Market Overview: FIBC Market to Reach $11.4 Billion by 2034 at 6.3% CAGR

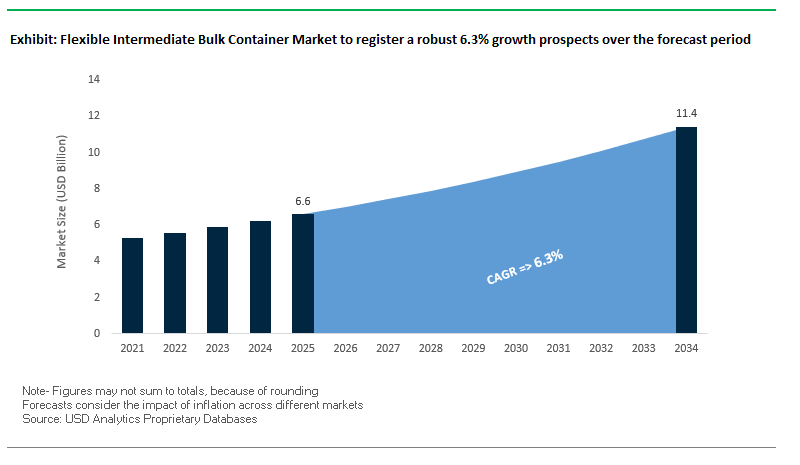

The global flexible intermediate bulk container (FIBC) market is projected to grow from $6.6 billion in 2025 to $11.4 billion by 2034, expanding at a CAGR of 6.3%. This growth is driven by increasing adoption of bulk handling solutions across industries such as chemicals, food, agriculture, construction, and pharmaceuticals, where efficiency, safety, and cost-effectiveness are paramount.

FIBCs are valued for their strength, lightweight structure, and reusability, making them indispensable for large-scale industrial logistics. They provide a balance of sustainability, operational cost savings, and material protection, answering critical questions for buyers around product safety, compliance, and supply chain optimization.

Key Insights for Industry Stakeholders:

- High-Strength Materials: A standard FIBC carrying 1 metric ton of goods weighs only 5–7 lb, showcasing superior strength-to-weight ratios.

- Logistics Savings: Collapsible, stackable designs lower shipping costs and improve warehouse efficiency.

- Smart Integration: IoT-enabled FIBCs with humidity and temperature sensors are emerging to ensure supply chain transparency.

- Safety Standards: Increasing adoption of Type B, C, and D static-dissipative bags ensures compliance for chemical and pharma industries.

Market Analysis: Strategic Acquisitions, Earnings Growth, and Sustainability Milestones

The FIBC industry is witnessing rapid developments, from sustainability breakthroughs to mergers that are reshaping competitive dynamics.

In August 2025, Greif, Inc. reported strong third-quarter earnings, posting an adjusted EPS of $1.03 and a 10.8% year-over-year EBITDA growth, reflecting efficiency improvements in its core FIBC and industrial packaging business. In July 2025, Packaging Corporation of America acquired Greif’s containerboard business for $1.8 billion, a move allowing Greif to streamline its portfolio and sharpen its focus on industrial packaging and FIBCs. That same month, Sigma Stretch Film of Georgia announced a $39 million investment to expand its Columbus, Georgia plant, increasing output of stretch films that are vital for palletizing and transporting FIBCs.

The industry is also being influenced by large-scale packaging consolidation. In July 2025, International Paper completed its $9.9 billion acquisition of DS Smith, reinforcing its dominance in paper packaging, which competes with FIBCs in select bulk applications. In April 2025, TOPPAN Holdings finalized the acquisition of Sonoco’s Thermoformed & Flexibles Packaging (TFP) business, strengthening its adjacent capabilities in flexible packaging.

A notable sustainability milestone was achieved in April 2025, when Packem Umasree, a Brazilian-Indian joint venture, became the first company to manufacture a 100% sustainable FIBC from recycled PET bottles. This represents a major step in advancing circular economy practices within industrial packaging. Other sectoral innovations include Mondi’s March 2025 launch of paper-based pouches, further validating the trend toward bio-based packaging alternatives that may complement or compete with FIBCs in certain applications.

