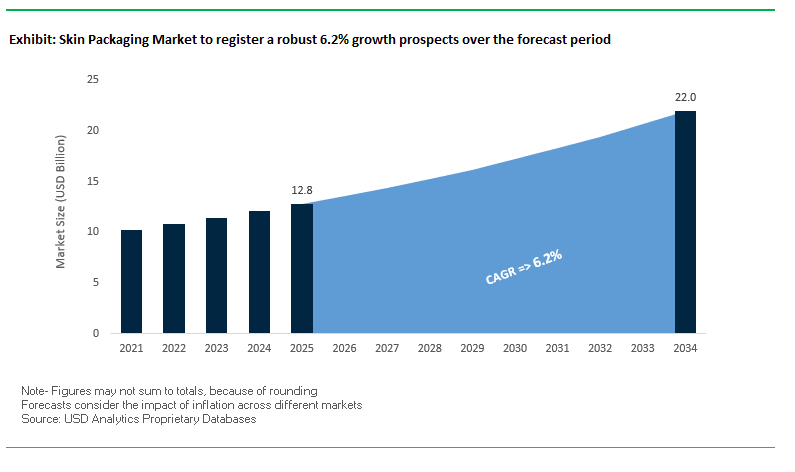

Skin Packaging Market Overview: Shelf-Life Gains and Sustainable Formats Propel Growth (MV: USD 12.8 Bn in 2025 → USD 22.0 Bn by 2034; CAGR 6.2%)

Executive summary for buyers & strategists. The global skin packaging market—spanning vacuum skin packaging (VSP) and carded skin packaging—is scaling as retailers and CPGs pursue longer shelf life, premium merchandising, and logistics resilience. By conforming film tightly to a tray or board, VSP reduces residual oxygen, curbs purge, and resists product shift during transport—critical in meat, seafood, cheese, ready meals, and DIY/industrial SKUs. At the same time, mono-material, recyclable, and fiber-hybrid structures help brands meet tightening sustainability KPIs without compromising pack integrity or clarity.

What decision-makers need to know

- Revenue trajectory: Market value expands from USD 12.8 Bn (2025) to USD 22.0 Bn (2034) at 6.2% CAGR, led by proteins, chilled convenience, and private-label upgrades.

- Shelf-life economics: High-barrier VSP (with oxygen/moisture barriers) demonstrably extends freshness, cuts markdowns, and reduces food waste—improving retailer margin.

- Retail impact: High-clarity, anti-fog films improve product visibility and perceived freshness; secure fit prevents transit damage and drip, enhancing e-commerce unboxing quality.

- Sustainability vector: Rapid shift toward light-weighted, recyclable films and paperboard tray systems (paper/PE <10% plastic) to align with EPR and retailer scorecards.

- Equipment compatibility: New skin tooling and seal platforms deliver higher throughput, easy-peel, and hermetic seals across PET, PP, PE, paperboard, and aluminum substrates.

Market Analysis: Recent Developments Signal Material Innovation and Circularity

Technology, material science, and M&A are reshaping the skin packaging industry. Awards and launches in 2025 spotlight circular content and barrier performance: in August 2025, Klöckner Pentaplast won a German Packaging Award (New Material) for kp 100% Tray2Tray®, validating tray-to-tray recycling in chilled foods. Also in July 2025, Amcor, with Volpak and Menshen, introduced an inverted pouch designed for recyclability and lower CO₂, underscoring brand demand for mono-material flexible formats. May 2025 saw DOW debut a lightweight shrink sleeve film to cut resin use in high-volume beverage packaging, and Chemco–Kandoi announced a INR 450-crore rPET JV to convert PET waste into industrial packaging feedstock. In February 2025, Berry Global and Mars converted pantry jars for M&M’S, SKITTLES, and STARBURST to 100% recycled plastic, removing >1,300 t/yr of virgin resin from that stream.

Momentum carried through 2024 with Lactips–Walki (November 2024) signing a JDA to accelerate fully recyclable paper-based food packaging, and Constantia Flexibles (October 2024) completing the Aluflexpack buyout to broaden high-barrier flexible capabilities. Critically for VSP, Stora Enso (April 2024) launched Trayforma BarrPeel, a barrier-coated paperboard for vacuum skin packaging enabling recyclable paperboard trays with <10% plastic, letting retailers upgrade shelf presentation and meet plastic-reduction commitments.

