PET Shrink Films Market Size, Overview, and Growth Outlook (2021–2034)

PET Shrink Films Market Set to Grow to $4.2 Billion by 2034 Driven by Sustainability and High-Performance Packaging Needs

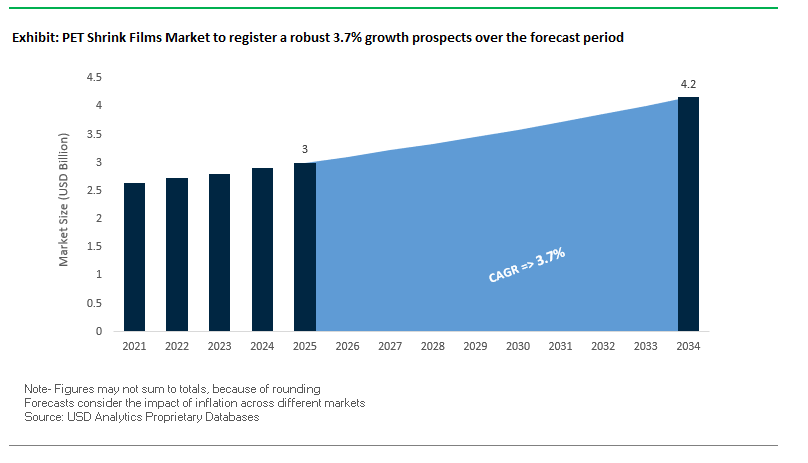

The Global PET Shrink Films Market is projected to grow from $3 billion in 2025 to $4.2 billion by 2034, registering a CAGR of 3.7%. PET shrink films are engineered to tightly wrap products or bundles upon heating, offering a tamper-evident, protective, and visually appealing layer. They are integral to the beverage, food, and consumer goods sectors, where functionality, branding, and sustainability are critical.

Key Insights for industry professionals and buyers:

- Sustainability Leadership: PET shrink films are fully recyclable and compatible with PET bottles, enabling a closed-loop recycling system.

- Visual Branding Advantage: High clarity and 360-degree printability enhance retail shelf appeal and product differentiation.

- Tamper-Evident Protection: Films provide robust seals and controlled shrinkage, ensuring product safety and quality.

- E-commerce Optimization: Durability and puncture resistance meet the rising demand for secure online product delivery.

- Market Innovation: Advances in high-performance films support multi-pack bundling, hygiene, and barrier protection.

Market Analysis: PET Shrink Films Market Expansion Fueled by Advanced Technology, Sustainability, and Capacity Investments

The PET shrink films industry is rapidly evolving with innovations in sustainability, manufacturing efficiency, and high-performance solutions. In August 2025, Berry Global announced a $25 million investment to expand its Ohio facility, targeting growing demand in the food packaging sector. In the same month, Amcor unveiled an automated shrink film converting unit in Texas to improve production efficiency for beverages and consumer goods. Sealed Air Corporation also launched a high-performance biodegradable shrink film in the U.S., enhancing environmental sustainability while maintaining packaging strength.

In July 2025, Mitsubishi Chemical introduced a next-generation heat-shrink film optimized for high-speed packaging lines, supporting Japanese market sustainability initiatives. UBE Industries invested $15 million in June 2025 to expand its Osaka plant, increasing capacity for industrial and food applications. Earlier in May 2025, Constantia Flexibles invested over €6 million in a new machine-direct orientation (MDO) line at its German facility, supporting production of high-barrier mono-polyethylene films like EcoLamHighPlus. April 2025 saw Toyo Seikan Kaisha introduce antimicrobial shrink films in Japan to improve hygiene and extend shelf life.

Strategic collaborations also strengthened the market. In February 2025, Berry Global partnered with VOID Technologies to develop high-performance, sustainable films for pet food packaging, highlighting the industry’s focus on eco-friendly solutions, high clarity, and barrier protection.

