Syrup Market Size, Overview, and Growth Outlook (2025–2034)

Global Syrup Market Projected to Reach $76 Billion by 2034 Driven by Health, Flavor, and Functional Innovation

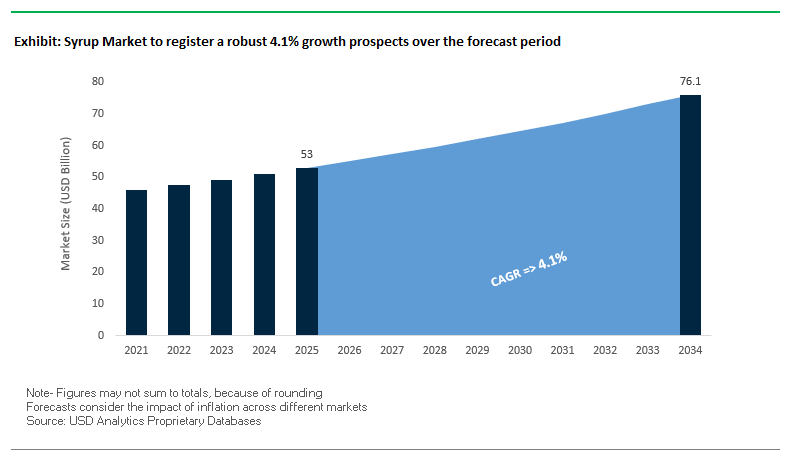

The global syrup market is forecast to grow from $53 billion in 2025 to $76.1 billion by 2034, at a CAGR of 4.1%, reflecting rising consumer demand for indulgent, functional, and health-oriented syrups. This diverse sector encompasses traditional sweeteners, flavor-infused syrups, and functional formulations, making it a critical component of the food and beverage landscape.

Key Insights for Industry Professionals:

- The shift toward clean-label, natural ingredients is prompting manufacturers to innovate with maple, fruit, honey, and other natural syrups.

- Rising health consciousness is fueling growth in low-sugar, sugar-free, and plant-based alternatives, using ingredients like stevia, monk fruit, and allulose.

- Flavor diversification is critical, with demand for exotic and nostalgic flavors such as ube, pandan, and cinnamon roll driving new product launches.

- Functional syrups with fiber, protein, and prebiotics are aligning with the wellness-focused consumer trend.

- Manufacturers are increasingly combining taste, functionality, and sustainability to cater to both foodservice and retail channels.

The syrup industry is positioned at the intersection of consumer taste innovation, health-conscious formulations, and functional food trends, providing opportunities for differentiation through product quality, flavor variety, and functional benefits.

Market Analysis: Recent Developments Highlight Strategic Partnerships and Product Innovations Driving Syrup Industry Growth

The global syrup industry is witnessing dynamic changes, marked by strategic partnerships, product launches, and acquisitions to enhance innovation, health focus, and geographic expansion. In September 2025, Monin launched its Cinnamon Roll syrup, targeting seasonal consumer demand for nostalgic autumn and winter flavors. In August 2025, Tate & Lyle partnered with BioHarvest to develop the next generation of plant-based ingredients, underscoring sustainability and health-conscious innovation.

Brand expansion into new regions is also evident. Hair Syrup, a UK-based haircare brand, partnered with Lyko in August 2025 to enter the Scandinavian market, reflecting syrup’s increasing application beyond traditional beverages. Ingredion and Alliance Bio-Refineries collaborated in July 2025 to scale bio-based solutions for food and beverage applications. Meanwhile, Roquette acquired IFF Pharma Solutions (July 2025) to strengthen its foothold in pharmaceutical and nutraceutical syrups, highlighting cross-sector expansion.

Strategic investments in production and innovation centers reinforce market growth. Cargill acquired Mig-Plus (June 2025) to expand its animal nutrition business and unveiled a transformed Innovation Center in Singapore (April 2025) for food innovation, focusing on syrups and sweeteners. The Hershey Company launched sugar-free syrup lines (March 2025) to meet health-conscious consumer demand, while Tate & Lyle (November 2024) and Ingredion (October 2024) invested in sweetener and plant-based protein facilities to drive innovation in reduced-sugar and plant-based syrup products.

Trends and Opportunities in the Syrup Market

Reformulation with Natural Sweeteners and Sugar Reduction

The syrup market is undergoing a fundamental reformulation shift as consumer health preferences and corporate ESG commitments converge. Global food and beverage brands are aggressively reducing sugar content to align with regulatory pressures and consumer demand for healthier alternatives. For instance, Coca-Cola’s 2024 corporate profile revealed a 4% reduction in average sugar content since 2019, with low- and no-sugar beverages now making up 45% of its portfolio. This reflects how reformulation strategies have become a competitive differentiator across product lines.