Trends and Opportunities Reshaping the Flexible Intermediate Bulk Container (FIBC) Market

Accelerated Integration of Post-Consumer Recycled (PCR) Content Driven by Regulation

The Flexible Intermediate Bulk Container market is experiencing a paradigm shift toward circular economy models, fueled by Extended Producer Responsibility (EPR) frameworks and ambitious corporate sustainability mandates. In Europe, the Packaging and Packaging Waste Regulation (PPWR) mandates recyclability by 2030, while U.S. states like California and New Jersey have established minimum recycled content standards. These policies are accelerating the integration of PCR polypropylene into FIBCs to reduce virgin resin dependency and financial liability under EPR schemes.

Technological advances are helping the industry overcome historical performance concerns associated with recycled materials. For instance, Starlinger’s advanced recycling lines have demonstrated that post-consumer polypropylene can be converted into regranulates suitable for high-load woven fabrics, maintaining tensile strength and a safety factor equivalent to virgin PP. This innovation enables FIBC manufacturers to comply with regulatory mandates while achieving durability and load-bearing performance standards. At the same time, industry collaborations such as the PolyStyreneLoop initiative highlight a collective effort to build scalable closed-loop recycling ecosystems for complex plastic applications, positioning the FIBC industry firmly within the global circular economy transition.

Proliferation of Smart FIBCs with Integrated Tracking and Sensing Technology

The evolution of smart packaging technologies is redefining FIBCs from bulk storage containers into real-time supply chain intelligence assets. Manufacturers are embedding IoT sensors, GPS modules, and RFID tags into FIBCs to deliver continuous visibility into shipment location, inventory levels, and environmental conditions. This is particularly valuable for sensitive sectors such as pharmaceuticals, chemicals, and food ingredients, where spoilage, contamination, or theft can result in substantial losses.

A logistics case study showed that smart FIBCs with temperature and humidity sensors enabled operators to intervene proactively, preventing spoilage during transit. In addition, GPS integration improves asset management, allowing companies to track the location of individual FIBCs, minimize loss, and ensure timely return for reuse. By integrating IoT-enabled FIBCs into enterprise ERP systems, manufacturers gain predictive analytics, loss prevention, and optimized route planning, elevating bulk packaging from a cost center to a strategic enabler of supply chain resilience and transparency.

Development and Commercialization of High-Barrier Mono-Material Liners

A pressing challenge for FIBC recyclability is the widespread use of multi-layer composite liners that combine PET, aluminum, and PE, contaminating recycling streams. The opportunity lies in developing mono-material barrier liners, engineered from single polymers such as all-PE or all-PP films, which are compatible with PP recycling streams while delivering the oxygen, moisture, and light barriers demanded by industrial users.

Innovations from Toppan and Mondi showcase this potential. Toppan has introduced recyclable mono-material barrier packages, while Mondi’s “re/cycle” portfolio demonstrates hermetically sealable mono-polymer liners suitable for high-performance industrial applications. These liners not only meet functional requirements of durability and barrier strength but also align with PPWR and global recyclability mandates, giving manufacturers a clear regulatory and competitive advantage. By solving this recyclability bottleneck, the industry can simultaneously enhance sustainability credentials and reduce the environmental burden of single-use FIBC liners.

Expansion of Service-Based Reusable FIBC Pooling Systems

The shift from ownership to access models is opening new revenue streams through FIBC pooling and leasing services. In this model, manufacturers or logistics providers lease reusable FIBCs to customers, manage their retrieval after use, and oversee cleaning, inspection, and recertification before redeployment. Studies from the Reusable Industrial Packaging Association (RIPA) confirm that such closed-loop, service-based systems significantly lower waste generation and carbon footprints compared to single-use FIBCs.

This approach is gaining traction in predictable, high-volume B2B supply chains, such as agriculture, where reusable FIBCs have been successfully adopted by grain exporters in India to reduce packaging waste and enhance operational efficiency. High-quality FIBCs with 6:1 or 8:1 safety factors are engineered for dozens of reuse cycles, creating measurable cost savings over time. The challenge and opportunity lies in building robust reverse logistics and cleaning infrastructure to support large-scale adoption. Companies that can deliver a turnkey service ecosystem from bag delivery and pickup to sanitation and redeployment stand to capture long-term contracts and secure a leadership position in the circular bulk packaging economy.

Competitive Landscape: Global Leaders Redefining the FIBC Market

The FIBC market is moderately fragmented, with global giants and specialized regional players driving competition through sustainability, compliance, and technological innovation.

