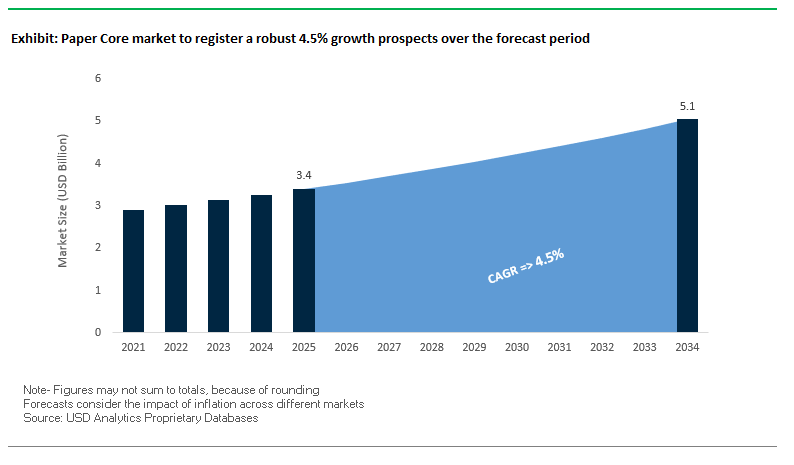

Market Overview: Paper Core Market Poised to Reach $5.1 Billion by 2034 Driven by Sustainability and Industrial Demand

Market Value (MV) 2025: $3.4 billion │ 2034: $5.1 billion │ CAGR (2025–2034): 4.5%

The global paper core market is undergoing a steady transformation as sustainability imperatives, technological innovation, and broad industrial applications converge to reshape growth trajectories. For packaging decision-makers and buyers, the critical questions are: How quickly can paper cores transition to 100% recycled inputs without compromising performance? Which technological advancements ensure efficiency for high-speed winding systems? And how does e-commerce acceleration amplify core demand across flexible packaging and labeling industries? Industry leaders are already answering these questions with heavy investments in automation, design engineering, and supply chain resiliency.

Key Insights for Executives:

- Sustainability as a core growth driver: Global focus on circular economies accelerates the adoption of 100% recycled paperboard for core manufacturing.

- Automation improves precision: Next-gen machinery enables high-strength, dimensionally accurate cores for modern high-speed winders.

- Versatility across industries: Paper cores serve printing, textiles, films, tapes, and construction, reinforcing their role as critical industrial components.

- E-commerce strengthens demand: Roll-based goods like flexible films, adhesive labels, and tapes require reliable cores for transit and storage integrity.

Market Analysis: M&A Wave, Strategic Investments, and Shifting Portfolios Define Growth

The paper core industry is deeply influenced by the broader consolidation wave sweeping through global paper and packaging. In April 2024, International Paper announced its landmark $7.2 billion acquisition of DS Smith, surpassing Mondi’s competing bid. The combined entity now operates with $28 billion+ pro forma sales, strengthening vertical integration across fiber resources and paper-based packaging. Similarly, in July 2024, the Smurfit Kappa–WestRock merger created Smurfit WestRock, with a clear focus on global leadership in sustainable packaging, signaling strong demand for circular, fiber-based solutions that underpin core demand.

Diversification and divestments are also reshaping strategies. Pactiv Evergreen’s sale of two facilities in July 2024 for $110 million to Suzano highlights a broader focus on optimizing operations. Meanwhile, Clearwater Paper’s $1 billion divestiture of its tissue business in July 2024 pivots its portfolio toward paperboard. Ball Corporation, after divesting its aerospace unit for $5.6 billion in February 2024, is now fully packaging-focused, freeing capital for future expansion and technology upgrades.

On the investment side, Sonoco’s $30 million capacity expansion (July 2025) targets the adhesives and sealants segment, signaling growing specialization within industrial cores. Veritiv’s acquisition of Orora Packaging Solutions (September 2024) further strengthens its specialty packaging portfolio, offering downstream synergies.

