Market Overview: Glass Packaging Market to Reach $136.8 Billion by 2034 on Premiumization and Circular Economy Growth

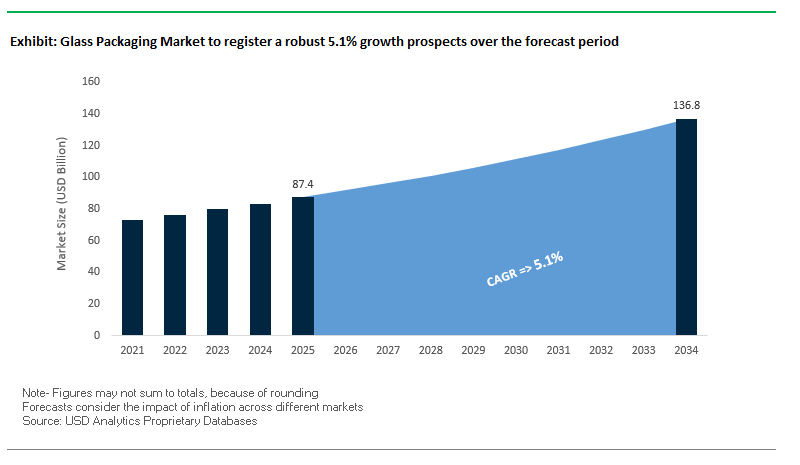

The global glass packaging market is valued at $87.4 billion in 2025 and is projected to reach $136.8 billion by 2034, expanding at a CAGR of 5.1%. Glass packaging continues to dominate in beverages, food, and pharmaceuticals, supported by its sustainability, recyclability, and product safety benefits. The industry is increasingly driven by lightweighting innovations, recycled content adoption, and premiumization trends, as brands align with consumer expectations for eco-friendly yet high-quality packaging.

Key Insights for industry professionals:

- Lightweighting drives cost & CO₂ reduction: New lightweight bottles, such as Ardagh Glass Packaging-Europe’s 300g wine bottle (Jul 2025), highlight progress in lowering logistics emissions.

- Cullet (recycled glass) integration surges: O-I Glass achieved 40% global cullet usage (Jul 2025), with some regions surpassing 75%, strengthening the circular economy.

- Premiumization sustains glass demand: Glass remains the packaging of choice in wine, spirits, and luxury beverages, enhancing brand value and consumer appeal.

- Non-reactive safety edge: Glass’ chemical inertness supports growth in pharma and biotech packaging, with Gerresheimer AG expanding global vial and cartridge portfolios.

Market Analysis: Recent Developments Reinforce Glass Packaging Innovation and Expansion

The glass packaging industry has seen rapid advancements in 2024–2025, reflecting sustainability targets, operational restructuring, and regional expansion. In September 2025, O-I Glass announced plans to shut its Portland, Oregon facility, impacting around 90 jobs, as part of strategic optimization. Simultaneously, in August 2025, O-I posted a strong Q2, with its “Fit to Win” initiatives reducing costs and delivering 4% growth in Americas sales volumes, offsetting sluggish European demand.

Also in August 2025, Verallia reported a rebound in profitability, highlighting volume gains and improved cash generation, underpinned by new financing strategies that strengthen growth capacity. Verallia’s acquisition of Vidrala’s Italian division (Jul 2024, €230M) reinforced its European footprint, giving access to advanced furnace capacity. Meanwhile, Ardagh Glass Packaging received multiple Clear Choice Awards (May 2025) for innovative, sustainable designs and in April 2025 switched its California plant to renewable solar power, advancing decarbonization targets.

Capacity expansion is a critical theme. Vitro announced a $70M furnace project in Toluca, Mexico (Mar 2025), responding to surging regional demand. Parallelly, machinery ecosystems evolved, with Krones’ acquisition of Netstal Maschinen AG (Jul 2025) strengthening closed-loop PET solutions impacting competitive strategies in adjacent packaging markets. The industry’s trajectory underscores a dual focus: premium consumer appeal through innovation and structural efficiency gains through recycled content and renewable energy adoption.

Trends and Opportunities Defining the Glass Packaging Market

Capital Intensity in Furnace Modernization and Cullet Processing

The glass packaging market is experiencing unprecedented capital intensity as manufacturers commit multi-million-dollar investments to modernize furnaces and expand cullet processing facilities. These initiatives are aimed at improving energy efficiency, lowering emissions, and ensuring compliance with tightening recycled content mandates. In the U.S., Arglass secured over $230 million to build a second advanced furnace at its Georgia site, expected to be fully operational by 2025. This expansion reflects a growing emphasis on localized production capacity to meet demand for domestically sourced glass containers.