Greif, Inc. Strengthening Core FIBC Business After Strategic Divestitures

Greif is a leading U.S. manufacturer of industrial packaging with a strong portfolio in FIBCs serving food, agriculture, and chemical sectors. In 2025, the company divested its paper packaging and containerboard businesses, sharpening its focus on FIBCs and industrial containers. Its global manufacturing footprint and supply chain expertise ensure scalable, customized solutions. Greif’s fiscal 2025 Q3 results, with EBITDA rising 10.8% YoY, underscore its robust operational performance.

Conitex Sonoco Delivering Safe and Compliant FIBCs

Conitex Sonoco, a joint venture with Sonoco, specializes in food-grade and pharma-compliant FIBCs. The company integrates Sonoco’s global network with Conitex’s technical expertise, ensuring reliable supply chain coverage. With innovations in anti-static bags and moisture-resistant FIBCs, Conitex Sonoco is well-positioned to serve industries requiring high safety and compliance standards.

Berry Global, Inc. Advancing Circular Economy in FIBC Production

Berry Global is a key supplier of flexible packaging and FIBCs, with strong emphasis on sustainable materials. Its Impact 2025 strategy commits to 100% reusable or recyclable packaging and increased use of PCR (post-consumer recycled) plastics. Recently, Berry won the Sika Sustainable Packaging Challenge for developing a container with 30% PCR, showcasing leadership in circular economy packaging.

Bulk-Pack, Inc. Custom-Engineered FIBCs for Diverse Industries

Bulk-Pack, based in North America, is known for tailor-made FIBCs across industries like food processing, agriculture, chemicals, and pharmaceuticals. Its portfolio includes baffle bags, duffle top bags, and anti-static FIBCs, designed to meet highly specific client needs. The company has gained recognition in industry events and safety advocacy, reinforcing its role as a trusted supplier of high-quality, compliant FIBCs.

Halsted Corporation Long-Standing Reputation for Quality FIBCs

Halsted Corporation has built a strong reputation for durable, high-performance bulk bags in the chemical and food industries. With fully integrated services spanning design, engineering, manufacturing, and logistics, Halsted ensures consistent quality and customer satisfaction. Its commitment to reliability and compliance with global standards continues to secure its position as a trusted industrial packaging partner.

Flexible Intermediate Bulk Container Market Share Insights

Type C FIBCs Dominate Market Share by Product Type in the FIBC Market

In 2025, Type C (conductive) FIBCs lead with 35% share, reflecting their status as the safety benchmark for flammable powders and solvents where mandatory grounding eliminates electrostatic ignition risk; this is reinforced by stringent chemical and pharma protocols. Type A bags at 25% remain the cost-effective workhorse for inert materials fertilizers, minerals, animal feed sustaining high-volume demand across agriculture and construction. Type D (static-dissipative) FIBCs are the fastest-rising cohort as facilities seek grounding-free operations that reduce human-error risk, trading higher unit cost for systemic safety. Food-grade FIBCs hold a protected niche on the strength of hygiene certifications and contamination control for starches, sugars, cocoa, and grains, while Type B persists narrowly where non-propagating brush discharge is acceptable. UN-certified FIBCs overlay these constructions to unlock hazardous-goods flows, signaling that compliance, not just cost, allocates product-type share. Net impact: market leadership maps directly to ESD safety performance, regulatory compliance, and total risk mitigation at scale.

Chemicals Lead Market Share by Application in FIBCs, Followed by Agriculture & Fertilizers

By application, chemicals command 30% share in 2025, anchoring demand for Type C/D bags where process safety, product value, and documentation are non-negotiable driving premium mix and repeat procurement. Agriculture & fertilizers at 25% provide the volume backbone, favoring Type A for seeds, urea, and feed with high seasonal throughput and forklift/hoist efficiency. Food & beverages prioritize food-grade compliance for ingredients, while minerals & mining require heavy-duty, often anti-static solutions for metal powders and ores. Pharmaceuticals remain a high-value, low-volume niche defined by cleanliness, traceability, and validation, with construction absorbing durable bags for powders and additives. The allocation of application share mirrors the intersection of hazard class, hygiene requirements, and cost-per-ton moved, with chemicals and agri flows dictating global FIBC capacity planning.

