PET Packaging Market Size, Overview, and Growth Outlook (2025–2034)

PET Packaging Market Poised to Reach $137.9 Billion by 2034 Driven by Sustainability and Advanced Barrier Innovations

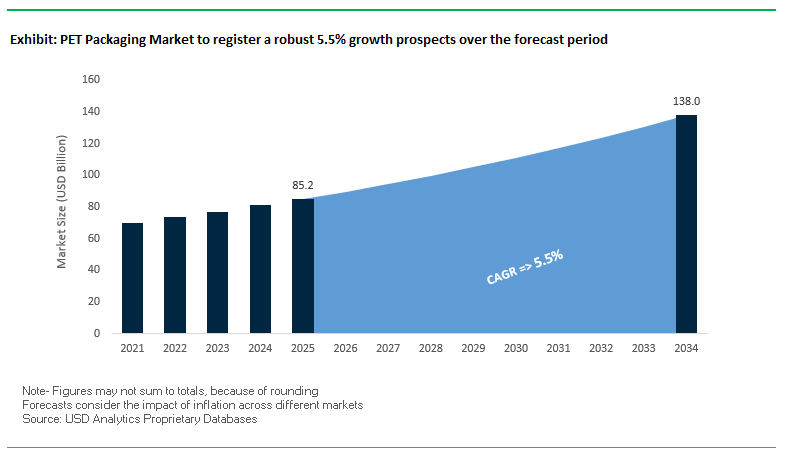

The Global PET Packaging Market is projected to grow from $85.2 billion in 2025 to $137.9 billion by 2034, registering a CAGR of 5.5%. PET packaging remains a critical solution across food and beverage, personal care, and pharmaceutical industries due to its clarity, durability, lightweight properties, and versatility. The industry is evolving from a traditional protective role to a strategic tool for brand differentiation, product preservation, and sustainable innovation.

Key Insights for industry professionals and buyers:

- Sustainability Leadership: Brands increasingly target 50%+ PCR content to satisfy regulatory and consumer demand.

- Lightweighting Technologies: Continuous reduction of virgin material lowers carbon footprint and material costs without compromising product integrity.

- Advanced Barrier Properties: Multi-layer PET and new resin innovations extend shelf life by protecting against oxygen, UV, and moisture.

- Mono-Material Designs for Circularity: Shift away from multi-material labels and closures enhances recyclability and supports closed-loop systems.

- Market Diversification: PET packaging adoption is expanding into industrial and healthcare applications beyond traditional F&B sectors.

- Consumer-Centric Solutions: Packages are optimized for convenience, freshness, and visual appeal, aligning with evolving lifestyle preferences.

Market Analysis: Technological Advancements, Sustainability Initiatives, and Market Expansion Fuel PET Packaging Growth

The PET packaging market is witnessing rapid transformation, driven by sustainability, material innovation, and global expansion strategies. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, enhancing PET packaging capabilities for the pharmaceutical and medical sectors. During the same month, Plastipak showcased sustainable, high-performance packaging at Drinktec in Munich, highlighting bio-based resins, bottle-grade rPET, and advanced barrier technologies. Amcor also partnered with Flügger to develop a 50% recycled paint container, demonstrating PET’s versatility beyond food and beverage applications.

In July 2025, the Pet Sustainability Coalition launched a program supporting companies transitioning to sustainable packaging, driving innovation in PET film and container development. Amcor reported strong fiscal 2025 earnings, reflecting successful global expansion and sustainable product adoption. In May 2025, Constantia Flexibles invested over €6 million in a new MDO line in Germany to support high-barrier mono-polyethylene films like EcoLamHighPlus, emphasizing performance and recyclability. Earlier in February 2025, Evertis committed $100 million to a new PET multilayer plant in South Carolina, expanding U.S. production capacity, while ALPLA announced plans in January 2025 to double its plastic recycling capacity to 700,000 tonnes by 2030, reinforcing the circular economy focus.