Targeted innovations are further driving this trend. Hershey’s launch of its 30% less sugar chocolate syrup in India, free from artificial sweeteners, highlights the potential for plant-based natural alternatives to penetrate mainstream markets. Beyond traditional sweeteners, rare sugars such as allulose are gaining traction due to their ability to mimic sucrose functionality while providing zero-calorie, clean-label appeal. Blends of allulose with monk fruit or stevia provide 1:1 sugar replacements that retain bulk and mouthfeel in liquid formulations, solving long-standing challenges for syrup applications. This reformulation wave positions natural sweeteners not only as healthier alternatives but also as strategic enablers of premium syrup innovation.

Transition to Lightweight and Recyclable Packaging Formats

Alongside reformulation, syrup packaging is undergoing a significant transformation to meet sustainability and efficiency goals. Lightweighting is a leading driver, as brands transition from heavy glass bottles to PET containers, reducing both material consumption and carbon emissions. A case study demonstrated that new reusable PET bottles are up to 90% lighter than glass and can cut carbon footprints by 30% during transportation. This weight reduction not only lowers logistics costs but also aligns with corporate net-zero targets.

Circular packaging strategies are accelerating with the use of recycled PET (rPET). Advanced technologies now allow bottles with up to 100% rPET content, maintaining durability across 25 reuse cycles. By integrating recyclability with reusability, syrup brands can reduce plastic dependency while maintaining product integrity. This transition is particularly relevant in regions like the EU, where packaging directives under the PPWR are pushing companies toward higher recycled content and reuse targets. As a result, sustainable packaging has become an essential competitive lever for syrup manufacturers.

Development of Syrups for the Functional Beverage and Nutrition Sector

A key growth opportunity lies in repositioning syrups beyond sweetness into the functional nutrition category. With the functional beverage market projected to expand rapidly, syrups are being reformulated with nutritional enhancements. Companies like Ingredion are offering syrup solutions enriched with soluble corn fiber, which not only reduces sugar content but also adds digestive and immune support benefits. This reflects a broader trend of syrups being redefined as carriers of bioactive ingredients, targeting health-conscious consumers.

However, functional formulation introduces technical challenges. The addition of vitamins, minerals, probiotics, or botanicals can alter viscosity, taste, and stability. Companies investing in specialized syrup bases with advanced stabilizers, emulsifiers, and natural flavor enhancers can overcome these issues. The opportunity lies in creating customized, science-backed functional syrups that deliver measurable health outcomes without compromising sensory appeal. This positions syrups as value-added wellness solutions within the booming nutrition and dietary supplement landscape.

Precision Fermentation for Sustainable Novel Syrups

Precision fermentation is emerging as a game-changer in sustainable syrup production, offering scalable pathways to create novel sweeteners and functional bio-compounds. Unlike traditional agricultural methods, fermentation consumes fewer resources and produces sweet proteins and specialty sugars at industrial scale. A 2025 company report highlights its ability to produce proteins thousands of times sweeter than sucrose, providing brands with sustainable sweetener options that require minimal formulation quantities.

Beyond sweet proteins, microbial fermentation is enabling the production of high-value functional sugars such as human milk oligosaccharides (HMOs). These bioactive compounds, vital for infant nutrition and functional supplements, can now be industrially produced using precision fermentation. This unlocks a premium market for next-generation syrups designed for specialized applications, including early-life nutrition, sports recovery, and clinical dietary products. With the growing demand for sustainability and advanced functionality, precision fermentation positions syrups at the intersection of biotechnology, health, and consumer innovation.

Competitive Landscape: Key Global Syrup Manufacturers Are Leveraging Innovation and Sustainability to Capture Market Share

The syrup industry’s competitive landscape is shaped by major players investing in plant-based ingredients, functional formulations, and geographic expansion, reflecting a focus on health-conscious and clean-label trends.

Tate & Lyle PLC: Driving Plant-Based Innovation and Sugar Reduction Through Strategic Partnerships

Tate & Lyle specializes in corn-based and non-GMO sweeteners, starches, and functional ingredients. In August 2025, the company partnered with BioHarvest to pioneer plant-based ingredients for healthier food and beverages. Tate & Lyle leverages vertical integration, corn refining expertise, and sustainability-focused R&D to deliver innovative solutions for global markets, emphasizing sugar reduction and functional fortification.

