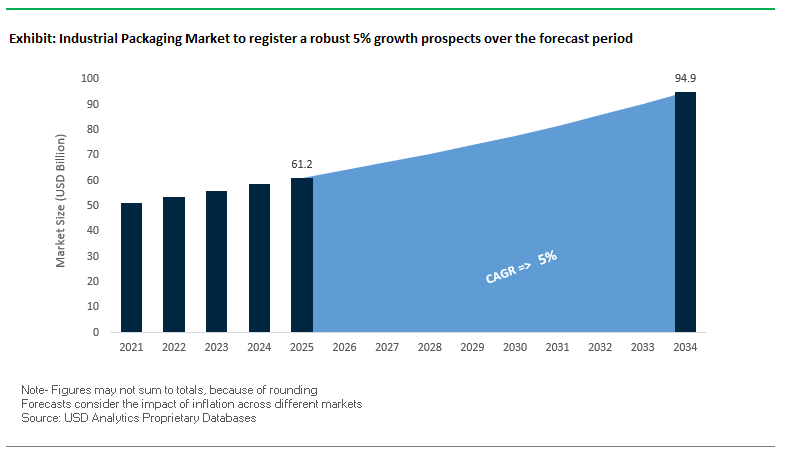

Industrial Packaging Market Overview: Reusable IBC fleets, smart containers, and lightweighting push the market from $61.2B (2025) to $94.9B (2034) at 5.0% CAGR

The Global Industrial Packaging Market the backbone of bulk and heavy-duty logistics across chemicals, food ingredients, automotive, and construction is in a structural upgrade cycle. Buyers are shifting toward reusable steel drums and Intermediate Bulk Containers (IBCs), investing in RFID/IoT-enabled asset visibility, and specifying lightweight yet high-integrity formats (reinforced corrugated and advanced plastics) to lower damage rates and cost-to-serve. Demand is increasingly shaped by ESG mandates, supply-chain transparency, and performance packaging that protects against puncture, moisture, and thermal extremes on long-haul, multi-modal routes.

Key Insights for Industry Professional

- Circular economy at scale: Reusable IBCs/steel drums reduce single-use reliance and deliver lower total cost of ownership.

- Connected packaging: RFID + IoT sensors enable real-time location, temperature, and fill-level monitoring for sensitive cargo.

- Performance first: High-hazard sectors (chemicals/auto) prioritize puncture resistance, barrier control, and thermal stability.

- Lightweighting ROI: Reinforced corrugated and advanced plastics cut freight emissions while maintaining stacking and crush specs.

Market Analysis: 2024–2025 moves show portfolio focus, circular infrastructure, PFAS-free bulk, and low-carbon adhesives

In August 2025, Greif, Inc. announced a definitive agreement to sell its Containerboard business for $1.8B to accelerate debt reduction and focus on core industrial packaging platforms. Also in August 2025, a leading flexible converter launched PFAS-free, compostable bulk bags for industrial food ingredients, aligning with tightening “forever-chemicals” scrutiny. July 2025 brought completion of the International Paper–DS Smith merger, creating a trans-Atlantic fiber leader and intensifying competition in sustainable, large-format transit packaging.

Circular infrastructure continued to scale. In June 2025, Mauser Packaging Solutions opened a reconditioning & recycling facility in Spain, expanding closed-loop capacity for IBCs and drums. The same month, sector research flagged a pickup in packaging M&A, especially in paper/corrugated evidence of consolidation and capability stacking. In May 2025, a European paper and packaging major unveiled water-resistant corrugated tailored for fresh food and agriculture, targeting moisture-prone supply chains.

Material decarbonization is entering converting lines. April 2025 saw H.B. Fuller launch near-carbon-neutral adhesives for industrial packaging, helping brands trim embedded CO₂ without sacrificing line efficiency. Upstream capacity is expanding too: in March 2025, Saica Group announced a $110M corrugated plant in Indiana (≈110M m²/yr), strengthening North American heavy-duty corrugated supply for export and domestic lanes.

