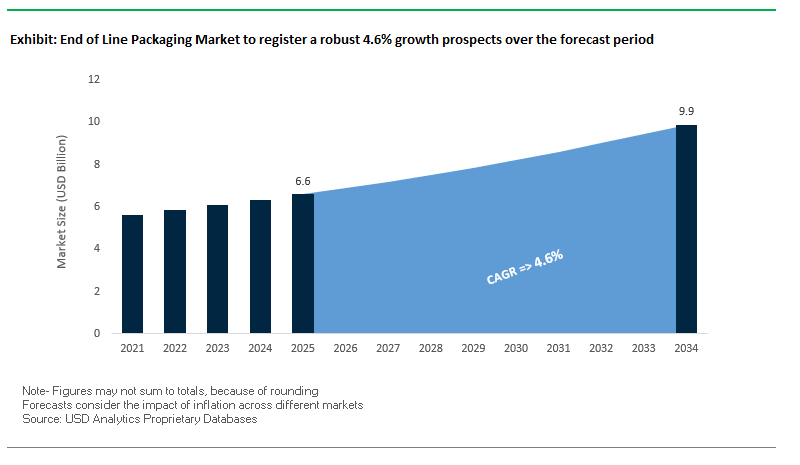

Market Overview: End-of-Line Packaging Market to Reach $9.9 Billion by 2034 at 4.6% CAGR

The global end-of-line packaging market is projected to grow from $6.6 billion in 2025 to $9.9 billion by 2034, reflecting a steady CAGR of 4.6%. As manufacturing, e-commerce, and food & beverage industries scale globally, the demand for automated, efficient, and sustainable end-of-line systems has surged. These systems are critical for the final stages of the production line, including case erecting, packing, palletizing, wrapping, and labeling. Industry professionals are increasingly prioritizing automation, integration, and data-driven decision-making to achieve operational efficiency and reduce costs.

Key Insights for Industry Stakeholders:

- Automation Dominance: Robotic palletizers, automated stretch wrappers, and digital case packers are now core investments to replace labor-intensive tasks and improve line speed.

- E-commerce Fulfillment: The rapid growth of online retail is driving demand for secure, customized, and visually appealing packages, shaping machine design and functionality.

- Integrated Systems: Buyers prefer single-source integrated solutions where case erecting, packing, sealing, and palletizing communicate seamlessly.

- Smart Packaging Tools: Real-time analytics, predictive maintenance, and performance dashboards are emerging as critical differentiators for return on investment.

Market Analysis: Automation, Acquisitions, and Sustainability Define Industry Growth

The end-of-line packaging market is witnessing rapid transformation through strategic acquisitions, material innovation, and breakthrough automation technologies.

In August 2025, Mondi launched Ad/Vantage Smooth Brown Paper for industrial use, a substrate innovation that supports sustainable packaging in end-of-line applications. That same month, Sidel confirmed it will unveil its laser bottle-blowing technology at Drinktec 2025, an innovation that reduces material usage and impacts downstream case-packing and palletizing efficiency.

In July 2025, Sigma Stretch Film announced a $39 million capacity expansion in Georgia, U.S., strengthening the supply of stretch films essential for pallet wrapping and load stability. In the same month, Bosch partnered with Tata Electronics in India to collaborate on chip packaging solutions, signaling a push into integrated packaging systems for electronics.

Earlier in June 2025, Pacteon Group (owner of Schneider Packaging) acquired Descon Integrated Conveyor Solutions, adding conveyance expertise to its robotic case packers and palletizers to deliver turnkey end-of-line automation. In May 2025, Innovia Films inaugurated a new German production line, producing sustainable films for wrapping and labeling applications, while Mondi partnered with Saga Nutrition on recyclable pet food packaging requiring adaptable end-of-line machinery.

A major consolidation move took place in April 2025, when International Paper completed its $9.9 billion acquisition of DS Smith, reshaping the global corrugated packaging sector and impacting case erecting and sealing material supply. Similarly, Ranpak Holdings launched its upgraded Cut’it! EVO automated packaging system in February 2025, featuring three new digital tools to improve throughput, ROI, and sustainability.