In Europe, Gerresheimer completed a €100 million modernization at its Lohr site in May 2025, anchored by an oxy-hybrid melting furnace capable of operating with up to 50% electricity. This upgrade is projected to cut CO₂ emissions by up to 40% compared to conventional technology, underscoring the role of advanced furnaces in decarbonization strategies. Meanwhile, in Asia, AGI Greenpac in India announced a ₹230 crore modernization investment in July 2024 to increase production output and meet both domestic and export demand. These large-scale investments highlight how furnace upgrades and cullet processing infrastructure have become essential levers for growth, efficiency, and regulatory compliance in the glass packaging market.

Legislative and Corporate Mandates Driving PCR Content Integration

The integration of Post-Consumer Recycled (PCR) glass content is accelerating under the dual influence of regulatory frameworks and corporate sustainability goals. India’s draft Environment Protection (EPR for Packaging) Rules, 2024 mandates recycled content thresholds starting at 50% by 2026–27 and increasing to 80% by 2029–30, making cullet integration a compliance necessity. Similarly, the European Union’s Packaging and Packaging Waste Regulation (PPWR), adopted in April 2024, enforces recyclability targets by 2030, directly pressuring all packaging materials, including glass, to integrate higher levels of recycled content.

On the corporate front, leading CPG companies like Unilever, Nestlé, and Coca-Cola have set ambitious public targets to incorporate between 50–100% PCR materials in their packaging portfolios within the next few years. These brand commitments are reshaping procurement and supply chain priorities, forcing glass manufacturers to secure high-purity cullet streams. The combination of legally binding mandates and market-driven sustainability pledges ensures that PCR integration is no longer optional but a strategic and operational requirement in the global glass packaging sector.

Capturing Value in the Premium Non-Alcoholic Beverage Segment

The rise of premium functional beverages and adult non-alcoholic drinks represents a lucrative growth opportunity for glass packaging manufacturers. Categories such as kombucha, botanical-infused sodas, cold-pressed juices, and mocktails are expanding rapidly, with consumers associating glass bottles with purity, quality, and premium positioning. A 2025 consumer trends study revealed that buyers are increasingly willing to pay higher prices for beverages offering health benefits, provided they are packaged in glass, which conveys luxury and authenticity.

Glass provides unmatched flavor preservation due to its inert properties, ensuring that beverages retain their natural taste and nutritional value without chemical interaction. This characteristic makes glass particularly attractive for products with delicate flavors and active ingredients. Moreover, glass’s aesthetic and branding potential including custom shapes, embossing, and premium closures allows brands to differentiate themselves in a competitive marketplace. Reports from the non-alcoholic beverage sector highlight that packaging is becoming a critical tool for market differentiation, with glass providing the visual and sensory premiumization that resonates with health-conscious and eco-aware consumers.

Forming Strategic Closed-Loop Alliances to Secure Supply

The surge in recycled content mandates and brand-level sustainability commitments creates a major opportunity for manufacturers to move beyond commoditized cullet markets and form direct closed-loop recycling partnerships. These alliances between glass producers, brand owners, municipalities, and waste management companies are vital to securing furnace-ready cullet at the scale required for long-term production stability.

The Close the Glass Loop initiative in Europe exemplifies this approach, bringing together stakeholders to boost collection rates to 90% by 2030. By focusing on color sorting and high-purity streams, such initiatives ensure consistent quality for re-melted glass packaging. In July 2025, Cosmetics Europe partnered with the platform to address recycling challenges specific to cosmetic glass, demonstrating how sector-specific alliances can create tailored solutions.

These partnerships also open the door to brand-led investments in recycling infrastructure, creating localized supply loops that enhance material security and circularity. Beyond regulatory compliance, these collaborations present a strategic business model shift, where manufacturers and brands co-invest to guarantee sustainable cullet supply, strengthen ESG credentials, and future-proof their packaging portfolios against tightening regulatory demands.

Competitive Landscape: Global Leaders Drive Lightweighting, Sustainability, and Expansion

The glass packaging market is highly consolidated, led by multinational corporations advancing lightweighting, cullet integration, renewable energy, and custom design services. Competition is centered on ESG commitments, premium brand alignment, and regional capacity expansions.

O-I Glass: “Fit to Win” strategy strengthens Americas growth

O-I Glass is among the world’s largest glass container producers, supplying food, beverage, and pharma. Its “Fit to Win” program modernizes facilities and optimizes its footprint, fueling a 4% Americas sales volume rise in Q2 2025. A pioneer in lightweighting, O-I introduced a 75cl wine bottle 25% lighter than conventional designs (Carbon Trust validated). With operations in 20+ countries and its MAGMA modular furnace technology, O-I leads in flexible, lower-carbon glass production.

