Market Overview: Recycled Content and Thermoformed Growth Fuel Expansion

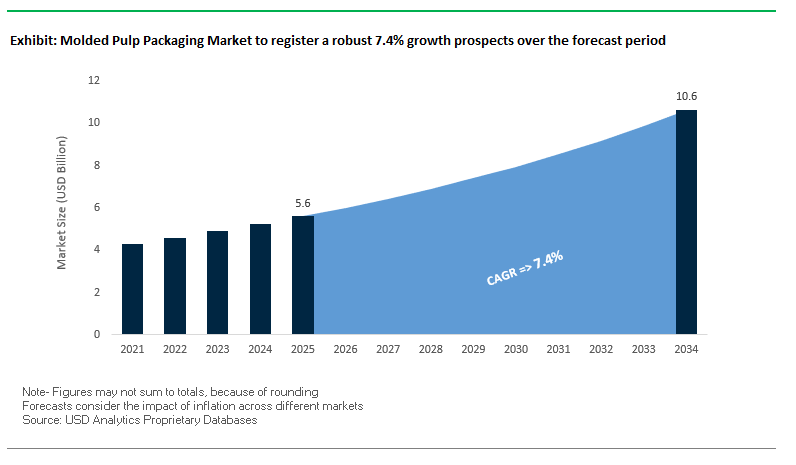

The global molded pulp packaging market is projected to reach USD 5.6 billion in 2025 and expand to USD 10.6 billion by 2034, advancing at a CAGR of 7.4%. Molded pulp packaging has positioned itself as one of the most sustainable and cost-efficient packaging formats, offering 100% recycled fiber-based solutions that fit seamlessly into the circular economy model. For industry professionals and buyers, the market addresses critical questions about material innovation, EPS replacement, and premium applications, while retaining its dominance in traditional end-use sectors like eggs and produce.

The industry is strongly driven by its ability to replace single-use plastics. Molded pulp solutions are widely adopted in egg packaging, where they deliver cushioning, breathability, and cost-effectiveness, maintaining a leading global market share. Thermoformed molded pulp is emerging as a premium growth area, offering higher smoothness, strength, and detailing suitable for electronics, medical devices, and high-value consumer goods. Meanwhile, e-commerce growth has created new demand for molded pulp protective packaging, especially for shipping fragile products.

Key Insights for Industry Professionals:

- 100% recycled content ensures molded pulp aligns with global sustainability regulations.

- Egg packaging dominates as the largest end-use, valued for safety and breathability.

- Thermoformed pulp supports premium, high-detail packaging for consumer electronics and medical devices.

- EPS foam replacement continues to expand adoption in protective and industrial packaging.

Market Analysis: Strategic Investments and Sustainability-Led Developments

The molded pulp packaging industry has seen rapid transformation through investments in recycled raw materials, advanced molding technologies, and sustainable alternatives to plastics. In August 2025, Greif unveiled its ModCan™ line, a sustainability-driven product with enhanced space efficiency that influences raw material dynamics in molded pulp and paper-based packaging. In July 2025, Smurfit Westrock announced operational improvements across North America, which will expand its recycled paper supply chain and strengthen its pulp-based packaging operations.

The sector is also being shaped by strategic consolidations and competitive material innovation. In May 2025, Packaging Corporation of America (PCA) acquired Greif’s containerboard business, reshaping supply for recycled paperboard, a critical input for molded pulp. Similarly, Mondi launched a paper-based functional barrier packaging solution in March 2025, creating cross-material competition with molded pulp for sustainable food packaging applications. Earlier, in June 2024, Corex Group received certification for 100% recycled fiber use, strengthening its positioning in the circular economy.

The market is also experiencing geographic and product portfolio expansions. In January 2025, Klabin launched the Wicket Paper Bag in Brazil, indirectly boosting demand for pulp cores and flexible film winding. Yazoo Mills invested $4 million in July 2024 in high-speed converting lines to strengthen production efficiency for pulp-based and paper cores.

