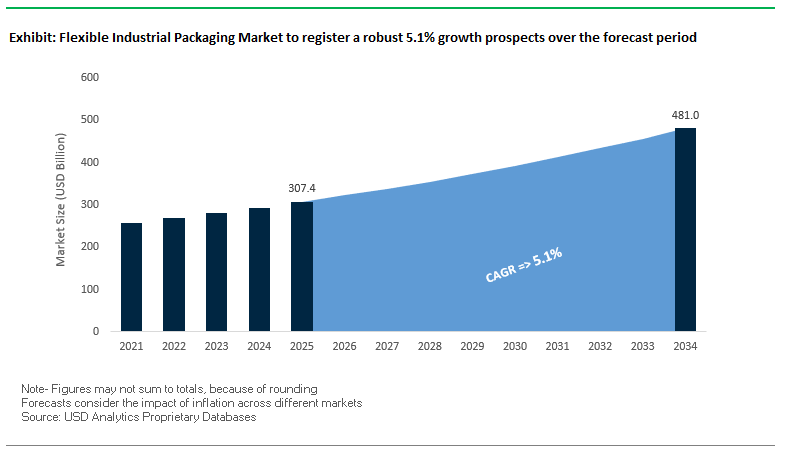

Market Overview: Flexible Industrial Packaging Market to Reach $481 Billion by 2034 at 5.1% CAGR

The global flexible industrial packaging market is projected to expand from $307.4 billion in 2025 to $481 billion by 2034, growing at a steady CAGR of 5.1%. This growth is driven by rising demand for durable, lightweight, and sustainable packaging solutions across industrial sectors such as chemicals, construction, agriculture, pharmaceuticals, and e-commerce logistics. Buyers and professionals are increasingly focusing on performance-driven innovation, recyclability, and advanced logistics compatibility when evaluating packaging solutions.

Key Insights for Industry Stakeholders:

- Plastic Film Dominance: Polyethylene (PE), polypropylene (PP), and multi-layer laminates continue to dominate due to durability, cost-effectiveness, and versatility.

- FIBC Growth: Flexible Intermediate Bulk Containers (FIBCs) remain a primary segment, serving bulk transportation of chemicals, grains, and construction materials.

- E-commerce Acceleration: Rising last-mile logistics and the need for stackable, damage-resistant packaging are reshaping film and industrial bag designs.

- Performance Enhancements: Demand is surging for packaging with improved puncture resistance, tear strength, and anti-static properties to meet the requirements of complex industrial supply chains.

Market Analysis: Strategic Expansions, M&A Activity, and Sustainable Packaging Innovations

The flexible industrial packaging industry is undergoing significant transformation, with strategic investments, acquisitions, and sustainability-led innovations reshaping market dynamics.

In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, reinforcing its footprint in the medical and pharmaceutical sectors. That same month, Amcor upgraded its UK recycling facility, enhancing its ability to integrate recycled content into its industrial films and flexible solutions. This aligns with growing circular economy goals across the sector.

In July 2025, Sigma Stretch Film of Georgia announced a $39 million investment to expand its manufacturing site in Columbus, Georgia, including a new warehouse to scale up stretch film production. This expansion strengthens its role in pallet unitization and logistics optimization. Earlier, in April 2025, TOPPAN Holdings completed the acquisition of Sonoco’s Thermoformed & Flexibles Packaging (TFP) business, creating a new global competitor with an enhanced flexible solutions portfolio. Also in April, BW Flexible Systems re-opened its renovated manufacturing facility in Mestrino, Italy, after a $3 million upgrade aimed at boosting efficiency and production capacity.

Other developments include Coral Products’ April 2025 acquisition of Arrow Film Converters, expanding its capabilities in film converting. In March 2025, Siegwerk announced a leadership reshuffle within its executive committee to support its long-term growth strategy in inks and coatings for flexible packaging. Additionally, in February 2025, Mondi partnered with Proquimia to launch paper-based stand-up pouches for dishwashing tabs, highlighting a wider industry shift toward bio-based and paper alternatives for industrial applications.

Emerging Trends and Growth Opportunities in the Flexible Industrial Packaging Market

Strategic Shift Towards Circular and Recycled Material Content

The flexible industrial packaging market is undergoing a structural transition as manufacturers pivot from a linear production model to a circular economy approach. This shift is being driven primarily by Extended Producer Responsibility (EPR) regulations, which mandate that producers take accountability for end-of-life packaging, and by corporate ESG commitments to reduce virgin plastic usage. In the United States, states such as California, Maine, and New Jersey have enacted legislation that requires recycled content in certain packaging formats, reinforcing the demand for post-consumer recycled (PCR) resins.