Verallia: European leader expanding recycled-content innovation

Verallia is a premier European supplier of wine, spirits, and food bottles. Its €230M acquisition of Vidrala Italy (Jul 2024) expanded furnace capacity by 225 kt/year. In Aug 2025, Verallia reported improved profitability and financing momentum to fund growth. Its “Verallia Green” line emphasizes high recycled content and lightweight solutions, reinforcing its reputation as a circularity-driven packaging partner for more than 10,000 customers worldwide.

Ardagh Group: Award-winning lightweight bottles powered by renewables

Ardagh Group produces infinitely recyclable glass across food and beverage segments. It won multiple Clear Choice Awards (May 2025) for design-led sustainable bottles and powered its California plant with solar energy (Apr 2025). Its ECO Series™ lightweight bottles reduce emissions while preserving strength. Ardagh’s **full-service integration design, manufacturing, decoration **helps global brands enhance premium shelf impact with sustainable value propositions.

Gerresheimer: Pharma and biotech packaging specialization

Gerresheimer AG supplies precision glass for pharma, biotech, and cosmetics, including vials, ampoules, and cartridges. In Aug 2025, it secured €200M loans to refinance its Bormioli Pharma acquisition, supporting strategic growth. It operates globally, producing 5B+ vials annually, and leads in drug delivery devices like pens and inhalers. Its differentiation lies in regulatory expertise, medical precision, and expansion into high-growth emerging markets.

Vidrala: Streamlined focus on carbon neutrality and efficiency

Vidrala specializes in lightweight wine and spirits bottles. Following the divestment of its Italian operations to Verallia (Jul 2024), Vidrala sharpened its European focus. Its strategy emphasizes carbon neutrality, investing in new furnace technologies and alternative fuels. Vidrala’s agility in lightweight design and sustainable operations positions it as a key partner for brands pursuing both efficiency and eco-responsibility.

Vitro: North American capacity expansion for regional demand

Vitro is a major player in North America’s food and beverage glass packaging segment. To meet growing demand, it committed $70M (Mar 2025) to build a new furnace in Toluca, Mexico, featuring advanced glass production technology. Vitro’s investments highlight its focus on capacity reliability and technology upgrades, ensuring strong supply chains for regional customers in beverage and food markets.

Glass Packaging Market Share Insights

Bottles Dominate Glass Packaging Market Share by Product Type

In 2025, glass bottles account for 58% of the global glass packaging market, making them the undisputed leader across all product types. Their dominance is anchored in the global beverage industry, where glass remains irreplaceable for preserving taste integrity and reinforcing premium brand positioning in categories such as beer, wine, spirits, and premium non-alcoholic drinks. Jars contribute a significant share as the workhorse of food preservation, particularly for baby food, sauces, and gourmet products where transparency and safety drive consumer trust. Vials and ampoules, though smaller in volume, represent a high-value niche with roughly 15% share, propelled by the pharmaceutical industry’s need for sterile, chemically inert, and tamper-proof packaging for vaccines and biologics. Other containers, including decorative formats and technical vessels, play a niche but stable role in luxury, specialty, and industrial applications. Collectively, this segmentation demonstrates how bottles dominate high-volume demand, jars maintain stability in food, and vials & ampoules drive value growth in pharma and biotech.

Beverages Anchor Glass Packaging Market Share by Application

By application, beverages command 55% of the glass packaging market in 2025, solidifying their position as the industry’s growth engine. Alcoholic beverages, particularly beer, spirits, and wine, remain the largest consumers of glass bottles due to their deep association with brand heritage, consumer trust, and sensory experience. Non-alcoholic beverages such as premium juices, craft sodas, and mineral waters further amplify this dominance, leveraging glass to reinforce purity and product differentiation. Food packaging holds around 20%, sustained by consumer preference for glass jars in sauces, condiments, and baby food, where flavor preservation and visibility are critical. Pharmaceuticals, though smaller in share, are a high-growth driver as injectable drugs, biologics, and vaccines expand, all requiring borosilicate glass vials for safety and compliance. Cosmetics and perfumes sustain glass’s role as a luxury material, with finely crafted bottles and jars used to justify premium pricing and strengthen brand prestige. This segmentation underscores how the beverage sector anchors industry volumes, while pharmaceuticals and cosmetics reinforce glass’s premium and safety-driven value propositions.

