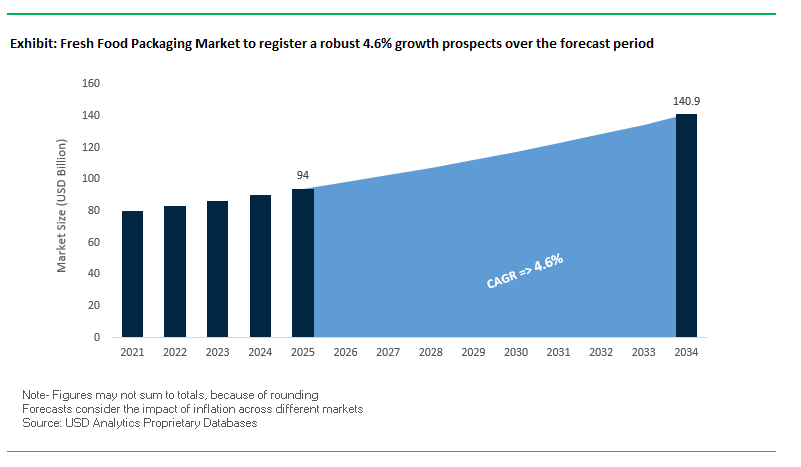

Fresh Food Packaging Market Overview: MAP/VSP, Mono-Material Films and PCR Content Power Growth (MV USD 94 Bn, 2025 → USD 140.9 Bn, 2034; CAGR 4.6%)

The fresh food packaging market is pivoting to shelf-life extension and circular packaging at scale. Solutions combining modified atmosphere packaging (MAP), vacuum skin packaging (VSP), high-barrier PE/PP lidding films, and fiber-based trays are displacing mixed laminates to meet retailer specs, FDA/EFSA food-contact rules, and EPR/PPWR-style recyclability mandates. Growth is concentrated in chilled proteins, produce, bakery, and ready-to-eat where line efficiency, seal integrity, and cold-chain performance determine total delivered cost.

Key insights at a glance

- Growth drivers: MAP/VSP formats delivering +3–10 days shelf-life uplift; anti-fog, easy-peel lidding that maintains visibility and seal strength; and automation-ready trays that boost OEE on high-speed lines.

- Sustainability: Rapid shift to mono-material PE/PP, rPET trays, and PCR content; fiber trays with barrier coatings where grease/moisture resistance is needed; label/adhesive systems optimized for wash-off.

- Risk & compliance: Tightening residue/NIAS limits and migration testing raise the bar for food-safe inks, adhesives, and coatings; end-to-end HACCP and lot-level traceability/UDI/QR now table stakes.

- Commercial levers: Light-weighting and right-sizing reduce resin per pack; digital printing enables frequent SKU changes and seasonal promos without inventory write-offs; retail-ready formats cut labor in stores.

Market Analysis: Shelf-Life Extension, Recyclability Mandates and Digital Traceability—Recent Developments

Momentum in fresh food packaging is anchored in shelf-life economics and recyclability. In July 2025, converters highlighted recycle-ready mono-PE/PP lidding films and anti-fog technologies tailored to refrigerated produce and protein MAP lines, aligning with retailer scorecards. June 2025 saw multiple partnerships around rPET tray loops and wash-off label systems that keep flakes clear for food-grade re-use, while May 2025 launches emphasized paper-plus-barrier trays for deli and bakery to displace EPS and reduce plastic intensity.

Digitalization is accelerating. In April 2025, suppliers rolled out QR/NFC-enabled smart labels for provenance, date coding, and recall speed—critical in fresh protein and prepared meals. Earlier, March 2025 reports flagged enzyme/antimicrobial additive packages enabling thinner films without compromising safety, and January 2025 pilots demonstrated closed-loop crate + liner systems for short-haul produce that cut shrink and damage. Regulatory cadence remained front-of-mind throughout 2024–2025, with retailers preparing for PPWR-style recyclability and recycled-content triggers and brand owners re-specifying from mixed laminates to mono-material plus barrier coatings to maintain machinability and seal performance.