Major players are aligning with these directives by investing in advanced recycling technologies, including chemical recycling, which allows contaminated or complex plastics to be broken down into virgin-equivalent monomers. For example, Amcor has pledged to achieve 30% recycled content across its product portfolio by 2030, creating sustained demand for PCR in woven polypropylene and polyethylene packaging applications. This trend not only supports environmental goals but also provides companies with supply chain resilience, as reliance on recycled inputs reduces exposure to volatile virgin resin markets. The strategic adoption of circularity positions fiber-reinforced woven sacks, FIBCs, and liners as eco-efficient industrial packaging solutions that align with customer and regulatory expectations.

Integration of IoT and Smart Tracking for Supply Chain Visibility

Another defining trend in the flexible industrial packaging industry is the integration of IoT-enabled smart features to transform packaging into a data-driven logistics asset. By embedding RFID tags, GPS units, and environmental sensors into flexible bulk containers, companies can monitor product conditions and location in real time. This is particularly critical for industries handling sensitive or high-value cargo, such as chemicals, pharmaceuticals, or agricultural commodities.

A study by a logistics technology provider demonstrated that combining RFID for warehouse-level inventory management with GPS for in-transit monitoring increased inventory accuracy from 65% to over 95%. Moreover, integrated sensors can monitor temperature, humidity, and shock events, alerting managers to potential spoilage or mishandling before goods are compromised. Linking this data to enterprise resource planning (ERP) systems further enables predictive maintenance, loss prevention, and route optimization, reducing both operational risks and costs. As a result, flexible industrial packaging is evolving beyond containment, becoming a critical enabler of transparency, efficiency, and resilience in global supply chains.

Development of High-Performance Mono-Material and Polymer-Alternative Films

A key opportunity for innovation lies in replacing traditional multi-layer industrial liners with mono-material barrier films or bio-based alternatives that meet recyclability and sustainability targets without compromising performance. Historically, multi-layer laminates were essential for moisture, UV, and chemical protection, but they are incompatible with current recycling streams. Emerging mono-material designs, such as Toppan’s PE- and PP-based barrier films, are capable of achieving high oxygen, moisture, and light resistance while being fully recyclable.

Bio-based materials such as PLA and cellulose-based films are also gaining traction, with academic research focusing on additives that improve durability, heat stability, and mechanical strength. Companies like Mondi are already commercializing recyclable flexible packaging portfolios under initiatives such as their re/cycle range, demonstrating that sustainable high-barrier films can scale commercially. For the industrial packaging sector, this development unlocks opportunities to offer durable yet fully recyclable packaging, addressing both regulatory requirements and growing customer demand for low-carbon, circular alternatives.

Expansion of Reusable and Returnable System Infrastructure

Another major growth avenue is the shift towards reusable and returnable flexible industrial packaging systems. Models where manufacturers lease or sell reusable FIBCs and woven sacks with cleaning, inspection, and redeployment handled through managed services are gaining momentum. According to the Reusable Industrial Packaging Association (RIPA), multi-use systems significantly cut down greenhouse gas emissions and waste compared to single-use solutions, aligning with corporate sustainability goals.

High-quality FIBCs with a 6:1 safety factor are specifically designed for repeated trips, making them cost-effective and environmentally advantageous. When combined with take-back programs and specialized cleaning services, this model allows companies to shift from a product-sales approach to a service-based revenue model, creating long-term client relationships. The success of this opportunity hinges on establishing efficient reverse logistics, including collection, sanitation, and redistribution networks. By scaling this model, companies can create circular packaging ecosystems that reduce both cost and environmental impact, while appealing to industries with high-volume, recurring packaging needs.

Competitive Landscape: Global Leaders Driving Flexible Industrial Packaging Growth

The flexible industrial packaging market is dominated by multinational leaders who compete on innovation, scale, and sustainability. Each company is actively investing in sustainable solutions, regional expansions, and high-performance products to maintain competitiveness.

Amcor PLC Leading with Sustainable Flexible Solutions

Amcor has established itself as a global leader in flexible films, bags, and pouches for industrial and consumer applications. Its AmPrima™ recycle-ready portfolio and AmFiber™ paper-based solutions are examples of innovation combining sustainability with high-barrier performance. In August 2025, Amcor expanded its Costa Rica healthcare network and upgraded its UK recycling plant to strengthen its sustainability-driven growth strategy. Leveraging global R&D centers and lifecycle assessment tools, Amcor supports customers in meeting regulatory and ESG targets.