Strategic implications. Across proteins and premium chilled, buyers can now specify recycle-ready, paper-hybrid, or PCR-rich skin pack structures without sacrificing clarity, seal integrity, or machinability. Converters investing in laser scoring, anti-fog coatings, and easy-peel resins are winning high-velocity retail programs and e-commerce assortments.

Skin Packaging Market: Sustainability and Automation Driving Next-Gen Packaging Solutions

Strategic Integration of Post-Consumer Recycled (PCR) Content

The skin packaging market is rapidly evolving as brands integrate post-consumer recycled (PCR) content to align with corporate sustainability targets and regulatory expectations. A 2025 case study highlights the launch of skin packaging films incorporating 30% PCR PET content, allowing brand owners to meet public commitments around recycled content usage while maintaining high-performance standards. This transition is being driven by both Extended Producer Responsibility (EPR) frameworks and increasing consumer preference for visible sustainability in packaging.

However, the incorporation of PCR into high-clarity films presents significant technical challenges. Impurities in recycled PET can affect optical clarity, tensile strength, and sealing performance, which are critical for retail-ready applications like meat, seafood, and consumer goods. A technical brief from a leading film manufacturer outlines advancements in extrusion, filtration, and resin purification technologies that ensure PCR content retains the visual transparency and performance integrity required in skin packaging. These innovations are positioning PCR integration as a mainstream solution rather than a niche application.

Automation and Robotics for Labor Optimization and Efficiency

Automation is emerging as a critical driver in the skin packaging industry, responding to labor shortages and rising operational costs. A 2025 equipment launch showcased a fully automatic skin packaging system capable of delivering 16 cycles per minute, reducing dependency on manual labor while significantly increasing throughput. For high-volume processors in the food, electronics, and industrial goods sectors, this level of automation provides measurable gains in efficiency and cost reduction.

Beyond productivity, automation also enhances workplace safety and ergonomics. Technical documentation for modern systems highlights features like automatic product loading, robotic unloading, and eject/reject stations, which eliminate direct manual contact with hot products or sharp tooling. This not only reduces worker strain but also improves operational reliability and consistency, ensuring packaging runs meet stringent quality standards demanded by global retail supply chains.

Development of Mono-Material and Polymer-Compatible Solutions

One of the most promising opportunities lies in solving the recyclability challenge of multi-material skin packs, traditionally made of a plastic film sealed to a paperboard backing. This hybrid construction complicates recycling and lowers the recovery value of materials. The U.S. Plastics Pact has specifically identified skin packaging as a priority area for redesign under its sustainable packaging goals.

Innovators are developing mono-material solutions such as all-polyolefin skin packs, which can be recycled in a single stream. Recent 2025 reports on sustainable packaging highlight advances in PE-based barrier films that offer the strength, puncture resistance, and barrier properties needed for retail and e-commerce applications while remaining fully compatible with existing curbside or store drop-off recycling programs. This shift toward mono-materials has the potential to future-proof skin packaging against regulatory bans and unlock higher recovery rates in recycling systems.

Expansion into High-Growth E-Commerce Product Protection

With the exponential rise of e-commerce, skin packaging is finding new relevance in product protection and shipping efficiency. Unlike clamshells or foam inserts, skin packs form a tight “second skin” around products, securing them in place and preventing movement or shock damage during transit. This makes them particularly well-suited for electronics, tools, and fragile consumer goods shipped directly to customers.

Skin packaging also offers significant cost advantages in e-commerce fulfillment. By reducing the need for void fill and bulky protective materials, skin packs minimize dimensional weight (DIM weight)—a key cost metric in parcel shipping. Industry sources note that this packaging format can lower freight expenses and warehouse storage costs while providing brands with a more sustainable, space-efficient solution. As companies continue to prioritize last-mile optimization, the use of skin packaging in e-commerce is expected to expand rapidly.

Competitive Landscape: Leaders Advancing Barrier Science, Circularity, and Retail Aesthetics

The skin packaging competitive field is led by materials specialists and integrated converters scaling barrier films, recyclable substrates, and line-ready equipment. Each player below demonstrates distinct strengths in shelf-life extension, sustainability, and pack presentation.