Transformative Trends and High-Value Opportunities in the Fresh Food Packaging Market

Strategic Shift to High-Barrier, Mono-Material Recyclable Trays and Films

The fresh food packaging market is witnessing a decisive pivot toward mono-material polypropylene (PP) and polyethylene (PE) solutions, replacing non-recyclable multi-material laminates such as PS/PE or PET/PE. This strategic shift is driven by the need to ensure compatibility with polyolefin recycling streams while maintaining high oxygen and moisture barriers essential for fresh meat, fish, and ready meals. Multi-material packaging often cannot be efficiently sorted and is frequently incinerated or landfilled, pushing leading brands to adopt circular packaging solutions. Companies like Nestlé are piloting mono-material flexible packaging for baby food, and Unilever is integrating PE-based mono-material pouches, aligning with circular economy goals. Partnerships, such as Jindal Films and TotalEnergies, are advancing certified circular polypropylene in premium flexible food packaging through advanced recycling technology. This trend offers a high-value growth avenue by protecting product integrity, enhancing sustainability, and ensuring compliance with emerging regulatory standards. The value chain is evolving, requiring resin manufacturers and converters to collaborate closely to produce films compatible with existing machinery without significant modifications.

Integration of Active Packaging Technologies for Shelf-Life Extension

Fresh food packaging is evolving into active preservation systems that combat food waste by controlling the internal package environment. Technologies include oxygen scavengers in tray walls, ethylene absorbers in fruit punnets, and moisture-control pads under fresh meat, extending shelf life without chemical preservatives. The driver behind this trend is the need to maintain product quality and reduce waste; even trace oxygen can trigger oxidation affecting color, taste, and nutritional value. Studies show zero-oxygen packaging systems can reduce oxygen levels to undetectable limits, preserving desirable fresh meat color. In fresh produce, active ethylene-controlling, paper-based packaging is increasingly adopted to prolong freshness. Global initiatives, such as OSY Group’s Xtend antimicrobial coating, are being tested with partners across the UK, New Zealand, Australia, Singapore, South Africa, and India, demonstrating worldwide adoption. Active packaging solutions provide a high-value growth avenue, offering economic benefits to brands and retailers by reducing spoilage while delivering fresher products to consumers.

Development of Bio-Based and Home-Compostable Formats for Fresh Produce

There is a significant opportunity to develop home-compostable, high-performance packaging for fresh produce using bio-based materials such as seaweed, chitosan, and PHA. These materials must provide breathability, moisture resistance, and anti-fogging properties while breaking down effectively in home composting systems. Regulatory drivers and consumer demand for sustainable alternatives are accelerating adoption, as international policies phase out conventional plastics in produce packaging. Academic research shows that chitosan, alginate, and starch-based nanocomposite films can offer oxygen and moisture barriers, antimicrobial activity, and enhanced mechanical properties. Projects funded by institutions like the Sustainable Packaging Innovation Lab (SPIL) at Clemson University demonstrate the potential for bio-based solutions, including compostable adhesives and labels. This opportunity promotes new collaborations across material science companies, packaging manufacturers, and the agricultural sector, ensuring integration into existing supply chains and compliance with performance requirements.

Smart Packaging with Integrated Freshness and Traceability Sensors

Beyond active preservation, intelligent fresh food packaging represents a high-value opportunity. Integration of time-temperature indicators (TTIs) and colorimetric freshness sensors provides real-time quality information to consumers and retailers, reducing uncertainty-driven waste and building brand trust. TTIs show cumulative cold chain exposure through irreversible color changes, while novel sensors detect spoilage metabolites like ammonia or biogenic amines. Academic research highlights colorimetric sensor arrays that visually indicate meat spoilage, offering an accessible and reliable freshness measure. Commercializing smart packaging allows manufacturers to offer products that actively reduce food waste, enhance safety, and provide economic value to the supply chain. This trend fosters a data-driven and interconnected value chain, requiring collaboration between packaging manufacturers, technology firms, and food scientists, transforming fresh food packaging into a high-tech, value-added product.

Competitive Landscape: MAP/VSP Specialists and Circular Materials Leaders Redefine the Category

The market is led by integrated players capable of materials science + converting + machinery support, ensuring food safety, line speed, and circularity without trading off shelf appeal.

Technology leadership centers on high-barrier mono-materials, anti-fog/easy-peel lidding, VSP films, rPET/fiber trays, and automation-ready tooling. Commercial advantage accrues to suppliers with PCR supply security, food-contact compliance expertise, and in-house testing for migration/NIAS and seal reliability across MAP atmospheres and cold-chain extremes.

