Composite Packaging Market Overview: Expansion Toward $136.9 Billion by 2034

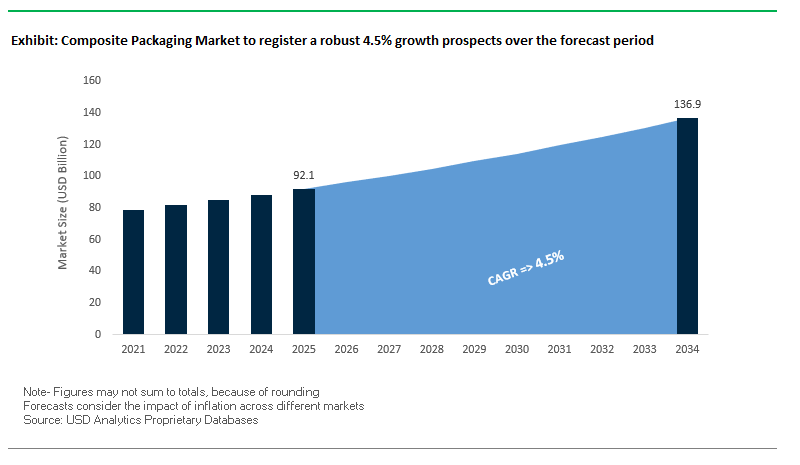

The global composite packaging market is projected to grow from $92.1 billion in 2025 to $136.9 billion by 2034, reflecting a CAGR of 4.5%. Composite packaging, which combines two or more materials to deliver enhanced functionality, is an essential pillar of the modern packaging industry. It is increasingly adopted across food, beverages, personal care, healthcare, and industrial sectors due to its ability to provide superior protection, lightweight efficiency, and brand-driven design opportunities. For packaging buyers and professionals, critical questions revolve around how recyclable mono-material composites will challenge traditional multi-layers, how e-commerce dynamics will accelerate lightweight adoption, and how high-definition printing will evolve packaging into a marketing channel.

Key Insights include:

- Material Innovation: New mono-material laminates are emerging as eco-friendly alternatives, engineered to replicate the barrier performance of aluminum foils while remaining recyclable.

- Food & Beverage Protection: Composite packaging dominates food and beverage applications dairy, powdered drinks, dry snacks where extended shelf life and moisture, oxygen, and light barriers are crucial.

- E-commerce Optimization: A single truckload of flexible composites equals 26 truckloads of rigid packaging, drastically cutting logistics costs and emissions, making it indispensable for online retail.

- Advanced Printing: Over 70% of new consumer goods packaging designs now leverage high-definition digital printing, turning functional packaging into a brand engagement platform.

This growth reflects a convergence of sustainability pressures, consumer convenience, and digital customization, positioning composite packaging as a transformative solution in global supply chains.

Market Analysis: Sustainability, Strategic Consolidation, and Material Innovation

The composite packaging industry is in a phase of rapid transformation, marked by sustainability-driven investments, mergers, and advanced material launches.

In September 2025, Constantia Flexibles announced its participation at FACHPACK 2025, where it will showcase its Ecolutions portfolio and new low-carbon aluminum lidding solutions, reinforcing its sustainability focus. A month earlier, in August 2025, industry news highlighted the impact of U.S. tariffs on PET shrink films, compelling stakeholders to recalibrate procurement strategies, boost domestic capacity, and improve supply chain resilience. That same month, RKW Group partnered with Dow to present collation shrink films using PCR plastics from household waste, a major advance in recycling contaminated waste streams.

In July 2025, Greif, Inc. announced the $1.8 billion sale of its Containerboard business to strengthen its portfolio and invest in growth areas like composite cans and tubes. Also in July, Smurfit Kappa and WestRock completed their merger, forming Smurfit WestRock, a packaging giant expected to shape future competition across composite packaging segments.

In June 2025, Sonoco committed multi-million-dollar investments to expand rigid paper can production across U.S. facilities, responding to growing snack food demand for recyclable formats. That same month, Mondi introduced its re/cycle PaperPlus Bag Advanced, designed for humidity-sensitive products as a paper-based substitute for plastics.