Emerging Trends and Opportunities Transforming the Molded Pulp Packaging Market

Accelerated Corporate Adoption Driven by Specific Plastic Reduction Mandates

The molded pulp packaging market is experiencing rapid growth as corporations and governments align around aggressive plastic reduction mandates. Unlike consumer-driven eco-preferences, this momentum stems from hard deadlines set by global brands and reinforced by legislative pressure. Nestlé has publicly pledged to make 100% of its packaging recyclable or reusable by 2025, positioning molded pulp as a critical solution. Similarly, HP has integrated molded fiber packaging across multiple product lines, leveraging renewable and recycled fibers to strengthen its sustainability profile. Regulatory frameworks, particularly the European Union’s stringent packaging rules, are forcing companies to accelerate the phase-out of single-use plastics, thereby expanding demand for biodegradable molded fiber. Capital investment further underscores this shift; in August 2023, Valmet partnered with Naini Papers to deliver specialty paper technologies for sustainable packaging, highlighting how companies are scaling capacity in anticipation of demand surges. These combined corporate and legislative commitments are propelling molded pulp from niche applications to mainstream adoption, particularly in industries where plastic reduction has become a reputational and compliance necessity.

Product Diversification and Performance Enhancement Through R&D

Molded pulp packaging has evolved far beyond its legacy role in egg cartons and fruit trays. Today, significant research and development is unlocking complex, high-value applications that rival plastic in performance. Companies are transitioning from traditional transfer molding to thermoforming, enabling smoother surfaces, tighter dimensional tolerances, and customer-specific designs. For example, Aarhus University has piloted thermoformed molded pulp containers ranging from bowls to cups, signaling the technology’s scalability for diverse consumer needs. A global electronics brand’s collaboration with Sonoco exemplifies this shift: custom-engineered molded pulp inserts reduced material usage by 20% while improving global logistics efficiency. Additionally, the adoption of alternative raw materials such as sugarcane bagasse has yielded products with greaseproof and waterproof characteristics, ideal for food service. By enhancing protective strength, aesthetic appeal, and barrier performance, molded pulp is entering premium markets that previously relied heavily on plastics, further accelerating its role in the sustainability-driven packaging transformation.

Capitalizing on the Formal Electronics Packaging Segment

One of the most lucrative opportunities lies in molded pulp’s expansion into the formal electronics packaging segment. For decades, EPS foam has dominated as the cushioning material of choice, but sustainability regulations and consumer backlash against plastic waste are pushing electronics manufacturers toward molded pulp. Major players like Dell and Samsung have already adopted molded pulp for select product lines, validating its technical viability. Molded pulp offers static-neutral properties that safeguard sensitive electronics, while coatings enhance performance against static discharge. Furthermore, the technology offers significant cost advantages: Payr Engineering reports tool costs up to 50% lower than traditional options, enabling cost-efficient production even at smaller scales. This positions molded pulp as both an environmentally superior and economically viable solution. As electronics brands increasingly incorporate circular economy principles into their ESG frameworks, molded pulp will continue gaining traction as the preferred alternative to EPS and plastic inserts in protective packaging.

Expansion into New, High-Growth Application Verticals

Beyond electronics and food packaging, molded pulp is penetrating new high-value sectors such as healthcare, agriculture, and industrial packaging, presenting a “blue-ocean” growth opportunity. In healthcare, biodegradable molded pulp is being deployed in disposable medical products like kidney bowls, bedpans, and urinals, where compliance with sterility and disposal requirements is critical. In agriculture, growers are replacing plastic seedling trays and produce packaging with molded pulp, benefiting from its biodegradability and protective cushioning. Meanwhile, industrial players are adopting molded pulp for aerospace, automotive, and heavy machinery components, leveraging its shock absorption and design flexibility to protect high-value goods during transit. The ability to mold pulp into complex geometries while offering lightweight yet sturdy protection allows it to compete with plastics, foams, and even wood. With sustainability mandates tightening across these industries, molded pulp is emerging as a multipurpose material capable of addressing regulatory, operational, and environmental priorities simultaneously.

Competitive Landscape: Global Leaders Shaping Molded Pulp Packaging Innovation

The molded pulp packaging market is moderately consolidated, with key multinational players leveraging vertical integration, recycled raw materials, and thermoforming innovations to strengthen their competitive edge.

Huhtamaki Oyj: Global Leader in Fiber-Based Molded Pulp Solutions

Huhtamaki is a pioneer in molded pulp packaging, with operations spanning 12 plants in 10 countries. Its Fiber Packaging division produces egg cartons, trays for produce, and cup carriers, all made from 100% recycled pulp. Its strength lies in vertical integration and advanced technology, offering fully recyclable and compostable products. The company’s long-term strategy focuses on circular economy leadership, with innovations that protect food, people, and the environment.