Cargill, Incorporated: Expanding Global Presence and Food Innovation Capabilities in Syrups and Sweeteners

Cargill offers a wide range of sweeteners, including high-fructose corn syrup and glucose syrup. In June 2025, Cargill acquired Mig-Plus to expand its animal nutrition business and enhanced its Innovation Center in Singapore (April 2025) for regional syrup and sweetener development. Cargill’s extensive manufacturing network, global reach, and vertical integration support its focus on innovation, sustainability, and circular economy initiatives.

Ingredion Incorporated: Scaling Plant-Based and Low-Calorie Syrup Solutions to Meet Health Trends

Ingredion focuses on starches, sweeteners, and texturizers, including corn syrups and glucose syrups. The company invested in a plant-based protein facility in Nebraska (October 2024) and is actively developing its Allulose platform as a low-calorie sugar alternative. Ingredion’s vertical integration enables efficient production, sustainable formulations, and rapid scaling for food and beverage manufacturers.

Archer Daniels Midland (ADM): Combining Agricultural Expertise with Innovative Syrup and Sweetener Solutions

ADM converts corn into sweeteners such as corn syrup and high-fructose corn syrup. With over 50 patents worldwide, ADM focuses on product optimization, lightweighting, and continuous innovation. Its strengths lie in agricultural integration, materials expertise, and global scale, supporting a strategy of high-quality, compliant, and sustainable syrup solutions.

Roquette Frères: Strengthening Pharmaceutical and Nutraceutical Syrup Offerings Through Strategic Acquisitions

Roquette provides plant-based ingredients, starches, and syrups for multiple industries. In July 2025, the company completed the acquisition of IFF Pharma Solutions, enhancing its position in pharmaceutical and nutraceutical markets. Roquette’s vertical integration, materials expertise, and plant-based focus enable the delivery of high-quality, innovative syrup solutions aligned with global health and sustainability trends.

Syrup Market Share Insights, 2025-2034

Corn-Based Syrups Lead Market Share by Source in the Global Syrup Industry

Corn-derived syrups account for 45% of the syrup market in 2025, making them the most widely used source due to their cost efficiency, high sweetness potency, and multifunctional characteristics. High-fructose corn syrup (HFCS) and glucose syrups dominate as the backbone of the processed food and beverage industry, particularly in North America where cost and performance advantages drive mass adoption. Their functional roles—including moisture retention, flavor enhancement, browning, and freezing point control—make them indispensable across beverages, bakery, and confectionery. Sugarcane-based syrups follow with a 25% share, strongly preferred in regions where natural sucrose is culturally and commercially dominant, and for applications demanding a clean-label appeal. Maple and agave syrups represent premium alternatives, positioned for their natural, plant-based profiles that appeal to health-conscious and specialty food consumers. Rice and fruit-based syrups remain niche but are expanding in organic, allergen-free, and artisanal product categories. Collectively, this segmentation highlights how corn-based syrups dominate global volume, while cane and natural syrups capture premium and regionalized demand.

Beverages Sector Dominates Market Share by Application in Syrup Industry

The beverages sector holds 50% of the global syrup market share in 2025, underscoring its role as the single largest consumer of syrups worldwide. Syrups are foundational to carbonated soft drinks, fruit beverages, flavored waters, sports and energy drinks, coffee syrups, and ready-to-drink teas, where they not only provide sweetness but also stabilize flavor and extend shelf life. This sector’s dominance is reinforced by the massive global volume of beverage consumption and the high syrup-to-product ratio required in manufacturing. Bakery and confectionery, along with food service, form the next critical segments, where syrups deliver sweetness, texture, moisture retention, and functional properties like browning and viscosity control. Dairy and frozen desserts leverage syrups to optimize taste and mouthfeel, while the household segment provides steady retail demand for cooking, baking, and homemade beverages. Pharmaceuticals and cosmetics, though niche, illustrate the functional versatility of syrups, with roles in liquid medication excipients and humectants for personal care formulations. Overall, this segmentation demonstrates how the beverage industry anchors syrup demand globally, while bakery, food service, and dairy sustain secondary but essential consumption channels.

India: Ethanol Diversion Policy and Growing Syrup Demand in Food & Beverage

The India syrup market is undergoing a significant transformation driven by the government’s recent policy changes in ethanol production. In the 2025–26 Ethanol Supply Year (ESY), the Indian government lifted the cap on sugar diversion, allowing unrestricted use of sugarcane juice, syrup, B-heavy molasses, and C-heavy molasses for biofuel production. This move is designed to help sugar mills manage their inventories, generate timely payments to farmers, and align with the national target of achieving 20% ethanol blending in gasoline by 2025–26. The Indian Sugar and Bio-Energy Manufacturers Association (ISMA) estimates that 450–500 crore liters of ethanol will be produced from the diversion of 5 million tonnes of sugar, balancing both energy security and price stability in the sugar sector.