Mondi plc Driving Circularity with Paper-based Packaging Innovations

Mondi is a recognized leader in kraft paper, industrial bags, and specialty films, operating under its Mondi Action Plan 2030 (MAP2030) strategy. The company recently launched FunctionalBarrier Paper Ultimate, a recyclable, high-barrier solution for industrial packaging. In June 2025, Mondi also partnered with Saga Nutrition on recyclable solutions, while expanding capacity at its Štětí plant in the Czech Republic with a new paper machine. Its vertically integrated model ensures supply chain security and sustainability leadership.

Berry Global Inc. Advancing Circularity Goals with PCR Integration

Berry Global continues to focus on plastic packaging with strong sustainability credentials. Its Impact 2025 strategy commits to achieving 100% recyclable or compostable packaging and scaling post-consumer recycled (PCR) content. Berry recently won the Sika North American Sustainable Packaging Challenge with containers containing 30% PCR and received APR recyclability recognition for its Versalite™ Cups. Its products span stretch films, industrial bags, and chemical containers, catering to a wide industrial base.

Sonoco Products Company Refocusing Portfolio on Core Industrial Packaging

Sonoco offers a strong portfolio of composite cans, tubes, cores, and flexible solutions for industrial markets. In April 2025, Sonoco divested its TFP business to TOPPAN Holdings for $1.8 billion, refocusing on industrial and consumer packaging. The company maintains leadership in film production, laminating, and custom design, supported by strong industry involvement, including leadership roles within the Flexible Packaging Association (FPA).

Hood Packaging Corporation Expanding Presence Through Strategic Acquisitions

Hood Packaging, a key North American player, specializes in industrial sacks, films, and woven bags. The company expanded its portfolio with the $95 million acquisition of TC Transcontinental’s industrial packaging business in late 2024. With over 23 facilities across North America, Hood provides localized service and quick turnaround for industrial clients. Its investment in high-density printing and advanced liquid filling systems demonstrates its focus on value-added, performance-driven flexible packaging.

Flexible Industrial Packaging Market Share Insights

FIBCs Lead Market Share by Product in Flexible Industrial Packaging

In 2025, FIBCs (bulk bags) hold 30% of flexible industrial packaging, reflecting unmatched efficiency for 500–2,000 kg flows of chemicals, minerals, fertilizers, and food ingredients; forklift/hoist handling, reusability (where permitted), and UN-rated safety features cement leadership. Industrial bags & sacks at 25% remain standardized volume drivers for cement, grains, and feed, balancing printability with toughness. Liners at 20% are the high-value barrier layer protecting against moisture, oxygen, and contamination in boxes, drums, and FIBCs mandatory for sensitive food, pharma, and specialty chemicals. Films & sheets (stretch, pallet covers) scale with freight volumes to unitize and weather-protect loads, while pouches and other formats grow in samples and small-lot ingredients where barrier performance and material efficiency beat rigid options. Product-level share mirrors a logistics equation: tonnage moved per handling cycle, contamination risk, and total landed cost.

Chemicals and Food & Beverages Drive Market Share by End-Use Industry in Flexible Industrial Packaging

Chemicals lead with 30% end-use share in 2025, demanding certified FIBCs, conductive options for powders, and high-barrier liners that meet strict safety/traceability standards performance and compliance are non-negotiable. Food & beverages at 25% represent the purity-critical volume engine, consuming multi-wall bags for flour/sugar and aseptic or high-barrier liners for oils and syrups under FSMA/FDA regimes. Agriculture is the seasonal volume anchor (fertilizers, seeds, feed) that stabilizes plant utilization, while industrial goods span abrasives, minerals, and components needing dust protection and pallet stability. Pharmaceuticals form a smaller but premium niche, prioritizing GMP-compliant materials, cleanliness, and serialization. The end-use split underscores how hazard class, hygiene requirements, and supply-chain efficiency collectively allocate share across flexible industrial formats.

United States: Driving Flexible Industrial Packaging Through Sustainability and Automation

The U.S. flexible industrial packaging market is witnessing rapid growth fueled by sustainability initiatives and advanced automation technologies. Companies like Berry Global are leveraging domestically recovered, mechanically recycled polypropylene (PP) to develop innovative products, reflecting a strong commitment to circular economy principles and the integration of post-consumer recycled (PCR) content. Technological integration, particularly AI-driven vision systems and robotics, is streamlining processes such as palletizing and packing, enhancing efficiency, and reducing labor costs in high-volume manufacturing.

