Industrial Bulk Packaging Market Overview: IBC-Led Efficiency, HDPE Dominance, and Circular Reuse Drive $28.9B to $45.2B (5.1% CAGR)

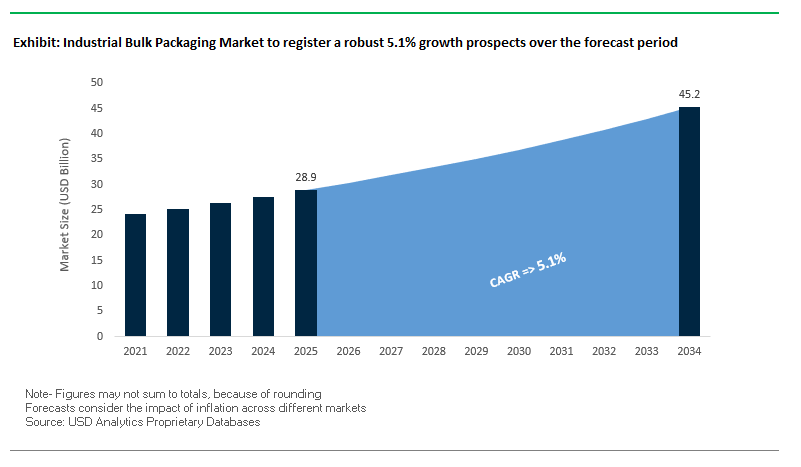

The Global Industrial Bulk Packaging Market is valued at USD 28.9 billion in 2025 and is projected to reach USD 45.2 billion by 2034, expanding at a CAGR of 5.1%. Growth is anchored by the IBC (Intermediate Bulk Container) advantage with capacities up to 3,000 liters which compresses cost-to-serve, lowers freight emissions, and improves bulk handling for chemicals, food & beverage, and pharmaceuticals versus drums and pails. The sector is also a mature circular-economy ecosystem: reconditioning and reuse of steel/plastic drums and IBCs prevent significant plastic waste and extend asset life. Material science remains pragmatic HDPE leads on chemical resistance, durability, and weight while smart packaging (RFID, GPS, sensorization) lifts supply-chain visibility, compliance, and asset security. For procurement and operations leaders, the case for industrial bulk packaging blends total cost of ownership (TCO), regulatory assurance, and scope-3 decarbonization.

Key Insights for industry professionals

- IBC economics: Up to 3,000 L capacity yields superior cube utilization, lower freight, and fewer handling events.

- Circularity at scale: Reconditioned IBCs/drums enable multi-cycle reuse and avert hundreds of kg of plastic waste per unit life.

- HDPE leadership: HDPE dominates IBCs, drums, and pails for chemical resistance, durability, and low mass.

- Smart packaging: RFID/GPS/sensors on IBCs and drums enable real-time location, temperature, and fill-level monitoring.

Market Analysis: 2024–2025 Pivots Accelerate Circular Infrastructure, Portfolio Focus, and Smart Reconditioning

In September 2025, Greif outlined a strategic plan to double down on its industrial core, following August 2025 divestiture of its Soterra land management business for USD 462 million. Also in August 2025, Mauser Packaging Solutions opened a reconditioning and recycling facility at BASF’s Tarragona (Spain) site, deepening on-site circularity for a key customer and expanding smart, reusable IBC capacity. During August 2025, Constantia Flexibles committed €100+ million to upgrade its global network, signaling sustained confidence in flexible solutions that increasingly interface with bulk workflows across food and pharma.

Portfolio sharpening continued in July 2025, when Greif signed a definitive agreement to sell its Containerboard Business for USD 1.8 billion, freeing capital for IBCs, drums, and bulk systems. Earlier moves underscore end-market alignment: in April 2025, RPC Inc. expanded Permian operations with the Pintail Alternative Energy acquisition, reinforcing exposure to oil & gas, a heavy user of industrial bulk packaging. In January 2025, Mauser launched a stainless-steel IBC line, addressing pharma and chemical customers that demand sanitary design, corrosion resistance, and long service life.

