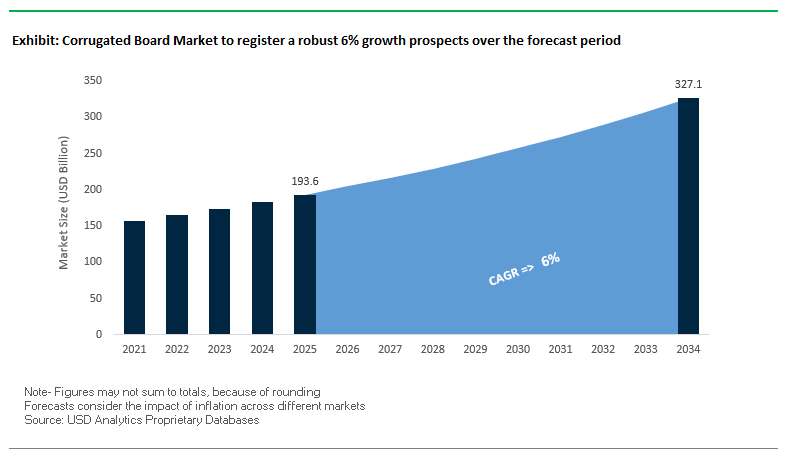

Market Overview: Global Corrugated Board Market Valued at $193.6 Billion in 2025

The Global Corrugated Board Market is valued at USD 193.6 billion in 2025 and projected to reach USD 327.1 billion by 2034, expanding at a CAGR of 6%. Corrugated board remains the foundation of global logistics and packaging, driven by the relentless expansion of e-commerce, heightened consumer demand for sustainable packaging, and regulatory pressure to cut plastic usage across supply chains.

The industry’s resilience stems from its recyclability, versatility, and cost efficiency. With recovery rates of old corrugated containers (OCC) exceeding 90% in some regions, corrugated packaging is among the most advanced examples of the circular economy. Lightweight corrugated formats and fit-to-product (FTP) packaging systems are reshaping e-commerce logistics by reducing void fill, cutting shipping costs, and enhancing efficiency.

Innovation is not confined to logistics. Digital printing on corrugated board has turned the traditional brown box into a high-value branding tool, enabling companies to deploy full-color, high-resolution graphics that elevate consumer engagement. Additionally, retail-ready packaging (RRP) is becoming a global standard, optimizing supply chain operations and improving on-shelf visibility for fast-moving consumer goods.

Key Insights for Industry Professionals:

- Market Size 2025: USD 193.6 Billion | 2034: USD 327.1 Billion | CAGR: 6%

- Circularity strength: OCC recovery rates exceed 90% in several global markets.

- E-commerce packaging: Lightweight and FTP systems reduce waste and costs.

- Digital printing growth: Corrugated evolving into a brand engagement platform.

- Retail-ready packaging: Enhancing shelf efficiency and shopper visibility.

- Plastic replacement: Corrugated expanding role as sustainable alternative.

Market Analysis: Recent Strategic Developments in Corrugated Board Industry

The corrugated board industry in 2025 is undergoing rapid change, with mergers, investments, and innovation initiatives reshaping competition and accelerating sustainability.

In August 2025, International Paper announced a transformative strategic shift, divesting its Global Cellulose Fibers business for $1.5 billion while investing $250 million in containerboard capacity in Alabama, underlining its focus on corrugated packaging. That same month, industry players highlighted the growing adoption of textured finishes and embossed patterns, mimicking premium materials to enhance unboxing experiences in e-commerce.

By July 2025, a major U.S. FMCG company transitioned to smart corrugated packaging with QR codes and NFC tags, enabling consumer interaction and traceability. Industry reports also highlighted a wave of smaller, high-value M&A activity in packaging, with private equity and strategic buyers targeting corrugated segments. In June 2025, a European firm launched water-resistant corrugated packaging for fresh food, addressing durability in moisture-heavy environments.

The focus on e-commerce efficiency is evident. In May 2025, publications highlighted the accelerating adoption of fit-to-product automated systems, enabling custom-sized boxes that reduce material usage and freight inefficiencies. Meanwhile, in March 2025, Saica Group announced a $110 million U.S. investment for a new corrugated board plant in Indiana, expanding North American capacity by over 110 million square meters annually.