The booming e-commerce sector is a significant driver for the U.S. market, creating strong demand for lightweight, durable, and protective flexible packaging solutions, including pouches, bags, and films. In addition, evolving regulatory frameworks, such as state-level Extended Producer Responsibility (EPR) mandates and bans on certain PFAS in food packaging, are pushing manufacturers to innovate and produce compliant, sustainable packaging solutions, positioning the U.S. as a global leader in eco-friendly and technologically advanced industrial packaging.

Germany: Leading Europe with Circular Economy and Material Innovation

Germany’s flexible industrial packaging industry is at the forefront of Europe’s circular economy, driven by stringent regulations like the VerpackG (Packaging Act) and the upcoming EU Packaging and Packaging Waste Regulation (PPWR). The market emphasizes high recycling rates and sustainable production practices, positioning Germany as a hub for environmentally responsible packaging solutions. Companies like Mondi are focusing on material innovation, developing recyclable yet high-performance flexible packaging through dedicated innovation hubs.

Strategic alliances are further strengthening the German market. Groups such as EOL Packaging Experts bring together multiple companies to offer integrated end-of-line packaging systems, essential for handling a diverse range of flexible industrial packaging formats. This combination of sustainability, innovation, and collaborative industrial infrastructure reinforces Germany’s leadership in high-quality, eco-conscious packaging solutions across Europe.

China: Global Manufacturing Powerhouse Driving Flexible Packaging Efficiency

China is a global manufacturing and export hub for flexible industrial packaging, with immense production capacity to serve both domestic consumption and international markets. The country’s competitive pricing and wide range of product offerings make it a key driver in the global packaging landscape. Government policies aimed at plastic waste reduction and improved recycling infrastructure are pushing companies to adopt sustainable materials and align with a circular economy approach.

To meet high-volume demand and regulatory standards, Chinese companies are investing heavily in advanced manufacturing and recycling technologies, including AI-driven robotics and intelligent sorting systems for plastic waste. These investments not only improve production efficiency but also ensure compliance with emerging national standards for recycled plastics, set to take effect in 2026, positioning China as a central hub for sustainable and technologically advanced flexible packaging solutions.

India: “Make in India” and Sustainability Driving Market Expansion

The Indian flexible industrial packaging market is experiencing strong growth, driven by government initiatives such as the ban on certain single-use plastics and the India Plastics Pact, which aims to make 100% of plastic packaging reusable, recyclable, or compostable by 2030. Flexible packaging is widely adopted in India due to its low cost, versatility, and durability, making it ideal for food, beverage, and e-commerce applications.

The “Make in India” initiative is catalyzing domestic and foreign investment in the packaging sector. For example, Swiss companies have invested in new aseptic carton pack facilities in Ahmedabad, boosting local manufacturing capabilities. India’s market is increasingly defined by cost-effective, versatile, and sustainable packaging solutions, meeting both industry demand and regulatory requirements.

Brazil: Pioneering Bioplastics and Supporting Industrial Applications

Brazil’s flexible industrial packaging market is distinguished by its leadership in bioplastics, with companies like Braskem producing green polyethylene from sugarcane ethanol, reducing reliance on fossil fuels and promoting sustainable production. The country’s booming e-commerce sector and industrial applications, particularly in agribusiness, are driving demand for robust and secure packaging solutions that can withstand long-distance transport.

Strategic investments are shaping Brazil’s market dynamics. Companies are expanding production capacity and introducing new products to cater to growing demand in the confectionery, dairy, and pharmaceutical sectors, positioning Brazil as a regional leader in sustainable, high-performance flexible industrial packaging.

Japan: High-Performance Materials and Regulatory-Driven Innovation

Japan’s flexible industrial packaging market emphasizes high-performance, technologically advanced materials. Multi-layer extrusion techniques are being used to develop films with superior barrier properties, critical for maintaining food safety and extending shelf life. Companies are also innovating with smart packaging, including digital tags and QR codes, to enhance supply chain traceability and consumer engagement.

Regulatory compliance drives innovation in Japan. The Food Sanitation Act mandates that food packaging meets stringent safety standards, compelling manufacturers to develop innovative, high-quality, and compliant materials. These factors collectively position Japan as a leader in precision-engineered and sustainable flexible industrial packaging solutions, catering to both domestic and international markets.

