Rigid Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Global Rigid Packaging Market Set to Reach $499.5 Billion by 2034 Driven by PET, Aluminum, and Glass Innovation

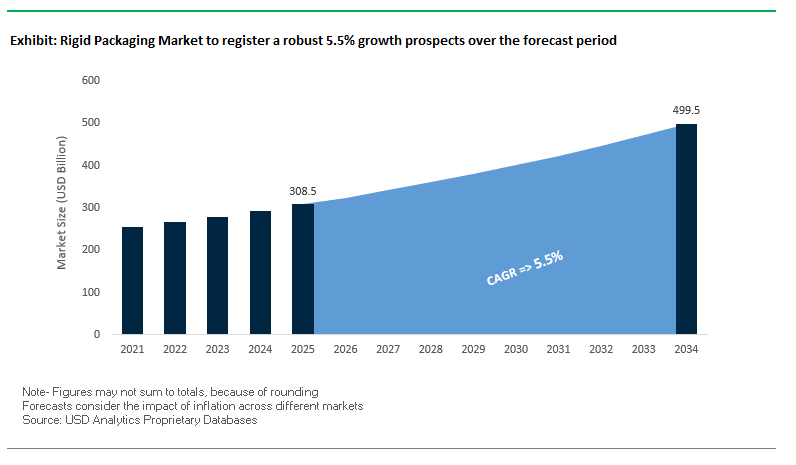

The global rigid packaging market is projected to grow from $308.5 billion in 2025 to $499.5 billion by 2034, representing a CAGR of 5.5%. Growth is propelled by rising consumer demand for PET containers, increased integration of recycled materials, and innovation in glass and aluminum packaging. Rigid packaging solutions are widely used across food, beverage, personal care, and industrial sectors, offering durability, protection, and premium presentation.

Key Insights for industry professionals and buyers:

- PET Dominance in Food & Beverage: Approximately 40% of North American food and beverage products are packaged in PET bottles and containers, highlighting its clarity, durability, and recyclability.

- Shift to Recycled Materials: The EU Packaging and Packaging Waste Regulation (PPWR) drives companies to integrate 25% or more recycled content by 2025.

- Aluminum Can Sustainability: Over 70% of aluminum cans are recovered for recycling in Europe and North America, making them a highly sustainable choice.

- Glass Packaging Innovation: Successful trials using 100% biofuel in glass furnaces have substantially reduced greenhouse gas emissions.

- Consumer & Regulatory Pressure: Demand for environmentally responsible packaging is increasing, fueled by both government regulations and consumer preferences.

- Premiumization Trends: Glass and aluminum offer premium visual appeal, enhancing brand perception in beverages and food packaging.

The rigid packaging industry demonstrates a balance between sustainability, consumer convenience, and premium product presentation, making it a key growth segment in global packaging.

Market Analysis: Strategic Acquisitions and Sustainable Material Innovation Are Shaping the Rigid Packaging Market

The rigid packaging sector is witnessing accelerated growth through strategic acquisitions, product innovations, and sustainability-focused initiatives. In August 2025, Amcor and Flügger launched a paint container made with 50% recycled material, exemplifying circular economy practices. The same month, Inteplast acquired German plastics board maker Con-pearl, expanding its capabilities in rigid plastics. LyondellBasell launched Pro-fax EP649U, a polypropylene impact copolymer for thin-walled injection molding, meeting the growing demand for lightweight and durable food packaging.

In July 2025, the Amcor-Berry Global merger was completed, creating a diversified global leader with a wide array of rigid packaging solutions. O-I Glass validated early achievement of key sustainability goals and continued its biofuel trials in March 2025, demonstrating a strong focus on green manufacturing. Collaborative efforts, such as the Linde-O-I Glass OPTIMELT® TCR installation, further illustrate the industry’s commitment to technological integration and emission reduction.

The market is also shaped by continuous capability expansion and sustainability investments. In April 2025, ALPLA enhanced its injection molding capacities with an acquisition in Italy, strengthening its global presence.