Transformative Trends and High-Impact Opportunities Driving the Corrugated Board Market

Strategic Investment in Domestic Production Capacity

The corrugated board market is experiencing a pronounced shift toward domestic production expansion, fueled by supply chain vulnerabilities and rising e-commerce demand. Leading manufacturers are committing multi-billion-dollar capital expenditure programs to establish highly automated plants and expand existing facilities in key consumer markets. According to the Ministry of Micro, Small and Medium Enterprises (MSME), India’s import of corrugated paper and boxes totaled approximately ₹93 crore in 2019–20, highlighting the strategic imperative for domestic self-reliance under the Atmanirbhar Bharat initiative. Global consolidation efforts, exemplified by International Paper’s US$7.2 billion acquisition of DS Smith, underscore the industry’s focus on regional demand alignment, reducing logistical costs and lead times. Investments in automation, ranging from US$300,000 to US$800,000 for medium-sized plants, enable production of 5,000–10,000 boxes per day, enhancing efficiency and competitiveness. Furthermore, vertical integration strategies allow manufacturers to secure domestic recycled fiber supply, mitigating dependency on imports while addressing a market worth approximately ₹30,000 crore in India.

Accelerated Adoption of Automated, Right-Sized Packaging Solutions

Driven by the dual pressures of minimizing shipping costs and reducing packaging waste, brands and retailers are rapidly integrating automated, on-demand box-making systems. Case studies, such as Smurfit Westrock, show that right-sized packaging can reduce shipping costs by up to 68% compared to conventional boxes. Automated systems like Sparck Technologies’ CVP Impack and CVP Everest achieve production rates up to 1,100 custom boxes per hour seven times faster than manual packing addressing labor shortages and rising costs in e-commerce fulfillment. The adoption of solutions like the Box On Demand® system further eliminates the need for secondary packaging, reducing material usage and contributing to corporate sustainability goals, positioning automated, right-sized packaging as a critical efficiency and cost-saving trend in the industry.

Development of Performance-Enhanced Recyclable Coatings

A key opportunity lies in developing barrier coatings for corrugated board that are fully recyclable within standard paper recycling streams while providing superior resistance to grease, moisture, and oxygen. Cortec Corporation’s EcoShield® Barrier Coating demonstrates a fully repulpable, waterborne solution capable of replacing traditional polyethylene and wax coatings. FDA-compliant, recyclable coatings expand applications into frozen foods, poultry, and fresh produce packaging, enabling the replacement of non-recyclable alternatives and creating a significant growth avenue. Collaborative efforts from companies like Safepack Industries, developing single-material, cold-set glueable kraft liners, further demonstrate the market’s shift toward functional, sustainable packaging solutions aligned with circular economy principles.

Proliferation of Integrated Digital Printing for Short-Run Packaging

The rise of high-quality digital printing on corrugated board unlocks opportunities for SMEs and large brands seeking flexible, short-run, and personalized packaging solutions. Digital printing eliminates costly plates and setup times, allowing rapid design changes, as evidenced by Dusobox, making custom packaging economically feasible for smaller companies. Advanced single-pass and multi-pass presses enable high-resolution, full-color printing, supporting seasonal, regional, and targeted marketing campaigns without waste. Integration with real-time market data allows brands to adapt packaging dynamically, providing a competitive advantage over traditional analog methods. This trend is reshaping marketing strategies in the corrugated board sector, blending production efficiency with brand engagement and sustainability.

Competitive Landscape: Global Leaders in Corrugated Board Market

The Global Corrugated Board Market is led by multinational giants with integrated operations, sustainability agendas, and e-commerce-driven innovations. Scale, circularity, and digital adoption remain the key competitive differentiators.

Smurfit Kappa Group PLC: Strengthening Scale Through WestRock Merger

Smurfit Kappa, now aligned with WestRock, has become one of the largest corrugated packaging providers worldwide. Its strength lies in vertical integration across mills and converting plants, supported by innovation in POS displays and e-commerce-ready packaging. The merger enhances global reach and operational synergies, reinforcing Smurfit Kappa’s position as the front-runner in sustainable corrugated solutions.

International Paper Company: Refocusing on Core Corrugated Operations

International Paper, following its acquisition of DS Smith in early 2025, has cemented its position as a fiber-based packaging leader. With a broad manufacturing footprint, it has streamlined operations through divestiture of non-core cellulose fibers and significant investments in containerboard expansion. Its strategic focus is on cost leadership and sustainability, delivering a stronger customer value proposition in North America and Europe.