Disruptive Trends and High-Value Opportunities in the PET Shrink Films Market

Accelerated Regulatory Phase-Out of PVC Driving Shift to PETG and rPET Shrink Films

The global PET shrink films market is witnessing a decisive shift away from PVC shrink films, accelerated by new regulatory frameworks and recycling challenges. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from early 2025, does not explicitly ban PVC but indirectly restricts its use through strict recyclability mandates and material circularity requirements. PVC’s incompatibility with PET recycling infrastructure—due to hydrochloric acid release during processing and its contamination of recycled PET (rPET) streams—makes it a liability for both brands and recyclers. Consequently, companies are transitioning to PET-based alternatives, particularly glycol-modified PET (PETG), which offers compatibility with PET recycling systems. PETG has an inherent advantage in shrink performance, delivering 70–80% shrinkage compared to PVC’s 50–60%, enabling tight, wrinkle-free wrapping even on complex bottle geometries. This superior shrinkage allows for high-quality graphics and aesthetics while reducing risks of recycling contamination. Additionally, rPET-based shrink films are emerging as sustainable alternatives, allowing brands to align packaging strategies with extended producer responsibility (EPR) frameworks and circular economy targets.

Adoption of High-Clarity, High-Shrink Films for Premium “Sleeve-Less” Labeling

Premiumization trends in food, beverage, and pharmaceutical packaging are driving the adoption of high-clarity PETG shrink films that function as “sleeve-less” labeling solutions. By replacing separate labels with full-body shrink films, brands achieve 360° printability, creating immersive, high-resolution graphics that elevate shelf appeal. This approach reduces overall packaging material by combining labeling and protective functions into one integrated structure. For instance, premium beverage brands are increasingly using PETG full-body sleeves to differentiate craft beer or functional beverages through bold, artistic designs. The enhanced shrink properties of PETG also improve tamper-evident functionality, as films can be shrunk tightly over caps and necks to provide a clear indicator of product integrity. This is particularly valuable for pharmaceuticals and nutraceuticals, where safety assurance directly impacts consumer trust. The convergence of premium aesthetics, convenience, and security positions PET shrink films as a critical enabler of brand loyalty and differentiation in competitive consumer markets.

Development of Functional Barrier Shrink Films for Sensitive Products

One of the most promising opportunities in the PET shrink films market lies in functional shrink films with integrated barrier properties. Sensitive products such as fresh juices, dairy, and craft beer require protection against oxygen, moisture, and UV light to maintain freshness and quality. Conventional PET bottles often rely on thicker walls or secondary packaging, increasing material use and costs. Innovations in co-extrusion and nano-coating technologies are enabling PET shrink films with barrier layers of Silicon Oxide (SiOx) or Aluminum Oxide (AlOx), drastically reducing oxygen transmission rate (OTR) and water vapor transmission rate (WVTR). This innovation could allow beverage companies to down-gauge bottles while relying on the shrink sleeve to provide the necessary protection, achieving both lightweighting and product integrity. By combining high-shrink functionality with barrier performance, these advanced films are poised to disrupt markets traditionally dominated by glass or aluminum, offering sustainability benefits without compromising shelf life.

Integration of Digital Watermarking for Intelligent Recycling Sortation

The integration of digital watermarking into PET shrink films presents a breakthrough opportunity for improving recycling efficiency and advancing circular economy goals. The HolyGrail 2.0 initiative, tested in late 2024, demonstrated detection accuracy above 99% and ejection rates exceeding 95% in industrial trials, proving the scalability of this innovation. Digital watermarks embedded in shrink films enable SKU-level identification, allowing high-speed sortation systems to distinguish between food-grade and non-food-grade PET, or to separate PET bottles with shrink sleeves from those without. This solves a long-standing challenge in PET recycling, where shrink sleeves—often of different material densities—contaminate rPET streams. By ensuring precise material recovery, watermarking not only enhances the quality of rPET feedstock but also supports compliance with EU PPWR mandates for consumer guidance and recycled content targets. Furthermore, brands can use watermark-enabled packaging for interactive consumer engagement and improved supply chain traceability, creating dual value in sustainability and marketing. As regulations tighten and demand for high-quality rPET surges, digital watermarking is positioned as a pivotal technology for scaling intelligent, closed-loop PET recycling systems.

Competitive Landscape: Key PET Shrink Films Manufacturers Are Leading the Industry Through Sustainability, Innovation, and Operational Excellence

The PET shrink films market is dominated by leading manufacturers leveraging material science expertise, high-performance solutions, and sustainable initiatives to meet growing global demand.