Earlier, in May 2025, Sonoco divested its thermoformed and flexible packaging business to TOPPAN Holdings, further aligning its portfolio with core strengths. These developments illustrate how the composite packaging market is being reshaped by sustainability imperatives, supply chain recalibration, and strategic consolidation.

Emerging Trends and Opportunities Shaping the Composite Packaging Market

Strategic Pivot to Monomaterial and Polymer-Barrier Solutions

The composite packaging market is undergoing a fundamental transformation, with industry players strategically shifting away from multi-material laminates that are challenging to recycle. Regulatory frameworks, particularly the European Union’s Packaging and Packaging Waste Regulation (PPWR), are acting as a catalyst by enforcing design-for-recycling principles and raising Extended Producer Responsibility (EPR) fees on hard-to-recycle materials. This regulatory push has made monomaterial packaging a financial and strategic priority for brand owners and manufacturers.

Companies like Toppan have introduced commercialized “mono-material barrier packages” engineered from single polymers such as PET. These films maintain the essential high-barrier properties required for oxygen and moisture protection while being compatible with established recycling streams. At the same time, corporate sustainability agendas are amplifying the shift. Peer-reviewed studies confirm that transitioning from multi-material to mono-material structures with recyclates can reduce CO₂ emissions by more than 3,600 kg per ton of plastic after four recycling cycles, highlighting the strong environmental case for this transition. This makes monomaterial innovation not just a compliance necessity but also a cost-efficient decarbonization pathway for the composite packaging industry.

Integration of Digital Technologies for Traceability and Anti-Counterfeiting

Composite packaging is evolving from a passive protective layer to an active digital asset within global supply chains. With rising risks of counterfeiting and diversion, packaging is now being embedded with technologies that guarantee product authenticity, enhance transparency, and deliver real-time data. Overt measures, such as holographic images and tamper-evident seals, provide visible consumer-level authentication. Meanwhile, covert technologies like invisible inks, embedded polymer signatures, and forensic markers are enabling discreet verification using specialized equipment. Brands are also turning packaging into a digital engagement tool through unique QR codes and NFC tags. These identifiers offer consumers instant verification of authenticity while enabling companies to gather real-time supply chain data for compliance and inventory management. By blending anti-counterfeiting and traceability, composite packaging is becoming an indispensable part of brand protection strategies and a driver of consumer trust in sensitive markets such as pharmaceuticals, cosmetics, and premium food.

Development of High-Barrier Bio-Based and Compostable Films

The demand for bio-based and compostable composite packaging presents one of the most promising opportunities in this sector. With regulators, brands, and consumers aligned around the need for circular economy solutions, there is a market gap for compostable films that match the high-barrier performance of conventional plastics.

Academic research has shown that incorporating natural fillers into biodegradable composite films significantly enhances their mechanical and thermal properties, making them fit for demanding applications. Real-world commercialization is already underway, with compostable coffee bags offering an effective proof point. These bio-based films integrate functional features like one-way degassing valves while maintaining oxygen and moisture barrier performance critical for product preservation. Such innovations position compostable composites as a premium yet sustainable alternative, particularly for food, beverage, and specialty product packaging.

Advanced Coating Technologies to Replace Aluminum and Plastic Foils

The reliance on aluminum foils and thick plastic laminates in composite packaging remains a major recyclability barrier. This has created a strong innovation pipeline for next-generation coating technologies that deliver high-barrier performance without the environmental drawbacks of multi-material layers.

Vapor-deposited coatings, such as aluminum oxide (AlOx), are being scaled up as a thin, recyclable alternative to traditional foils. When combined with novel lacquers, these coatings can achieve excellent oxygen and moisture barrier properties while maintaining compatibility with recycling streams. On the frontier of material science, nanomaterial-based coatings notably graphene oxide hybrids on polyolefin substrates are demonstrating dramatic reductions in oxygen and water vapor permeability. These breakthroughs enable the creation of recyclable mono-material structures that preserve product integrity and reduce waste. By replacing non-recyclable foils with advanced coatings, manufacturers can simultaneously achieve regulatory compliance, sustainability targets, and product protection at scale.

Competitive Landscape: Key Companies Driving the Composite Packaging Market

The composite packaging market is highly competitive, with global leaders and specialized players focusing on eco-friendly materials, advanced printing, and portfolio expansion to capture demand across multiple industries.