Emerging Trends and Strategic Opportunities Transforming the Industrial Packaging Market

Strategic Corporate Investment in Circular Economy Infrastructure

Industrial packaging is witnessing a substantial strategic shift as major chemical and packaging corporations make large-scale capital investments to integrate recycled content into their products. This trend represents a tangible response to customer sustainability mandates and upcoming regulatory pressures. Dow, for instance, has committed to advanced recycling initiatives through a partnership with Lucro Plastecycle in India, aiming to co-develop post-consumer recycled polyethylene film solutions. Similarly, investment firms like Circulate Capital are channeling millions into startups such as Recykal, building digital platforms to formalize waste recovery and recycling supply chains. Furthermore, direct partnerships between producers and recyclers are enabling packaging to be designed for optimal end-of-life recovery, targeting collection rates of 60-80% over time, as highlighted by the Consumer Goods Forum’s circular economy guidelines. This comprehensive investment in infrastructure not only enhances sustainability but also positions companies as leaders in eco-conscious industrial packaging solutions.

Adoption of Smart Packaging Technologies for Supply Chain Resilience

The integration of Industrial Internet of Things (IIoT) sensors and trackers into industrial bulk containers is revolutionizing supply chain management. These technologies allow real-time condition monitoring, mitigating risks of spoilage, damage, or logistical delays, which is critical for high-value industrial goods. By monitoring parameters such as temperature, humidity, and shock, companies can proactively prevent product loss and ensure optimal quality during transit. Predictive maintenance enabled by IIoT sensors improves overall equipment effectiveness (OEE), reduces waste, and prevents unplanned downtime. Additionally, IIoT facilitates the creation of a digital supply network, providing end-to-end visibility from the factory floor to the customer, enhancing inventory management, and enabling a rapid response to supply chain disruptions.

Development of Packaging for U.S. Semiconductor Manufacturing Expansion

The U.S. CHIPS and Science Act, with over $52 billion allocated to semiconductor research and manufacturing, creates a high-value opportunity for specialized industrial packaging providers. Ultra-high-purity (UHP) containers, drum liners, and protective packaging solutions are now in high demand for transporting sensitive silicon wafers and fabrication components. The surge in domestic semiconductor manufacturing, driven by federal grants and tax credits, is fueling this demand. Additionally, the National Advanced Packaging Program under the CHIPS Act focuses on assembly, testing, and packaging (ATP) of semiconductors, necessitating advanced hermetic and contamination-free packaging solutions that safeguard critical components while supporting domestic production objectives.

Expansion of Reusable Packaging-As-A-Service Models

The rise of reusable transport packaging models is transforming industrial packaging from a one-time sale into a recurring service revenue stream. This aligns with circular economy principles by reducing environmental impact and operational costs. B2B reusable packaging solutions, including pallets, crates, and IBCs, have already demonstrated economic viability by lowering material expenses and fuel usage. The “packaging-as-a-service” model converts capital expenditures into operational expenditures, benefiting SMEs and large corporations alike. Companies offering global-scale services handle the design, provision, collection, cleaning, and redistribution of reusable packaging, streamlining logistics for clients while ensuring a consistent, reliable supply of clean, eco-friendly packaging assets.

Competitive Landscape: Global platforms standardize reuse, smart tracking, and high-integrity bulk systems

A concentrated set of multinationals is defining best-in-class industrial packaging via closed-loop services (reconditioning/reuse), HDPE/steel systems engineering, heavy-duty fiber, and digital traceability. Differentiation hinges on life-cycle economics, regional service density, and sector expertise.

Greif, Inc. Portfolio focus and core industrial scale

Greif is realigning around its “Build to Last” strategy enhancing capital efficiency and doubling down on core industrial packaging. In August 2025, it moved to divest Containerboard ($1.8B) following earlier timberlands exit to deleverage and create optionality for targeted investments. The portfolio spans steel/plastic/fiber drums, IBCs, and bulk corrugated for chemicals, pharma, and food. Strengths include a global manufacturing network, breadth of formats, and a service ethos aimed at being the “customer service company” tailoring specifications, safety, and sustainability to end-market needs.