United States: Driving Growth with Food-Grade FIBCs and Smart Packaging Technologies

The U.S. flexible intermediate bulk container (FIBC) market is witnessing strong growth driven by specialized food and pharmaceutical-grade bulk bags. Manufacturers are producing FIBCs with dust-proof seams, anti-static properties, and enhanced contamination resistance, catering to high-value sectors such as food, pharmaceuticals, and chemicals. Companies are also integrating smart technologies, including RFID tags and QR codes, enabling real-time tracking, inventory management, and enhanced supply chain transparency.

Sustainability is a key focus, with the industry shifting towards FIBCs containing higher post-consumer recycled (PCR) content and implementing closed-loop recycling programs. Strategic collaborations, such as the partnership between Berry Global and Plastic Energy, are helping develop recycled materials for use in flexible industrial packaging. These innovations are positioning the U.S. market as a leader in sustainable, technologically advanced, and high-performance FIBC solutions.

Germany: Pioneering Circular Economy and Automated FIBC Production

Germany’s FIBC market is a cornerstone of Europe’s circular economy, driven by stringent sustainability regulations and corporate commitments. Manufacturers are focusing on reusable and recyclable FIBCs, supporting the European Green Deal and reducing industrial waste. The market also benefits from technological leadership in automation, with robotic systems used for filling, discharging, and stacking bulk bags, improving both operational efficiency and safety in industrial settings.

Compliance with EU standards is another key market driver. Manufacturers are developing FIBCs that meet rigorous requirements for transporting hazardous and flammable materials, including Type C and D conductive bags, ensuring safe and efficient bulk material handling across diverse industries. Germany’s combination of sustainability, automation, and regulatory adherence reinforces its position as a leading FIBC hub in Europe.

China: Global Manufacturing Leader Driving FIBC Production and Sustainability

China is a global powerhouse in FIBC manufacturing, serving both domestic and international markets with a wide range of high-quality, competitively priced bulk containers. The country’s growth is fueled by increasing demand from the construction, agriculture, and chemical industries, along with large-scale infrastructure projects that require efficient bulk material handling solutions.

Government initiatives are shaping the market by implementing policies to reduce plastic pollution and improve recycling infrastructure. National standards for recycled plastics, effective from early 2026, are expected to drive the adoption of sustainable FIBCs and enhance circular economy practices. Chinese manufacturers are investing in advanced production technologies and eco-friendly materials to meet rising domestic demand while maintaining a strong export presence.

India: Expanding as a Global FIBC Manufacturing Hub

India’s FIBC industry is rapidly growing, emerging as a major global manufacturer with exports to over 65 countries. Government initiatives such as Make in India are boosting domestic production, and companies are investing in clean room facilities to produce food-grade FIBCs that comply with international standards such as BRC, catering to the expanding food export market.

Strategic alliances and technology transfers are strengthening India’s market. For instance, a joint venture with a Brazilian company enables the production of 100% sustainable FIBCs from recycled PET (rPET). The Indian Flexible Intermediate Bulk Container Association (IFIBCA) plays a critical role in promoting industry growth, aligning with the Atmanirbhar Bharat (Self-Reliant India) vision. These factors position India as a hub for cost-effective, high-quality, and sustainable bulk packaging solutions.

Brazil: Leading Sustainable and Reusable FIBC Solutions for Agribusiness

Brazil’s FIBC market is strongly influenced by its agribusiness sector, where efficient and secure bulk packaging solutions are essential for commodities such as grains and fertilizers. The market is increasingly focusing on reusable and eco-friendly FIBCs, which help reduce plastic waste while offering cost efficiency across multiple uses.

Strategic investments are supporting market expansion and technological innovation. Companies like Greif Inc. have launched FIBCs with integrated RFID tracking, enabling real-time inventory management and enhancing supply chain efficiency. Brazil’s combination of sustainability, technological adoption, and agribusiness demand positions it as a regional leader in high-performance, environmentally responsible FIBC solutions.