Trends and Opportunities Reshaping the End-of-Line (EOL) Packaging Market

Rapid Integration of Collaborative Robotics (Cobots) for Flexible Palletizing

The end-of-line packaging market is experiencing a rapid transformation with the adoption of collaborative robots (cobots) in palletizing and depalletizing applications. Unlike traditional caged robots, cobots are designed to work safely alongside human operators, bringing scalability and adaptability to manufacturers facing labor shortages and high turnover in physically demanding tasks.

Industry case studies illustrate the productivity impact OMRON Robotics documented an 80% increase in packaging capacity when a manufacturer implemented cobots for palletizing, simultaneously reducing injury risks and reallocating workers to higher-value roles. Cobots also stand out for ease of deployment with built-in safety features like collision detection, they require minimal guarding, reducing floor space needs and allowing faster integration. Their programming flexibility enables manufacturers to quickly adapt to new palletizing patterns or packaging formats, ensuring that packaging lines remain agile in response to shifting market demand.

Strategic Adoption of Digital Twin Technology for System Optimization and Uptime

Another defining trend is the rise of digital twin technology, where manufacturers build virtual replicas of their packaging lines to simulate, optimize, and predict performance. Digital twins combine IoT data with predictive analytics to provide real-time visibility into machine health, throughput, and bottlenecks.

By enabling virtual testing, companies can trial new formats, workflows, or machinery configurations in a risk-free environment before implementation. This shortens commissioning times, reduces trial-and-error, and cuts costs. Predictive maintenance powered by digital twins further ensures that parts are replaced proactively, minimizing unplanned downtime. For large packaging operations, where a minute of downtime can cost thousands, this technology provides measurable operational resilience. Leaders in the packaging machinery sector are already reporting higher OEE (Overall Equipment Effectiveness) and faster ramp-up times by embedding digital twin systems into EOL solutions.

Development of Integrated, Data-Driven Contract Packaging Services

The EOL packaging market presents a significant opportunity for third-party logistics (3PL) and contract packaging providers to create differentiation by offering data-driven, fully integrated solutions. Instead of being viewed as a cost center, contract packagers can leverage automation, IoT sensors, and AI analytics to deliver real-time insights into throughput, efficiency, and quality control.

Companies like Signode are already shifting to a consultative model, giving clients dashboards to monitor key performance metrics such as OEE, defect rates, and sustainability impacts. This transparency builds trust and elevates contract packaging into a strategic partnership. Furthermore, data-driven models enable providers to offer predictive inventory planning, sustainability scorecards, and proactive quality assurance services, unlocking new revenue streams while helping brand owners optimize supply chains and reduce waste.

Standardization of Robotic Cell Integration for Mid-Sized Manufacturers

A second major opportunity lies in developing standardized, pre-engineered robotic workcells tailored for mid-sized manufacturers. Historically, robotic automation has been a costly, complex investment accessible only to large enterprises. Pre-engineered “automation-in-a-box” EOL solutions are changing this dynamic by offering plug-and-play modular cells with simplified interfaces and scalable deployment models.

Suppliers like ProMach are leading this shift by offering fully integrated robotic palletizing and case-packing solutions that can be deployed in a fraction of the time of custom systems. These solutions reduce upfront costs, accelerate ROI (often within months), and give smaller manufacturers access to automation without prohibitive risk. Their modularity also ensures scalability companies can start with one workcell and expand as production grows. This democratization of robotics is a key enabler for mid-sized firms seeking to remain competitive in the era of Industry 4.0 packaging automation.

Competitive Landscape: Key Companies Shaping the End-of-Line Packaging Market

The end-of-line packaging market is highly competitive, with companies differentiating through automation technology, integrated solutions, and sustainability-driven innovation.

Krones AG Driving Digital Transformation with Service 4.0

Krones delivers complete end-of-line systems for the beverage and liquid food sectors, covering filling, labeling, packing, palletizing, and wrapping. Its Service 4.0 program provides real-time monitoring and predictive maintenance, reducing downtime for clients. Financial performance in 2024 and early 2025 showed EBITDA margin growth to 10.6%, reflecting disciplined pricing and operational efficiency. Krones’ integrated equipment is designed as seamless systems, providing full production line connectivity.