Transformative Trends and Emerging Opportunities in the PET Packaging Market

Legislative Mandates Driving Unprecedented Demand for Recycled PET (rPET)

Government regulations are the single most powerful force reshaping the PET packaging market, creating an unprecedented surge in demand for recycled PET (rPET). The European Union’s Single-Use Plastics Directive (SUPD) mandates that PET beverage bottles must contain a minimum of 25% rPET by 2025 and 30% by 2030. In parallel, the United States is implementing state-level policies, such as California’s AB 793, which requires plastic bottles to reach 25% recycled content by 2025 and 50% by 2030. These mandates are not advisory but legally binding, meaning non-compliance translates into financial penalties and reputational risks. Beverage companies are not waiting for deadlines—many are exceeding requirements ahead of schedule. The Coca-Cola Company has introduced bottles made from 100% rPET (excluding caps and labels) in more than 40 markets, including Singapore and the U.S., and has pledged to reach 50% recycled content globally by 2030. Danone has committed to 50% recycled content by 2025, aiming for 100% rPET in its water business across Europe. To support these targets, companies are pouring billions into recycling infrastructure expansion. Across the U.S. and Europe, new processing facilities are being commissioned and legacy plants upgraded to handle higher PET volumes, ensuring a steady, high-quality supply of rPET for food and beverage packaging applications.

Strategic Shift to Lightweighting and Monomaterial Design for Recyclability

Another defining trend is the dual emphasis on lightweighting and monomaterial design, which directly enhances packaging recyclability and reduces overall carbon footprints. Lightweighting strategies are allowing brands to minimize resource usage without compromising functionality. Coca-Cola, for example, has cut the weight of its 16.9 oz and 20 oz PET bottles from 21 grams to 18.5 grams, lowering raw material costs and decreasing emissions from transportation by allowing more bottles per truckload. At the same time, monomaterial design is gaining traction as companies seek to streamline recycling processes. Innovations include PET-only bottles with PET labels, direct-to-bottle printing, and PET caps that eliminate the need for mixed materials like HDPE or PP. By moving toward full PET bottle-and-cap systems, brands are ensuring compatibility with existing recycling infrastructure. Additionally, beverage brands are removing colored pigments from bottles, particularly iconic green or blue, to create high-value clear rPET streams. Clear rPET has greater utility in closed-loop recycling because it can be repurposed into a wider range of high-performance applications, including new bottles. This strategic redesign highlights how packaging innovation now extends beyond aesthetics, becoming a vital enabler of circularity in the PET packaging ecosystem.

Commercialization of Advanced Purification Technologies for Food-Grade rPET

A critical opportunity in the PET packaging market lies in overcoming the persistent challenge of limited food-grade rPET supply. Advanced purification technologies are providing solutions through “super-cleaning” processes that deliver rPET meeting stringent food-contact safety standards. These high-temperature and vacuum decontamination methods ensure that post-consumer PET flakes are suitable for beverages and packaged foods. Systems such as the VACUNITE process are already approved by the U.S. FDA and European EFSA, making them commercially viable at scale. For PET streams that are heavily contaminated or colored, depolymerization offers an alternative. By breaking PET down into its base monomers—purified terephthalic acid (PTA) and monoethylene glycol (MEG)—and then re-polymerizing, chemical recycling can generate virgin-quality PET indistinguishable from fossil-derived alternatives. Companies like Koch Technology Solutions and Ioniqa Technologies are advancing catalytic depolymerization to transform mixed-color and low-grade PET waste into high-value, food-grade rPET. These technologies not only alleviate supply shortages but also expand the scope of recyclable inputs, making them a cornerstone opportunity for closing the PET circular economy loop.

Development of Bio-Based PTA and MEG for Renewable PET

The push toward decarbonization is creating momentum for renewable PET, manufactured from bio-based feedstocks instead of fossil fuels. PET consists of PTA and MEG, and while Coca-Cola’s pioneering PlantBottle used bio-based MEG derived from sugarcane as early as 2009, its renewable content was capped at 30%. The untapped potential lies in commercializing bio-based PTA to complement bio-MEG, enabling the production of 100% bio-based PET bottles. Current R&D is exploring sources such as agricultural waste, sugarcane derivatives, and even captured CO₂ as feedstocks. Once scaled, bio-PET offers a “drop-in” solution, meaning it can be manufactured on existing infrastructure and recycled within the same streams as fossil-derived PET, avoiding disruptions to the circular economy. This compatibility ensures adoption is not limited by technology gaps and makes bio-PET highly attractive for brands committed to net-zero targets. By reducing reliance on petroleum-based inputs while maintaining recyclability, bio-based PET represents one of the most promising long-term opportunities for the packaging industry, combining renewable sourcing with circular design.

Competitive Landscape: Global PET Packaging Leaders Are Driving Innovation, Sustainability, and High-Performance Packaging Solutions

The PET packaging market is dominated by key players leveraging material science expertise, manufacturing innovation, and sustainable solutions to provide high-performance, versatile packaging.

