Packaging Materials Market Set to Surpass $1,003 Billion by 2034 Driven by Circularity and Smart Materials

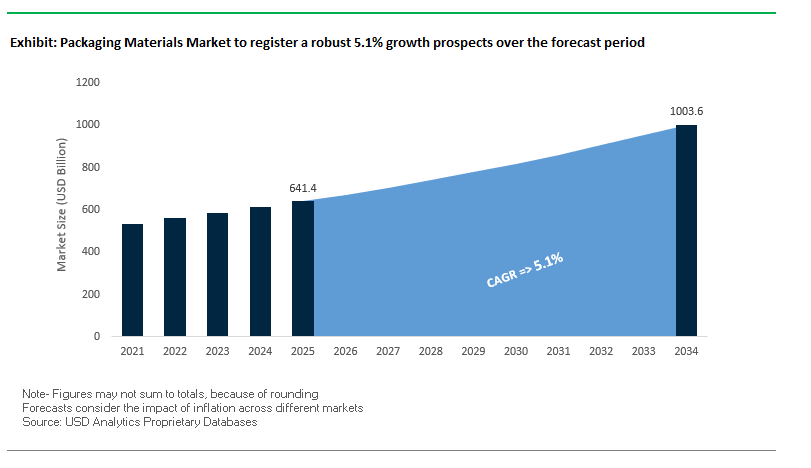

The Global Packaging Materials Market is projected to grow from $641.4 billion in 2025 to $1,003.6 billion by 2034, representing a CAGR of 5.1%. This growth underscores the critical role of packaging materials in protecting, preserving, and presenting goods across industries, while serving as a primary interface between brands and consumers. The market is increasingly defined by sustainability, digitalization, and superior barrier properties, with companies innovating to meet regulatory demands, consumer expectations, and supply chain efficiency goals.

Key Insights for Industry Professionals:

- Shift Towards Circular and Recyclable Materials: Regulatory pressures and consumer demand are driving adoption of mono-material and high-recycled-content solutions, replacing complex multilayer structures.

- Lightweighting and Material Efficiency: Innovations in thinner, stronger materials reduce both raw material usage and transportation costs, lowering carbon footprints.

- Enhanced Barrier Performance: Advanced materials provide superior protection against moisture, oxygen, and light, extending product shelf life and reducing food waste.

- Digital and Smart Material Integration: Materials embedded with QR codes, RFID, and other digital features are transforming packaging into interactive, traceable, and anti-counterfeiting tools.

- Sustainability as a Competitive Advantage: Companies increasingly integrate eco-friendly materials and resource-efficient production methods to meet global environmental goals.

The market is poised for strategic expansion, with a strong emphasis on innovative, sustainable, and digitally connected packaging materials that address modern consumer and supply chain needs.

Market Growth Accelerated by Strategic Acquisitions, Sustainable Innovation, and Regional Expansions

The Packaging Materials Industry has experienced several pivotal developments highlighting sustainability, technological innovation, and market consolidation. In August 2025, Avery Dennison acquired Meridian Adhesives Group’s U.S.-based flooring adhesives business for $390 million, expanding its specialty adhesives portfolio.

July 2025 marked the completion of the Amcor-Berry Global all-stock combination, creating a dominant player in flexible and rigid packaging materials. The same month, UPM Adhesive Materials invested in a state-of-the-art coating line in Johor Bahru, Malaysia, accelerating growth in Southeast Asia.

In June 2025, Mondi collaborated with Saga Nutrition to launch a paper-based pet food pouch, reducing plastic usage. May 2025 saw Avery Dennison opening a joint venture apparel facility in Vietnam, integrating Embelex innovations and RFID technology for digital identification products. Earlier, April 2025 witnessed International Paper completing its $9.9 billion acquisition of DS Smith, strengthening its sustainable paper packaging portfolio in Europe. Strategic collaborations include Mondi and Nestlé developing fully recyclable pet food pouches in October 2024, and Smurfit WestRock’s formation in November 2024, consolidating leadership in corrugated and cushioning materials.