The broader substrate landscape also consolidated: in December 2024, the Smurfit Kappa–WestRock merger formed Smurfit WestRock, a paper-based giant capable of scaling bulk corrugated for heavy/oversized goods. Earlier, in July 2024, DS Smith introduced PackRight 2.0, a hybrid collaboration model that helps FMCG and e-commerce users co-design sustainable bulk and transit formats a sign that fiber innovators are partnering more closely with industrial users to optimize damage rates, pallet efficiency, and recyclability.

Key Trends and Strategic Opportunities Shaping the Industrial Bulk Packaging Market

Strategic Shift Towards Lightweighting and High-Performance Material Composites

Industrial bulk packaging is undergoing a transformative shift as manufacturers adopt advanced polymer resins and composite designs to reduce the tare weight of IBCs and drums without compromising strength or chemical resistance. Lightweighting directly lowers shipping costs and fuel consumption while helping companies achieve Scope 3 emissions targets. Innovations in HDPE and LLDPE allow production of thinner, lighter containers that retain durability, enabling substantial material reduction. This trend is particularly significant for the chemical, food, and beverage industries, where large volumes of products are transported globally, making lighter, high-performance materials a critical competitive advantage.

Integration of IoT and RFID for Real-Time Asset Tracking and Condition Monitoring

The industrial bulk packaging sector is rapidly embedding IoT sensors and RFID technology into IBCs and drums, enabling real-time monitoring of location, temperature, shock, and tampering. This provides enhanced supply chain visibility, mitigates risks for high-value or sensitive products, and optimizes asset utilization. Companies can track container usage, reduce idle time, and detect potential counterfeiting or diversion. By integrating digital identifiers, manufacturers and shippers can secure the entire product journey, ensuring compliance with regulatory and safety standards while enhancing operational efficiency.

Development of Advanced, Closed-Loop Circular Service Models

A significant opportunity exists to establish circular economy models where packaging producers manage the full lifecycle of IBCs and drums. This includes leasing, professional cleaning, refurbishment, and redeployment. Case studies, such as initiatives promoted by the Ellen MacArthur Foundation, demonstrate that reusable packaging systems can cut waste and CO2 emissions significantly compared to single-use solutions. By converting packaging from a capital expense to an operational expense, these models offer long-term financial and environmental benefits while supporting sustainability goals.

Proliferation of Bio-Based and Chemically Recycled Polyolefins for Regulatory Compliance

With growing extended producer responsibility (EPR) regulations and plastic taxes, industrial bulk packaging manufacturers are investing in bio-based polyethylene (Bio-PE) and chemically recycled polypropylene (mass-balance approach). Chemical recycling enables production of virgin-quality plastics from multi-layer or contaminated waste, meeting food-grade or hazardous material standards. Bio-based materials can reduce carbon footprint by hundreds of millions of tons of CO2 equivalents annually. The mass-balance certification ensures that sustainable claims are verifiable, allowing companies to comply with regulations, achieve sustainability targets, and appeal to environmentally conscious clients.

Competitive Landscape: Global Leaders Standardize Reuse, Smart Tracking, and High-Integrity Bulk Formats

A tight field of multinational specialists is shaping the market through reusable IBC fleets, drum reconditioning networks, HDPE/steel systems engineering, and digital traceability. Differentiation hinges on closed-loop services, material breadth (HDPE/steel/stainless), regional service density, and end-market expertise in chemicals, food, pharma, and energy.

Mauser Packaging Solutions Scaling reconditioned IBCs and smart, heavy-duty fleets

Mauser delivers rigid industrial packaging across plastic/steel drums, IBCs, and pails for chemicals, agriculture, and food & beverage. Sustainability is embedded: the Poly-MT IBC is a reusable, smart, heavy-duty solution designed to cut carbon and digitize supply chains. A global reconditioning/recycling network underpins multi-cycle reuse economics. Strategically, Mauser covers the full life cycle design, manufacture, recondition, recycle reducing TCO for global accounts. With 170+ sites worldwide, Mauser acts as a one-stop partner for multi-region specifications and service SLAs.