Flexible Industrial Packaging Market Report Scope

Flexible Industrial Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$307.4 Billion

|

|

Market Size (2034)

|

$481 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Material (Plastics, Paper, Aluminum Foil, Others), By Product (Pouches, Films & Sheets, Industrial Bags, Sacks, FIBCs, Wraps, Liners, Other Products), By End-Use Industry (Food & Beverages, Chemicals, Industrial Goods, Agriculture, Pharmaceuticals, Other End-Users), By Printing Technology (Flexography, Rotogravure, Digital Printing, Other Technologies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Mondi Group, Novolex Holdings, LLC, Sealed Air Corporation, Sonoco Products Company, DS Smith Plc, International Paper Company, Rengo Co., Ltd., Huhtamaki Oyj, BillerudKorsnäs AB, TCPL Packaging Ltd., Uflex Ltd., Constantia Flexibles Group GmbH, Coveris Holdings S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flexible Industrial Packaging Market Segmentation

By Material

- Plastics

- Paper

- Aluminum Foil

- Others

By Product

- Pouches

- Films & Sheets

- Industrial Bags

- Sacks

- FIBCs

- Wraps

- Liners

- Other Products

By End-Use Industry

- Food & Beverages

- Chemicals

- Industrial Goods

- Agriculture

- Pharmaceuticals

- Other End-Users

By Printing Technology

- Flexography

- Rotogravure

- Digital Printing

- Other Technologies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flexible Industrial Packaging Market

- Amcor plc

- Berry Global, Inc.

- Mondi Group

- Novolex Holdings, LLC

- Sealed Air Corporation

- Sonoco Products Company

- DS Smith Plc

- International Paper Company

- Rengo Co., Ltd.

- Huhtamaki Oyj

- BillerudKorsnäs AB

- TCPL Packaging Ltd.

- Uflex Ltd.

- Constantia Flexibles Group GmbH

- Coveris Holdings S.A.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the evolving landscape of the flexible industrial packaging market, highlighting breakthroughs in sustainable and high-performance packaging solutions across multiple industrial sectors. It provides a detailed analysis reviewing market dynamics, competitive strategies, and emerging innovations in FIBCs, industrial films, pouches, and liners. The report also highlights opportunities in mono-material barrier films, bio-based polymers, and circular packaging solutions, offering actionable insights for manufacturers, logistics providers, and corporate sustainability teams. By combining historical trends with future projections, this report is an essential resource for industry professionals seeking to optimize supply chain efficiency, enhance product safety, and meet evolving regulatory and ESG requirements globally. It emphasizes growth catalysts such as IoT-enabled smart packaging, integration of recycled content, and reusable packaging models, while profiling key players driving innovation and expansion across the United States, Europe, Asia Pacific, Latin America, the Middle East, and Africa. USDAnalytics ensures that this report serves as a comprehensive guide for decision-making in strategy, investment, and operational planning within the flexible industrial packaging industry.

Scope Highlights:

- Segmentation: By Material (Plastics, Paper, Aluminum Foil, Others); By Product (Pouches, Films & Sheets, Industrial Bags, Sacks, FIBCs, Wraps, Liners, Other Products); By End-Use Industry (Food & Beverages, Chemicals, Industrial Goods, Agriculture, Pharmaceuticals, Other End-Users); By Printing Technology (Flexography, Rotogravure, Digital Printing, Other Technologies)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Detailed analysis/profiles of 15+ leading companies including Amcor plc, Berry Global, Inc., Mondi Group, Novolex Holdings, LLC, Sealed Air Corporation, Sonoco Products Company, DS Smith Plc, International Paper Company, Rengo Co., Ltd., Huhtamaki Oyj, BillerudKorsnäs AB, TCPL Packaging Ltd., Uflex Ltd., Constantia Flexibles Group GmbH, and Coveris Holdings S.A.

Methodology

The research methodology adopted for this report involves a structured combination of primary and secondary data collection, ensuring the highest level of accuracy and reliability for industry professionals. Primary research was conducted through in-depth interviews with key executives, supply chain managers, and R&D heads across leading flexible industrial packaging manufacturers, distributors, and end-user companies. Secondary research encompassed an extensive review of company annual reports, press releases, patent filings, industry publications, regulatory frameworks, and government databases to validate market trends and growth drivers. Quantitative data analysis techniques, including market sizing, CAGR calculation, and segmentation forecasting, were applied to historical data from 2021–2024 and extended to projections for 2025–2034. Competitive intelligence and benchmarking were integrated to assess strategic moves, product launches, and capacity expansions among global leaders. Additionally, a bottom-up approach was used to ensure precision in regional and global market estimates, while scenario analysis addressed potential risks from regulatory shifts, supply chain disruptions, and emerging technological trends in smart, sustainable, and high-performance flexible industrial packaging.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.