DS Smith PLC: Integrated Into International Paper’s Global Strategy

DS Smith, long recognized for retail-ready packaging and display innovations, officially merged with International Paper in January 2025. Its legacy expertise in supply chain efficiency and sustainable packaging design now strengthens International Paper’s corrugated portfolio. The integration enhances competitive positioning across both European retail channels and North American e-commerce markets.

Orora Limited: Diversifying Portfolio Through Strategic Acquisitions

Australia-based Orora continues to expand through acquisitions in beverage and glass packaging, complementing its corrugated operations. Its diversified portfolio ensures resilience, while its investments in automation and sustainability initiatives demonstrate a disciplined capital allocation strategy. Orora’s corrugated offerings serve multiple industries, with emphasis on tailored, eco-friendly solutions.

Saica Group: Expanding North American Footprint with Major U.S. Investment

Saica Group, a European leader in recycled paper and corrugated board, is extending its reach in North America. In March 2025, it announced a $110 million corrugated plant in Indiana, marking its second major U.S. investment. Saica’s competitive edge lies in circular economy leadership, leveraging high OCC recovery rates and eco-certified operations to deliver packaging with low environmental impact.

Corrugated Board Market Share Insights

Corrugated Boxes Command Market Share by Product Type in the Corrugated Board Industry

Corrugated boxes dominate with nearly 70% share of the corrugated board industry, making them the undisputed backbone of global logistics and commerce. The Regular Slotted Container (RSC) format leads due to its simple yet highly functional design that ensures stackability, structural integrity, and cost efficiency. Corrugated boxes are the default solution for shipping fast-moving consumer goods (FMCG), fresh produce, beverages, and e-commerce parcels. Their recyclability rate often exceeding 80% in developed markets aligns with regulatory mandates like the EU Packaging and Packaging Waste Regulation (PPWR), ensuring their long-term market stability. Global e-commerce alone consumes billions of corrugated boxes annually, pushing manufacturers to invest in high-speed digital printing for branding and right-sized box-making technology to reduce void space and optimize freight efficiency. This scale of integration across industries solidifies corrugated boxes as the industry’s volume leader.

Food and Beverages Retain the Largest Market Share by End-Use in the Corrugated Board Industry

The food and beverages sector secures approximately 30% of corrugated board demand, reflecting its role as the volume giant within the industry. From bulk distribution of fresh produce in ventilated boxes to beverage multipacks and shelf-ready displays in supermarkets, corrugated packaging is indispensable to maintaining product safety, freshness, and supply chain efficiency. Corrugated’s inert and safe material properties also make it suitable for direct food contact, reinforced by compliance with FDA, EFSA, and ISO food safety standards. In addition, corrugated packaging plays a critical role in cold chain logistics, supporting perishable goods such as dairy and frozen foods with moisture-resistant coatings. Global population growth, urbanization, and rising consumption of packaged foods continue to expand this segment, while sustainability mandates such as replacing plastics with recyclable corrugated trays further secure its dominance as the top end-use sector.

United States: Corrugated Board Market Expansion Fueled by Mergers, E-commerce, and Customization

The U.S. corrugated board market is witnessing significant consolidation, reshaping competitive dynamics and reinforcing the country’s dominance in global packaging. In January 2025, International Paper finalized its acquisition of DS Smith, creating a powerhouse in sustainable packaging solutions with strengthened presence across North America and Europe. This followed the 2024 Smurfit Kappa-WestRock merger, marking a wave of mega-deals that consolidate resources and enhance innovation in sustainable corrugated solutions. To strengthen infrastructure, International Paper also announced a $250 million investment at its Riverdale mill in Alabama, converting a machine to produce containerboard by 2026, aligning with the broader trend of capacity optimization and modernization.

E-commerce and direct-to-consumer (DTC) shipments, projected by the U.S. Department of Transportation to grow 35.1% between 2025 and 2050, remain a pivotal driver of demand. This surge is increasing the need for durable, lightweight, and recyclable corrugated packaging that can withstand long-distance logistics. The Inflation Reduction Act of 2022 provides additional incentives for manufacturers to integrate energy-efficient processes, further boosting sustainability efforts. At the same time, customization through digital printing technologies is enabling brands to enhance visibility and consumer engagement. Key industries such as processed foods, beverages, and automotive are increasingly relying on corrugated packaging for both protection and branding, cementing the U.S. as a frontrunner in innovation-driven growth.