Trends and Opportunities Reshaping the Paper Core Market

Strategic Investment in High-Performance, Specialized Paper Cores for Industrial Applications

The paper core market is shifting from commoditized, standard products to high-value engineered cores tailored for demanding applications in composites, films, textiles, and flexible packaging. Manufacturers are investing heavily in advanced machinery, adhesive technologies, and precision engineering to deliver products with superior crush resistance, dimensional stability, and surface smoothness.

High-performance cores are designed with tailored ply counts ranging from 3 to over 50 layers combined with advanced adhesives and winding techniques (spiral vs. convolute) to meet application-specific requirements. For instance, in flexible packaging film production, cores must deliver flawless smoothness, straightness, and roundness to ensure defect-free winding at high speeds, making precision engineering critical. Capital investments underline this trend, as seen with Andhra Paper’s investment in upgraded paper-making machinery, which boosts production capacity for high-strength paper grades suitable for industrial cores. This transition highlights how the market is aligning with the stringent requirements of high-value manufacturing sectors.

Accelerated Adoption of 100% Recycled Content and Enhanced Recyclability

Sustainability is becoming a non-negotiable driver in the paper core industry, with companies transitioning to 100% recycled paperboard and innovating new adhesive systems that support full recyclability. Corporate sustainability pledges and regulatory mandates like the EU’s Packaging and Packaging Waste Regulation (PPWR) are accelerating the push toward circularity.

Paper cores, already sustainable by nature, are evolving further with the use of post-consumer recycled fibers and water-soluble adhesives that allow full fiber recovery during recycling. By addressing the adhesive challenge traditionally a barrier to recyclability manufacturers are ensuring that cores do not contaminate recycling streams. Additionally, state-level mandates in the U.S., such as Washington’s PCR laws, reinforce the urgency for producers to integrate higher recycled content. This trend not only supports corporate ESG targets but also enhances the industry’s alignment with circular economy frameworks, positioning paper cores as a preferred sustainable alternative to plastic or composite cores.

Development of Integrated RFID and Smart Core Solutions for Supply Chain Visibility

A significant opportunity lies in transforming paper cores from passive structural components into smart, data-enabled assets. By embedding RFID tags or IoT sensors directly into the core structure, manufacturers can enable real-time tracking, inventory management, and anti-counterfeiting solutions.

Smart paper cores allow for non-line-of-sight inventory tracking, which can streamline inbound and outbound logistics, enhance warehouse automation, and provide full supply chain transparency. In industries handling high-value materials like specialty textiles or composite films, RFID-enabled cores serve as unique identifiers, creating an auditable chain of custody and protecting against counterfeiting. Beyond authentication, data captured from RFID-enabled cores such as production date, roll usage, and unwinding details can be used to optimize manufacturing schedules and improve operational efficiency. This opportunity positions paper cores as an integral part of Industry 4.0-enabled supply chains, moving well beyond their traditional role.

Expansion into New Markets with Bio-Based and Home-Compostable Cores

The growing demand for eco-friendly and consumer-facing solutions is opening new markets for bio-based and home-compostable paper cores. Unlike industrial applications, where strength is paramount, consumer products such as toilet paper, paper towels, and kitchen rolls allow for thinner, lighter cores. This creates an opportunity to introduce bio-based materials like bamboo, rice straw, and bagasse, which reduce reliance on conventional wood pulp.

Several companies and research initiatives are already exploring the use of agricultural residues to create packaging-grade paper, offering a sustainable raw material alternative. Additionally, achieving home-compostable certifications provides third-party verification and boosts consumer trust critical in sustainability-driven markets. For eco-conscious consumers, compostable cores eliminate the recycling burden and offer a zero-waste disposal option, making them highly attractive in both developed and emerging markets. This shift enables paper core manufacturers to diversify their product portfolios and tap into the rapidly expanding green consumer economy.

Competitive Landscape: Leaders Advance Sustainability, Precision, and Customization

The global paper core market features a mix of multinational packaging leaders and specialized manufacturers. Competition hinges on sustainability credentials, innovation in tube geometry and strength, precision for automated winding, and tailored solutions for diverse end markets.