Rigid Packaging Market: Emerging Trends and Opportunities Driving Sustainable Growth

Strategic Investment in Advanced Recycling Infrastructure for rPET

One of the most defining trends in the rigid packaging market is the direct corporate investment in advanced recycling facilities to secure a sustainable supply of food-grade recycled PET (rPET). Beverage and consumer packaged goods (CPG) companies are moving from sourcing recycled material on the open market to backing infrastructure development directly. A prime example is Circulate Capital’s Ocean Fund, which, with support from PepsiCo and The Coca-Cola Company, invested over $10 million in Srichakra Polyplast to establish India’s first food-grade plastic recycling facility in Hyderabad. This facility produces recycled PET pellets suitable for direct use in food and beverage packaging, closing the loop and advancing a circular economy model. By mid-2025, five Indian manufacturers—including Reliance Industries, Uflex, Ester Industries, Ganesha Ecopet, and Srichakra Polyplast—received official approval to produce food-grade rPET, enabling global brands to meet both regulatory compliance mandates and internal sustainability goals. This trend demonstrates how rigid packaging is evolving into a strategically secured value chain, where sustainability and reliability of supply are intertwined.

Lightweighting and Material Reduction in Metal Packaging

Another major trend is the ongoing lightweighting of rigid metal packaging, particularly in beverage cans and food containers. According to Metal Packaging Europe, technological advancements have reduced the aluminum and steel required for cans by nearly 50% over the past four decades, bringing a 500ml aluminum can down to around 16 grams today. This material efficiency has a cascading effect on logistics, transportation, and sustainability performance. A logistics study showed that reducing can size and weight led to up to 50% lower greenhouse gas emissions in transport, due to decreased freight loads and improved efficiency across distribution networks. Beyond carbon footprint reductions, lightweighting also translates into significant cost savings, making it a win-win strategy for manufacturers and brand owners. As rigid packaging continues to be scrutinized under environmental regulations, material reduction through lightweighting is becoming a critical competitive differentiator for metal packaging companies globally.

Adoption of Smart and Connected Packaging for Consumer Engagement

The rigid packaging sector is increasingly viewed as a platform for digital transformation, with smart and connected features offering powerful consumer engagement opportunities. Brands are embedding QR codes and NFC tags into bottles, jars, and rigid containers to enhance authentication, traceability, and interactive consumer experiences. A 2025 smart packaging industry report highlights how these features help brands combat counterfeiting—particularly in pharmaceuticals, premium beverages, and cosmetics—while also providing real-time access to product provenance, nutritional information, and sustainability credentials. In parallel, the upcoming EU Digital Product Passport (DPP) under the Ecodesign for Sustainable Products Regulation (ESPR) will mandate data carriers on packaging. This regulation is expected to transform rigid packaging into a digital gateway, enabling companies to disclose material sourcing, recycled content levels, and end-of-life disposal instructions. For forward-looking manufacturers, this presents a clear opportunity to integrate smart features into rigid formats as both a compliance tool and a consumer trust-building mechanism.

Development of Mono-Material and Polymer-Barrier Solutions

A second opportunity lies in the transition from multi-material rigid packaging to mono-material barrier solutions that maintain functionality while enhancing recyclability. Global packaging leaders such as Toppan are spearheading this shift with mono-material barrier packaging solutions composed entirely of PET or PE. These structures are designed to replicate the performance of multi-layered laminates, while enabling simplified recycling streams. A technical report from SpecialChem highlighted a breakthrough in PE-based thermoformed rigid packaging that delivers high puncture resistance and strong oxygen barriers, making it a viable alternative for sensitive food products such as cheese and ready meals. By eliminating the complex separation process required for multi-material formats, mono-material rigid packaging helps brands meet extended producer responsibility (EPR) targets and align with global recycling mandates. This innovation positions mono-material barrier solutions as a critical enabler of both compliance and brand-led sustainability commitments, reinforcing the long-term resilience of rigid packaging in competitive markets.

Competitive Landscape: Leading Rigid Packaging Companies Are Driving Market Growth Through Innovation and Sustainability

The global rigid packaging industry is highly competitive, with leading players leveraging technological innovation, sustainable materials, and global distribution networks to enhance market presence. Companies focus on PET, glass, aluminum, and specialty plastics to meet consumer demand for durable, eco-friendly, and premium packaging.

Amcor plc: Expanding Global Leadership Through Mergers and Sustainability Initiatives

Amcor offers a diversified portfolio of high-performance PET bottles and jars across beverages, food, and personal care. The July 2025 merger with Berry Global expanded its geographic footprint and product offerings. The company emphasizes sustainability with initiatives like AmFiber Performance Paper and innovative closures that enhance product safety and recyclability. Amcor aims for 100% of packaging to be recyclable or reusable by 2025, driving both market leadership and environmental impact reduction.