Amcor plc: Expanding Automated Production Capabilities and Sustainable PET Films

Amcor offers a wide range of PET shrink films for full-body labels and tamper-evident seals in beverages and consumer goods. In August 2025, the company unveiled an automated shrink film converting unit in Texas to enhance production efficiency. Amcor also partnered with a paint brand to develop 50% recycled content containers, expanding its sustainable film portfolio. Its core strengths include global manufacturing reach, material science expertise, and vertically integrated operations, supporting circular economy initiatives and branding requirements.

Toyobo Co., Ltd.: Pioneering Eco-Friendly Shrink Films With High Recyclability

Toyobo, a Japanese specialty film manufacturer, offers PET shrink films like ReCrysta™, designed for recyclability with PET bottles. In May 2024, ReCrysta™ was recognized by the Association of Plastic Recyclers (APR) for its recyclability using over 50% recycled PET. Toyobo’s strengths include longstanding innovation in film technology and commitment to eco-friendly solutions, particularly in Southeast Asia, where demand for recycled PET is increasing.

Berry Global Inc.: Driving Expansion and High-Performance Sustainable Shrink Films

Berry Global produces shrink films for food, beverages, and industrial goods. In August 2025, it invested $25 million in Ohio to expand production capacity and partnered with VOID Technologies to develop sustainable, high-performance films for pet food packaging. The company’s strengths lie in diverse product portfolio, expertise in rigid and flexible packaging, and commitment to circular economy solutions.

Sealed Air Corporation: Launching Biodegradable Shrink Films to Reduce Environmental Impact

Sealed Air provides shrink films for food, beverage, and industrial applications. In June 2025, the company launched a high-performance biodegradable shrink film in the U.S. to combine strength with environmental sustainability. Its strengths include innovation in materials science and comprehensive packaging solutions designed to protect products across the supply chain.

Constantia Flexibles Group GmbH: Investing in High-Barrier Mono-Polyethylene Shrink Films

Constantia Flexibles offers a broad range of flexible packaging, including high-barrier shrink films. In May 2025, the company invested over €6 million in a new MDO line in Germany, supporting the production of films like EcoLamHighPlus. Strengths include material innovation, customized packaging solutions, and focus on sustainable product development for food and beverage brands.

PET Shrink Films Market Share Insights, 2025-2034

PET-G Dominates Market Share by Film Type in the PET Shrink Films Industry

PET-G shrink films command nearly 68% of the global market, establishing themselves as the benchmark for performance, sustainability, and regulatory compliance. Their dominance stems from superior optical clarity, high gloss, and consistent shrinkage rates of up to 80%, which enable seamless application across containers with complex geometries. PET-G films deliver mechanical robustness, resisting tearing during transit and application, which is a critical factor for global FMCG and beverage companies seeking reliable brand presentation at scale. Furthermore, their compatibility with existing PET recycling streams makes them an attractive option for brand owners under increasing regulatory and consumer scrutiny to adopt sustainable solutions. In contrast, OPS films hold a niche share due to lower cost but face limitations in recyclability and brittleness, which undermine their long-term competitiveness. Meanwhile, legacy materials like PVC are rapidly losing relevance due to environmental hazards, while bio-based PLA remains a small but emerging contender, restricted by cost and performance gaps. This shift underscores how sustainability mandates and functional superiority are consolidating PET-G’s leadership in the shrink films sector.

Full Body Sleeves Lead Market Share by Application in the PET Shrink Films Industry

Full body sleeves account for 35% of PET shrink film applications, making them the most widely adopted format in the sector. Their appeal lies in providing 360° printable surface area, enabling brand owners to maximize shelf impact, communicate product stories, and differentiate through high-quality graphics and vibrant decoration. They are particularly effective for complex and irregular container shapes, where conventional labels are inadequate. This segment has grown in tandem with the beverage, personal care, and homecare industries, where brand visibility is central to consumer purchase decisions. Labels follow as a high-volume workhorse, particularly in food and beverage packaging where cost-effective decoration and barrier performance are key. Tamper-evident bands represent another high-value segment, mandated in pharmaceuticals, premium beverages, and regulated food categories to ensure consumer safety and brand protection. Multipacks, ROSS (roll-on shrink sleeves), and specialty wraps round out the market, each serving efficiency or niche promotional roles. Collectively, these dynamics show how PET shrink film applications balance branding power, operational efficiency, and safety compliance, with full body sleeves emerging as the dominant platform for premium and mass-market goods alike.