Sonoco Products Company Expanding with Strategic $30M Investment

Sonoco remains one of the most influential names in industrial paper products, producing tubes, cores, and yarn carriers for high-speed textile winders. In July 2025, the company announced a $30 million capacity expansion targeting adhesives and sealants applications, adding 100 million+ units annually. Its Hi-Radius tube innovation, which minimizes yarn breakage, highlights its commitment to performance-driven design. Built on recyclable paperboard, Sonoco’s solutions align with its broader sustainability lifecycle model from raw material to end-of-life.

Smurfit Kappa Group Scaling Circular Economy Through M&A

Smurfit Kappa, now part of Smurfit WestRock after the July 2024 merger, produces 23 million tons of paper annually and integrates 14 million tons of recovered fiber into its production cycle. While known for corrugated packaging, the company also manufactures composite cardboard tubes that serve industrial roll goods markets. Its business model exemplifies the circular economy, with recycling operations feeding back into production, strengthening its leadership in fiber-based industrial packaging.

Corex Group Precision-Engineered Cores for High-Performance Applications

Corex Group specializes in paper cores, tubes, and edge protectors, offering dimensionally precise products for industries like films, foils, and tapes. Its global presence allows it to serve niche industrial markets with customer-tailored designs that prevent tension spikes and ensure winding efficiency. Corex’s ongoing R&D into new surface technologies enhances grip and material protection, positioning it as a preferred partner for industries relying on automated high-speed winding.

Caraustar Industries, Inc. Recycling-Integrated Tube and Core Production

Caraustar operates across Industrial Products, Paperboard Mills, CPG, and Recycling, with integration that supports end-to-end lifecycle management. Its industrial tubes and cores cater to textiles, nonwovens, and carpets, with production exceeding 1 million tons annually in North America. Manufacturing exclusively from 100% recycled paperboard, Caraustar reinforces its environmental commitment while offering a vast portfolio with diameters from 0.75” to 60”. This vertical integration allows for cost stability and resource efficiency across product lines.

Yuanlong Paper Products Co., Ltd. International Expansion and Diversified Growth

Yuanlong leverages both industrial and financial investment strategies to expand its packaging portfolio. A notable example is its acquisition of Ardagh’s Australian and New Zealand packaging units, now rebranded as Jamestrong Australasia Holdings, reflecting its internationalization strategy. By continuously incubating businesses across the financial and industrial value chain, Yuanlong supports innovation and integration. Its dual-focus model allows it to pursue global expansion and product diversification while investing in eco-friendly paper solutions.

Paper Core Market Share Insights

Core Tubes Dominate Market Share by Product Type in Paper Core Packaging

Core tubes represent 75% of the global paper core market in 2025, reflecting their status as the universal industrial workhorse. Their cylindrical geometry provides exceptional strength and roll integrity, making them indispensable for winding and unwinding applications across the paper, film, textile, and converting industries. The scale of demand is immense, as nearly every roll of paper, packaging film, or textile product depends on paper cores for processing and transport. Core board, by contrast, holds a smaller but stable share, serving niche structural applications such as furniture components, insulation substrates, and composite packaging formats. Its growth is constrained by its narrower industrial use cases, but its role is vital in supporting construction and specialized packaging innovations. The segmentation underscores how core tubes anchor the industry through high-volume industrial use, while core board sustains specialized structural demand in construction and niche applications.

Paper & Pulp Industry Anchors Market Share by End-Use in Paper Core Packaging

The paper and pulp sector holds 30% of the global paper core market in 2025, making it the single largest end-use industry. This dominance is inherently self-reinforcing, as the paper industry consumes massive volumes of cores to process, transport, and distribute its own rolls of newsprint, packaging grades, and specialty papers. Packaging follows closely with 25%, driven by the relentless expansion of flexible packaging, laminates, foils, and label stock all of which require precise winding and unwinding processes on cores. The textile industry remains a traditional and steady consumer, relying on engineered cores to handle yarns and fabrics under high-speed mechanical stress. Construction applications, though smaller, leverage high-strength cores and core boards for concrete casting, industrial tapes, and structural composites. Food and beverage, along with consumer goods, represent direct and indirect consumption, ranging from household aluminum foil rolls to consumer-facing products like tapes and wrapping paper. Collectively, these end-use patterns show how paper and pulp sustains leadership, packaging fuels modern growth, and textiles and construction anchor stable, specialized demand.