Amcor Plc invests in recyclable, high-barrier composites

Amcor offers a comprehensive range of rigid and flexible composite packaging, including cans, pouches, and films. Its recent innovations include metal-free, recyclable high-barrier films and RPETG shrink films with verified recycled content. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, targeting medical device demand. Its extensive global network ensures seamless integration from design to scale, making it a trusted partner for leading consumer brands.

Sonoco Products Company focuses on recyclable rigid paper cans

Sonoco is a global leader in rigid paper containers and composite cans, with flagship products such as EnviroCan and EnviroSense. In June 2025, it expanded U.S. production of paper-bottom composite cans, enhancing recyclability by eliminating metal closures. Sonoco is also streamlining its portfolio, highlighted by its May 2025 divestiture to TOPPAN Holdings, allowing stronger focus on high-growth packaging areas. Its solutions are widely used in snack foods, industrial, and personal care packaging.

Smurfit WestRock strengthens its global footprint post-merger

The merger of Smurfit Kappa and WestRock in July 2025 created Smurfit WestRock, one of the largest packaging companies worldwide. Its composite packaging offerings include corrugated composites, bag-in-box, and barrier board solutions designed to reduce plastic usage. With vertically integrated operations from forest management to packaging delivery, the company ensures consistency and sustainability. Its expanded global footprint over 100,000 employees in 40 countries positions it as a key competitor in replacing single-use plastics with composite alternatives.

Mondi Group drives innovation with paper-based composites

Mondi delivers high-performance composite packaging across flexible food applications and specialty paper segments. In June 2025, it launched the re/cycle PaperPlus Bag Advanced, a recyclable, high-barrier paper solution for moisture-sensitive goods. Mondi is also investing in renewable energy, including an August 2025 biomass power plant in Slovakia to boost energy independence. Its 2030 sustainability strategy, validated by the Science Based Targets initiative (SBTi), reinforces its leadership in the circular economy.

Berry Global Group, Inc. advances high-performance multi-layer films

Berry Global specializes in multi-layer films and rigid composite packaging, serving food, healthcare, and industrial markets. Its focus lies in process efficiency, RPETG-based shrink films, and digital printing compatibility. Berry’s vertically integrated model from resin sourcing to final packaging ensures regulatory compliance and consistent quality. Its ongoing innovations in recyclable, high-performance barrier films reinforce its role as a benchmark in reliable and sustainable packaging solutions.

Composite Packaging Market Share Insights

Flexible Pouches Dominate Composite Packaging Market Share by Format

Flexible pouches and bags hold the largest share of the composite packaging market with around 45% in 2025, underscoring their position as the industry’s most versatile and cost-efficient packaging format. They are widely adopted across food, beverage, and personal care industries due to their lightweight structure, ability to integrate high-barrier layers, and convenience features such as resealable zippers and spouts. Their ability to reduce packaging weight by up to 70% compared to rigid containers not only lowers logistics costs but also supports sustainability goals by reducing overall material usage and carbon footprint. Composite cans account for 25% of the market, serving as a recyclable, rigid alternative for dry foods, snacks, powders, and beverages. Their cylindrical design offers excellent stacking strength and high-quality printability, making them attractive for brand differentiation. Rigid composite containers, blister packs, and tubs form the balance of the market, fulfilling specialized needs such as premium unboxing experiences, tamper-evidence, and maximum barrier protection for pharmaceuticals, cosmetics, and sensitive goods. Collectively, these formats highlight how the market balances volume efficiency with protective performance and premium branding.

Food & Beverage Leads Composite Packaging Market Share by End-Use Industry

The food and beverage sector dominates the composite packaging market with a commanding 60% share in 2025, driven by rising demand for extended shelf life, lightweighting, and sustainable packaging formats. Composite packaging solutions particularly stand-up pouches and high-barrier cans are increasingly used for snacks, coffee, dairy, frozen foods, and ready-to-eat meals, offering both product protection and superior branding through vibrant graphics and printing. Pharmaceuticals and healthcare represent 15% of the market, where composite blister packs and high-barrier pouches provide critical protection against moisture, oxygen, and light to preserve drug efficacy and patient safety. Personal care and cosmetics are another high-value growth driver, where composite packaging’s ability to combine premium aesthetics, unique textures, and functional innovations like airless pumps supports brand positioning in luxury and sustainable beauty markets. Consumer goods, industrial products, and electronics hold smaller but vital shares, leveraging composite packaging for durability, anti-static protection, and secure retail presentation. Together, these end-use sectors showcase the market’s broad applicability, with food and beverage anchoring volume demand while pharmaceuticals and cosmetics drive high-value innovation.