Mauser Packaging Solutions Closed-loop IBCs and smart reconditioning at global scale

Mauser leads in rigid industrial packaging with IBCs, steel & plastic drums, and pails, backed by a global reconditioning/recycling network that operationalizes circularity. Its Poly-MT IBC brings reusability + embedded digitalization to minimize carbon and enhance fleet visibility. Strategy spans the full life cycle design, manufacture, recondition, recycle lowering TCO and compliance risk for multinationals. With 170+ sites worldwide, Mauser is a one-stop partner for standardized specs and multi-region service SLAs.

Mondi plc Fiber systems and FunctionalBarrier Papers for industrial duty

Mondi’s material-neutral approach pairs paper-based and flexible plastic solutions, targeting 100% reusable/recyclable/compostable portfolios by 2025. Innovations such as FunctionalBarrier Papers replace plastics in selected industrial applications without sacrificing machinability or moisture/grease resistance. Vertical integration from forestry to converting tightens quality control and sustainability assurance, allowing buyers to optimize performance vs. end-of-life across diverse industrial use cases.

Amcor plc Mono-material films and circular polymers for industrial applications

Amcor’s industrial solutions emphasize recyclability and material efficiency, with a roadmap to make all products recyclable or reusable by 2025. In August 2025, Amcor advanced UK capabilities to upgrade recycled polymers for flexible applications, reinforcing circular supply. The offer spans heavy-duty films and bags with rising adoption of mono-material structures (PE/PP) that simplify recycling streams. Strengths combine global reach, materials science, and co-development with customers navigating evolving regulatory and ESG targets.

Smurfit Kappa Group PLC Heavy-duty corrugated and fit-to-product automation

As one of the largest paper-based packaging players (enhanced by the combination with WestRock), Smurfit Kappa brings vertically integrated fiber loops to industrial customers. The portfolio includes bulk/heavy-duty corrugated and Hexacomb for cushioning and edge protection. Recent efforts prioritize fit-to-product automated packaging, cutting material usage and freight while protecting large or fragile parts. Strategy centers on tailored industrial solutions that lift supply-chain efficiency, reduce environmental footprint, and maintain load stability under real-world logistics stresses.

Industrial Packaging Market Share Insights

FIBCs Hold the Largest Product Share in the Industrial Packaging Market

In the broader industrial packaging market, FIBCs capture the highest product share at around 28%, driven by their versatility, recyclability, and cost competitiveness in global logistics. They remain the preferred solution for dry bulk materials across chemicals, petrochemicals, agriculture, and construction. IBCs represent 22% share, growing rapidly due to their superior cube utilization and reusability compared to drums. Their adoption is accelerating in chemicals, food-grade liquids, and lubricants. Drums retain a resilient share due to their durability and compliance in hazardous goods transport, particularly in petrochemicals and specialty chemicals. By contrast, sacks and pails are gradually losing share, with sacks facing substitution by FIBCs in bulk distribution and pails being replaced by smaller flexible formats for consumer-facing goods. Despite this decline, they maintain relevance in niche applications such as bagged cement and hand-held coatings or adhesives packaging.

Chemicals and Petrochemicals Drive Market Share by End-Use in the Industrial Packaging Market

Chemical and petrochemical industries dominate the industrial packaging end-use landscape with around 30% share. Their demand is anchored in the transport of resins, solvents, lubricants, and hazardous materials, which necessitate packaging that is both UN-compliant and operationally efficient. Food and beverage packaging follows closely at 25%, driven by stringent hygiene and regulatory requirements for dry and liquid ingredients in global trade. Construction is a major bulk user of sacks and FIBCs for cement and aggregates, its packaging demand closely tied to regional and global infrastructure growth. Agriculture is a steady consumer, dependent on seasonal fertilizer, feed, and seed distribution, with volumes fluctuating alongside global crop cycles. Pharmaceuticals occupy a smaller but high-value segment, characterized by sterile, validated packaging for APIs and biopharmaceuticals. Automotive packaging demand stems from just-in-time supply chains, using returnable containers, IBCs for lubricants, and specialty drums for coatings. Together, these end-use industries define a diverse but regulation- and cost-driven market structure.

