Market Overview: Expanding Role of Recycled Fiber in Sustainable Packaging

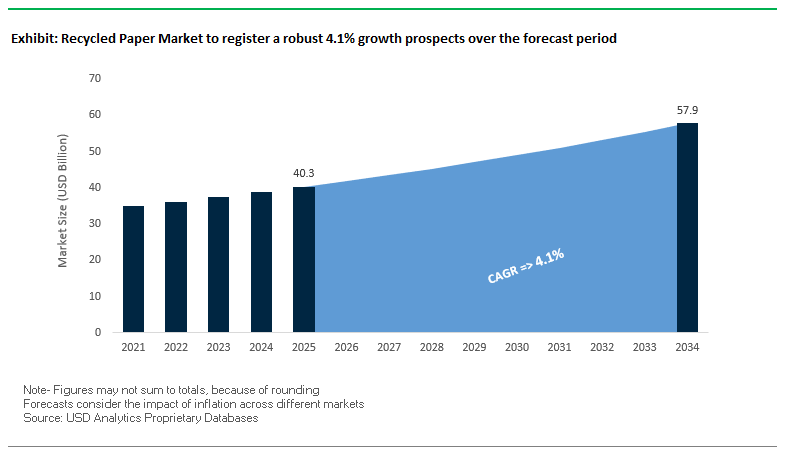

The global recycled paper market is forecasted to reach USD 40.3 billion in 2025 and expand to USD 57.9 billion by 2034, progressing at a CAGR of 4.1%. The industry is increasingly driven by circular economy principles, with recycled paper becoming a core material for packaging, publishing, and industrial applications. For industry professionals and buyers, the key questions revolve around supply chain reliability, recycled fiber integration, and the ability to replace virgin pulp while maintaining product performance.

In the United States, paper recycling rates remain among the highest globally, with paperboard recycling between 69% and 74% in 2024. Recycled fiber accounted for 44.4% of total fiber used by U.S. mills in 2024, up from 36.6% in 2005, reflecting the industry’s steady shift toward sustainability. Packaging continues to be the primary end-use segment, with over 68% of recycled paper consumed in corrugated boxes, molded pulp packaging, and e-commerce solutions. Furthermore, domestic consumption of recycled paper in U.S. mills rose by 1.29 million tons in 2024, a trend supported by reduced exports and investments in domestic recycling infrastructure.

Key Insights for Market Professionals:

- U.S. recycling rates exceed 60%, highlighting robust infrastructure.

- 44.4% of U.S. fiber use from recycled sources signals growing adoption.

- Packaging dominates with 68% share, especially corrugated boxes and molded pulp.

- Mill consumption increased by 32.7 million tons in 2024, supported by reshoring and reduced export dependence.

Market Analysis: Recycling Infrastructure, Mergers, and Fiber-Based Innovations

The recycled paper market is undergoing a period of consolidation and innovation, marked by mergers, facility expansions, and technological upgrades that are reshaping global supply chains. In August 2025, the American Forest & Paper Association (AF&PA) reported that U.S. mills consumed more recycled paper than in 2023 while exports decreased, demonstrating a clear trend toward domestic fiber circularity. In July 2025, Smurfit Westrock announced operational upgrades in North America, boosting its paperboard output and reinforcing recycled fiber use across packaging.

In June 2025, Ence secured environmental approval to build a new recycled fiber bioplant in Spain, adding to Europe’s processing capacity. Earlier, in March 2025, Mondi launched a functional barrier paper packaging solution for dry foods, a product designed to replace plastics and expand recycled paper’s role in sustainable food packaging. On the mergers and acquisitions front, International Paper and DS Smith shareholders approved a merger in January 2025, creating one of the world’s most influential players in fiber-based packaging.

Infrastructure improvements also continued in 2024. WestRock announced a closed-loop recycling system in November 2024, reinforcing sustainable fiber supply for its operations. DS Smith secured $34 million in October 2024 for capacity expansions at its Hungarian sites, while Smurfit Kappa’s acquisition of WestRock in June 2024 formed Smurfit Westrock, reshaping the competitive landscape.