United States: Advancing Sustainable Composite Packaging with Convenience Features

The U.S. composite packaging market is being reshaped by a strong focus on sustainable and recyclable packaging solutions. Companies are innovating with mono-material composites and paper-based solutions, including composite cans with fully recyclable paper bottoms. This aligns with growing consumer demand for eco-friendly packaging and supports corporate circular economy initiatives.

The boom in e-commerce and food delivery has further accelerated demand for lightweight, durable composite packaging that can withstand shipping while protecting product integrity. Innovations also include easy-to-open and resealable designs, particularly for snacks, ready-to-eat meals, and nutraceutical products. Technological advancements, such as improved thermoforming, lamination techniques, and the integration of smart features like QR codes and RFID for traceability, are becoming critical for manufacturers aiming to meet regulatory, safety, and consumer requirements. The health and wellness sector, especially for protein powders and dietary supplements, is a key driver, favoring composite packaging that preserves freshness and extends shelf life.

China: Manufacturing Powerhouse Driving Advanced and Secure Composite Solutions

China’s composite packaging market is fueled by its massive manufacturing base and export capabilities, particularly in electronics, consumer goods, and food and beverage industries. The country’s emphasis on improving food safety, logistics standards, and quality assurance is driving the adoption of advanced composite packaging solutions that comply with both domestic and international regulations.

To address challenges such as counterfeiting, manufacturers are increasingly using holographic laminates, unique identification codes, and security-enhanced composites. Furthermore, the focus on scale and efficiency has prompted substantial investments in automation and robotics, enabling high-volume production while reducing operational costs. The combined effect of robust domestic demand, export requirements, and technological innovations positions China as a dominant player in the global composite packaging market.

Germany: Leading Europe’s Circular Economy and Sustainable Composite Packaging

Germany is a front-runner in the European shift toward sustainable composite packaging, driven by the European Green Deal and the Packaging and Packaging Waste Regulation (PPWR). Manufacturers prioritize easily recyclable, high-quality, and resource-efficient materials, with a strong focus on post-consumer recycled (PCR) content.

Strategic collaborations between material producers and packaging companies are fostering innovation. For example, partnerships between Borealis and German packaging firms have produced collation shrink films with exceptionally high PCR content. Germany is also leveraging advanced material science research, with institutions like the Fraunhofer Institute developing detachable cardboard-plastic composites to simplify recycling processes. These initiatives demonstrate Germany’s commitment to sustainability while maintaining product protection and quality.

India: Rapid Urbanization and E-commerce Driving Composite Packaging Demand

India’s composite packaging market is witnessing robust growth due to urbanization, rising disposable incomes, and increasing demand for packaged food, beverages, and consumer goods. The market is expanding across composite cans, flexible pouches, and multi-material packaging solutions.

The government’s Plastic Waste Management (Amendment) Rules 2025 mandate the inclusion of barcodes and QR codes for multi-layer packaging, enhancing traceability and influencing the design of composite solutions. India’s booming e-commerce and food delivery sectors further propel demand for durable, protective packaging capable of ensuring product integrity during transit. Domestic manufacturers are scaling production and adopting advanced technologies to meet the growing consumer and industrial requirements.

Brazil: Sustainable Packaging in Agri-Business and Export Markets

Brazil’s composite packaging market is heavily driven by the country’s agricultural exports and the need for durable packaging for commodities such as coffee, grains, and frozen foods. The market is increasingly influenced by initiatives that promote sustainability, reflecting both governmental policies and industry-led efforts.

A notable example is the collaboration between Klabin, a Brazilian paper company, and packaging machine manufacturers, which resulted in a 100% recyclable, repulpable paper wicket bag for diaper packaging. This innovation highlights the growing trend toward eco-friendly composite packaging in Brazil, ensuring that packaging solutions meet both environmental goals and the functional demands of high-volume export logistics.