United States: E-commerce Expansion and Sustainable Innovation Driving Paper Core Demand

The U.S. paper core market is closely tied to the country’s booming e-commerce and logistics sectors, which drive demand for durable and lightweight cores for winding packaging paper, films, and other materials. Sustainability is a major industry trend, with manufacturers focusing on producing cores from 100% recycled paper while improving water and energy efficiency across production lines. The market is also witnessing significant automation and technological innovation, with AI and IoT systems being adopted to enhance production efficiency and cutting precision. Additionally, regulatory compliance is shaping operations, as the Environmental Protection Agency (EPA) has updated guidelines for emissions and wastewater management, prompting investments in cleaner and more environmentally friendly production technologies.

Germany: Circular Economy Leadership and Regulatory Framework Supporting Sustainable Paper Cores

Germany’s paper core industry operates under a strict regulatory framework, including the German Packaging Act (VerpackG) and the EU Packaging and Packaging Waste Regulation (PPWR), creating strong demand for eco-friendly and recyclable paper core products. Germany’s emphasis on the circular economy drives manufacturers to develop cores with high recycled content and full recyclability, aligning with national and EU sustainability targets. Technological advancements in recycling processes, such as optical sorting, allow efficient handling of paper materials at scale, ensuring compliance with stringent material-specific recycling quotas and reducing environmental impact.

China: Rapid Capacity Expansion and Sustainability Initiatives Boost Paper Core Production

China’s paper core market is benefitting from rapid capacity expansion in the paper and paperboard industry. Projects like Nine Dragons Paper’s 6-billion-yuan pulp-paper integrated intelligent factory in Chongqing are securing a self-sufficient raw material supply, driving increased demand for paper cores. Government initiatives promoting a green transformation in express delivery and packaging are encouraging companies to adopt eco-friendly and reusable cores, positioning paper cores as a sustainable alternative to plastic. A robust export market for packaged goods further incentivizes manufacturers to produce high-quality paper cores that meet international standards, while innovations in design and materials help the industry remain competitive globally.

India: Strategic Investments and E-commerce Growth Accelerating Paper Core Market Expansion

India’s paper core industry is experiencing growth through strategic investments, such as Andhra Paper upgrading its Paper Machine-3 to increase production by 60 tons per annum, addressing rising domestic demand. The rapid growth of e-commerce, particularly in corrugated packaging, is a major catalyst for the paper core market, as cores are critical for winding packaging materials. Sustainability trends, driven by India’s Plastic Waste Management Amendment Rules, are creating strong demand for paper-based alternatives, while the expansion of manufacturing industries such as textiles, adhesives, and paper products further fuels the need for reliable paper cores.

Brazil: Virgin Pulp Leadership and Technological Innovation Supporting Paper Core Industry

Brazil is a global leader in high-quality virgin pulp production, providing a vital raw material for the paper core market. The country’s favorable climate, research investments, and advanced forestry practices make it a benchmark for pulp quality and sustainability. Leading companies like Suzano Papel e Celulose are implementing blockchain solutions to optimize supply chain traceability, compliance documentation, and geolocation data management. Regulatory compliance, including alignment with the EU’s deforestation regulation, is driving further innovation and investment in transparent and sustainable production practices, ensuring the Brazilian paper core industry remains competitive and environmentally responsible.

Japan: Advanced Recycling Systems and Material Innovation Driving Sustainable Paper Cores

Japan’s paper core market benefits from one of the world’s highest waste paper collection and utilization rates, providing a strong foundation for producing cores from recycled materials. Companies such as Oji Holdings have introduced initiatives like Renewa, focusing on recycling difficult-to-process materials, including liquid paper packages, into new products like corrugated boxes and paper hand towels. The Japanese government’s commitment to recycling and resource circulation supports sustainable practices, creating a favorable environment for paper core production. Innovation in materials and processes ensures that cores meet the needs of a wide range of end-use industries while maintaining environmental responsibility.