Sealed Air Corporation advances Cryovac® skin formats for proteins and chilled foods

Sealed Air (SEE) leverages its Cryovac® franchise to deliver high-barrier VSP with anti-fog clarity and strong puncture resistance across PET/PE and PP trays. In August 2025, SEE expanded fiber protection with a Bubble Wrap® embossed paper line, reflecting a broader resin-reduction agenda that complements film light-weighting. The company’s global equipment footprint (skinners, thermoformers, sealers) enables systems selling—film + machinery + technical service—raising OEE and reducing seal failures. Strategic focus centers on sustainability, damage reduction, and automation to protect margin and meet retailer KPIs in meat, seafood, and deli.

Amcor scales recycle-ready SkinTite and paper-hybrid solutions for premium retail sets

Amcor’s skin portfolio (including AmPrima™ recycle-ready platforms and SkinTite technologies) targets high-clarity, easy-peel packs with mono-material pathways. In July 2025, Amcor collaborated with Volpak and Menshen on a recyclable inverted pouch, echoing its broader push to lower CO₂ and improve end-of-life outcomes; its SkinNova concept communicates up to 70% plastic reduction in certain specs. Amcor pairs material science with global converting and design services, helping brands migrate from MAP/clamshells to VSP on PET/PP/paperboard while preserving shelf standout and machinability.

Berry Global Group accelerates PCR integration and brand conversions at scale

Berry Global couples film extrusion, coating, and thermoforming to deliver skin films and trays suited to high-throughput retail protein lines. In February 2025, Berry partnered with Mars to shift pantry jars to 100% recycled plastic, signaling supply assurance and PCR quality that translates to food-grade applications. Berry’s skin solutions emphasize seal reliability, anti-fog optics, and downgauging, with a sustainability roadmap built on mechanical/advanced recycling and closed-loop partnerships for stable PCR feedstock.

Mondi Group enables paperboard-tray VSP and recyclable barrier upgrades

Mondi integrates paper & flexible packaging capabilities to deliver paperboard-tray + skin film combinations that reduce plastic intensity while maintaining barrier and seal strength. Strategic moves—such as the October 2024 agreement to acquire Schumacher Packaging assets—expand corrugated/board converting capacity and downstream control. Mondi’s engineering focus is on fiber-based trays, peelable films, and mono-material structures that fit retailer recyclability schemes, giving buyers credible EPR-aligned options without sacrificing pack performance.

Klöckner Pentaplast (kp) proves tray-to-tray circularity for chilled proteins

kp’s kp® Tray2Tray® program captures and recycles PET trays back into food-grade rPET trays, closing the loop in chilled foods. The platform won a German Packaging Award (August 2025) for kp 100% Tray2Tray®, evidencing circular material quality and supply-chain readiness. In skin packaging, kp supplies barrier skin films engineered for strong seals, high transparency, and anti-fog while supporting recycled content targets. Its strategy blends circular PET infrastructure with customer education on design-for-recycling, accelerating retailer rollouts in meat/seafood aisles.

Skin Packaging Market Share Insights, 2025-2034

Vacuum Skin Packaging (VSP) Dominates Market Share by Technology in the Skin Packaging Industry

Vacuum Skin Packaging (VSP) holds 65% of the skin packaging market, cementing its position as the preferred solution for fresh proteins and premium food products. VSP technology eliminates oxygen inside the pack, significantly extending shelf life, reducing food waste, and preserving product appearance with its “second skin” effect. This makes it particularly valuable for meat, poultry, seafood, and cheese, where freshness and visual quality directly influence consumer purchasing decisions. The premium retail presentation offered by VSP allows brands and retailers to command higher margins, further reinforcing its widespread adoption. At the same time, the method reduces purge (liquid loss), enhances hygiene, and supports clear branding opportunities through printable backing boards. While Modified Atmosphere Packaging (MAP) retains relevance for specific applications like delicate fish fillets and cheeses, VSP remains the dominant force due to its ability to deliver both extended shelf life and enhanced consumer appeal in the competitive fresh food market.