Trends and Opportunities Defining the Future of the Packaging Materials Market

Legislative Mandates for Post-Consumer Recycled (PCR) Content

The packaging materials market is being fundamentally reshaped by stringent legislative mandates for recycled content. The European Union’s Single-Use Plastics Directive (SUPD) enforces minimum thresholds, requiring 25% recycled plastic in PET beverage bottles by 2025 and 30% by 2030, covering all single-use plastic bottles. These mandates are legally binding, making recycled polymers like rPET critical inputs across the supply chain. In the United States, state-level requirements are accelerating the same transition. California Assembly Bill 793 mandates 50% recycled content in plastic beverage containers by 2030, setting the benchmark for other states to follow.

Corporate leaders are aligning ahead of regulation. Unilever has pledged to halve virgin plastic use by 2026 and has already partnered with over 60 suppliers of recycled plastic to ensure quality and availability. Similarly, advanced recycling is becoming a cornerstone of supply resilience, with SABIC’s TRUCIRCLE portfolio producing virgin-equivalent polymers from mixed plastic waste. This not only supports regulatory compliance but also meets food-contact standards, which are critical for fast-moving consumer goods (FMCG) and healthcare packaging. Collectively, these developments establish PCR mandates as one of the most powerful and non-negotiable growth drivers in the global packaging materials market.

Strategic Material Substitution from Plastic to Fiber

A parallel transformation in the packaging materials industry is the rapid substitution of plastic with fiber-based materials. IKEA’s pledge to eliminate plastic packaging by 2028 highlights the scale of this shift, with the retailer already replacing 8,000 tons of EPS annually with molded paper and corrugated fiber. In e-commerce, Amazon India’s elimination of single-use plastic packaging and adoption of paper-based mailers and cushioning showcases how global leaders are pivoting toward sustainable fiber solutions to meet consumer and regulatory expectations.

Industry consolidation is amplifying this momentum. The 2025 merger of International Paper and DS Smith created one of the world’s largest fiber-focused packaging companies, explicitly targeting innovation in sustainable materials. Innovation is also strengthening fiber’s competitive edge, with academic research demonstrating bio-derived coatings that provide water, grease, and oxygen barriers—features that make paper viable for foodservice and perishable applications. This signals a strategic material shift where fiber-based solutions are no longer niche substitutes but core components of the packaging materials value chain, particularly in food, retail, and e-commerce segments.

Commercialization of High-Barrier, Fiber-Based Materials

The most immediate growth avenue for the packaging materials market is the commercialization of high-barrier fiber-based materials that maintain recyclability. Thin-layer barrier coatings such as SiOx (silicon oxide) and AlOx (aluminum oxide) enable paper packaging to resist oxygen and moisture without contaminating the recycling stream, making them attractive for snacks, dry foods, and household products. Chemical companies are forming partnerships to scale these solutions—Solenis joining the Dry Molded Fiber Network is a prime example of enabling coatings for recyclable, compostable packaging formats.

Academic research is solving key bottlenecks. Studies on PLA coatings combined with core-shell pigments demonstrate improved oxygen and moisture resistance, bringing fiber laminates closer to performance parity with plastics. Meanwhile, leading brands are already deploying these technologies. UPM Raflatac’s moisture-resistant paper labels with wash-off adhesives highlight real-world commercial applications that enhance recyclability while maintaining shelf performance. For the packaging industry, these breakthroughs represent an opportunity to scale fiber-based packaging beyond traditional applications, making it a cornerstone of sustainable material innovation.

Advanced Sorting and Recycling via Digital Watermarking

The integration of digital watermarking technology offers a transformative opportunity for intelligent recycling in the packaging materials market. The HolyGrail 2.0 initiative has demonstrated industrial-scale viability, achieving over 90% detection efficiency in German trials while sorting 56,000 packaging items daily. Crucially, the system achieved SKU-level sortation, distinguishing 5,949 unique product types and separating food-contact from non-food packaging—capabilities that existing NIR-based systems cannot match.

Corporate adoption is moving quickly. Procter & Gamble and Nestlé have piloted digitally watermarked packaging in European markets, signaling brand-level readiness for commercialization. Technology providers such as Digimarc are making it easier for recyclers to adopt this system by offering simplified licensing models and modular integration with existing sorting lines. Beyond improving recycling economics by producing higher-value PCR, digital watermarking creates a pathway for digital product passports, offering traceability, brand accountability, and compliance reporting under EPR frameworks. This opportunity positions watermarking as not just a recycling enabler but a strategic technology for circular economy alignment in packaging materials.