Amcor plc: Expanding Sustainable PET Packaging Across Healthcare and Industrial Applications

Amcor offers a wide range of PET containers, bottles, jars, and flexible films for food, beverage, and healthcare markets. Innovations include PowerPost™, a lightweight PET bottle. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica and partnered with a paint brand to introduce containers with 50% recycled content. The company’s core strengths lie in global manufacturing capabilities, material science expertise, and vertical integration, supporting recyclability and brand differentiation.

ALPLA Group: Leading the Circular Economy with Recycled and Reusable PET Packaging

ALPLA specializes in blow-molded bottles, caps, and preforms, with a strong focus on reusable and refillable PET formats. In January 2025, ALPLA announced plans to double its recycling capacity to 700,000 tonnes by 2030 and inaugurated a PET recycling plant in South Africa in October 2024. Its core strengths include blow-molding expertise, extensive recycling infrastructure, and circular business model, positioning ALPLA as a leader in rPET development.

Plastipak Packaging, Inc.: Driving High-Performance PET Packaging with Closed-Loop Innovations

Plastipak manufactures PET bottles, jars, and preforms for food, beverage, and consumer goods industries. In August 2025, the company highlighted bottle-grade rPET, bio-based resins, and advanced barrier technologies at Drinktec. It also invested in packaging talent development. Plastipak’s strengths include container design innovation, proprietary manufacturing, and closed-loop recycling focus, delivering sustainable and high-performance PET solutions.

Berry Global Inc.: Delivering Sustainable Rigid and Flexible PET Packaging Across Multiple Sectors

Berry Global produces a wide range of PET containers with high PCR content. In February 2025, Berry Global partnered with VOID Technologies for high-performance sustainable films and collaborated with a pet food brand to create 100% recycled treat canisters. Its strengths lie in product portfolio diversity, expertise in rigid and flexible packaging, and B Circular sustainability range, emphasizing circular economy solutions.

Resilux NV: Pioneering rPET Solutions for High-Quality, Barrier-Enhanced PET Packaging

Resilux manufactures PET preforms and bottles for beverages, edible oils, and sauces, offering customized barrier properties. Its Poly Recycling division converts PET containers into food-grade rPET. Core strengths include manufacturing expertise, in-house recycling, and circular economy commitment, supporting bottle-to-bottle solutions. Resilux’s strategic focus centers on sustainable PET packaging innovation and long-term circular business growth.

PET Packaging Market Share Insights, 2025-2034

Rigid Packaging Holds Majority Share by Type in the PET Packaging Industry

Rigid packaging dominates the PET packaging industry with 65% share, anchored by the global prevalence of PET bottles for water, carbonated soft drinks (CSDs), juices, and edible oils. Bottles remain the flagship format due to PET’s unique combination of clarity, light weight, shatter resistance, and superior CO₂ and moisture barrier properties. Lightweighting innovations have significantly reduced resin usage per unit while maintaining strength, improving cost-efficiency and sustainability. At the same time, the accelerated adoption of recycled PET (rPET) is reshaping the rigid packaging segment, with beverage multinationals increasingly pledging 25–50% rPET integration in line with global regulatory mandates. Preforms hold a strong intermediate share, serving as the logistical backbone of the beverage supply chain, where “blow-fill” systems allow efficient transport and on-demand bottle manufacturing. Closures and caps are another critical contributor, driven by regulatory requirements like EU-mandated tethered caps to minimize litter and ensure recyclability. While flexible PET packaging, including films and laminates, accounts for a smaller portion of the market, it is growing rapidly in applications like specialty pouches and laminates for food, balancing space efficiency and lightweighting with challenges in recyclability. The sheer scale and resilience of rigid PET packaging affirm its indispensable role in global beverage, food, and household sectors.

Food & Beverages Command Overwhelming Market Share by End-User in the PET Packaging Industry

The food and beverage sector accounts for 78% of end-user demand in the PET packaging market, making it the undisputed engine of growth. Bottled water, carbonated soft drinks, and ready-to-drink beverages drive the bulk of this demand, supported by PET’s exceptional clarity, durability, and lightweight properties that make it superior to glass and metal alternatives. PET is also indispensable in packaging sauces, spreads, dairy products, and fresh produce trays, further consolidating this dominance. The rise of sustainability commitments has led leading food and beverage companies to embrace rPET and closed-loop recycling systems, ensuring compliance with evolving extended producer responsibility (EPR) regulations. Personal care and cosmetics represent a valuable growth niche, leveraging PET’s glass-like aesthetics and moldability into unique shapes that enhance brand storytelling. Pharmaceuticals rely on PET for moisture-sensitive formulations like syrups and tablets, where compliance with FDA and USP standards is essential. Household and industrial applications, though smaller, utilize PET for cleaning products, detergents, and chemicals, where barrier performance and cost-efficiency justify its use over HDPE. Ultimately, the overwhelming dominance of food and beverages highlights PET packaging’s unmatched versatility, cost competitiveness, and alignment with consumer demand for safe, convenient, and sustainable packaging solutions.