O-I Glass, Inc.: Pioneering Sustainable Glass Manufacturing with Biofuel Trials

O-I Glass specializes in premium glass containers widely used in food and beverages. The company has focused on its Fit to Win initiatives to maintain competitive strength and announced strategic business transformations in France. With biofuel trials and partnerships with Linde for OPTIMELT® TCR Technology, O-I Glass is leading the decarbonization and sustainable manufacturing movement within the glass packaging industry.

Sealed Air Corporation (SEE): Innovating Through Automation, Digitalization, and Circular Packaging

SEE delivers innovative solutions in rigid packaging and fluid systems, including CRYOVAC® and LIQUIBOX® products. Strategic acquisitions like APS and Liquibox complement its goal of a Net Positive Circular Ecosystem. SEE is also focused on automation and digital solutions, aiming to double its automation portfolio by 2027 and digitize over 80% of sales, positioning itself as a sustainability and technology-driven leader.

Sonoco Products Company: Leveraging Recycled Materials to Deliver Durable and Eco-Friendly Packaging

Sonoco provides a variety of rigid packaging including paper, plastic, and composite cans, with 100% recycled fiber for paper containers. Its advanced barrier solutions ensure product protection and premium presentation. Sonoco operates multiple mills globally, allowing supply chain control and scalability, while emphasizing eco-friendly solutions and sustainability-focused innovations.

Silgan Holdings Inc.: Driving Innovation in Metal and Plastic Rigid Containers

Silgan Holdings is a major supplier of rigid containers and closures in the food and consumer goods sector. In August 2025, the company completed the acquisition of a European packaging firm to expand regional presence. Silgan emphasizes product preservation, shelf life enhancement, and sustainability, making it a key player in the global rigid packaging market.

Rigid Packaging Market Share Insights, 2025-2034

Bottles & Jars dominate Market Share by Product Type in the Rigid Packaging Industry

Bottles and jars hold the largest share at 28% within rigid packaging, underpinned by their universal use across food & beverages, healthcare, and personal care industries. Their dominance stems from high-volume global production, with PET, HDPE, and glass containers forming the backbone of retail-ready packaging. Innovation in this segment centers on light-weighting, recyclability, and recycled content integration (rPET, rHDPE), driven by regulatory and brand sustainability commitments. Boxes and cartons remain a retail powerhouse, balancing branding and protection, particularly in folding cartons and rigid cases for premium goods. Trays and containers are expanding rapidly due to the rise in fresh food packaging, ready-to-eat meals, and convenience-focused formats. Caps and closures, often overlooked, form a massive high-volume segment where tamper evidence, child-resistance, and reduced resin use are key growth drivers. Cans remain resilient as beverage mainstays, supported by aluminum’s infinite recyclability and premium perception. Industrial applications like drums, pails, and IBCs retain steady demand for chemical, hazardous, and bulk transport, while blisters and clamshells preserve niches in pharmaceuticals and retail theft prevention despite recyclability scrutiny. The diversity of this market reflects rigid packaging’s status as a cornerstone of global manufacturing and trade.

Food & Beverages lead Market Share by End-Use Industry in the Rigid Packaging Industry

Food & beverages represent nearly 45% of rigid packaging demand, cementing their role as the largest consumer of rigid formats globally. The sector’s requirements span extended shelf life, moisture/oxygen barriers, resealability, and strong shelf appeal, all of which align with rigid packaging strengths. Healthcare and pharmaceuticals, while smaller in volume, are high-value users where sterility, tamper evidence, and regulatory compliance take precedence over cost, making blister packs, pill bottles, and sterile containers indispensable. Industrial use remains a bulk driver, with lubricants, paints, and construction materials relying on strength and chemical resistance to secure supply chains. Cosmetics and personal care stand out for their design and aesthetics, leveraging glass jars, premium bottles, and aluminum tins as both functional and branding assets. Chemicals form another critical segment, demanding UN-certified drums, jerricans, and HDPE pails for hazardous material compliance. Meanwhile, e-commerce is reshaping demand through secondary packaging needs, favoring rigid solutions that reduce freight damage and improve shipping efficiency. Collectively, these end-use patterns reinforce rigid packaging’s indispensable role in ensuring product integrity, safety, and consumer trust across global industries.