United States: Regulatory Compliance and Technological Innovation Fuel Industrial Packaging Growth

The U.S. industrial packaging market is strongly influenced by evolving regulations, particularly state-level Extended Producer Responsibility (EPR) laws, with Maryland and Washington among the early adopters. These laws place responsibility for packaging waste management on producers, incentivizing the use of sustainable and recyclable materials. Technological advancements, including AI-powered automated recycling systems, are enhancing operational efficiency by accurately identifying, sorting, and processing recyclable materials, setting new benchmarks for sustainability in industrial packaging.

Corporate initiatives are also shaping the market, exemplified by Greif, Inc.’s launch of reusable, eco-friendly drums in 2025 to reduce the carbon footprint of chemical transport. Infrastructure investments, such as Germany’s Schütz Container Systems’ $31 million expansion in St. Joseph, Missouri, highlight the strategic push to meet rising demand for intermediate bulk containers (IBCs) in North America. The growing e-commerce and home delivery sectors are driving demand for lightweight, durable, and eco-friendly bulk containers, while regulatory oversight from the U.S. Department of Transportation (DOT) and Federal Trade Commission (FTC) ensures safety and compliance for hazardous material transportation.

China: Carbon-Neutral Policies and Automation Drive Sustainable Industrial Packaging

China’s industrial packaging market is undergoing a green transformation, driven by the government’s “dual carbon” goals of achieving carbon peak and carbon neutrality. A new packaging regulation, effective June 1, 2025, promotes recycled materials, reusable systems, and minimal excess packaging to reduce delivery waste. Technological innovation is at the forefront, with manufacturers leveraging AI and “5G plus industrial internet” to optimize production efficiency and enable flexible manufacturing capabilities.

Sustainability initiatives are reshaping product development, with restrictions on non-degradable plastics boosting demand for paper-based and eco-friendly packaging alternatives. Regulatory reforms, such as the State Council’s September 2022 circular to prevent over-packaging, aim to establish a whole-chain administration system by 2025. Industry consolidation is occurring as smaller, less-efficient manufacturers exit the market, while leading companies like Jingxing Packaging Materials in Zhejiang adopt closed-loop systems that utilize approximately 1.1 tonnes of recycled boxes per tonne of corrugated paper, exemplifying China’s commitment to sustainable industrial packaging.

Germany: Circular Economy Leadership and Technological Advancements Strengthen Industrial Packaging

Germany’s industrial bulk packaging market operates under stringent regulatory frameworks, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. This regulation mandates that all packaging be fully recyclable or reusable by 2030 and sets minimum recycled content targets. The country’s leadership in circular economy practices, reinforced by the Packaging Act (Verpackungsgesetz), incentivizes producers to innovate in recyclable materials and sustainable packaging solutions.

Technological innovation is a key driver, with companies developing next-generation substrates such as grass paper and high-strength recycled fibers to comply with environmental standards. Corporate expansions, such as Mauser Packaging Solutions’ facility investments to increase capacity for IBCs and other bulk containers, reflect Germany’s commitment to sustainability and circular economy principles. The EU PPWR’s focus on reuse and refill targets is further catalyzing innovation and efficiency across the industrial packaging sector.

India: Government Initiatives and Industrialization Drive Market Expansion

India’s industrial bulk packaging market benefits from initiatives like “Make in India” and “Zero Effect Zero Defect,” which promote high-quality domestic production and infrastructure investment. The Production Linked Incentive (PLI) Scheme for the food processing sector further enhances manufacturing capabilities, generating demand for standardized, high-quality packaging solutions.

Corporate expansion, including Mauser Packaging Solutions’ facility growth in India in August 2024, reinforces the region’s market presence and ability to meet increasing demand in chemical and pharmaceutical industries. Regulatory policies such as the Plastic Waste Management (Amendment) Rules, which aim to phase out single-use plastics, are driving adoption of eco-friendly packaging alternatives. Rapid industrialization, including the development of IT parks and commercial hubs, is further increasing demand for industrial packaging, positioning India as a key growth market in Asia-Pacific.

Brazil: Sustainability Regulations and Technological Integration Propel Industrial Packaging

Brazil’s industrial bulk packaging market is influenced by the National Solid Waste Policy, which encourages a circular economy and the adoption of reusable, durable packaging. Technological advancements, including robotics and AI, are enhancing efficiency and quality control, enabling sophisticated operations such as automated sorting and defect detection.