Transformative Trends and Emerging Opportunities in the Recycled Paper Market

Mandated Corporate Procurement Driving Consistent Demand

The recycled paper market is undergoing a structural shift as demand is increasingly underpinned by mandated procurement rather than voluntary sustainability pledges. Governments and corporations alike are embedding minimum recycled-content requirements into their procurement strategies, creating a reliable baseline of demand. In the United States, the Environmental Protection Agency (EPA) has set specific guidelines mandating 30% post-consumer fiber for most printing and writing papers, and 40–60% for paper towels, ensuring institutional buyers contribute to a stable market. At the state level, California’s Senate Bill 1383 requires agencies to purchase recycled-content paper that is also recyclable, reinforcing a circular supply chain. These mandates extend into the private sector, where companies such as global CPG leaders and retailers are setting time-bound commitments to integrate recycled materials across packaging and office use. This creates a predictable and high-volume demand base, reducing market volatility and driving consistent growth for recycled paper producers.

Technological Advancements in Deinking and Fiber Quality

Innovation in recycling technology is enabling recycled paper to match or even surpass virgin fiber in certain applications. Deinking, historically a bottleneck in achieving high-quality output, is being transformed by enzymatic and chemi-enzymatic processes. Recent studies show that enzymatic deinking can reduce chemical consumption by up to 60% while maintaining comparable physical strength and brightness in final products, lowering both costs and environmental impact. High-yield deinking processes are improving fiber recovery rates, especially for difficult-to-recycle laser-printed materials, increasing the economic viability of post-consumer waste streams. At the same time, research into fiber strength enhancement is addressing the traditional weakness of recycled pulp. Chemical additives and mechanical refinements are improving fiber flexibility and cleanliness, which directly translates into better tensile strength and optical properties. These advances allow recycled fiber to expand into premium markets such as food-grade packaging and higher-quality printing, solidifying its position as a competitive alternative to virgin pulp.

Expansion into Molded Fiber Packaging for E-commerce

The explosive rise of e-commerce is creating a new high-margin pathway for recycled paper: molded fiber packaging. With global brands under pressure to eliminate EPS foam and plastic inserts, recycled paper is being channeled into molded pulp formats that provide both sustainability and superior product protection. Companies in the electronics, cosmetics, and glassware sectors are increasingly adopting molded pulp for protective inserts and trays, as it offers cushioning comparable to foam while being biodegradable and recyclable. This not only meets consumer expectations for sustainable packaging but also enhances the unboxing experience through custom-engineered designs tailored to product dimensions. The e-commerce sector, which faces mounting scrutiny for packaging waste, is driving demand for scalable alternatives. Recycled paper suppliers entering this segment can capitalize on significant volume demand while capturing higher value compared to traditional recycled paper applications like tissue or newsprint.

Strategic Positioning within the Bio-Circular Economy

Recycled paper mills are evolving into integrated bio-refineries, unlocking new revenue streams by valorizing their waste streams. Beyond producing recycled fiber, mills are capturing value from by-products such as sludge, wastewater, and lignin. Paper mill sludge, rich in cellulose, is being trialed for bioethanol production, creating synergies with renewable energy markets and aligning with circular economy goals. Biogas generation from wastewater treatment is enabling mills to become energy self-sufficient, with surplus bio-oil, biochar, and biogas sold into the market as renewable energy commodities. Additionally, waste outputs are being repurposed as agricultural amendments, providing sustainable alternatives to synthetic fertilizers while reducing landfill dependence. This transformation not only strengthens mills’ profitability but also positions the recycled paper industry as a critical enabler of the bio-circular economy, where materials are continuously looped across energy, agriculture, and packaging value chains.

Competitive Landscape: Global Leaders Driving Fiber Circularity

The global recycled paper industry is shaped by large multinational players with vertically integrated operations. These companies are leveraging mergers, acquisitions, and recycling investments to expand capacity and enhance sustainability credentials.

Smurfit Kappa Group plc: Circular Model Strengthened by WestRock Merger

Smurfit Kappa, through its 2024 merger with WestRock, now operates as Smurfit Westrock, a global powerhouse in fiber-based packaging. Its vertically integrated model—from recycled fiber collection to finished packaging—ensures supply security and high-quality output. The company’s circular business model allows it to consistently deliver sustainable solutions while meeting surging demand in both Europe and North America.