Competitive Landscape Dominated by Leaders Advancing Sustainable and High-Performance Packaging Materials

The Packaging Materials Market is shaped by key players leveraging materials science, technological innovation, and global scale to provide durable, sustainable, and high-performance packaging solutions.

Smurfit WestRock: Leading Paper-Based Packaging with Vertically Integrated Sustainability

Smurfit WestRock, formed in November 2024 from the merger of Smurfit Kappa and WestRock, is a global leader in paper-based packaging materials. Its vertically integrated operations ensure a consistent supply of high-quality containerboard, corrugated board, and paper-based bags. The company focuses on a circular business model, using renewable fiber to replace plastics while delivering cost-effective, sustainable packaging solutions for industrial and consumer applications.

Amcor PLC: Pioneering Sustainable Flexible and Rigid Materials with High Barrier Performance

Amcor, following its July 2025 combination with Berry Global Group, leads in flexible and rigid packaging materials. Its offerings, including mono-material PE films and AmLite Recyclable laminates, deliver high oxygen and moisture barrier performance while being recyclable. Amcor focuses on sustainable innovation and consumer-friendly solutions across food, beverage, and healthcare sectors.

International Paper Company: Expanding Fiber-Based Packaging Leadership through Strategic Acquisitions

International Paper completed its $9.9 billion acquisition of DS Smith in April 2025, significantly enhancing its European presence in sustainable paper-based materials. Its portfolio includes containerboard, corrugated board, and specialty paper packaging, with a strategic focus on innovation, operational excellence, and sustainable fiber-based solutions for a wide range of consumer goods.

Mondi Group: Advancing Eco-Friendly Laminates and Paper-Based Solutions for Consumer and Pet Food Packaging

Mondi Group invested €400 million in May 2025 in its Štětí mill and collaborated with Nestlé in October 2024 to develop fully recyclable pet food pouches, demonstrating leadership in sustainable laminates. Its offerings include flexible laminates, paper-based sacks, and corrugated boards, combining innovation with environmental responsibility to meet growing global demand for eco-friendly materials.

Huhtamaki Oyj: Leading Food Packaging Innovation with Sustainable Flexible and Paper-Based Materials

Huhtamaki, a global food packaging leader, launched paper-based flexible packaging for confectionery in Europe in November 2024. The company provides flexible, paper-based, and rigid materials with a strong emphasis on food safety, sustainability, and high-performance films. Huhtamaki is committed to making its products recyclable, compostable, or reusable by 2030, supporting the global shift toward circular packaging solutions.

Packaging Materials Market Share Insights, 2025-2034

Plastics Retain Largest Market Share by Material Type in the Packaging Materials Industry

Plastics account for the largest 40% share of the packaging materials market, reflecting their unmatched combination of lightweight properties, flexibility, barrier performance, and cost-efficiency across industries. Despite mounting regulatory and consumer scrutiny, plastics remain indispensable in high-volume applications such as flexible pouches, rigid bottles, and protective films, where durability and moisture resistance are critical. The segment’s resilience is sustained by rapid material innovation, including mono-material structures for recyclability, recycled-content grades like rPET and rPP, and bio-based polymers aimed at reducing environmental impact. Paper and paperboard are the fastest-growing challengers, propelled by e-commerce shipping boxes, molded pulp solutions, and fiber-based barriers that substitute for plastics. Metals and glass, while niche in share, retain entrenched roles in canned food, premium beverages, and pharmaceuticals due to their superior barrier properties, inertness, and recyclability. Meanwhile, wood and other specialty substrates, such as emerging biopolymers, remain confined to heavy-duty crates, luxury packaging, and pilot-scale sustainable alternatives, making plastics the versatile backbone of global packaging demand.