United States PET Shrink Films Market Driven by Sustainability and Smart Packaging

The United States PET shrink films market is leading in the adoption of advanced technologies for packaging across beverages, food, and personal care. Companies are prioritizing high-clarity PET shrink films that enhance product visibility on retail shelves, reinforcing brand storytelling and consumer engagement. The shift toward recycled PET (rPET) shrink films is accelerating, supported by consumer demand for eco-friendly products and corporate sustainability goals.

A major innovation driver is digital printing on PET shrink films, enabling enhanced graphics, personalization, and dynamic brand messaging, particularly important in competitive retail categories. The rise of e-commerce packaging has also pushed demand for robust yet lightweight shrink films that can withstand distribution stress while lowering material use and costs. Industry organizations such as the Association of Plastic Recyclers (APR) are working on compatibility improvements to ensure PET shrink labels can integrate seamlessly into bottle recycling streams, addressing a critical sustainability challenge.

China PET Shrink Films Market Boosted by Regulation and Beverage Demand

The China PET shrink films market is heavily shaped by government policies, particularly the GB 23350-2021 regulation, which restricts excessive packaging and drives material efficiency. The explosive growth of e-commerce grocery channels is creating high demand for shrink films that offer high-barrier protection, particularly for perishable food and beverage products.

The beverage sector is one of the largest application areas, with strong demand for full-body PET shrink sleeves that combine tamper-evident sealing with premium branding opportunities. Local manufacturers are scaling up production of PET-G shrink films, known for superior shrinkage and clarity, to meet evolving market needs. Sustainability is also gaining traction, with companies developing eco-friendly PET shrink films to align with consumer preferences and national green economy targets.

Germany PET Shrink Films Market Transitioning from PVC to PET-G Solutions

The Germany PET shrink films market is undergoing a significant shift from conventional PVC shrink films to recyclable PET-G alternatives, driven by the European Union’s Single-Use Plastics Directive and Germany’s national sustainability goals. German manufacturers are investing in multi-layer PET shrink films that offer superior oxygen barrier, clarity, and recyclability.

Applications are expanding across the food and beverage industries, where high-barrier PET shrink films are essential to maintain freshness and extend shelf life of perishable goods. Innovations in compostable and biodegradable shrink films are also emerging, ensuring compliance with the EU’s circular economy policies. Alongside technical advancements, German companies are focusing on developing premium shrink sleeves and lidding films, combining sustainability with consumer convenience.

United Kingdom PET Shrink Films Market Driven by EPR and Recycling Targets

The United Kingdom PET shrink films market is shaped by regulatory measures such as the Extended Producer Responsibility (EPR) framework, which transfers packaging waste management costs to producers. The government’s mandate to collect flexible plastics by March 2027 is a major driver for the adoption of recyclable mono-material PET shrink films.

Key industry players like Mars are rolling out recyclable mono-material packaging formats, setting new benchmarks for circularity in the pet food and FMCG sectors. Reports from the Flexible Plastic Fund (2025) highlight the potential for nationwide collection and recycling infrastructure, supporting PET film recovery. Consumer preferences are increasingly favoring eco-friendly and recyclable packaging, boosting demand for PET shrink films in fresh produce, beverages, and convenience foods.

Japan PET Shrink Films Market Anchored in Recycling Innovation and Food Preservation

The Japan PET shrink films market is driven by strong sustainability commitments and advanced preservation needs. The Japan Soft Drink Association has set a target of 50% bottle-to-bottle recycling by 2030, encouraging widespread adoption of recyclable PET packaging materials. Strategic collaborations, such as the agreement between JEPLAN Group, Ito En, and Far East Ishizuka Green PET, integrate chemical and mechanical recycling technologies to achieve higher recovery rates.