Greif, Inc. Refocusing capital on core industrial packaging platforms

Greif offers steel, plastic, and fiber drums, IBCs, and bulk corrugated to chemical, pharma, and food sectors. The company is executing a portfolio realignment: August 2025 sale of Soterra (USD 462M) and July 2025 agreement to divest the Containerboard Business (USD 1.8B) sharpen focus on IBCs/drums/services and deleveraging. Strategy centers on being the best customer service company, investing in safety, performance, and sustainability. Flagship offerings include GCUBE IBC for high-performance liquid handling and enhanced transportation efficiency.

Smurfit WestRock Paper-based bulk systems with vertically integrated fiber loops

Formed via the December 2024 merger, Smurfit WestRock leads in paper-based packaging, including bulk corrugated containers, heavy-duty boxes, and industrial bags for agriculture, chemicals, and general industrials. The combined footprint from forestry and paper to converting delivers consistent quality, fiber security, and recycled-content options aligned with customer ESG goals. Strategic focus: innovative, recyclable fiber solutions that complement rigid bulk systems and improve palletization, stacking strength, and cube utilization in global logistics.

Silgan Holdings Inc. Rigid metal/plastic containment with convenience and waste reduction

Silgan supplies metal and plastic containers/closures across consumer and industrial uses. In July 2025, the company reported adjusted EPS growth driven by organic volume gains and contributions from its Weener Packaging acquisition. Silgan’s industrial portfolio includes metal containers and closures for diverse products, with designs such as EZ-Open that improve line efficiency and product yield. Strategy emphasizes reliability, safety, and sustainability, investing in materials and processes that meet industrial customers’ performance and compliance requirements.

Industrial Bulk Packaging Market Share Insights

Flexible Intermediate Bulk Containers Dominate Market Share by Product Type in the Industrial Bulk Packaging Market

Flexible Intermediate Bulk Containers (FIBCs) command the largest share of the industrial bulk packaging market, accounting for around 40%. Their dominance is attributed to their unmatched cost efficiency, lightweight design, and collapsibility, which reduces reverse logistics costs by as much as 95%. FIBCs are indispensable for global trade in dry, flowable commodities such as polymers, fertilizers, minerals, and food ingredients. The rise of containerized shipping and bulk dry cargo movements has entrenched them as the global workhorse. Intermediate Bulk Containers (IBCs) follow with a substantial 30% share, particularly critical for liquid and hazardous materials. Their efficiency each 1,000-liter tote replaces four drums makes them the preferred choice in chemicals, pharmaceuticals, and food-grade liquids. Drums remain a legacy standard in smaller batch shipments, mandated by UN transport codes for certain hazardous materials. Multi-wall sacks maintain their share in regional distribution of branded products like cement and animal feed, while pails continue as the niche solution for paints, adhesives, and food syrups requiring portability and manual handling.

Chemicals Lead Market Share by Application in the Industrial Bulk Packaging Market

The chemicals sector secures the highest application share at about 35%, reflecting its critical reliance on UN-certified FIBCs, IBCs, and drums for transporting corrosives, solvents, and specialty polymers. Compliance with stringent safety standards such as ADR, IMDG, and DOT underpins packaging innovation in this segment. Industrial and agricultural goods follow with 30% share, driven by fertilizers, ores, and resins commodities that depend on the lowest cost-per-ton transport solutions. Food and beverages represent a significant quality-driven segment where FDA- and EFSA-compliant FIBCs and IBCs dominate, ensuring hygiene, traceability, and product integrity for ingredients like sugar, flour, and edible oils. Building and construction demand is cyclical but steady, relying heavily on sacks and bulk bags for cement and gypsum distribution. Pharmaceuticals, though smaller by volume, remain the highest-value niche with cleanroom-manufactured IBCs and validated FIBCs ensuring purity and compliance with GMP and USP standards.

United States: Sustainability and Regulatory Compliance Drive Industrial Bulk Packaging Demand

The U.S. industrial bulk packaging market is increasingly shaped by evolving regulations, particularly state-level Extended Producer Responsibility (EPR) laws, which hold producers accountable for packaging waste management. This regulatory focus is driving demand for sustainable and recyclable materials. Technological advancements, including AI-powered automated recycling systems, are transforming production by improving the identification, sorting, and processing of recyclable materials with high precision and efficiency.