United States PET Packaging Market Driven by Smart Solutions and rPET Adoption

The United States PET packaging market is undergoing a rapid transformation, fueled by strong demand for smart, sustainable, and durable solutions across food, beverages, pharmaceuticals, and personal care. A growing trend is the use of smart packaging technologies such as QR codes and NFC-enabled labels, which enhance consumer engagement and ensure product authenticity. At the same time, major brands are investing in refillable and reusable packaging systems to reduce waste and foster brand loyalty.

Sustainability remains a key growth driver, with companies like Plastipak Packaging and Amcor plc leading the adoption of post-consumer recycled PET (rPET). The pharmaceutical sector is also a significant contributor, with PET bottles widely used for syrups and liquid medications due to their lightweight, shatter-resistant nature. The Association of Plastic Recyclers (APR) is piloting initiatives to improve recycling of household flexible packaging, reinforcing circular economy goals. Furthermore, innovations in barrier technologies to enhance resistance against oxygen, moisture, and UV light are extending product shelf life, ensuring PET remains indispensable in the U.S. market.

China PET Packaging Market Shaped by Regulation and Social-Commerce Growth

The China PET packaging market is being strongly influenced by the government’s GB 23350-2021 regulation, which restricts excessive packaging and compels companies to reduce material use. This has led to widespread adoption of thinner PET structures and paperboard sleeves for secondary packaging. Simultaneously, the country’s booming social-commerce channels are redefining packaging aesthetics, with a clear consumer preference for clean, minimalist, and matte-finish designs.

The skincare segment represents one of the largest end-use sectors for PET packaging, with brands utilizing airless jars and pumps to highlight clean beauty and efficacy. Flexible PET-based refill pouches are also gaining popularity in bath and shower categories as part of waste reduction strategies. Investments in high-end packaging are rising, illustrated by Ushopal’s multi-million-dollar investment in fragrance brand Documents, signaling confidence in premium domestic brands. Together, these dynamics underscore how China’s PET packaging industry balances sustainability, design innovation, and scalability to meet surging demand.

Germany PET Packaging Market Led by Bio-Based Innovation and Pharmaceutical Demand

The Germany PET packaging market is a European leader in advancing bio-based and biodegradable PET alternatives in response to strict environmental regulations. German companies are investing heavily in high-performance barrier coatings to protect sensitive products, particularly in the food and pharmaceutical sectors, where PET packaging is valued for durability and shelf-life extension.

Smart pharmaceutical packaging is emerging as a key innovation area, with RFID-enabled PET bottles and containers improving product traceability and preventing counterfeiting. The market is also witnessing a significant surge in recycled PET (rPET) adoption, supported by the EU’s ambitious recycling targets. Events like CosmeticBusiness 2025 highlight ongoing R&D into plant-based materials and sustainable production technologies, ensuring that Germany remains at the forefront of PET packaging innovation and eco-compliance.

United Kingdom PET Packaging Market Driven by EPR, DRS, and Recycling Targets

The United Kingdom PET packaging market is being reshaped by regulatory frameworks such as the Plastic Packaging Tax, which imposes £217.85 per metric ton on packaging containing less than 30% recycled content. Combined with the Extended Producer Responsibility (EPR) framework, this has created strong financial incentives for brands to adopt recycled PET (rPET) and other sustainable solutions.

A significant milestone was the launch of a world-first mechanical recycling plant in 2023, capable of producing food-grade recycled polypropylene, with similar innovations boosting PET recovery. The planned Deposit Return Scheme (DRS) for drinks containers in 2027 is expected to push PET bottle recycling rates above 90% within three years of operation. Consumer demand for plastic-free and sustainable packaging continues to rise, driving the adoption of rPET bottles, FSC-certified paperboard, and hybrid PET-aluminum solutions. These shifts position the UK as one of the most regulation-driven PET packaging markets globally.

India PET Packaging Market Growing with Investments and Single-Use Plastic Ban

The India PET packaging market is expanding rapidly, supported by government regulations and strong domestic manufacturing capacity. The ban on single-use plastics enforced on July 1, 2022, has significantly accelerated the adoption of PET alternatives. Jindal Poly Films (JPFL Films) has invested over INR 700 crore in new PET and film production lines in Nashik, boosting supply for both domestic and export markets. Similarly, Uflex Limited and Cosmo Films are expanding production to capture the rising demand.