Food & Beverages Overwhelm Market Share by Application in the Skin Packaging Industry

The food and beverages segment accounts for 75% of all skin packaging applications, making it the overwhelming driver of market demand. The dominance of this application is rooted in its ability to provide a unique value proposition—maximum shelf life, superior product appearance, and reduced food waste—which is critical for the fresh food supply chain. Premium meat, poultry, seafood, and cheese categories are the primary users, where packaging not only protects but also serves as a marketing tool by enhancing visibility and consumer trust. The growing trend of premiumization in food retail has further boosted adoption, as consumers associate skin-packaged products with higher freshness and quality standards. In parallel, the sector benefits from the efficiency of automated VSP lines that can process high volumes for both supermarkets and export markets. While consumer goods, hardware, and medical devices leverage skin packaging for security and visibility, the food industry’s sheer volume consumption and high-value requirements ensure its lasting dominance in this specialized packaging segment.

United States: Recycling Mandates and Rising Demand for Vacuum Skin Packaging

The United States skin packaging market is expanding rapidly due to strong regulatory and industry initiatives focused on sustainability and efficiency. The U.S. Environmental Protection Agency (EPA) has set a national recycling target of 50% by 2030, which is directly influencing investments in recycling infrastructure for packaging materials, including skin films. The food industry is the largest adopter of vacuum skin packaging (VSP), particularly for meat, poultry, and seafood, as it extends shelf life, improves product visibility, and reduces food waste.

Manufacturers are also responding with material innovations to meet sustainability goals. Berry Global announced in April 2024 that it would begin producing certain films, including skin packaging, from post-consumer recycled (PCR) plastic. At the same time, automation and efficiency upgrades across food processing and packaging lines are becoming critical for cost control and productivity. The Association of Plastic Recyclers (APR) is further guiding best practices by endorsing washable inks and floatable films, enhancing the recyclability of skin packaging.

European Union: PPWR, ESPR, and the Shift Toward Circular Economy Solutions

The European Union skin packaging market is experiencing a structural transformation under the Packaging and Packaging Waste Regulation (PPWR), enforced in February 2025. The regulation mandates that all plastic parts of packaging, including skin films, must contain specified minimum percentages of post-consumer recycled content by 2030. Alongside PPWR, the Ecodesign for Sustainable Products Regulation (ESPR) is fostering the development of mono-material packaging solutions that are easier to recycle, which is especially important for skin packaging traditionally made of multi-layer laminates.

The ban on PFAS in food-contact packaging, effective August 2026, is another driver of innovation, pushing companies to develop alternative barrier coatings for skin films. In addition, the Single Use Plastics Directive (SUPD), active since July 2021, continues to influence the market by banning specific items and setting recycling requirements for PET bottles. These combined frameworks are steering the EU market toward sustainable, recyclable, and mono-material skin packaging formats.

China: Advanced Food Packaging and Green Policy Integration

The China skin packaging market is being shaped by both consumer demand for premium food packaging and government sustainability mandates. Under the “14th Five-Year Plan”, China is intensifying its control of plastic pollution, including June 2025 regulations that require eco-friendly, reduced, and reusable packaging in express delivery services. Additionally, Shanghai’s August 2025 policy imposes fines on enterprises that use non-compliant disposable packaging, a move that pressures manufacturers to innovate with compliant skin packaging solutions.

The market is also driven by rising demand for high-end food and consumer products, leading to the adoption of oxygen-barrier films and UV-stabilized skin packaging. This innovation supports food safety while appealing to quality-conscious consumers. To reinforce sustainability, the Chinese government is offering tax incentives for remanufacturing and green technology adoption, boosting the market for eco-friendly skin packaging.

India: EPR Regulations and E-Commerce Fuel Packaging Demand

The India skin packaging market is expanding rapidly due to strict regulations under the Plastic Waste Management (Amendment) Rules, 2024, which emphasize Extended Producer Responsibility (EPR). Effective July 1, 2025, all plastic packaging, including skin packaging, must be traceable via QR or barcodes, holding manufacturers accountable for recycling and waste management. While MSMEs are exempt, the responsibility falls on large manufacturers and importers, increasing demand for sustainable packaging solutions.

The rise of e-commerce and retail, combined with growth in the food and personal care sectors, is significantly boosting the use of skin packaging in India. The sector is also seeing government-backed modernization projects, such as investments in food supply chain infrastructure, which indirectly fuel demand for packaging that ensures freshness, safety, and extended shelf life. These factors make India a fast-emerging market for sustainable and traceable skin packaging solutions.