Alongside biofuel diversification, the domestic food and beverage industry is fueling syrup demand. India’s bakery, ice cream parlors, and café culture are expanding rapidly, driving higher consumption of flavored syrups. There is also rising consumer preference for indigenous fruit syrups, functional blends, and herbal syrups in health beverages, reflecting a growing wellness trend. Key players like E.I.D.-Parry, Balrampur Chini Mills, and Bajaj Hindusthan are expanding ethanol capacity while simultaneously capturing opportunities in food-grade syrup markets, making India a critical growth hub.

United States: Shift Toward Low-Calorie and Clean-Label Syrup Formulations

The United States syrup market is heavily influenced by health regulations and consumer trends. The U.S. Food and Drug Administration (FDA) has intensified its focus on reducing added sugars and encouraging alternative sweeteners, spurring innovation in low-calorie syrups formulated with stevia, monk fruit, and natural plant-based extracts. This regulatory push aligns with rising consumer health consciousness, leading to a surge in organic, non-GMO, and clean-label syrups. Major manufacturers are investing in organic certifications and transparent labeling to meet growing retail and e-commerce demand.

Innovation hubs are central to market evolution. For instance, Tate & Lyle’s Chicago innovation center and its collaboration with PepsiCo on sugar-reduction trials underscore the focus on next-generation syrup solutions. Similarly, The Kraft Heinz Company is diversifying its portfolio with organic syrup lines in response to consumer demand in supermarkets. Meanwhile, specialty coffee shops, cocktail bars, and artisanal beverage makers are driving premium syrup demand, with gourmet and exotic flavors increasingly gaining traction. Together, these shifts reinforce the U.S. as a hub for health-driven and premium syrup innovations.

European Union: Health-Driven Regulations and Sustainable Packaging Integration

The European Union syrup market is shaped by stringent health and sustainability regulations. The European Food Safety Authority (EFSA) continuously evaluates food additives and sweeteners, directly impacting syrup formulations used in food and beverages. EU-wide public health campaigns advocating reduced sugar intake are accelerating the demand for fiber-enriched syrups and stevia-based blends, with companies like Tate & Lyle and Mondelēz International leading adoption.

From a packaging perspective, the Packaging and Packaging Waste Regulation (PPWR) that came into force in February 2025 is driving a transition toward a circular economy, compelling syrup producers to shift to recyclable, lightweight, and sustainable containers. Companies like Mondi are leveraging this regulation to expand sustainable laminates and flexible packaging tailored for syrup applications. With simultaneous consumer demand for healthier options and regulatory focus on eco-friendly packaging, the EU syrup market is positioning itself as both health- and sustainability-centric.

Brazil: Sugarcane Leadership and Sustainable Syrup Packaging

The Brazil syrup market benefits from the country’s dominant position as a global sugarcane producer. Beyond food applications, sugarcane derivatives are being used in bio-based materials for packaging. For instance, Braskem and Raízen have partnered to produce bio-based polyethylene (PE) from ethanol, which is also used in syrup containers. This strengthens Brazil’s leadership in both syrup production and sustainable packaging integration.

The National Center for Research in Energy and Materials (CNPEM) has developed antistatic packaging from sugarcane bagasse, initially aimed at electronics, but applicable across industries, including syrups. Regulatory support from Brazil’s National Solid Waste Policy (PNRS) ensures that companies adopt reverse logistics systems, making producers responsible for post-consumer collection and recycling of syrup packaging. Combined with Brazil’s Law No. 15,088 (January 2025) banning the import of plastic waste, these measures reinforce the nation’s transition to renewable, circular packaging systems alongside its syrup industry.

China: Premium Syrup Demand and Regulatory Push for Sustainable Packaging

The China syrup market is expanding rapidly, fueled by rising urban consumption and evolving regulations. Under the 14th Five-Year Plan, new rules effective June 1, 2025, require express delivery companies to adopt eco-friendly and reusable packaging, which indirectly influences syrup packaging design for retail and e-commerce. Simultaneously, China’s large consumer base and urban dining culture are propelling syrup demand across beverages, confectionery, and bakery applications, especially in flavored and premium syrup categories.