Flexible Intermediate Bulk Container Market Report Scope

Flexible Intermediate Bulk Container Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.6 Billion

|

|

Market Size (2034)

|

$11.4 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Product Type (Type A FIBCs, Type B FIBCs, Type C FIBCs, Type D FIBCs, UN Certified FIBCs, Food Grade FIBCs), By Application (Chemicals, Food & Beverages, Pharmaceuticals, Construction, Agriculture & Fertilizers, Minerals & Mining, Other Applications), By Design (4-Panel Bags, U-Panel Bags, Circular/Tubular Bags, Baffle Bags, Other Designs), By Filling and Discharging Options (Top Filling Spouts, Bottom Discharging Spouts, Duffel Tops, Full Open Tops, Plain Bottoms, Other Options)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Greif, Inc., Berry Global, Inc., LC Packaging International, Rishi FIBC Solutions Pvt. Ltd., Halsted Corporation, Bulk-Pack, Inc., Sackmakers Private Limited, Conitex Sonoco, Jumbo Bag Limited, Taihua Group, Pelsma Group, Umasree Texplast Private Limited, AmeriGlobe, LLC, Bulk Corp International, Langston Companies, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Intermediate Bulk Container Market Segmentation

By Product Type

- Type A FIBCs

- Type B FIBCs

- Type C FIBCs

- Type D FIBCs

- UN Certified FIBCs

- Food Grade FIBCs

By Application

- Chemicals

- Food & Beverages

- Pharmaceuticals

- Construction

- Agriculture & Fertilizers

- Minerals & Mining

- Other Applications

By Design

- 4-Panel Bags

- U-Panel Bags

- Circular/Tubular Bags

- Baffle Bags

- Other Designs

By Filling and Discharging Options

- Top Filling Spouts

- Bottom Discharging Spouts

- Duffel Tops

- Full Open Tops

- Plain Bottoms

- Other Options

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Intermediate Bulk Container Market

- Greif, Inc.

- Berry Global, Inc.

- LC Packaging International

- Rishi FIBC Solutions Pvt. Ltd.

- Halsted Corporation

- Bulk-Pack, Inc.

- Sackmakers Private Limited

- Conitex Sonoco

- Jumbo Bag Limited

- Taihua Group

- Pelsma Group

- Umasree Texplast Private Limited

- AmeriGlobe, LLC

- Bulk Corp International

- Langston Companies, Inc.

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the dynamic growth, technological advancements, and strategic shifts shaping the global Flexible Intermediate Bulk Container (FIBC) market. The analysis reviews breakthroughs in sustainable material integration, smart FIBC solutions, high-barrier mono-material liners, and reusable pooling systems, while highlighting mergers, acquisitions, and regional expansions that are redefining competitive landscapes. This report is an essential resource for industry professionals, investors, and supply chain managers seeking actionable insights into market trends, regulatory impacts, and performance-driven product innovations. Additionally, the report emphasizes sustainability milestones such as the adoption of post-consumer recycled (PCR) polypropylene and circular economy initiatives, offering a comprehensive view of operational efficiencies, cost optimization, and regulatory compliance across diverse industrial sectors. By combining historical market data from 2021 to 2024 with detailed forecasts from 2025 to 2034, USDAnalytics provides a robust and strategic understanding of FIBC growth potential, market segmentation, and key industry players to guide investment, procurement, and innovation strategies.

Scope Highlights:

- Segmentation: By Product Type (Type A, B, C, D FIBCs, UN Certified, Food Grade), By Application (Chemicals, Food & Beverages, Pharmaceuticals, Construction, Agriculture & Fertilizers, Minerals & Mining, Other Applications), By Design (4-Panel, U-Panel, Circular/Tubular, Baffle, Other), By Filling & Discharging Options (Top Filling Spouts, Bottom Discharging Spouts, Duffel Tops, Full Open Tops, Plain Bottoms, Other).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historical data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies: Profiles and analysis of 15+ leading FIBC manufacturers, including Greif, Berry Global, Conitex Sonoco, Bulk-Pack, Halsted, and LC Packaging International.

Methodology

This FIBC market study is based on a multi-step research methodology combining both primary and secondary sources. USDAnalytics employed expert interviews with key stakeholders, including manufacturers, distributors, and logistics operators, to obtain qualitative insights on trends, adoption rates, and emerging challenges. Secondary data from annual reports, regulatory filings, trade publications, and global packaging databases were analyzed to quantify historical market performance, competitive dynamics, and regional demand patterns. Forecasting employed a combination of bottom-up and top-down approaches, integrating macroeconomic indicators, industrial output, regulatory policies, and technological adoption rates. Advanced statistical and econometric modeling ensured accurate projections for product type, application, and regional growth. Additionally, the methodology incorporates scenario analysis to assess the impact of sustainability mandates, circular economy initiatives, and technological innovations on market share and revenue potential, providing decision-makers with actionable insights for strategic planning and investment prioritization.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.