Sustainability is a key driver, reinforced by the 2025 ban on imported solid waste, including plastics, which encourages domestic recycling and innovation. Strategic investments in factory expansions, reverse logistics, and sustainable packaging technologies, amounting to R10.5 billion per year ($1.8 billion), are expected to drive growth despite tariff uncertainties. Key applications in the food and beverage sector, coupled with Brazil’s expanding food processing industry, are creating strong demand for bags, totes, IBCs, and other industrial bulk packaging solutions.

Japan: Advanced Recycling and Bio-Based Materials Fuel Industrial Packaging Innovation

Japan’s industrial packaging market benefits from a robust foundation in recycled material usage under the Containers and Packaging Recycling Law, which assigns recycling responsibilities to businesses. Technological innovation is driving the production of high-performance bulk packaging with superior dimensional stability and resistance to deformation.

Regulatory updates, such as the May 2025 revision to the Food Sanitation Act, ensure compliance for food-contact packaging, while the adoption of bio-based materials, exemplified by LyondellBasell’s partial use of bio-based polypropylene in Shiseido packaging, underscores Japan’s commitment to sustainability. E-commerce growth is driving demand for durable, reliable packaging with advanced customization and branding capabilities, reinforcing Japan’s leadership in functional, eco-conscious industrial packaging solutions.

Industrial Packaging Market Report Scope

Industrial Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$61.2 Billion

|

|

Market Size (2034)

|

$94.9 Billion

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Product Type (Flexible Intermediate Bulk Containers (FIBCs), Intermediate Bulk Containers (IBCs), Drums, Pails, Sacks), By Material (Plastic, Metal, Paper & Paperboard, Wood), By Application (Food & Beverages, Chemicals, Pharmaceuticals, Industrial & Agricultural Goods, Building & Construction), By End-Use Industry (Food & Beverage, Chemical & Petrochemical, Pharmaceutical, Construction, Agriculture, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Mauser Packaging Solutions, Berry Global Group, Inc., International Paper, WestRock Company, Amcor plc, Mondi Group, Smurfit Kappa Group, RTS Packaging, CDF Corporation, Schoeller Allibert, O-I Glass, Sonoco Products Company, DS Smith Plc, Novolex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Packaging Market Segmentation

By Product Type

By Material

- Plastic

- Metal

- Paper & Paperboard

- Wood

By Application

- Food & Beverages

- Chemicals

- Pharmaceuticals

- Industrial & Agricultural Goods

- Building & Construction

By End-Use Industry

- Food & Beverage

- Chemical & Petrochemical

- Pharmaceutical

- Construction

- Agriculture

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Industrial Packaging Market

- Greif, Inc.

- Mauser Packaging Solutions

- Berry Global Group, Inc.

- International Paper

- WestRock Company

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- RTS Packaging

- CDF Corporation

- Schoeller Allibert

- O-I Glass

- Sonoco Products Company

- DS Smith Plc

- Novolex

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous, multi-layered research methodology to deliver precise and actionable insights into the Industrial Packaging Market. Our approach combines primary research interviews with procurement managers, packaging engineers, supply chain professionals, and industry executives with secondary research, including analysis of corporate reports, regulatory filings, sustainability initiatives, and trade publications. Market sizing and forecasts are developed using both top-down and bottom-up approaches, factoring in product types such as Flexible Intermediate Bulk Containers (FIBCs), Intermediate Bulk Containers (IBCs), drums, pails, and sacks, alongside materials including plastics, metal, paper, and wood. USDAnalytics also evaluates emerging trends, including circular economy adoption, smart packaging technologies (IoT/RFID), lightweighting, PFAS-free solutions, and reusable packaging-as-a-service models, while assessing their adoption across major regions such as the U.S., China, Germany, India, Brazil, and Japan. Competitive benchmarking includes portfolio strategies, reconditioning networks, digital traceability, and sustainability commitments of leading players such as Greif, Mauser Packaging Solutions, Mondi, Amcor, and Smurfit Kappa. This methodology ensures stakeholders receive reliable, forward-looking intelligence to optimize supply chain efficiency, ESG performance, and total cost of ownership.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.