Japan’s health-conscious and aging consumer base is driving demand for PET shrink films with enhanced food preservation properties, reducing waste while ensuring safety. The rapid rise of e-commerce and home delivery services has expanded applications for PET shrink films in transit packaging, where breathable and protective designs are required. Together, these factors make Japan a global leader in eco-friendly PET shrink film innovation.

India PET Shrink Films Market Expands with Domestic Investments and Food Applications

The India PET shrink films market is witnessing strong growth, supported by government regulations and significant industry investments. The ban on single-use plastics enforced in July 2022 has accelerated the shift toward recyclable PET shrink films. Companies like Jindal Poly Films (JPFL Films) have invested over INR 700 crore in new PET and film production lines in Nashik, strengthening India’s manufacturing capacity. Similarly, Garware Polyester has introduced medium and low shrink force PET films tailored for bottle and container labeling, while Uflex Limited is expanding its sustainable film offerings.

The surge in urban consumption of fresh produce, bakery, and ready-to-eat foods is driving demand for PET shrink films, particularly in retail and e-commerce packaging. With a growing emphasis on digital marketing and online distribution, Indian companies are developing aesthetically appealing and protective PET shrink packaging to cater to both domestic and export markets. The combination of policy enforcement, consumer demand, and industry capacity positions India as a rising hub for PET shrink film innovation and production.

PET Shrink Films Market Report Scope

PET Shrink Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3 Billion

|

|

Market Size (2034)

|

$4.2 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Film Type (PET-G, OPS, Others), By Thickness (Below 20 microns, 20–50 microns, Above 50 microns), By Shrinkage (Low, Medium, High), By Application (Full Body Sleeves, Roll-on Shrink Sleeves, Tamper-evident Bands, Multipacks, Labels, Wraps), By End-Use Industry (Food & Beverage, Pharmaceuticals, Personal Care & Cosmetics, Industrial Packaging, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Klöckner Pentaplast Group, Berry Global, Inc., Toyobo Co., Ltd., Jindal Poly Films, Fuji Seal International, Inc., Tekni-Plex, Inc., Uflex Limited, Cosmo Films Ltd., Toray Industries, Inc., Bonset America Corporation, Allen Plastic Industries Co., Ltd., Amcor plc, Bolloré Packaging Films, TCL Packaging Ltd., ProAmpac

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PET Shrink Films Market Segmentation

By Film Type

By Thickness

- Below 20 microns

- 20–50 microns

- Above 50 microns

By Shrinkage

By Application

- Full Body Sleeves

- Roll-on Shrink Sleeves

- Tamper-evident Bands

- Multipacks

- Labels

- Wraps

By End-Use Industry

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Packaging

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PET Shrink Films Market

- Klöckner Pentaplast Group

- Berry Global, Inc.

- Toyobo Co., Ltd.

- Jindal Poly Films

- Fuji Seal International, Inc.

- Tekni-Plex, Inc.

- Uflex Limited

- Cosmo Films Ltd.

- Toray Industries, Inc.

- Bonset America Corporation

- Allen Plastic Industries Co., Ltd.

- Amcor plc

- Bolloré Packaging Films

- TCL Packaging Ltd.

- ProAmpac

* List Not Exhaustive

Methodology

USDAnalytics applies a comprehensive research methodology to provide precise, actionable insights into the PET Shrink Films Market, combining primary and secondary data sources to ensure robustness and reliability. Primary research includes interviews with key stakeholders such as manufacturers, distributors, and regulatory bodies to capture first-hand perspectives on market dynamics, technological innovations, and regulatory compliance. Secondary research leverages verified trade publications, company reports, government databases, and industry journals to validate historical trends and emerging developments. Market sizing and forecasting are derived using a hybrid approach, combining top-down and bottom-up analyses while accounting for material innovations, sustainability mandates, and shifts from PVC to PET-G and rPET films. USDAnalytics employs advanced statistical modeling to calculate market value, CAGR, and segment share, cross-verified against production capacity, investments, and global consumption patterns. Special attention is given to trends such as high-clarity full-body sleeves, functional barrier films, mono-material design, digital watermarking for recycling, and premium “sleeve-less” packaging, ensuring that the analysis captures both current market realities and forward-looking growth opportunities, providing industry professionals with actionable intelligence for strategic decision-making.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.