Food & Beverage Industry Commands Majority Market Share by End-Use in Packaging Materials

The food and beverage sector dominates with 60% of packaging materials demand, making it the single largest driver of the industry. This dominance stems from the enormous scale of processed foods, beverages, frozen meals, and fresh produce, which require packaging solutions spanning plastics for lightweight bottles and pouches, corrugated paperboard for cartons, metals for cans, and glass for premium or long-shelf-life items. Extended shelf-life requirements, stringent food safety regulations, and consumer demand for convenience and portion control amplify the sector’s reliance on innovative packaging. E-commerce has emerged as the second-largest driver, accelerating the use of corrugated paperboard and sustainable void-fill solutions. Pharmaceuticals and healthcare contribute a smaller but high-value share, demanding sterile blister packs, medical-grade vials, and specialized laminates. Personal care and cosmetics emphasize branding and sustainability, adopting glass, PCR plastics, and flexible refill pouches. Electronics packaging remains protection-focused, leveraging molded pulp, foams, and rigid paperboard to ensure safe transit. Yet, the food and beverage sector’s scale, combined with its pivotal role in sustainability and recyclability adoption, ensures its continued leadership in shaping packaging material innovation.

United States Packaging Materials Market Advanced by GS1 Sunrise 2027 and Federal R&D Programs

The United States packaging materials market is undergoing transformation due to the GS1 Sunrise 2027 initiative, which requires a shift to 2D barcodes and accelerates the adoption of smart packaging and RFID-enabled labels. This regulatory push is reinforced by state-level Extended Producer Responsibility (EPR) laws passed in Maine, Maryland, and Washington, which mandate the use of recyclable materials and higher post-consumer recycled (PCR) content. Together, these initiatives are reshaping how brands design packaging materials for compliance, traceability, and sustainability.

Federal programs are also playing a pivotal role. The National Advanced Packaging Manufacturing Program (NAPMP), part of the CHIPS for America Act, is investing up to $1.6 billion in semiconductor advanced packaging R&D, directly stimulating demand for high-tech precision packaging materials. On the corporate front, the US Flexible Film Initiative (USFFI) launched in August 2025 by General Mills, Mars, and PepsiCo is funding scalable recycling solutions for flexible packaging, highlighting industry momentum toward a circular economy. Key demand segments include e-commerce packaging and consumer packaged goods (CPG), where lightweight, durable, and recyclable materials are critical for safe transport and brand communication.

Germany Packaging Materials Market Driven by PPWR Compliance and Circular Economy Leadership

Germany’s packaging materials market is defined by strict regulatory oversight under the EU Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. The regulation sets ambitious targets for recyclability and mandates recycled content thresholds by 2030 and 2040, while restricting specific single-use plastics. Complementing this, the German Packaging Act (VerpackG) expanded in 2022, pushing companies to meet aggressive recycling targets for glass, plastics, and paper through improved recovery systems.

Germany also leads in technological innovation for sustainable materials. Advanced recycling and AI-enhanced optical sorting systems are being deployed to meet circular economy goals. With stricter transparency rules introduced in 2025, packaging must now disclose material composition and recyclability to reduce contamination in recycling streams. Key applications are concentrated in food, beverage, and cosmetics packaging, where the use of bioplastics, recycled paper, and renewable fibers aligns with both regulatory compliance and consumer preference for sustainable products.

China Packaging Materials Market Strengthened by Dual-Carbon Targets and New Labeling Standards

The packaging materials market in China is advancing rapidly under the government’s dual-carbon strategy, which targets carbon peaking by 2030 and neutrality by 2060. New express delivery regulations introduced in June 2025 require degradable and reusable materials, significantly impacting the design and adoption of packaging across logistics and e-commerce.

China is also tightening compliance with the GB 7718-2025 food labeling standard, effective March 2027, which mandates allergen disclosures, clearer date coding, and restrictions on misleading claims. This standard also allows digital labeling via QR codes, boosting demand for intelligent packaging materials. Manufacturers are investing heavily in automation, AI, and smart regulatory platforms to enhance traceability and food safety. The surge in consumer goods, electronics, and e-commerce shipments—175 billion parcels in 2024 is driving demand for durable, lightweight, and compliant packaging materials at a scale unmatched globally.