Corporate initiatives are strengthening market growth, exemplified by Greif, Inc.’s launch of reusable, eco-friendly drums made from recycled materials to reduce the carbon footprint associated with chemical transport. Investments in infrastructure, such as Schütz Container Systems’ $31 million expansion in Missouri, demonstrate a strategic push to meet rising demand for intermediate bulk containers (IBCs) across North America. Logistics and e-commerce growth further fuel the market, with durable, lightweight packaging increasingly needed to withstand last-mile delivery challenges. Regulatory oversight from the U.S. Department of Transportation (DOT) and the Federal Trade Commission (FTC) ensures compliance with safety and labeling standards, especially for hazardous materials.

China: Green Transformation and E-Commerce Growth Shape Industrial Bulk Packaging

China’s industrial bulk packaging market is being propelled by governmental initiatives aligned with the “dual carbon” goal of achieving carbon peak and carbon neutrality. Policies promoting eco-friendly and reusable materials are transforming the design and production of bulk packaging solutions. Manufacturers are also investing heavily in automation and AI, integrating “5G plus industrial internet” technologies to optimize production efficiency and enhance flexible manufacturing capacity.

Sustainability is a key driver, with restrictions on non-degradable plastics spurring demand for paper-based and sustainable alternatives. The rapid growth of domestic e-commerce platforms is creating additional demand for customizable and durable bulk packaging solutions suitable for chemicals, food products, and other industrial goods. Regulatory reforms, such as the State Council’s circular issued in September 2022 to prevent over-packaging, aim to establish a whole-chain administration system by 2025. Market consolidation is occurring as smaller, less-efficient manufacturers close operations, leaving larger producers with a dominant share in China’s industrial bulk packaging market.

Germany: Circular Economy and Technological Innovations Strengthen Industrial Bulk Packaging

Germany’s industrial bulk packaging industry is heavily influenced by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates full recyclability or reusability of packaging by 2030 and sets minimum recycled content targets. The country’s leadership in circular economy practices, under the Packaging Act (Verpackungsgesetz), ensures that producers are responsible for the entire lifecycle of their packaging, incentivizing innovation in recyclable and sustainable materials.

Technological advancements include the development of next-generation substrates such as grass paper and high-strength recycled fibers to meet stringent environmental standards. Corporate expansions, such as Mauser Packaging Solutions’ investment in new production lines for IBCs and bulk containers, demonstrate Germany’s commitment to sustainable growth. The EU PPWR’s waste reduction measures and reuse targets are reshaping the market, driving the adoption of environmentally responsible industrial bulk packaging solutions.

India: Infrastructure Investments and Government Initiatives Fuel Market Growth

India’s industrial bulk packaging market benefits from governmental initiatives such as “Make in India” and “Zero Effect Zero Defect,” which encourage high-quality domestic production and infrastructure investment. The Production Linked Incentive (PLI) Scheme for the food processing industry further enhances manufacturing capabilities, creating demand for standardized, high-quality packaging solutions.

Corporate expansions, such as Mauser Packaging Solutions’ facility growth in India in August 2024, reinforce the country’s market presence and capacity to serve chemical and pharmaceutical sectors. Regulatory policies like the Plastic Waste Management (Amendment) Rules, which phase out single-use plastics, are boosting demand for eco-friendly alternatives. Rapid industrialization, including IT parks and commercial hubs, increases consumption of bulk packaging for a variety of goods, positioning India as a key growth market in Asia-Pacific.

Brazil: Sustainability and Technological Integration Shape Industrial Bulk Packaging

Brazil’s industrial bulk packaging market is heavily influenced by the National Solid Waste Policy, which promotes a circular economy and encourages reusable, durable packaging solutions. Technological advancements, including robotics and AI, are enhancing operational efficiency and quality control, enabling more sophisticated production, from automated sorting to defect detection.