Amcor anchors recycle-ready pouches and lidding in fresh proteins & produce

Amcor pairs AmPrima™-style recycle-ready films with MAP/VSP know-how for meat, seafood, cheese, and produce. Its portfolio spans anti-fog, peelable, and high-barrier PE/PP lids, skin films, and rPET rigid formats, engineered for high-speed sealers and form-fill-seal lines. Differentiators include global technical service, downgauging while holding OTR/MVTR, and PCR integration that passes food-contact and migration tests. Strategy focuses on mono-material adoption without retooling penalties.

Sealed Air (Cryovac) scales VSP and MAP systems for protein shelf-life gains

Sealed Air’s Cryovac® platform integrates films, trays, and equipment to deliver vacuum skin packaging and MAP with consistent seals and presentation. Its anti-fog, puncture-resistant skins and reseal lidding reduce purge and extend freshness, directly lowering shrink. Line-side services optimize OEE, while format libraries help customers pivot from EPS to recycle-ready structures with minimal change parts. Emphasis: shelf-life economics + circular redesign.

Huhtamaki advances fiber and rPET trays with barrier science

Huhtamaki brings fiber-based trays with bio/aqueous barrier coatings alongside rPET solutions for ready meals, produce, and bakery. Tooling is tuned for oven/microwave-safe options, and designs target EPR ease with clear recycling pathways. Its innovation pipeline addresses grease/moisture resistance and seal-through-contamination to maintain line speed on lidding stations. Positioning: hybrid paper-plastic systems that meet retailer plastic-reduction targets.

Mondi integrates EcoSolutions across films, paper, and hybrid fresh formats

Mondi’s EcoSolutions approach offers mono-PE/PP lidding and flow wraps, plus paper-plus-barrier where it’s fit-for-purpose. Produce and bakery lines benefit from anti-fog clarity, easy-open features, and digital-printable surfaces for SKU agility. Mondi’s ability to pick paper or plastic based on LCAs and MRF compatibility helps brands hit recyclability KPIs while preserving machinability and seal performance on legacy assets.

Berry Global supplies PCR-enabled rigids and high-clarity films

Berry’s portfolio covers rPET trays, light-weighted closures, and PE/PP high-barrier lidding tuned for MAP/VSP applications. Proprietary recycling and food-grade PCR streams de-risk supply for retailers targeting recycled-content thresholds. On lines, Berry supports downgauging, seal-through-contamination, and anti-fog specs that maintain visibility in chill cabinets. Strategic thrust: scale circular materials without sacrificing throughput or pack integrity.

Fresh Food Packaging Market Share Insights

Flexible Packaging Secures Majority Market Share by Packaging Type in Fresh Food Packaging

Flexible packaging leads the fresh food packaging market with a projected 60% share in 2025, driven by its versatility, material efficiency, and ability to deliver strong preservation benefits. Lightweight films and bags are widely adopted for fruits, vegetables, meat, and bakery items, offering cost savings, reduced plastic consumption, and adaptability across product formats. Flexible solutions also enable advanced preservation technologies such as modified atmosphere packaging (MAP), which extends freshness and reduces waste in perishable foods. In addition, transparent films enhance product visibility and consumer appeal at retail. Rigid packaging, while smaller in share, remains indispensable for delicate and high-value fresh foods. Trays, clamshells, and molded fiber cartons are essential for protecting berries, eggs, seafood, and ready meals, providing both structural protection and stackability for logistics efficiency. Together, these dynamics highlight how flexible packaging dominates through volume and efficiency, while rigid formats secure critical value-added roles in fragile and high-risk categories.

Fruits and Vegetables Hold Largest Market Share by Application in Fresh Food Packaging

Fruits and vegetables represent 40% of the fresh food packaging market by 2025, making them the largest application segment by volume. The sheer scale of global produce consumption from bulk bags of root vegetables to protective clamshells for grapes and berries—drives this leadership. Packaging ensures not only protection from handling damage but also critical shelf-life extension, reducing food waste and enabling global distribution. The meat, poultry, and eggs segment follows as a high-value user, requiring rigid trays, absorbent pads, and specialized films to maintain freshness, safety, and visual appeal, with eggs further demanding molded pulp or fiber cartons for impact resistance. Prepared salads and ready-to-eat meals are the fastest-growing application, fueled by consumer demand for convenience and supported by rigid bowls and trays sealed with high-barrier lidding films and MAP technology. Dairy and seafood segments round out the market, with dairy relying on oxygen- and light-barrier packaging for freshness, while seafood requires highly specialized high-barrier solutions for super-chilled distribution. This segmentation reflects how fruits and vegetables dominate volumes, while proteins and prepared foods push packaging technology into high-performance, safety-focused solutions.