ProMach Scaling Through Acquisitions and Integrated Turnkey Solutions

ProMach is a global leader in packaging machinery, with over 30 manufacturing facilities worldwide. Its May 2025 acquisition of DJS Systems expanded automation for disposable food packaging. Known for offering “single-source” turnkey solutions, ProMach integrates case packers, palletizers, and stretch wrappers with project management and after-sales service. Its scale and broad service network make it a preferred partner for multinational manufacturers.

Sidel Group Innovating with Laser Bottle-Blowing Technology

Sidel specializes in end-of-line systems for liquids, foods, and personal care products, particularly in PET, cans, and glass. At Drinktec 2025, Sidel is debuting a laser bottle-blowing technology, which reduces plastic use and improves sustainability. Its Next Level Performance strategy leverages digital lifecycle tools to extend equipment lifespan. Sidel is also advancing lightweight packaging and 100% rPET solutions, helping clients achieve their sustainability goals.

Schneider Packaging (Pacteon Group) Expanding with Integrated Conveyor Systems

As part of Pacteon Group, Schneider Packaging focuses on robotic case packers, palletizers, and integrated automation. In June 2025, Pacteon acquired Descon Integrated Conveyor Solutions, adding upstream conveyance expertise. Schneider also unveiled a collaborative robot case erector-palletizer at Pack Expo 2024, enabling integrated end-of-line automation in compact spaces. Its custom-engineered robotic systems are well-suited for handling complex product geometries.

KHS GmbH Prioritizing Sustainability in End-of-Line Packaging

KHS provides palletizers, packers, and AGVs for beverage and liquid food industries. With an SBTi-approved target to cut Scope 1 and 2 emissions by 36% by 2028 and achieve net-zero by 2045, sustainability is central to its operations. Its Hamburg expansion in 2025 supports growing demand for resource-efficient packaging lines. The Innopal PLR Palletizer, which cuts energy use by 30%, underscores KHS’s commitment to eco-efficient innovations.

End of Line Packaging Market Share Insights

Automatic Systems Dominate End-of-Line Packaging Market Share by Technology

By technology, automatic systems hold the largest share of the end-of-line packaging market in 2025, driven by the rising adoption of fully integrated solutions across food, beverage, pharmaceuticals, and e-commerce sectors. Companies are investing heavily in automation to boost throughput, reduce labor costs, and minimize errors in high-volume production environments. Semi-automatic systems retain a steady share, appealing to mid-sized manufacturers that require flexibility, moderate throughput, and lower upfront investment compared to fully automated solutions. Manual systems, while holding the smallest share, continue to serve niche markets and low-volume operations, especially in emerging economies where capital budgets are limited. The dominance of automatic systems underscores the industry’s accelerating shift toward Industry 4.0, robotics, and smart packaging lines that deliver efficiency, consistency, and scalability.

Palletizing and Wrapping Lead End-of-Line Packaging Market Share by Function

By function, palletizing, stretch wrapping, and shrink wrapping collectively represent the largest share of the end-of-line packaging market in 2025, as these functions are critical for securing goods during storage and transportation across nearly every industry. Case erecting and case packing also command a significant portion of demand, driven by the global e-commerce boom and the need for shelf-ready, durable packaging that optimizes supply chain flow. Labeling and coding remain indispensable functions, particularly in food, beverage, and pharmaceutical industries, where regulatory compliance and traceability are paramount. Other specialized functions such as inspection and strapping serve targeted applications but represent a smaller portion of the market. The strong position of palletizing and wrapping highlights the critical role of end-of-line packaging in ensuring product safety, logistics efficiency, and brand protection in increasingly complex global supply chains.

United States: Automation and Smart Technologies Driving End-of-Line Packaging Efficiency

The U.S. end-of-line packaging market is experiencing a transformative shift driven by automation and robotics, with collaborative robots (cobots) increasingly used for case packing, palletizing, and de-palletizing. This trend enhances manufacturing productivity and worker safety, while reducing operational costs.