Composite Packaging Market Report Scope

Composite Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$92.1 Billion

|

|

Market Size (2034)

|

$136.9 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Material (Paper & Paperboard, Plastic, Aluminum, Other Materials), By Packaging Format (Composite Cans, Flexible Pouches & Bags, Blister Packs, Rigid Containers, Composite Tubs), By End-Use Industry (Food & Beverage, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Consumer Goods, Electronics, Industrial)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Smurfit Kappa Group plc, Mondi plc, Sonoco Products Company, DS Smith plc, Greif Inc., Huhtamaki Oyj, Tetra Pak International S.A., Sealed Air Corporation, International Paper Company, BillerudKorsnäs AB, WestRock Company, Constantia Flexibles Group GmbH, Novolex, Graphic Packaging International, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Composite Packaging Market Segmentation

By Material

- Paper & Paperboard

- Plastic

- Aluminum

- Other Materials

By Packaging Format

- Composite Cans

- Flexible Pouches & Bags

- Blister Packs

- Rigid Containers

- Composite Tubs

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Consumer Goods

- Electronics

- Industrial

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Composite Packaging Market

- Amcor plc

- Smurfit Kappa Group plc

- Mondi plc

- Sonoco Products Company

- DS Smith plc

- Greif Inc.

- Huhtamaki Oyj

- Tetra Pak International S.A.

- Sealed Air Corporation

- International Paper Company

- BillerudKorsnäs AB

- WestRock Company

- Constantia Flexibles Group GmbH

- Novolex

- Graphic Packaging International, LLC

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the global composite packaging market, highlighting breakthroughs in material science, sustainability initiatives, and digital integration. The analysis reviews historical trends from 2021 to 2024 and provides forecasts from 2025 to 2034, capturing market dynamics driven by lightweight solutions, mono-material innovations, and high-barrier packaging for sensitive products. This report highlights the strategic adoption of recyclable laminates, compostable films, and advanced coating technologies, while assessing e-commerce-optimized formats and high-definition printing as brand engagement tools. It reviews mergers, divestitures, and portfolio realignments among leading players, offering insights into competitive positioning and growth opportunities. By profiling 15+ companies including Amcor plc, Sonoco Products Company, Mondi plc, Smurfit Kappa Group, Greif Inc., Tetra Pak, DS Smith, and Constantia Flexibles this report is an essential resource for brand owners, packaging designers, and investors seeking to navigate regulatory shifts, sustainability pressures, and technological innovations that are transforming the composite packaging industry. USDAnalytics ensures decision-makers gain an in-depth understanding of market trends, recyclability imperatives, and premium packaging strategies that shape global supply chains.

Scope Highlights:

- Segmentation: By Material (Paper & Paperboard, Plastic, Aluminum, Other Materials); By Packaging Format (Composite Cans, Flexible Pouches & Bags, Blister Packs, Rigid Containers, Composite Tubs); By End-Use Industry (Food & Beverage, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Consumer Goods, Electronics, Industrial).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historical and Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Company Analysis: In-depth coverage of 15+ leading companies, including Amcor plc, Smurfit Kappa Group plc, Mondi plc, Sonoco Products Company, DS Smith plc, Greif Inc., Huhtamaki Oyj, Tetra Pak International S.A., Sealed Air Corporation, International Paper Company, BillerudKorsnäs AB, WestRock Company, Constantia Flexibles Group GmbH, Novolex, and Graphic Packaging International, LLC.

Methodology

The study applies a robust research methodology integrating primary and secondary data collection to ensure precise market insights. USDAnalytics conducted interviews with industry stakeholders, including packaging manufacturers, converters, brand owners, and sustainability specialists, to validate emerging trends and market developments. Secondary research involved reviewing corporate reports, regulatory frameworks, academic studies, trade publications, and market literature. Quantitative analysis included historical market sizing, CAGR calculations, and detailed segmentation by material, packaging format, and end-use industry. Forecasting employed scenario-based modeling, factoring in sustainability regulations, technological innovation, and e-commerce growth. Competitive intelligence was compiled through company profiles, strategic initiatives, mergers, acquisitions, and product launches, providing an exhaustive understanding of the global composite packaging landscape for industry professionals.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.