Smurfit Kappa Group: Circular Economy Model Supporting Molded Pulp Packaging

Smurfit Kappa’s coreboard division supplies recycled raw materials that are essential for molded pulp applications. The company leverages its circular business model, integrating forestry, paper production, and packaging conversion, ensuring consistent supply and quality. In July 2025, operational improvements in North America underscored its commitment to strengthening pulp-based packaging. Its strategic focus remains on scaling sustainable fiber-based solutions across protective and food applications.

DS Smith plc: Replacing Plastics with Fiber-Based Alternatives

DS Smith has made sustainability a core business strategy, with a goal to replace one billion units of plastic by 2025. By 2023, it had already replaced over 762 million units, demonstrating clear progress. Although primarily a corrugated packaging leader, DS Smith’s fiber innovation pipeline directly supports molded pulp adoption. Its competitive strength lies in its integrated recycling operations, ensuring a consistent supply of high-quality paperboard for molded pulp and related products.

Pactiv Evergreen Inc.: PFAS-Free Molded Fiber Food Packaging

Pactiv Evergreen has emerged as a major innovator in the North American market with its EarthChoice® molded fiber line, including trays, containers, and plates. Its key differentiation is the development of PFAS-free molded fiber solutions, addressing regulatory and consumer concerns over harmful chemicals. The company’s products are widely used in food service—schools, restaurants, and catering—positioning it as a leader in sustainable food packaging applications.

Sonoco Products Company: Integrated Paper-Based Packaging Portfolio

Sonoco leverages its recycled paperboard mills to maintain reliable supply for its industrial and consumer packaging operations. While well-known for paper cores and tubes, its paper-based sustainable solutions portfolio positions it as a strong competitor in molded pulp and related packaging. In late 2024, Sonoco acquired Alucan to expand its aluminum packaging division but continues to optimize and diversify its paper packaging capabilities. Its integration model ensures quality control, supply consistency, and competitive cost advantages.

Molded Pulp Packaging Market Share Insights

Trays Dominate Molded Pulp Packaging Market Share by Product Type

Trays hold 35% of the molded pulp packaging market in 2025, making them the most widely adopted format due to their versatility and sheer volume demand. Their dominance stems from their multi-industry utility: from egg cartons and produce trays in food packaging to structural carriers in electronics and industrial shipping. Trays are particularly suited for automated high-volume packing lines, where uniformity and durability are critical, and their eco-friendly credentials align with global plastic reduction mandates. Clamshells follow as the second-largest category, directly replacing single-use plastics in consumer goods packaging, driven by legislation and brand sustainability commitments. End caps, though less visible to consumers, are indispensable in protecting industrial and automotive components during transit. Meanwhile, cups and bowls are surging in food service, powered by bans on polystyrene and single-use plastics, offering compostable solutions for restaurants and QSR chains. Other products, such as molded pulp lids and custom protective solutions, showcase innovation and the industry’s expansion into premium, high-margin niches. The dominance of trays underscores molded pulp’s role as a structural backbone in both consumer-facing and industrial packaging, while clamshells and food service formats illustrate its rapid rise as a plastic alternative.

Food Packaging Leads Molded Pulp Packaging Market Share by End-Use Industry

Food packaging represents 40% of the molded pulp packaging market in 2025, securing its place as the volume leader and the foundation of this industry. Egg cartons, produce trays, and protective carriers for grocery retail remain non-discretionary, high-volume applications that reinforce molded pulp’s market strength. This dominance is reinforced by consumer perception of molded pulp as a natural, sustainable, and food-safe material aligned with organic and fresh produce categories. Food service is the fastest-growing end-use, propelled by global legislation eliminating single-use plastics and accelerating adoption of molded pulp cups, bowls, and takeout containers by quick-service restaurants and cafes. Consumer electronics is emerging as a premium growth driver, with companies like Apple and Google using molded fiber for device accessories and retail packaging, enhancing both protection and brand image. Healthcare and medical devices represent a high-value niche, where molded pulp meets strict sterilization and sustainability needs, while industrial goods leverage molded pulp for cost-efficient, heavy-duty protection in transit. The dominance of food packaging highlights the sector’s irreplaceable role in global grocery logistics, while food service and electronics reflect how sustainability mandates and premium branding are expanding molded pulp’s applications.