Sustainability remains a core focus, reinforced by the January 2025 ban on imported solid waste, including plastics, which encourages domestic recycling and innovation. Strategic investments in factory expansions, reverse logistics, and recycling technologies, totaling approximately $1.8 billion annually, are expected to support industry growth despite tariff uncertainties. Key applications in the food and beverage sector, along with Brazil’s expanding food processing industry, are driving demand for bags, totes, IBCs, and other industrial bulk packaging solutions.

Japan: Advanced Recycling and Bio-Based Materials Drive Industrial Bulk Packaging

Japan’s industrial bulk packaging market is supported by robust recycling systems under the Containers and Packaging Recycling Law, assigning recycling roles to businesses and promoting efficient collection and repurposing of packaging materials. Technological innovations are enhancing packaging functionality, including high dimensional stability and resistance to deformation for high-performance applications.

Regulatory policies, including the May 2025 update to the Food Sanitation Act, set new standards for food-contact packaging, promoting safety and compliance. The country is also shifting toward bio-based materials, with initiatives such as LyondellBasell’s partial incorporation of bio-based polypropylene in Shiseido packaging reflecting growing adoption of sustainable solutions. E-commerce growth is creating demand for durable, customizable packaging options, while innovation in printing and functionality supports Japan’s industrial bulk packaging market in meeting consumer and industrial requirements.

Industrial Bulk Packaging Market Report Scope

Industrial Bulk Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.9 Billion

|

|

Market Size (2034)

|

$45.2 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (Flexible Intermediate Bulk Containers, Intermediate Bulk Containers, Drums, Pails, Sacks), By Material (Plastic, Metal, Paper & Paperboard, Wood), By Application (Food & Beverages, Chemicals, Pharmaceuticals, Industrial & Agricultural Goods, Building & Construction), By End-Use Industry (Food & Beverage, Chemical & Petrochemical, Pharmaceutical, Construction, Agriculture, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Mauser Packaging Solutions, Berry Global Group, Inc., International Paper, WestRock Company, Amcor plc, Mondi Group, Smurfit Kappa Group, RTS Packaging, CDF Corporation, Schoeller Allibert, O-I Glass, Sonoco Products Company, DS Smith Plc, Novolex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Bulk Packaging Market Segmentation

By Product Type

- Flexible Intermediate Bulk Containers

- Intermediate Bulk Containers

- Drums

- Pails

- Sacks

By Material

- Plastic

- Metal

- Paper & Paperboard

- Wood

By Application

- Food & Beverages

- Chemicals

- Pharmaceuticals

- Industrial & Agricultural Goods

- Building & Construction

By End-Use Industry

- Food & Beverage

- Chemical & Petrochemical

- Pharmaceutical

- Construction

- Agriculture

- Automotive

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Industrial Bulk Packaging Market

- Greif, Inc.

- Mauser Packaging Solutions

- Berry Global Group, Inc.

- International Paper

- WestRock Company

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- RTS Packaging

- CDF Corporation

- Schoeller Allibert

- O-I Glass

- Sonoco Products Company

- DS Smith Plc

- Novolex

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to provide actionable insights into the Industrial Bulk Packaging Market, combining primary and secondary data sources to ensure accuracy and reliability. Our approach integrates interviews with industry leaders, supply chain managers, and packaging engineers alongside analysis of company reports, trade publications, regulatory filings, and sustainability initiatives. Market sizing and forecasts are derived using a hybrid bottom-up and top-down modeling approach, accounting for product types such as FIBCs, IBCs, drums, and pails, as well as materials including HDPE, metal, paper, and composites. USDAnalytics further examines industry trends such as lightweighting, IoT-enabled smart containers, circular economy models, and bio-based material adoption, while mapping growth across key regions including the U.S., China, Germany, India, Brazil, and Japan. Competitive benchmarking covers portfolio strategies, reconditioning networks, sustainability practices, and digital traceability initiatives of leading players like Mauser Packaging Solutions, Greif, Smurfit WestRock, and Silgan Holdings. This methodology ensures market insights are precise, forward-looking, and aligned with operational, environmental, and regulatory priorities critical for procurement, logistics, and sustainability decision-makers in industrial bulk packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.