International Paper Company: Expanding Global Footprint Through DS Smith Merger

International Paper remains a leading producer of packaging, pulp, and paper, with recycled fiber as a core input. Its planned merger with DS Smith in January 2025 positions it as a stronger player in Europe, complementing its existing footprint. With a wide global customer base, International Paper focuses on sustainable packaging innovations and continues to invest in recycled fiber integration to reduce reliance on virgin pulp.

DS Smith plc: Scaling Fiber-Based Alternatives to Plastic

DS Smith has positioned itself as a leader in circular packaging, with products made from 100% recycled paper. The company approved a $34 million capacity expansion in Hungary in October 2024, strengthening its recycled packaging output. Its ambitious goal of replacing one billion units of plastic with fiber-based alternatives by 2025 underscores its role as a sustainability leader in the industry.

Sonoco Products Company: Vertical Integration in Paper Tubes and Cores

Sonoco is a major player in industrial and consumer packaging, with paper tubes and cores manufactured from 100% recycled paperboard. Its vertical integration, supported by in-house paperboard mills, ensures consistent raw material supply. In late 2024, Sonoco expanded its portfolio with the acquisition of Alucan, diversifying into sustainable aluminum packaging while reinforcing its leadership in recycled fiber-based solutions.

WestRock Company: Closed-Loop Recycling Enhancing Sustainability

WestRock, now part of Smurfit Westrock, remains a key consumer of recovered paper. Prior to its merger in 2024, it had launched a closed-loop recycling system, reinforcing its sustainable operations. Its strength lies in its broad manufacturing base and diverse recycled packaging portfolio, serving industries from corrugated to consumer goods. WestRock continues to prioritize sustainable packaging innovation and efficient fiber utilization within its expanded corporate structure.

Recycled Paper Market Share Insights

Corrugated Containers Dominate Recycled Paper Market Share by Product Type

Corrugated containers account for 55% of the recycled paper market in 2025, making them the single largest consumer of recovered fiber globally. This overwhelming share is driven by the explosive growth of e-commerce, which has multiplied the demand for shipping boxes across industries. Old Corrugated Containers (OCC) form the backbone of this segment, serving as the key input for containerboard production worldwide. Tissue paper follows at 25%, representing a high-value, consumer-centric segment that includes toilet paper, paper towels, and napkins—all marketed heavily on sustainability claims tied to recycled content. Newsprint and printing/writing paper, once pillars of recycled paper demand, are now in structural decline due to digital substitution, but they retain a small share for legacy needs such as newspapers, flyers, and office paper. Other products, including recycled fiber used in folding cartons, molded pulp, and specialty boards, reflect the versatility of recycled fiber in high-value, niche applications. The dominance of corrugated containers reflects how packaging, particularly in e-commerce and logistics, is the central engine of the recycled paper industry, while tissue paper adds resilience as an essential, everyday consumer good.

Packaging Industry Holds the Largest Share of Recycled Paper Market by End-Use

Packaging accounts for 70% of the recycled paper market in 2025, underscoring its role as the dominant end-use sector. Corrugated shipping boxes, folding cartons, and paper bags are the most visible outcomes of recycled fiber, tying this segment’s growth directly to e-commerce, retail logistics, and sustainability regulations mandating recycled content in packaging. Consumer goods follow at 15%, with demand anchored in tissue products—an everyday necessity in households, healthcare, and commercial environments, making it a stable, recession-resilient sector. Construction consumes a smaller but important share, with recycled fiber used in gypsum wallboard liners, roofing felts, and insulation, linking its demand to housing and infrastructure activity. Printing and publishing continues to decline, as digitization erodes demand for newsprint and office paper, though recycled fiber still finds niche use in books, magazines, and marketing materials. Other industries, including filters, specialty papers, and industrial applications, highlight recycled paper’s adaptability to engineered solutions. The overwhelming dominance of packaging demonstrates how the circular economy has cemented recycled fiber as an irreplaceable input in global trade and logistics, while consumer goods and construction diversify its downstream demand.

United States: Consumer and Corporate Sustainability Driving Recycled Paper Demand

The U.S. recycled paper market is experiencing substantial growth, fueled by evolving consumer and corporate preferences for sustainable products. Both individuals and businesses are prioritizing materials with lower environmental impact, driving adoption across packaging, printing, and industrial applications. Technological advancements, such as advanced recycling processes and modernization of paper mills, are enabling higher efficiency and improved product quality. The American Forest & Paper Association (AF&PA) reports over $4.5 million invested between 2019 and 2025 in new mills, equipment upgrades, and modernization projects, highlighting a strong industry commitment to sustainability.