United States: Driving Sustainability and Premiumization in Glass Packaging

The U.S. glass packaging industry is increasingly focused on sustainability, lightweighting, and premiumization to meet evolving consumer and regulatory demands. Major players like O-I Glass are leading the charge in lightweighting technology, developing furnaces to produce lighter glass containers that reduce transportation costs and carbon emissions. In September 2023, Ardagh Group partnered with St. Michelle Wine Estates to introduce ECO Series sustainable glass bottles, which have a 25% smaller carbon footprint compared to traditional bottles. The Glass Packaging Institute (GPI) is advancing recycling infrastructure by increasing the availability of recycled glass (cullet), lowering energy consumption and reliance on virgin materials. The craft beverage sector, including beer, wine, and spirits, is driving premiumization, with custom-designed bottles and advanced decoration techniques enhancing brand differentiation. Regulatory advantages, such as the FDA’s GRAS classification for glass, provide chemical safety assurances, while smart packaging innovations like QR codes enhance transparency and consumer engagement by sharing information on product origin, nutrition, and recycling.

Germany: Circular Economy Leadership and Advanced Pharmaceutical Glass Solutions

Germany’s glass packaging market is shaped by strict regulatory frameworks, including the German Packaging Act (VerpackG) and the upcoming EU Packaging and Packaging Waste Regulation (PPWR). From January 2026, a minimum standard for determining packaging recyclability will align design practices with actual recycling capabilities. German manufacturers, such as Stoelzle Glass Group, are leaders in lightweighting technology, producing low-weight, high-quality glass for pharmaceutical, cosmetic, and spirits sectors, reducing the carbon footprint of production and transportation. Germany also excels in pharmaceutical glass, with Gerresheimer AG developing sustainable glass vials for injectable drugs to meet growing demand for safe, reliable packaging. Circular economy initiatives drive production with high percentages of recycled cullet, supported by advanced optical sorting technologies using NIR spectroscopy and X-ray systems to comply with stringent regulations. The government’s target of 90% glass recycling is further incentivizing manufacturers to adopt sustainable practices.

China: Expanding Domestic Demand and Government-Led Sustainability Initiatives

China’s glass packaging market benefits from rapid urbanization, rising disposable incomes, and strong domestic demand, especially in the alcoholic beverage sector with products like baijiu. The growing middle class is fueling demand for premium, aesthetically appealing glass packaging with advanced decoration techniques for cosmetics, perfumery, and spirits. Government policies such as plastic bans, waste management regulations, and the Cleaner Production Promotion Law encourage cleaner production methods, pushing manufacturers to adopt sustainable, reusable glass packaging. International expansion is also a key trend; in August 2024, Tefu International launched a new production line in Tanzania, expanding regional coverage and addressing local market needs.

India: Make in India and Rising Specialty Glass Demand

India’s glass packaging industry is receiving a boost from the “Make in India” initiative, attracting capital investments and expanding domestic manufacturing capacities. Major players such as AGI Greenpac are investing in greenfield facilities to produce high-end specialty glass for cosmetics, perfumery, and export markets. Rising consumer awareness of health, hygiene, and product quality is driving a shift towards glass packaging for food and pharmaceutical applications. The alcoholic beverage segment, particularly premium Indian Made Foreign Liquor (IMFL), is a key growth driver, with increasing adoption of 100% glass packaging. Additionally, in May 2023, Gerresheimer enhanced its production capabilities in India with a state-of-the-art facility in Kosamba, producing high-quality containers and plastic closures to meet growing market demand.

Brazil: Circular Economy and Sustainability Boosting Glass Packaging Adoption

The Brazilian glass packaging market is increasingly influenced by sustainability initiatives and regulatory frameworks. A WWF-Brasil study highlights that reducing disposable plastic could generate BRL 6 billion in market value and prevent 18 million tons of CO₂ emissions, supporting the shift to alternative materials like glass. Anvisa continues to update regulations for food contact materials, ensuring high-quality and safe glass packaging. Brazil’s National Solid Waste Policy mandates reverse logistics for packaging waste, promoting recycling and circular economy practices. Programs like Recircula Brasil, launched in August 2024 by ABDI and Abiplast, track recycled plastics and enhance recycling efforts, indirectly driving innovation and adoption in the glass packaging segment.