Paper Core Market Report Scope

Paper Core market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$5.1 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Type (Core Board, Core Tube), By Diameter (Less than 10 mm, 10 mm to 50 mm, 51 mm to 100 mm, 101 mm to 200 mm, More than 200 mm), By End-Use Industry (Paper & Pulp, Textile, Construction, Packaging, Consumer Goods, Food & Beverage, Other End-Use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sonoco Products Company, Smurfit Kappa Group plc, Konica Minolta, Inc., Oji Holdings Corporation, International Paper, Corex Group, The Corrugated Company, Kunert Group, Vayhan Paper & Boards, Star Paper Mills Limited, Purbanchal Paper Mills Ltd., Paper Tubes & Cores, Inc., Industrial Paper Corporation, Paper Tube Company, Pacific Paper Cores

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Core Market Segmentation

By Product Type

By Diameter

- Less than 10 mm

- 10 mm to 50 mm

- 51 mm to 100 mm

- 101 mm to 200 mm

- More than 200 mm

By End-Use Industry

- Paper & Pulp

- Textile

- Construction

- Packaging

- Consumer Goods

- Food & Beverage

- Other End-Use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Core Market

- Sonoco Products Company

- Smurfit Kappa Group plc

- Konica Minolta, Inc.

- Oji Holdings Corporation

- International Paper

- Corex Group

- The Corrugated Company

- Kunert Group

- Vayhan Paper & Boards

- Star Paper Mills Limited

- Purbanchal Paper Mills Ltd.

- Paper Tubes & Cores, Inc.

- Industrial Paper Corporation

- Paper Tube Company

- Pacific Paper Cores

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global paper core market with a focus on sustainability-driven innovations, industrial applications, and technological advancements shaping the sector between 2021 and 2034. The study highlights key breakthroughs in high-performance cores, automation, recycled content adoption, and smart core solutions for supply chain visibility, providing in-depth insights for investors, operations managers, and packaging decision-makers. Analysis reviews the evolution of demand across diverse end-use industries such as paper & pulp, packaging, textiles, construction, and consumer goods, emphasizing the strategic impact of mergers, capacity expansions, and precision-engineered product portfolios. The report also examines market dynamics, competitive positioning, and technological trends, including RFID integration, bio-based cores, and home-compostable solutions, to identify opportunities that align with circular economy goals. This report is an essential resource for executives seeking to understand market drivers, anticipate regulatory impacts, benchmark competitor strategies, and optimize fiber-based investments. USDAnalytics further provides actionable insights into growth forecasts, enabling stakeholders to prioritize capital expenditure, expand production capabilities, and implement sustainable practices across global operations.

Scope Highlights

- Segmentation: By Product Type (Core Board, Core Tube), By Diameter (Less than 10 mm, 10 mm to 50 mm, 51 mm to 100 mm, 101 mm to 200 mm, More than 200 mm), By End-Use Industry (Paper & Pulp, Textile, Construction, Packaging, Consumer Goods, Food & Beverage, Other End-Use Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic Data: 2021–2024

- Forecast Data: 2025–2034

- Companies Covered: Analysis/profiles of 15+ key players including Sonoco Products Company, Smurfit Kappa Group plc, Oji Holdings Corporation, International Paper, Corex Group, and others

Methodology

The research methodology integrates both primary and secondary data sources to ensure robust and actionable market intelligence. Primary research involved in-depth interviews with senior executives, plant managers, and product development specialists across the paper core value chain, capturing first-hand insights on technological advancements, production efficiency, and sustainability initiatives. Secondary research encompassed financial reports, industry journals, company filings, regulatory frameworks, and trade databases to validate historical trends and market forecasts. Quantitative modeling was applied to project market size, growth rates, and adoption trends for various product types, diameters, and end-use industries, while qualitative assessments evaluated competitive strategies, mergers, acquisitions, and innovation trajectories. The analysis also incorporates scenario planning to account for regulatory shifts, supply chain dynamics, and macroeconomic influences, delivering a comprehensive view of opportunities and challenges in the paper core market for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.