Technological integration is another key growth factor, as AI-driven vision systems, sensors, and IoT devices enable real-time monitoring, predictive maintenance, and quality control. Sustainability is a major focus, with companies adopting recyclable cartons, trays, and stretch films containing post-consumer resins (PCR). Additionally, state-level Extended Producer Responsibility (EPR) laws, particularly in California and Oregon, are influencing market demand, requiring manufacturers to implement eco-friendly, material-efficient end-of-line packaging systems.

Germany: Industry 4.0 and AI Integration Strengthen Packaging Leadership

Germany is a global leader in end-of-line packaging automation, propelled by its strong industrial base and Industry 4.0 initiatives. The country’s focus on interconnected, high-efficiency production lines ensures superior operational performance and reduced labor dependency.

The German market is also integrating AI and machine learning to optimize supply chains, anticipate production disruptions, and minimize material waste. Compliance with the European Green Deal is driving the adoption of machinery capable of handling sustainable and recyclable materials, such as bio-based plastics. Strategic alliances, like the EOL Packaging Experts group, consolidate expertise across companies to deliver fully integrated end-of-line packaging solutions, reinforcing Germany’s position as a European innovation hub.

China: High-Volume Manufacturing and E-Commerce Propel Market Expansion

China’s end-of-line packaging industry benefits from its massive manufacturing and e-commerce ecosystem. The growing need for high-volume, efficient packaging solutions for both domestic consumption and exports drives the demand for advanced end-of-line systems.

Government policies promoting industrial modernization, automation, and packaging waste reduction have accelerated the adoption of robotic palletizing and case packing technologies, improving productivity and material efficiency. Heavy investment in advanced machinery allows Chinese manufacturers to maintain cost-effective production at scale, positioning the country as a critical global supplier of end-of-line packaging equipment.

India: Industrialization and E-Commerce Growth Driving Automated Packaging Adoption

India’s end-of-line packaging market is rapidly expanding, fueled by the Make in India initiative and growing domestic industrialization. Investments in packaging machinery focus on cost-effective, high-efficiency solutions to meet increasing production demands.

The booming e-commerce and FMCG sectors are significant applications for end-of-line equipment, as the demand for packaged foods, personal care products, and electronics continues to rise. Automation adoption, including automatic case erectors, sealers, and palletizers, enhances operational efficiency while reducing labor costs. Government regulations banning single-use plastics further push manufacturers toward eco-friendly and sustainable packaging solutions, aligning operational goals with environmental sustainability.

Brazil: Agribusiness and Consumer Goods Drive Sustainable Packaging Innovation

Brazil’s end-of-line packaging industry is strongly influenced by its thriving agribusiness and consumer goods sectors, which require efficient, reliable, and protective packaging systems. The growing emphasis on sustainability has led companies like Klabin to expand sustainable corrugated board production, necessitating compatible end-of-line equipment.

Consumer awareness and stringent governmental regulations on packaging waste are further propelling the adoption of eco-friendly packaging solutions, which companies leverage as a key differentiator in marketing. The Brazilian market reflects a convergence of industrial growth, sustainability, and regulatory compliance, establishing it as a dynamic region in the global end-of-line packaging landscape.

End of Line Packaging Market Report Scope

End of Line Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.6 Billion

|

|

Market Size (2034)

|

$9.9 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Technology (Automatic, Semi-Automatic, Manual), By Function (Case Erecting, Case Packing, Palletizing, Stretch Wrapping & Shrink Wrapping, Labeling & Coding, Other Functions), By End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Personal Care & Cosmetics, Automotive, Electronics & Semiconductors, Chemicals, Other End-Users), By Product Type (Cartons & Cases, Pallets, Wrappers, Trays, Other Products)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Krones AG, Bosch Packaging Technology (Syntegon Technology), ABB Ltd., Schneider Electric SE, Fanuc Corporation, Omron Corporation, Robopac S.p.A., Sidel, Sealed Air Corporation, Sorma Group, Markem-Imaje (Dover Corporation), Fuji Yusoki Kogyo Co., Ltd., O.N.E. S.r.l., A+F Automation + Fördertechnik GmbH, EOL Packaging Experts

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

End of Line Packaging Market Segmentation

By Technology

- Automatic

- Semi-Automatic

- Manual

By Function

- Case Erecting

- Case Packing

- Palletizing

- Stretch Wrapping & Shrink Wrapping

- Labeling & Coding

- Other Functions

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Medical

- Personal Care & Cosmetics

- Automotive

- Electronics & Semiconductors

- Chemicals

- Other End-Users

By Product Type

- Cartons & Cases

- Pallets

- Wrappers

- Trays

- Other Products

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in End of Line Packaging Market

- Krones AG

- Bosch Packaging Technology (Syntegon Technology)

- ABB Ltd.