European Union: PPWR and ESPR Driving Circularity in Rigid Packaging

The European Union rigid packaging market is undergoing a fundamental transformation with the implementation of the Packaging and Packaging Waste Regulation (PPWR) in February 2025. This legislation mandates that by January 2030, all plastic components of rigid packaging must contain minimum percentages of post-consumer recycled content, creating direct incentives for recyclers and packaging converters to scale infrastructure. The regulation also introduces reuse targets and mandates per capita packaging waste reductions, pushing companies toward rigid reusable formats such as refillable bottles and containers.

The EU is further advancing circularity through Deposit Return Systems (DRS), which secure high-quality recycled streams essential for rigid PET, HDPE, and PP containers. Complementing this, the Ecodesign for Sustainable Products Regulation (ESPR), effective from mid-2024, mandates a Digital Product Passport, ensuring transparency in product origin and compliance. Additionally, the restriction of PFAS in food contact packaging from August 2026 is accelerating the shift toward safer material alternatives. Corporate innovation is evident, with Amcor and Flügger launching a paint container with 50% recycled content, setting a benchmark for sustainability-driven rigid packaging design.

United States: EPA Goals and Corporate Innovation Boosting Rigid Packaging Demand

The United States rigid packaging market is shaped by the EPA’s national recycling goal to increase the U.S. recycling rate to 50% by 2030, alongside state-level Extended Producer Responsibility (EPR) laws. For instance, Maryland’s legislation requires that Producer Responsibility Organizations (PROs) cover 90% of packaging waste management costs by 2030, placing accountability squarely on manufacturers.

Innovation is central to U.S. market growth. Berry Global has introduced customizable rigid bottles with up to 100% PCR content, while Chlorophyll Water became the first bottled water brand in the country to achieve Clean Label Project Certification by using 100% rPET bottles. Fresh Del Monte Produce’s partnership with Arena Packaging to deploy reusable plastic containers (RPCs) for bananas demonstrates how rigid packaging can cut both food waste and carbon emissions. Infrastructure investments through the Infrastructure Investment and Jobs Act are also bolstering advanced recycling capabilities, ensuring a steady supply of high-quality recycled resin for rigid formats.

China: Government Regulations and Premium Market Demand Strengthening Rigid Packaging

The China rigid packaging market is being reshaped by the government’s “14th Five-Year Plan”, which emphasizes reducing plastic pollution and strengthening circular economy practices. From June 2025, new regulations require express delivery companies to adopt eco-friendly and reusable packaging, a major boost to demand for durable rigid containers.

Corporate initiatives are aligning with this policy direction. For example, Coca-Cola’s Hong Kong operations are now producing bottles with 100% rPET sourced in China, a landmark move showcasing the country’s growing recycling infrastructure. At the same time, the rising demand for premium food and beverage products is pushing brands to adopt higher-quality rigid packaging with enhanced durability and aesthetic appeal. Government tax incentives for remanufacturing are further encouraging companies to invest in green rigid packaging solutions, strengthening China’s position as a fast-expanding market for high-performance rigid formats.

India: EPR Mandates and Cold-Chain Growth Driving Rigid Packaging Expansion

The India rigid packaging market is experiencing significant momentum with the Plastic Waste Management (Amendment) Rules, 2024, which require Extended Producer Responsibility (EPR) compliance for producers and importers. From April 1, 2025, all PIBOs must include a minimum of 30% recycled content in Category I rigid plastics, driving adoption of recycled PET, HDPE, and PP. Meanwhile, the Food Safety and Standards Authority of India (FSSAI) is drafting guidelines for rPET use in food packaging, further legitimizing recycled rigid formats.

The government’s ethanol-blended fuel initiative is also fueling demand for HDPE jerrycans and rigid containers, while the PM Gati Shakti plan is boosting cold-chain infrastructure. This has led to increased reliance on rigid PET preforms for dairy, juices, and frozen foods. Additionally, India is seeing a surge in advanced manufacturing technologies, including injection molding and thermoforming, which enable complex and precision-driven rigid packaging formats for pharmaceuticals and personal care products. Together, regulatory, industrial, and consumer drivers are positioning India as one of the fastest-growing rigid packaging markets globally.

Japan: Plastic Circulation Strategy and Bio-PP Integration Reshaping Rigid Packaging

The Japan rigid packaging market is advancing rapidly under the Plastic Resource Circulation Strategy, which requires all plastic packaging to be reusable or recyclable by 2025. By 2030, the government targets the introduction of 2 million tons per year of bio-polypropylene (bio-PP), underscoring its commitment to bioplastics in rigid applications.