United States Fresh Food Packaging Market Driven by FDA Regulations and Sustainable Innovations

The U.S. fresh food packaging market is strongly influenced by a fragmented regulatory landscape, with California’s SB-54 Extended Producer Responsibility (EPR) law mandating a 25% plastic reduction by 2032 and establishing a $5 billion waste fund. This regulation is driving manufacturers to adopt sustainable packaging practices while complying with federal and state-level requirements. Technological advancements, such as Amcor’s AmFiber Performance Paper—a recyclable high-barrier laminated solution compatible with existing flow wrap machinery—highlight the push toward sustainable and high-performance packaging.

Corporate investments are accelerating growth, with Amcor’s planned acquisition of Berry Global Group, expected in mid-2025, consolidating resources to create a powerhouse with substantial R&D investments in sustainable solutions. Key applications are concentrated in e-commerce and direct-to-consumer (DTC) channels, fueled by the rise of online food delivery that requires durable, lightweight, and efficient packaging. The market’s focus on sustainability is evident through increased adoption of bio-based films and recyclable paperboard, reflecting strong consumer demand for environmentally responsible fresh food packaging solutions.

Germany Fresh Food Packaging Market Strengthened by Circular Economy Leadership and High-Barrier Solutions

Germany’s fresh food packaging market is shaped by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which requires all packaging to be fully recyclable or reusable by 2030 and phases out chemicals like PFAS. The country’s Packaging Act (VerpackG) promotes circular economy practices by incentivizing recycling-friendly designs and reusable containers, driving innovation in sustainable packaging.

Technological advancements, such as Syntegon’s SVX Agile vertical packaging machine capable of processing paper-based and mono-material films, are setting new standards for sustainable fresh food packaging. Demand is particularly strong in food, beverage, and personal care sectors, where consumers value premium, high-barrier packaging that extends shelf life and ensures product integrity. Germany’s leadership in sustainability and regulatory compliance positions it as a benchmark for high-performance, eco-conscious packaging solutions across Europe.

China Fresh Food Packaging Market Expands with Governmental Support and Advanced Manufacturing

China’s fresh food packaging market is benefiting from government initiatives targeting the “dual carbon” goal, promoting the adoption of sustainable materials and recycling practices. The March 2024 Action Plan for equipment upgrades and the revised GB/T 31268 standard, limiting excessive packaging, are reshaping production processes, particularly for e-commerce and food delivery sectors.

Technological adoption, including AI, automation, and “5G plus industrial internet” integration, is improving efficiency and flexible production capacity. Domestic manufacturing is emphasized, with local companies expanding production to substitute imported technologies. Rapid growth in online grocery and food delivery channels is a key driver, ensuring that China remains a major market for high-quality, circular fresh food packaging solutions.

India Fresh Food Packaging Market Fueled by Circular Economy Policies and Rapid Food Sector Growth

India’s fresh food packaging market is gaining momentum from government initiatives promoting circular economy practices, with FSSAI implementing regulations to ensure safe and hygienic packaging. Automated packaging systems are increasingly adopted, particularly in frozen and packaged food sectors like snacks and vegetables, to improve efficiency and product protection.

Corporate investments, supported by the Make in India initiative, are driving the development of new production facilities, exemplified by UFlex’s large-scale plants in Noida and Jammu. Expanding food and beverage, and personal care sectors, coupled with rising e-commerce penetration, are key growth drivers. The domestic food processing industry is projected to reach $535 billion by FY26, directly influencing demand for modern, high-performance fresh food packaging solutions.

Japan Fresh Food Packaging Market Emphasizes High-Performance Sustainable Films

Japan’s fresh food packaging industry is leveraging advanced precision manufacturing and sustainable materials. In September 2024, Toppan Inc., in collaboration with RM Tohcello Co. Ltd. and Mitsui Chemicals Inc., developed recycled BOPP film ready for mass production. Regulatory guidance from the Plastic Resource Circulation Act promotes environmentally-conscious packaging design and reduction of single-use plastics, influencing sustainable practices in food packaging.