- Schneider Electric SE

- Fanuc Corporation

- Omron Corporation

- Robopac S.p.A.

- Sidel

- Sealed Air Corporation

- Sorma Group

- Markem-Imaje (Dover Corporation)

- Fuji Yusoki Kogyo Co., Ltd.

- O.N.E. S.r.l.

- A+F Automation + Fördertechnik GmbH

- EOL Packaging Experts

*List not Exhaustive

Research Coverage

This report investigates the global end-of-line (EOL) packaging market, examining automation breakthroughs, data-driven integration, and sustainability-led innovations that are reshaping production line efficiency across food & beverage, e-commerce, pharmaceuticals, personal care, and industrial applications. USDAnalytics’ analysis reviews the impact of collaborative robotics, digital twin technology, integrated conveyor solutions, and eco-friendly materials, highlighting how these advancements enhance throughput, minimize labor dependency, and optimize operational costs. This report is an essential resource for manufacturing engineers, operations managers, supply chain strategists, and packaging technology investors seeking insights into emerging trends, regulatory compliance, and market dynamics. It provides a detailed overview of industry consolidation, strategic acquisitions, and regional adoption patterns, covering both high-volume production hubs and mid-sized manufacturing facilities. With historical data spanning 2021–2024 and forecasts through 2034, the study presents material innovation trends, functional adoption across automated and semi-automated systems, and strategic company initiatives. The report also highlights performance optimization strategies, predictive maintenance adoption, and turnkey solutions enabling manufacturers to implement Industry 4.0 principles effectively, offering actionable intelligence for decision-makers navigating the evolving EOL packaging landscape.

Scope Highlights:

- Segmentation: By Technology (Automatic, Semi-Automatic, Manual); By Function (Case Erecting, Case Packing, Palletizing, Stretch Wrapping & Shrink Wrapping, Labeling & Coding, Other Functions); By End-Use Industry (Food & Beverages, Pharmaceuticals & Medical, Personal Care & Cosmetics, Automotive, Electronics & Semiconductors, Chemicals, Other End-Users); By Product Type (Cartons & Cases, Pallets, Wrappers, Trays, Other Products)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historical & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies Covered: Profiles and analysis of 15+ companies, including Krones AG, Bosch Packaging Technology (Syntegon Technology), ABB Ltd., Schneider Electric SE, Fanuc Corporation, Omron Corporation, Robopac S.p.A., Sidel, Sealed Air Corporation, Sorma Group, Markem-Imaje (Dover Corporation), Fuji Yusoki Kogyo Co., Ltd., O.N.E. S.r.l., A+F Automation + Fördertechnik GmbH, EOL Packaging Experts

Methodology

The study employs a rigorous methodology combining primary and secondary research to provide a comprehensive view of the end-of-line packaging market. Primary research included interviews with operations managers, packaging engineers, automation specialists, and supply chain directors to validate adoption trends, technology performance, and investment priorities. Secondary research leveraged company annual reports, patent filings, regulatory documents, trade journals, and industrial whitepapers to evaluate innovations in collaborative robotics, digital twin systems, and eco-friendly packaging materials. Market sizing and forecasts were derived using top-down and bottom-up approaches, accounting for production capacity, regional industry demand, automation penetration, and functional adoption across sectors. Competitive benchmarking assessed acquisitions, strategic partnerships, technological deployment, and sustainability initiatives. USDAnalytics ensured data validation through cross-verification, delivering insights that enable industry professionals to optimize production lines, reduce costs, and implement scalable, integrated end-of-line solutions.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.