Japan: Plastic Resource Circulation Laws Accelerating Sustainable Alternatives

The Japan skin packaging market is being transformed by the Plastic Resource Circulation Strategy, which mandates that all packaging be reusable or recyclable by 2025. Reinforcing this, the Plastic Resource Circulation Promotion Law, effective in 2025, requires the redesign of 12 types of single-use plastic products, pushing companies to explore eco-friendly alternatives for films, including skin packaging.

Japan has also set a target to double renewable material usage by 2030 and is enforcing stricter waste-sorting systems to optimize recycling efficiency. Companies are actively exploring paper-based and compostable film alternatives to replace conventional plastic-based skin packaging. With its strong regulatory framework and focus on innovation, Japan is positioning itself as a leader in sustainable skin packaging development.

Brazil: Reverse Logistics and Waste Management Policies Strengthening Market

The Brazil skin packaging market is aligned with the National Solid Waste Policy (PNRS), which focuses on reuse, recycling, and responsible waste management. A major regulatory change came with Law No. 15,088, effective January 2025, which bans the import of solid waste and rejects, including plastic, encouraging the adoption of sustainable domestic packaging solutions.

Additionally, the Brazilian government is heavily promoting a reverse logistics system, holding producers accountable for the post-consumer recycling and disposal of their packaging, including skin packaging. With growing food retail and agricultural exports demanding extended shelf life packaging, skin packaging adoption is rising in Brazil. These regulations and market dynamics position the country as a key growth market for recyclable and circular skin packaging solutions in Latin America.

Skin Packaging Market Report Scope

Skin Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.8 Billion

|

|

Market Size (2034)

|

$22 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material (PE, PVC, Ionomer, PP, PET), By Technology (Vacuum Skin Packaging, Modified Atmosphere Packaging), By Application (Food & Beverages, Consumer Goods, Medical & Pharmaceuticals, Industrial Products, Hardware), By End-Use Industry (Food Processing & Retail, Consumer Electronics, Medical Devices, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Amcor plc, MULTIVAC, Coveris Holdings S.A., Berry Global, Inc., ProAmpac, Klockner Pentaplast, Mondi Group, Sonoco Products Company, Techniflex, Pactiv Evergreen, Winpak Ltd., Plastirol, Novolex, Polyrafia

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Skin Packaging Market Segmentation

By Material

By Technology

- Vacuum Skin Packaging

- Modified Atmosphere Packaging

By Application

- Food & Beverages

- Consumer Goods

- Medical & Pharmaceuticals

- Industrial Products

- Hardware

By End-Use Industry

- Food Processing & Retail

- Consumer Electronics

- Medical Devices

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Skin Packaging Market

- Sealed Air Corporation

- Amcor plc

- MULTIVAC

- Coveris Holdings S.A.

- Berry Global, Inc.

- ProAmpac

- Klockner Pentaplast

- Mondi Group

- Sonoco Products Company

- Techniflex

- Pactiv Evergreen

- Winpak Ltd.

- Plastirol

- Novolex

- Polyrafia

* List Not Exhaustive

Methodology

The research methodology for the Skin Packaging Market combines both primary and secondary approaches to ensure comprehensive, reliable, and accurate insights. Primary research involved interviews with senior executives, packaging engineers, sustainability specialists, and supply chain professionals across key regions including North America, Europe, Asia-Pacific, India, Brazil, and Japan. Secondary research included analysis of company annual reports, regulatory and policy databases, patents, sustainability disclosures, trade publications, and verified industry journals. Advanced data triangulation was applied to validate market sizing, growth projections, and technology adoption trends, integrating factors such as raw material pricing, automation penetration, barrier-film innovations, and mono-material packaging developments. Forecasts were constructed using both top-down and bottom-up approaches, with regional insights contextualized against Extended Producer Responsibility (EPR) regulations, recycling mandates, consumer demand for sustainable and high-clarity packaging, and trade flows. This multi-layered methodology ensures that the report delivers precise, fact-based, and actionable intelligence for decision-makers, reflecting real-world market dynamics and emerging trends in vacuum skin packaging, carded skin packaging, and sustainable packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.