United States: Sustainability and Technological Innovation Fuel Molded Pulp Packaging Demand

The U.S. molded pulp packaging market is witnessing rapid growth, driven by consumer preferences for sustainable and biodegradable solutions, particularly in the food service and e-commerce sectors. The shift away from single-use plastics is prompting companies to adopt eco-friendly packaging alternatives, with major players like Huhtamaki and Sabert Corp. expanding operations to produce recyclable and compostable molded pulp containers. Technological advancements, including advanced thermoforming and dry-formed fiber technologies, are enhancing production efficiency and minimizing waste. For example, PulPac’s Modula machine allows for rapid, low-waste manufacturing of molded fiber products, catering to the increasing demand for high-performance and eco-conscious packaging solutions.

Regulatory developments, such as Extended Producer Responsibility (EPR) laws in states like Maryland, are incentivizing brands to incorporate sustainable materials like molded pulp. Corporate initiatives by leading retailers and e-commerce giants, including Amazon’s replacement of plastic air pillows with paper fillers, are further accelerating adoption. This confluence of sustainability trends, technological innovation, and regulatory support positions the U.S. molded pulp packaging market for continued expansion, particularly in protective and consumer-facing applications.

Germany: Circular Economy Leadership and High-Performance Molded Pulp Solutions

Germany’s molded pulp packaging market is strongly shaped by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) 2025, which promotes eco-friendly and highly recyclable packaging. The country is a global leader in the circular economy, fostering close collaboration between manufacturers and end-users to develop molded pulp packaging designed for recyclability with high recycled content.

Technological innovation is driving product advancements, with companies developing barrier coatings for moisture and grease resistance, expanding applications in the food service and fresh food sectors. These innovations allow molded pulp packaging to compete effectively with plastics while meeting sustainability mandates. Germany’s emphasis on eco-compliant packaging and innovative material solutions reinforces its position as a hub for high-quality, environmentally responsible molded pulp products.

China: Industrial Growth and E-commerce Expansion Strengthen Molded Pulp Packaging Demand

China’s molded pulp packaging market is propelled by its rapid industrialization and manufacturing expansion, particularly in electronics and food sectors, which require durable protective packaging. The growing e-commerce market is a primary catalyst for demand, with molded pulp inserts and clamshells increasingly used to safeguard fragile goods during shipping.

Governmental sustainability initiatives aligned with the dual carbon goal are transforming the packaging industry. Chinese manufacturers are investing heavily in automation, AI integration, and advanced production technologies, enhancing both production efficiency and flexibility. Additionally, companies are diversifying applications, producing molded pulp wine holders, fruit trays, and even medical trays, reflecting the versatility and growing importance of molded pulp packaging across multiple sectors.

India: Government Incentives and Technological Investment Drive Market Expansion

India’s molded pulp packaging market is expanding in response to governmental sustainability initiatives and rapid growth in food processing and e-commerce sectors. Recent GST reforms reducing tax on paper pulp molded trays to 5% have lowered costs for consumers and increased the competitiveness of domestic businesses, particularly MSMEs.

Investments in new machinery and alternative raw materials, such as rice husk and bagasse, are improving production efficiency and product quality. The Make in India initiative encourages local manufacturing, reducing reliance on imports and boosting domestic production capacity. These trends are driving the adoption of molded pulp packaging for eggs, fruits, and other perishable items, emphasizing both eco-friendliness and functionality.

Brazil: Strategic Investments and Technological Advancements Accelerate Molded Pulp Growth

The Brazilian molded pulp packaging market is supported by regulatory initiatives promoting circular economy practices, particularly the National Solid Waste Policy, which discourages single-use plastics. Strategic investments, such as Suzano’s $4 billion fossil-free pulp plant with 2.55 million tons annual capacity, ensure a stable and sustainable raw material supply for the industry.

Technological integration, including robotics and AI for production efficiency and quality control, is enhancing operational sophistication. These advancements enable automated sorting, defect detection, and higher throughput, positioning Brazil as a key market for sustainable and high-performance molded pulp packaging solutions in Latin America.