Germany: Corrugated Board Market Driven by Circular Economy and Smart Packaging Innovation

Germany’s corrugated board industry is governed by stringent EU-level regulations, particularly the EU Packaging and Packaging Waste Regulation (PPWR) that came into effect in February 2025. This mandates that all packaging must be 100% recyclable by 2030, alongside minimum recycled content thresholds, pushing manufacturers to innovate with eco-friendly substrates like grass paper and high-strength recycled fibers. The country’s Verpackungsgesetz (Packaging Act) further supports the recycling loop, holding producers accountable for the life cycle of packaging and embedding circular economy practices across the value chain.

Technological innovation is at the forefront, with companies deploying smart packaging solutions such as embedded sensors for humidity and shock detection, and smart labels enabling real-time supply chain tracking. These features not only improve functionality but also reduce waste and product spoilage. Mergers and acquisitions also play a role, with Palm’s acquisition offer for five corrugated box plants in France, Spain, and Portugal reflecting Germany’s outward expansion strategy within Europe. With its strong recycling infrastructure and push toward intelligent packaging, Germany is solidifying its position as a leader in sustainable and tech-enabled corrugated board solutions.

China: Corrugated Board Market Transformation Under Dual Carbon Goals and Industry Consolidation

China’s corrugated board market is undergoing a major shift, aligned with the government’s dual carbon goals of carbon peak and carbon neutrality. National policies aimed at reducing non-degradable plastics are boosting demand for paper-based alternatives, positioning corrugated packaging as a preferred choice. The Made in China 2025 plan is further driving domestic innovation, with the objective of raising local content in high-tech manufacturing including corrugated board production to 70% by 2025.

On the technology front, Chinese manufacturers are rapidly integrating automation, AI, and “5G plus industrial internet” applications to improve flexibility and efficiency in corrugated board production. The boom in e-commerce giants like Alibaba and JD.com is another critical factor, creating massive demand for customizable and durable packaging. At the same time, stricter environmental regulations are leading to the closure of smaller, inefficient mills, consolidating production among larger, more sustainable players. This trend not only strengthens compliance but also enhances the competitiveness of China’s corrugated board exports in global markets.

India: Corrugated Board Market Growth Driven by Government Incentives and E-commerce Expansion

India’s corrugated board market is expanding rapidly, supported by government initiatives such as “Make in India” and “Zero Effect Zero Defect”, which encourage high-quality domestic manufacturing. The Production Linked Incentive (PLI) Scheme, with a budget of INR 10,900 crore for the food processing sector, is further fueling demand for standardized, high-quality packaging, creating ripple effects for corrugated board manufacturers. Additionally, regulatory reforms like the Plastic Waste Management (Amendment) Rules banning single-use plastics have created strong momentum for eco-friendly corrugated alternatives.

E-commerce growth, fueled by internet penetration and smartphone adoption, is transforming packaging requirements. Online retailers and logistics providers increasingly demand robust, recyclable, and tamper-evident corrugated boxes to support safe and efficient delivery. Beyond e-commerce, India’s pharmaceutical and healthcare sectors are becoming important growth drivers, requiring secure and protective corrugated packaging. Coupled with rapid urbanization and infrastructure expansion particularly IT parks and business hubs the demand for corrugated board in India is set to accelerate further, positioning the country as a high-growth market in Asia-Pacific.

Brazil: Corrugated Board Market Expansion Through Sustainability and Logistics Innovation

Brazil’s corrugated board market is evolving under the framework of the National Solid Waste Policy, which emphasizes circular economy principles and promotes durable, recyclable materials. Reinforcing these efforts, a 2025 law banning the import of solid waste, including plastics, has encouraged domestic recycling and packaging innovation, increasing the use of corrugated board as a sustainable alternative.