The market is also seeing a shift toward sophisticated packaging solutions with barrier protection, anti-counterfeiting features, and premium designs, enhancing consumer trust in branded syrups. Reports from the Ellen MacArthur Foundation and Tsinghua University highlight the need for China to scale up high-quality recycled plastic systems, a move that will impact future syrup container design. Together, the interplay of policy, consumer preference, and packaging innovation makes China one of the most dynamic syrup markets globally.

Japan: Plastic Resource Circulation Laws and Innovation in Syrup Containers

The Japan syrup market is advancing in alignment with national sustainability strategies. The Plastic Resource Circulation Strategy mandates that all plastic packaging be reusable or recyclable by 2025, a rule reinforced by the Plastic Resource Circulation Promotion Law (2025), which targets the redesign of 12 categories of single-use plastics. For syrup packaging, this regulatory environment accelerates the shift toward compostable and bio-based materials.

The Ministry of Health, Labor and Welfare (MHLW) has further tightened safety through its positive list system for synthetic food containers effective June 2025, ensuring only approved materials are used for food contact applications like syrups. This combination of regulatory rigor and consumer preference for eco-friendly, health-conscious products is creating opportunities for innovation in biomass-based bottles, recyclable laminates, and lightweight syrup packaging solutions. Japan’s syrup market, therefore, stands at the intersection of health compliance, sustainability, and premiumization.

Syrup Market Report Scope

Syrup Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$53 Billion

|

|

Market Size (2034)

|

$76.1 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Source (Corn, Sugarcane, Maple, Agave, Rice, Other), By Product Type (Natural Syrups, Artificial/Flavored Syrups, Fruit Syrups, Chocolate Syrups, Coffee & Tea Syrups, Pancake & Waffle Syrups), By Application (Beverages, Bakery & Confectionery, Dairy & Frozen Desserts, Pharmaceuticals, Cosmetics & Personal Care, Food Service, Household), By End-Use Industry (Food & Beverage, Pharmaceutical, Personal Care), By Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Sales, Specialty Stores)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archer-Daniels-Midland Company, Cargill, Incorporated, The Kraft Heinz Company, The J.M. Smucker Company, Monin Inc., The Hershey Company, Sensient Technologies Corporation, Ingredion Incorporated, Roquette Frères, Tate & Lyle PLC, Torani (S.F. & Co.), DaVinci Gourmet, Amoretti, B&G Foods, Inc., Kerry Group plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Syrup Market Segmentation

By Source

- Corn

- Sugarcane

- Maple

- Agave

- Rice

- Others

By Product Type

- Natural Syrups

- Artificial/Flavored Syrups

- Fruit Syrups

- Chocolate Syrups

- Coffee & Tea Syrups

- Pancake & Waffle Syrups

By Application

- Beverages

- Bakery & Confectionery

- Dairy & Frozen Desserts

- Pharmaceuticals

- Cosmetics & Personal Care

- Food Service

- Household

By End-Use Industry

- Food & Beverage

- Pharmaceutical

- Personal Care

By Distribution Channel

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Sales

- Specialty Stores

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Syrup Market

- Archer-Daniels-Midland Company

- Cargill, Incorporated

- The Kraft Heinz Company

- The J.M. Smucker Company

- Monin Inc.

- The Hershey Company

- Sensient Technologies Corporation

- Ingredion Incorporated

- Roquette Frères

- Tate & Lyle PLC

- Torani (S.F. & Co.)

- DaVinci Gourmet

- Amoretti

- B&G Foods, Inc.

- Kerry Group plc

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-layered research methodology to deliver actionable insights on the global syrup market. Our approach integrates both primary and secondary research, drawing on interviews with key industry stakeholders, including syrup manufacturers, ingredient suppliers, distributors, and foodservice experts, to validate market dynamics, emerging trends, and technological advancements. Secondary research involves systematic analysis of company reports, regulatory frameworks, trade journals, and market databases to capture historical data, recent product innovations, and competitive landscapes. USDAnalytics also applies quantitative modeling techniques to forecast market growth, segment performance, and geographic trends, accounting for macroeconomic indicators, consumer behavior shifts, and health and sustainability-driven demand. Particular emphasis is placed on tracking functional and plant-based syrup innovations, packaging sustainability developments, and regulatory impacts across major markets such as the U.S., EU, China, India, Japan, and Brazil. All findings undergo rigorous validation through triangulation, ensuring accuracy and reliability for strategic decision-making by buyers, manufacturers, and investors seeking a complete view of the syrup industry’s growth trajectory, competitive landscape, and innovation opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.