Japanese firms are pioneering material science innovations. Collaborations between LyondellBasell, Shiseido, Futamura Chemical, and Iwatani are incorporating bio-based PP into cosmetic packaging, aligning luxury brands with sustainability. Furthermore, the Plastic Resource Circulation Promotion Law (2025) mandates the redesign of 12 single-use plastic products, spurring demand for reusable and compostable rigid alternatives. Production efficiency is also scaling, with Coca-Cola Bottlers Japan Inc. (CCBJI) unveiling an aseptic production line in Aichi Prefecture, capable of producing 600 small PET bottles per minute, ensuring supply meets rising demand for convenience-oriented beverages.

Brazil: Reverse Logistics and Waste Import Ban Supporting Rigid Packaging Sustainability

The Brazil rigid packaging market is strongly influenced by the National Solid Waste Policy (PNRS), which emphasizes recycling, reuse, and waste reduction. To reinforce local sustainability, Law No. 15,088, effective January 2025, prohibits the import of solid waste, including plastic and metal, pushing industries to build domestic recycling capabilities for rigid packaging production.

A growing emphasis on reverse logistics systems requires producers to take responsibility for post-consumer collection and recycling of rigid packaging. This regulatory environment, combined with increasing demand for plastic trays and MAP/vacuum packaging for shelf-life extension, is shaping the industry’s growth trajectory. By promoting local recycling, reducing imports, and enhancing food preservation technologies, Brazil is positioning itself as a regional leader in sustainable rigid packaging adoption.

Rigid Packaging Market Report Scope

Rigid Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$308.5 Billion

|

|

Market Size (2034)

|

$499.5 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (Plastics, Glass, Metal, Paper & Paperboard), By Product Type (Bottles & Jars, Trays & Containers, Caps & Closures, IBCs, Drums & Pails, Blisters & Clamshells, Cans, Boxes & Cartons), By End-Use Industry (Food & Beverages, Healthcare & Pharmaceuticals, Cosmetics & Personal Care, Industrial, E-commerce, Chemicals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Silgan Holdings Inc., Sonoco Products Company, Ball Corporation, DS Smith Plc, Mondi Group, Greif, Inc., Graphic Packaging Holding Company, International Paper Co., WestRock Company, Crown Holdings, Inc., Huhtamaki Oyj, Orbis Corporation, Plastipak Holdings, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Rigid Packaging Market Segmentation

By Material

- Plastics

- Glass

- Metal

- Paper & Paperboard

By Product Type

- Bottles & Jars

- Trays & Containers

- Caps & Closures

- IBCs

- Drums & Pails

- Blisters & Clamshells

- Cans

- Boxes & Cartons

By End-Use Industry

- Food & Beverages

- Healthcare & Pharmaceuticals

- Cosmetics & Personal Care

- Industrial

- E-commerce

- Chemicals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Rigid Packaging Market

- Amcor plc

- Berry Global, Inc.

- Silgan Holdings Inc.

- Sonoco Products Company

- Ball Corporation

- DS Smith Plc

- Mondi Group

- Greif, Inc.

- Graphic Packaging Holding Company

- International Paper Co.

- WestRock Company

- Crown Holdings, Inc.

- Huhtamaki Oyj

- Orbis Corporation

- Plastipak Holdings, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust and comprehensive research methodology to deliver precise insights into the global rigid packaging market. Our approach integrates extensive secondary research, including regulatory frameworks, corporate sustainability disclosures, industry publications, and market reports, with primary interviews of key stakeholders such as manufacturers, brand owners, distributors, and end-users across food, beverage, healthcare, personal care, and industrial sectors. Market sizing and forecasting are derived from detailed analyses of material usage trends (PET, glass, aluminum, plastics, and paperboard), innovations in recycling and lightweighting, smart and connected packaging adoption, and premiumization strategies. USDAnalytics evaluates the impact of regional regulations—such as the EU PPWR and ESPR, U.S. EPR mandates, China’s 14th Five-Year Plan, and India’s Plastic Waste Management Rules—on sustainable packaging uptake. We also examine mergers, acquisitions, technological advancements, and corporate sustainability initiatives to provide actionable intelligence on CAGR, regional dynamics, end-use segmentation, and supply chain trends. This methodology ensures industry professionals receive an accurate, data-driven, and holistic understanding of growth opportunities, competitive positioning, and innovation trends within the rigid packaging market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.