The country’s growing middle-class population and disposable income are fueling demand for premium packaged goods, while the rise of e-commerce platforms requires robust, tamper-proof, and aesthetically designed PET packaging. Additionally, the Bureau of Indian Standards (BIS) IS 11968:2019 framework sets voluntary specifications for hygiene and labeling of packaged goods, indirectly supporting PET adoption. With one of the world’s largest BOPP and BoPET capacities, India is positioning itself as a global hub for PET packaging production and export.

Japan PET Packaging Market Driven by Recycling Agreements and Advanced Preservation

The Japan PET packaging market is anchored by strong recycling goals and advanced material science. The Japan Soft Drink Association has set an ambitious target of 50% bottle-to-bottle recycling of PET by 2030, aligning with national sustainability commitments. To support this, JEPLAN Group, Ito En, and Far East Ishizuka Green PET signed a cooperation agreement with Miyakonojo City to integrate chemical and mechanical recycling technologies, enabling higher recovery and reducing reliance on petroleum-derived resins.

Japan’s packaging sector also prioritizes advanced preservation technologies, which are crucial for reducing food waste and supporting the country’s e-commerce and home delivery expansion. Companies such as Toppan Inc. and RM Tohcello Co. Ltd. are collaborating on high-barrier PET packaging solutions that maintain freshness while being recyclable. With a culture that values both convenience and sustainability, Japan is driving innovation in eco-friendly, recyclable PET packaging solutions that balance performance and environmental impact.

PET Packaging Market Report Scope

PET Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$85.2 Billion

|

|

Market Size (2034)

|

$137.9 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (PET, rPET, Bio-based PET, PE, PP, Others), By Packaging Type (Rigid Packaging, Flexible Packaging, Closures & Caps, Preforms), By Application (Beverages, Food, Personal Care & Cosmetics, Pharmaceuticals, Household & Industrial Chemicals, Pet Food), By End-User (Food & Beverage Companies, Personal Care & Cosmetics Companies, Pharmaceutical Companies, Household & Industrial Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Plastipak Packaging, Inc., Alpla Group, Huhtamaki Oyj, Silgan Holdings Inc., Sonoco Products Company, Resilux NV, Graham Packaging Company, Mondi Group, Toray Industries, Inc., Uflex Limited, Sealed Air Corporation, AptarGroup, Inc., Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

PET Packaging Market Segmentation

By Material

- PET

- rPET

- Bio-based PET

- PE

- PP

- Others

By Packaging Type

- Rigid Packaging

- Flexible Packaging

- Closures & Caps

- Preforms

By Application

- Beverages

- Food

- Personal Care & Cosmetics

- Pharmaceuticals

- Household & Industrial Chemicals

- Pet Food

By End-User

- Food & Beverage Companies

- Personal Care & Cosmetics Companies

- Pharmaceutical Companies

- Household & Industrial Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in PET Packaging Market

- Amcor plc

- Berry Global, Inc.

- Plastipak Packaging, Inc.

- Alpla Group

- Huhtamaki Oyj

- Silgan Holdings Inc.

- Sonoco Products Company

- Resilux NV

- Graham Packaging Company

- Mondi Group

- Toray Industries, Inc.

- Uflex Limited

- Sealed Air Corporation

- AptarGroup, Inc.

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and systematic methodology to analyze the PET Packaging Market, integrating both qualitative and quantitative research techniques to ensure accuracy and actionable insights. The research process begins with an extensive review of primary sources, including interviews with key industry stakeholders such as manufacturers, suppliers, distributors, and regulatory bodies, to capture real-time market dynamics. Secondary research is conducted using verified industry reports, company filings, trade publications, and government databases to validate historical trends, technological developments, and competitive strategies. Market sizing and forecasting are derived using a combination of top-down and bottom-up approaches, accounting for global and regional consumption patterns, regulatory impacts, sustainability mandates, and material innovations such as rPET and bio-based PET adoption. USDAnalytics applies advanced statistical models to calculate CAGR, revenue projections, and market share distribution, while cross-verifying these estimates against real-world supply chain and production data. The methodology also factors in disruptive trends such as mono-material design, lightweighting strategies, advanced barrier technologies, and digital/consumer-centric packaging innovations, ensuring that the analysis not only reflects current market realities but also provides forward-looking insights tailored for strategic decision-making by industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.