The market is increasingly focused on high-performance, specialty films with superior barrier properties and IoT-enabled tracking solutions. Innovation in functionality, including easy-open tear notches and resealable closures, addresses the needs of aging populations and single-person households. Japan’s integration of technology and sustainability positions it as a leader in the Asia-Pacific fresh food packaging market.

Brazil Fresh Food Packaging Market Advances with Sustainable Materials and Digital Packaging

Brazil’s fresh food packaging market is being shaped by regulatory support and sustainability initiatives. In February 2025, Anvisa updated the country’s positive list of substances for food contact plastics, adding two new chemicals, highlighting a focus on food safety compliance. Technological adoption, including robotics and AI, is improving quality control, production efficiency, and defect detection across packaging lines.

The market is shifting toward premium and specialized digital packaging solutions that maintain product freshness while extending shelf life. Sustainability is a core focus, with innovations like Klabin’s EkoFlex flexible packaging paper demonstrating the industry’s commitment to eco-friendly alternatives. These advancements are enabling Brazil to meet growing domestic demand while positioning itself competitively in the global fresh food packaging market.

Fresh Food Packaging Market Report Scope

Fresh Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$94 Billion

|

|

Market Size (2034)

|

$140.9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Material Type (Plastic Films, Paper & Paperboard, Metal, Glass, Bio-Based/Biodegradable Films), By Packaging Type (Rigid Packaging, Flexible Packaging), By Application (Fruits & Vegetables, Meat, Poultry & Eggs, Seafood, Dairy Products, Prepared Salads & Ready-to-Eat Meals), By Technology (Modified Atmosphere Packaging, Vacuum Skin Packaging, Active & Intelligent Packaging)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Huhtamaki Oyj, Reynolds Consumer Products Inc., Berry Global Group, Inc., Sonoco Products Company, Sealed Air Corporation, WestRock Company, DS Smith Plc, ProAmpac, Pactiv Evergreen Inc., UFlex Ltd., Constantia Flexibles Group, Smurfit Kappa Group, Novolex Holdings, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fresh Food Packaging Market Segmentation

By Material Type

- Plastic Films

- Paper & Paperboard

- Metal

- Glass

- Bio-Based/Biodegradable Films

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Application

- Fruits & Vegetables

- Meat

- Poultry & Eggs

- Seafood

- Dairy Products

- Prepared Salads & Ready-to-Eat Meals

By Technology

- Modified Atmosphere Packaging

- Vacuum Skin Packaging

- Active & Intelligent Packaging

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fresh Food Packaging Market

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Reynolds Consumer Products Inc.

- Berry Global Group, Inc.

- Sonoco Products Company

- Sealed Air Corporation

- WestRock Company

- DS Smith Plc

- ProAmpac

- Pactiv Evergreen Inc.

- UFlex Ltd.

- Constantia Flexibles Group

- Smurfit Kappa Group

- Novolex Holdings, LLC

* List Not Exhaustive

Methodology

USDAnalytics employed a comprehensive research methodology to provide an in-depth analysis of the Global Fresh Food Packaging Market. Our approach integrated primary research, including interviews with packaging manufacturers, food processors, retailers, and regulatory authorities, alongside secondary research using company reports, trade journals, patent filings, and regulatory publications. Market sizing and forecasts were derived for material types (plastic films, paper & paperboard, metal, glass, bio-based/biodegradable films), packaging types (rigid, flexible), applications (fruits & vegetables, meat, poultry & eggs, seafood, dairy, prepared salads & ready-to-eat meals), and technologies (modified atmosphere packaging, vacuum skin packaging, active & intelligent packaging). We analyzed sustainability trends, mono-material adoption, circular economy initiatives, and smart packaging technologies, including QR/NFC-enabled traceability and time-temperature indicators. Regulatory compliance, including FDA, EFSA, PPWR, and EPR mandates, was assessed for global relevance. Competitive landscape evaluation highlighted key strategies of leaders such as Amcor, Huhtamaki, Sealed Air, Mondi, and Berry Global, emphasizing technological innovation, recyclable solutions, and high-barrier performance. Regional market dynamics spanning the U.S., Germany, China, India, Japan, and Brazil were also considered, ensuring actionable insights for industry professionals, investors, and supply chain stakeholders seeking growth, compliance, and innovation opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.