Japan: Lightweighting Innovations and Advanced Recycling in Glass Packaging

Japan’s glass packaging market is at the forefront of lightweighting technology, with companies like Toyo Glass developing eco-friendly, energy-efficient glass packaging. Strict adherence to the Japanese Sanitation Act ensures high-quality, hygienic, and safe packaging, minimizing contamination risks. Japan has developed an extensive recycling infrastructure with over 18 facilities processing glass bottles and containers into cullets and powder for new production. In April 2024, AGC successfully demonstrated the use of approximately 5 tons of recycled solar panel cover glass in float glass production, marking a significant advancement in sustainable recycling technology and setting a benchmark for eco-friendly manufacturing practices in the industry.

Glass Packaging Market Report Scope

Glass Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$87.4 Billion

|

|

Market Size (2034)

|

$136.8 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint (Clear), Amber, Green, Other Colors), By Application (Beverages, Food Packaging, Pharmaceuticals, Cosmetics & Perfumes, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Owens-Illinois (O-I), Ardagh Group S.A., Verallia S.A., Gerresheimer AG, Vidrala S.A., Vitro S.A.B. de C.V., Stoelzle Glass Group, Hindustan National Glass & Industries Limited (HNG), AGI Greenpac, Consol Glass (Pty) Ltd., PGP Glass Private Limited, Nihon Yamamura Glass Co., Ltd., Zignago Vetro S.p.A., Anchor Glass Container Corporation, Saverglass S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Packaging Market Segmentation

By Product Type

- Bottles

- Jars

- Vials & Ampoules

- Other Containers

By Color

- Flint

- Clear

- Amber

- Green

- Other Colors

By Application

- Beverages

- Food Packaging

- Pharmaceuticals

- Cosmetics & Perfumes

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Glass Packaging Market

- Owens-Illinois (O-I)

- Ardagh Group S.A.

- Verallia S.A.

- Gerresheimer AG

- Vidrala S.A.

- Vitro S.A.B. de C.V.

- Stoelzle Glass Group

- Hindustan National Glass & Industries Limited (HNG)

- AGI Greenpac

- Consol Glass (Pty) Ltd.

- PGP Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Zignago Vetro S.p.A.

- Anchor Glass Container Corporation

- Saverglass S.A.

*List not Exhaustive

Research Coverage

This report investigates the evolving dynamics of the global glass packaging market, highlighting breakthroughs in lightweighting, post-consumer recycled (PCR) content integration, premiumization trends, and circular economy initiatives. USDAnalytics’ analysis reviews structural expansions, furnace modernization programs, and strategic acquisitions shaping competitive advantages in key regions. The report highlights industry developments such as Ardagh Glass Packaging-Europe’s 300g wine bottles, Verallia’s acquisition of Vidrala’s Italian operations, and O-I Glass’s “Fit to Win” initiatives, illustrating how manufacturers balance sustainability, operational efficiency, and premium brand appeal. Furthermore, this report is an essential resource for packaging executives, sustainability managers, and investors seeking insights into market drivers, regional growth patterns, and competitive positioning across beverages, food, pharmaceuticals, and cosmetics. By examining capacity expansions, recycling initiatives, and regulatory compliance strategies, USDAnalytics provides a comprehensive understanding of the forces shaping the market and the opportunities for strategic investment and innovation.

Scope Highlights:

- Segmentation: By Product Type (Bottles, Jars, Vials & Ampoules, Other Containers), By Color (Flint/Clear, Amber, Green, Other Colors), By Application (Beverages, Food Packaging, Pharmaceuticals, Cosmetics & Perfumes, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Time Horizon: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Owens-Illinois (O-I), Ardagh Group S.A., Verallia S.A., Gerresheimer AG, Vidrala S.A., Vitro S.A.B. de C.V., Stoelzle Glass Group, Hindustan National Glass & Industries Limited (HNG), AGI Greenpac, Consol Glass (Pty) Ltd., PGP Glass Private Limited, Nihon Yamamura Glass Co., Ltd., Zignago Vetro S.p.A., Anchor Glass Container Corporation, Saverglass S.A.

Methodology

This report employs a comprehensive methodology combining primary and secondary research, market modeling, and expert validation to ensure accuracy and reliability. USDAnalytics gathered primary insights from interviews with key industry stakeholders, including packaging executives, sustainability officers, and technology providers, while secondary sources included corporate disclosures, industry journals, regulatory documents, and market databases. Quantitative analysis leverages historical trends from 2021–2024, while predictive modeling projects the market trajectory from 2025–2034, accounting for factors such as premium beverage growth, PCR adoption mandates, regional investment in furnace modernization, and sustainability-driven consumer behavior. Competitive benchmarking, supply chain mapping, and scenario analysis provide a multi-dimensional understanding of the market landscape, enabling strategic recommendations for investors, manufacturers, and brand owners.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.