Technology is another growth driver, with Brazilian manufacturers deploying robotics and AI for quality control and efficiency improvements. Industry leader Klabin is spearheading product and logistics innovation, with the development of high-strength corrugated papers tailored for fruit exports requiring high humidity resistance, and a pioneering inland maritime shipping model that reduces dependency on land transport. These advancements not only improve efficiency but also reinforce sustainability by reducing carbon emissions. Together, regulatory backing and industry-led innovation are shaping Brazil into a key Latin American hub for corrugated packaging growth.

Japan: Corrugated Board Market Strengthened by Recycling Systems and Functional Innovation

Japan’s corrugated board market stands out for its highly structured recycling ecosystem under the Containers and Packaging Recycling Law, which assigns clear responsibilities to businesses in waste collection and repurposing. This has created one of the most advanced recycling systems globally, enabling continuous repurposing of corrugated packaging into new materials. Environmental regulations and consumer preferences further accelerate the shift toward recyclable and biodegradable corrugated packaging, positioning it as the sustainable choice across industries.

Technological innovation remains central, with Japanese manufacturers adopting lean production principles like 5S and Muda elimination to reduce waste and improve productivity. The rise of e-commerce in Japan has created additional demand for corrugated packaging, prompting the adoption of advanced digital printing for customization and branding. Moreover, Japan is at the forefront of functional innovation, developing corrugated products with high dimensional stability and resistance to deformation for demanding applications. This combination of sustainability, innovation, and efficiency continues to make Japan a global benchmark for corrugated board solutions.

Corrugated Board Market Report Scope

Corrugated Board Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$193.6 Billion

|

|

Market Size (2034)

|

$327.1 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Product Type (Corrugated Boxes, Corrugated Sheets, Die-Cut Boxes, Other Products), By Flute Type (Single-wall, Double-wall, Triple-wall), By Material (Virgin Kraft Paper, Recycled Corrugated Paper, Testliner, Semichemical Paper), By End-Use Industry (Food & Beverages, E-commerce & Retail, Electronics & Electrical Goods, Consumer Goods, Automotive, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, WestRock Company, Smurfit Kappa, Packaging Corporation of America (PCA), DS Smith Plc, Oji Holdings Corporation, Mondi Group, Nippon Paper Industries Co., Ltd., Rengo Co., Ltd., Shanying International Holdings Co., Ltd., Georgia-Pacific LLC, Pratt Industries, BillerudKorsnäs AB, VPK Group, Klabin S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Board Market Segmentation

By Product Type

- Corrugated Boxes

- Corrugated Sheets

- Die-Cut Boxes

- Other Products

By Flute Type

- Single-wall

- Double-wall

- Triple-wall

By Material

- Virgin Kraft Paper

- Recycled Corrugated Paper

- Testliner

- Semichemical Paper

By End-Use Industry

- Food & Beverages

- E-commerce & Retail

- Electronics & Electrical Goods

- Consumer Goods

- Automotive

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Board Market

- International Paper

- WestRock Company

- Smurfit Kappa

- Packaging Corporation of America (PCA)

- DS Smith Plc

- Oji Holdings Corporation

- Mondi Group

- Nippon Paper Industries Co., Ltd.

- Rengo Co., Ltd.

- Shanying International Holdings Co., Ltd.

- Georgia-Pacific LLC

- Pratt Industries

- BillerudKorsnäs AB

- VPK Group

- Klabin S.A.

* List Not Exhaustive

Methodology

The Corrugated Board Market analysis by USDAnalytics is developed through a comprehensive methodology combining both primary and secondary research, designed to provide actionable insights for industry professionals and decision-makers. Primary research involved direct engagement with leading corrugated board manufacturers, packaging solution providers, e-commerce logistics operators, and regulatory bodies across key markets including the U.S., Germany, China, India, Brazil, and Japan, providing first-hand data on production capacity, digital printing adoption, automated right-sized packaging systems, and sustainable coating innovations. Secondary research encompassed the study of company annual reports, government regulations, industry publications, trade shows, and market databases to validate emerging trends in circularity, e-commerce logistics, retail-ready packaging, and sustainability initiatives. USDAnalytics leveraged historical growth data (2015–2024), coupled with regional regulatory frameworks, technological advancements, and strategic investments, to project market growth to 2034. Advanced forecasting models and scenario analyses were applied to assess the impact of M&A activity, domestic production expansion, automation adoption, and environmental mandates on market dynamics, delivering precise, data-driven insights to guide stakeholders navigating the rapidly evolving global corrugated board industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.