The rapid expansion of e-commerce has created significant demand for corrugated boxes and fiber-based packaging, further boosting the use of recycled paper. Corporate initiatives from companies like Amazon, which has replaced all plastic air pillows with paper fillers in its global fulfillment centers, demonstrate a strong push toward eco-friendly packaging solutions. The U.S. Environmental Protection Agency (EPA) is actively promoting a circular economy with waste prevention, reuse, and recycling programs funded by the Infrastructure Investment and Jobs Act, reinforcing market growth for recycled paper products.

Germany: Circular Economy Leadership and Advanced Recycled Paper Technologies

Germany’s recycled paper market thrives under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which mandates high recyclability and eco-friendly packaging solutions. The country is a leader in the circular economy, with well-established systems for collecting, sorting, and processing waste paper. Manufacturers and end-users collaborate closely to develop high-quality recycled paper products, ensuring compliance with national and EU sustainability targets.

Technological innovation in Germany is enhancing production capabilities. Automated recycling facilities and advanced fiber recovery systems allow the creation of premium recycled paper suitable for food and beverage packaging. Governmental mandates under PPWR are driving companies to repurpose textile and industrial waste into new paper products, demonstrating a commitment to resource efficiency and sustainable production practices.

China: Industrial Expansion and E-commerce Propel Recycled Paper Market Growth

China’s recycled paper market is significantly influenced by governmental sustainability initiatives, particularly the dual carbon goals of carbon peak and carbon neutrality. These policies are transforming the paper and packaging industry, promoting eco-friendly production and increased use of recycled materials. Technological investments in automation, AI, and the integration of 5G with the industrial internet are improving efficiency, flexibility, and output quality across paper mills.

The e-commerce boom in Tier 2 and 3 cities has increased the demand for durable, secure, and tamper-proof recycled paper packaging. Additionally, China’s ban on unsorted solid waste imports has strengthened domestic sourcing, stimulating collection and processing of local recycled feedstock. By 2025, the inclusion of recycled paper in the national carbon trading market encourages manufacturers to monetize sustainability performance, aligning with green manufacturing and ESG compliance trends.

India: Government Initiatives and E-commerce Expansion Boost Recycled Paper Demand

India’s recycled paper market is growing rapidly due to governmental initiatives like Make in India and Zero Effect Zero Defect, which promote quality domestic production and sustainable industrial practices. Investments in infrastructure, including seven mega textile parks under the PM MITRA scheme, enhance industrial efficiency and capacity for producing recycled paper.

The surge in food processing and e-commerce sectors is driving demand for affordable, protective, and eco-friendly packaging solutions. GST reforms, reducing taxes on paper pulp molded trays to 5%, make products more cost-competitive and accessible. Manufacturers are also investing in new machinery and alternative raw materials, such as rice husk and bagasse, to produce recycled paper products. The Indian Paper Manufacturers Association (IPMA) is advocating for policy support to safeguard local producers against cheap imports, which could significantly influence the domestic market landscape.

Brazil: Regulatory Push and Strategic Investments Elevate Recycled Paper Production

Brazil’s recycled paper industry is benefiting from stringent legislation promoting circular economy practices, including the National Solid Waste Policy, which discourages single-use plastics. Strategic investments, such as Suzano’s $4 billion fossil-free pulp plant with an annual capacity of 2.55 million tons, provide a sustainable and stable supply of raw materials for recycled paper production.

Technological advancements, including AI and robotics for automated sorting and quality control, are enhancing production efficiency and accuracy. Additionally, the ban on solid waste imports effective January 2025 incentivizes domestic collection and processing, fostering sustainable waste management practices. These factors collectively position Brazil as a key player in the global recycled paper market, supporting both local and export-oriented industries.

Japan: Advanced Recycling and Bio-Based Innovations Strengthen Recycled Paper Market

Japan’s recycled paper market leverages advanced recycling systems under the Containers and Packaging Recycling Law, ensuring efficient collection and repurposing of waste paper and cardboard. The industry is increasingly incorporating bio-based materials, with innovations like Spiber’s Brewed Protein™ demonstrating the potential of microorganism-based sustainable materials.

