technologies.

Beverage Packaging Market Report Scope

Beverage Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$180.6 Billion

|

|

Market Size (2034)

|

$294.9 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (Plastics, Glass, Metal, Paper & Paperboard, Others), By Product Type (Bottles, Cans, Cartons, Pouches & Sachets, Cups & Lids, Others), By Application (Alcoholic Beverages, Non-Alcoholic Beverages), By End-User (Commercial, Institutional)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ball Corporation, Amcor plc, Crown Holdings Inc., Tetra Pak, Mondi Group, DS Smith Plc, WestRock Company, Sonoco Products Company, Ardagh Group S.A., Berry Global Inc., Oji Holdings Corporation, ALPLA Group, Smurfit Kappa Group, Huhtamäki Oyj, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Beverage Packaging Market Segmentation

By Material Type

- Plastics

- Glass

- Metal

- Paper & Paperboard

- Others

By Product Type

- Bottles

- Cans

- Cartons

- Pouches & Sachets

- Cups & Lids

- Others

By Application

- Alcoholic Beverages

- Non-Alcoholic Beverages

By End-User

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Beverage Packaging Market

- Ball Corporation

- Amcor plc

- Crown Holdings Inc.

- Tetra Pak

- Mondi Group

- DS Smith Plc

- WestRock Company

- Sonoco Products Company

- Ardagh Group S.A.

- Berry Global Inc.

- Oji Holdings Corporation

- ALPLA Group

- Smurfit Kappa Group

- Huhtamäki Oyj

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics applies a robust, multi-faceted research methodology to analyze the global beverage packaging market, integrating primary and secondary data sources for actionable insights. Primary research involves consultations with packaging manufacturers, beverage companies, material suppliers, and end-users across alcoholic, non-alcoholic, commercial, and institutional sectors. Secondary research leverages corporate reports, regulatory publications, sustainability frameworks, and trade journals to track trends in smart packaging, lightweighting, recycled PET (rPET), aluminum cans, aseptic cartons, and paper-based solutions. Market sizing and forecasts are derived using proprietary models accounting for drivers such as circular economy adoption, sustainability mandates, technological integration, and material innovations. Competitive landscape assessments cover strategic mergers, acquisitions, capacity expansions, and product innovations by global leaders including Ball Corporation, Tetra Pak, Amcor, Crown Holdings, and Ardagh Group. Regional analysis incorporates regulatory frameworks, including the EU PPWR, U.S. EPR laws, China’s dual carbon initiatives, India’s rPET mandates, and Japan’s bioplastic roadmap, alongside emerging trends in e-commerce packaging, smart labels, and active packaging. By triangulating verified quantitative data with expert insights, USDAnalytics provides industry professionals with comprehensive, forward-looking intelligence on opportunities, innovation, and growth strategies in the global beverage packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.