Japan: Advanced Recycling and Bio-Based Materials Enable High-Performance Molded Pulp

Japan’s molded pulp packaging market leverages advanced recycling systems under the Containers and Packaging Recycling Law, ensuring efficient collection and repurposing of waste paper and cardboard for molded pulp production. The industry is also focusing on bio-based materials, utilizing renewable fibers to create sustainable packaging solutions.

Innovation in functionality is a hallmark of the Japanese market, with companies producing high-stability, deformation-resistant molded pulp products suitable for electronics and other high-value goods. These developments reflect Japan’s commitment to eco-conscious packaging innovation, integrating sustainability with high-performance application capabilities.

Molded Pulp Packaging Market Report Scope

Molded Pulp Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.6 Billion

|

|

Market Size (2034)

|

$10.6 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Product Type (Trays, Clamshells, Cups, Bowls, End Caps, Other Products), By Molded Type (Thick Wall, Transfer Molded, Thermoformed, Processed Pulp), By End-Use Industry (Food Packaging, Food Service, Consumer Electronics, Healthcare & Medical Devices, Industrial Goods, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Brodrene Hartmann A/S, Huhtamaki Oyj, Sonoco Products Company, UFP Technologies, Inc., Pactiv Evergreen Inc., Tekni-Plex, Inc., Sabert Corporation, James Cropper PLC, Sealed Air Corporation, Genpak, LLC, Eco-Products, Inc., CKF Inc., Visy, Zume, Inc., Pulpac

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Molded Pulp Packaging Market Segmentation

By Product Type

- Trays

- Clamshells

- Cups

- Bowls

- End Caps

- Other Products

By Molded Type

- Thick Wall

- Transfer Molded

- Thermoformed

- Processed Pulp

By End-Use Industry

- Food Packaging

- Food Service

- Consumer Electronics

- Healthcare & Medical Devices

- Industrial Goods

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Molded Pulp Packaging Market

- Brodrene Hartmann A/S

- Huhtamaki Oyj

- Sonoco Products Company

- UFP Technologies, Inc.

- Pactiv Evergreen Inc.

- Tekni-Plex, Inc.

- Sabert Corporation

- James Cropper PLC

- Sealed Air Corporation

- Genpak, LLC

- Eco-Products, Inc.

- CKF Inc.

- Visy

- Zume, Inc.

- Pulpac

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global molded pulp packaging market, analyzing breakthroughs in thermoformed pulp, high-performance fiber blends, and sustainable packaging innovations that are replacing single-use plastics across multiple industries. The analysis reviews market dynamics across food packaging, electronics, healthcare, and industrial applications, highlighting trends in corporate sustainability adoption, regulatory compliance, and premium product offerings. It highlights opportunities emerging from EPS foam replacement, advanced R&D in surface smoothness and barrier performance, and expansion into high-value applications such as electronics inserts and medical disposables. This report is an essential resource for packaging manufacturers, brand owners, and investors seeking actionable insights on product type innovations, molded processes, end-use adoption, and competitive strategies. By integrating historical data from 2021–2024 with forecasts through 2025–2034, and profiling 15+ leading companies, it provides a comprehensive view of production capacities, technological advancements, sustainability initiatives, and market growth potential.

Scope Highlights:

- Segmentation: By Product Type (Trays, Clamshells, Cups, Bowls, End Caps, Other Products), By Molded Type (Thick Wall, Transfer Molded, Thermoformed, Processed Pulp), By End-Use Industry (Food Packaging, Food Service, Consumer Electronics, Healthcare & Medical Devices, Industrial Goods, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies including Huhtamaki Oyj, Pactiv Evergreen Inc., Sonoco Products Company, Brodrene Hartmann A/S, and PulPac

Methodology

USDAnalytics employed a comprehensive research methodology combining primary interviews with manufacturers, brand owners, and distributors, along with secondary research from corporate reports, trade publications, and regulatory filings. Market sizing and forecasts were developed using historical production, consumption, and trade data, alongside analysis of material adoption trends and industry-specific regulatory influences. Qualitative insights focused on technological advancements such as thermoforming, transfer molding, and thick-wall pulp innovations, while quantitative evaluation assessed production capacity, market share, and growth potential of leading global players. Regional studies incorporated regulatory frameworks, sustainability mandates, and consumer trends to identify opportunities in high-value segments such as electronics, medical devices, and premium food packaging. This integrated approach ensures industry professionals gain actionable intelligence on market expansion, operational efficiencies, and competitive strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.