India Packaging Materials Market Expands with EPR Mandates and Circular Economy Initiatives

The Indian packaging materials market is experiencing accelerated growth under the government’s Make in India initiative and the Production Linked Incentive (PLI) scheme, which are fostering domestic manufacturing capabilities. New Extended Producer Responsibility (EPR) rules, requiring 30% recycled content in rigid plastics by April 2025, are pushing companies toward recyclable and circular packaging solutions.

Technological adoption is expanding, with greater integration of automation, robotics, and AI-driven packaging systems. Corporate initiatives such as the Huhtamaki Foundation’s “CloseTheLoop” program, which is setting up plastic recycling facilities, are critical for building India’s recycling infrastructure. Demand is strongest in the food and beverage sector, supported by the expansion of supermarkets and rapid online retail growth. Packaging materials that provide convenience, product safety, and brand differentiation are becoming indispensable to both multinational and domestic FMCG brands.

Japan Packaging Materials Market Evolving with Positive List Rules and Bio-Based Innovation

Japan’s packaging materials market is adapting to the positive list system for food-contact substances, introduced in June 2025. This regulation restricts the use of unapproved synthetic substances in packaging, compelling companies to develop compliant and safer food-grade materials. Alongside regulatory reform, Japan is advancing e-labeling solutions, supported by QR codes and digital traceability to enhance transparency for consumers and regulators.

Japanese companies are investing in bio-based and recyclable packaging innovations. For instance, Stora Enso’s paper-based barrier materials are gaining traction for use in fragile goods and thermal packaging of sensitive items. Sustainability targets—cutting GHG emissions by 46% by 2030 and reaching net zero by 2050—are driving the adoption of bio-PP and compostable packaging. Strong demand comes from the ready-to-drink tea, coffee, and snack segments, where consumers expect packaging that combines aesthetic appeal, durability, and eco-friendliness.

Packaging Materials Market Report Scope

Packaging Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$641.4 Billion

|

|

Market Size (2034)

|

$1003.6 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastics, Glass, Metal, Wood, Others), By Packaging Type (Rigid, Flexible, Semi-Rigid), By End-Use Industry (Food & Beverage, Consumer Electronics, Healthcare & Pharmaceutical, Personal Care & Cosmetics, E-commerce & Logistics, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Amcor plc, WestRock Company, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Ball Corporation, Crown Holdings Inc., Sealed Air Corporation, Huhtamaki Oyj, Berry Global Inc., Sonoco Products Company, Graphic Packaging Holding Company, Avery Dennison Corporation, Tetra Pak

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Materials Market Segmentation

By Material Type

- Paper & Paperboard

- Plastics

- Glass

- Metal

- Wood

- Others

By Packaging Type

- Rigid

- Flexible

- Semi-Rigid

By End-Use Industry

- Food & Beverage

- Consumer Electronics

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- E-commerce & Logistics

- Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Materials Market

- International Paper Company

- Amcor plc

- WestRock Company

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Huhtamaki Oyj

- Berry Global Inc.

- Sonoco Products Company

- Graphic Packaging Holding Company

- Avery Dennison Corporation

- Tetra Pak

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-dimensional research methodology to deliver an authoritative analysis of the Global Packaging Materials Market. Our approach integrates primary research through interviews with packaging material manufacturers, brand owners, suppliers, and end-users across food & beverage, healthcare, consumer electronics, personal care, and e-commerce sectors, alongside secondary research from company reports, regulatory publications, sustainability initiatives, and industry journals. Quantitative models are applied to forecast market growth from 2025 to 2034, examining material types, packaging formats, and end-use applications, while capturing innovations in high-barrier, fiber-based, bio-derived, and recyclable materials. We also analyze technological trends, including smart packaging, digital watermarking, RFID integration, and advanced coating solutions that enhance barrier performance and recyclability. Regional studies cover North America, Europe, China, India, and Japan, highlighting compliance with regulations such as Extended Producer Responsibility (EPR), SUPD, PPWR, GB 7718-2025, and local sustainability mandates. Competitive landscape analysis includes mergers, acquisitions, R&D initiatives, and strategic collaborations of leading players such as Smurfit WestRock, Amcor, International Paper, Mondi, and Huhtamaki. By combining regulatory, technological, and market dynamics, USDAnalytics provides industry professionals with actionable insights into sustainable innovation, digital integration, and material efficiency in the packaging materials sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.