Innovation in functionality is a hallmark of the Japanese market. Researchers at Yamagata University’s Innovation Center for Organic Electronics have developed printable, UV-densified barrier films with glass-like performance, offering applications in high-performance packaging for food and electronics. These developments highlight Japan’s leadership in sustainable, high-performance recycled paper products, integrating environmental responsibility with cutting-edge functionality.

Recycled Paper Market Report Scope

Recycled Paper Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$40.3 Billion

|

|

Market Size (2034)

|

$57.9 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Source (Post-Consumer Recovered Paper, Post-Industrial Recovered Paper), By Product Type (Corrugated Containers, Newsprint, Printing and Writing Paper, Tissue Paper, Other Products), By End-Use Industry (Packaging, Printing & Publishing, Construction, Consumer Goods, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, WestRock, Smurfit Kappa Group, DS Smith Plc, Nine Dragons Paper Holdings Limited, Oji Holdings Corporation, Mondi Group, Nippon Paper Industries Co., Ltd., Stora Enso Oyj, UPM-Kymmene Oyj, Asia Pulp & Paper (APP), Resolute Forest Products, Domtar Corporation, Suzano S.A., Graphic Packaging International

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Recycled Paper Market Segmentation

By Source

- Post-Consumer Recovered Paper

- Post-Industrial Recovered Paper

By Product Type

- Corrugated Containers

- Newsprint

- Printing and Writing Paper

- Tissue Paper

- Other Products

By End-Use Industry

- Packaging

- Printing & Publishing

- Construction

- Consumer Goods

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Recycled Paper Market

- International Paper

- WestRock

- Smurfit Kappa Group

- DS Smith Plc

- Nine Dragons Paper Holdings Limited

- Oji Holdings Corporation

- Mondi Group

- Nippon Paper Industries Co., Ltd.

- Stora Enso Oyj

- UPM-Kymmene Oyj

- Asia Pulp & Paper (APP)

- Resolute Forest Products

- Domtar Corporation

- Suzano S.A.

- Graphic Packaging International

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global recycled paper market, highlighting breakthroughs in high-yield deinking, fiber quality enhancement, and sustainable packaging solutions that are driving the transition from virgin pulp to recycled alternatives. The analysis reviews market dynamics across packaging, tissue, printing, and specialty applications, emphasizing the role of recycled fiber in e-commerce, industrial, and consumer goods sectors. It highlights emerging trends including corporate mandates for recycled content, technological innovations in enzymatic deinking, and expansion into molded fiber packaging for protective applications. This report is an essential resource for paper manufacturers, packaging suppliers, and sustainability professionals seeking actionable insights on supply chain optimization, circular economy integration, and high-value application opportunities. By incorporating historical data from 2021–2024 alongside forecasts through 2025–2034, and profiling 15+ leading global companies, it delivers a comprehensive overview of market structure, competitive positioning, capacity expansion, and regulatory influences shaping growth trajectories.

Scope Highlights:

- Segmentation: By Source (Post-Consumer Recovered Paper, Post-Industrial Recovered Paper), By Product Type (Corrugated Containers, Newsprint, Printing and Writing Paper, Tissue Paper, Other Products), By End-Use Industry (Packaging, Printing & Publishing, Construction, Consumer Goods, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ key players including International Paper, Smurfit Kappa Group, DS Smith Plc, WestRock, Nine Dragons Paper, Suzano S.A., and Mondi Group

Methodology

USDAnalytics conducted this study using a rigorous combination of primary and secondary research. Primary research included interviews with industry executives, packaging end-users, and recycling facility managers to capture market trends, regulatory impacts, and demand drivers. Secondary research analyzed corporate filings, annual reports, government statistics, trade publications, and scientific studies on recycled fiber technologies. Market sizing and forecasts were derived using historical consumption, production, and trade flow data, while scenario analysis assessed adoption trends in packaging, tissue, and molded fiber applications. Advanced modeling accounted for regional recycling infrastructure, technological investments, and corporate mandates, ensuring insights on competitive strategies, capacity expansions, and market opportunities. This comprehensive methodology enables industry professionals to make informed decisions based on reliable, data-driven intelligence.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.