Drum Liners Market Overview: Scaling to $660.9 Million by 2034 Driven by Chemical Safety, Cost Efficiency, and Sustainability (CAGR 3.6%)

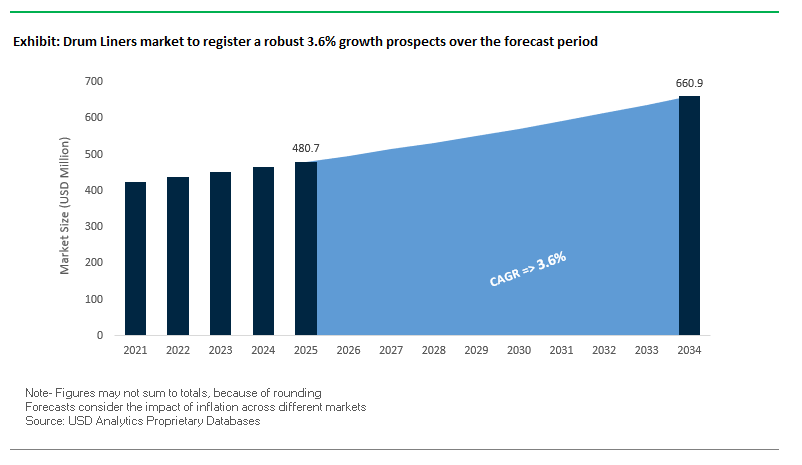

The global drum liners market will expand from $480.7 million in 2025 to $660.9 million by 2034, achieving a steady CAGR of 3.6%. Drum liners are indispensable in industrial packaging, serving as a protective barrier across chemicals, pharmaceuticals, food, and agro-industrials. For professionals in procurement, supply chain, and regulatory compliance, key questions revolve around material innovation (PE, anti-static, food-grade), sustainability readiness, and total cost of ownership through reduced drum reconditioning.

Key Insights for buyers and industry stakeholders

- Chemical & Flammable Safety: Nearly 60% of liners are used in corrosive or volatile applications where inert barrier properties ensure product purity and regulatory compliance.

- Cost Efficiency & Drum Reuse: Polyethylene liners eliminate expensive reconditioning, extend drum lifespan, and lower operating costs.

- Specialized Applications: Food-grade liners support hygienic handling of consumables, while anti-static liners are essential in paints, solvents, and volatile chemicals.

- Sustainability Push: Thinner, recyclable liners are being commercialized, cutting plastic use by up to 25%, in line with circular economy mandates.

Market Analysis: Financial Strength, AI-driven Supply Chains, and M&A Activity Redefining Drum Liners

Sustainability and margin-focused strategies are reshaping the market. In August 2025, Greif Inc. posted strong Q3 earnings on the back of robust performance in its customized polymer division, which includes drum liners. Its focus on value over volume and cash generation underlined how large players are pivoting toward high-margin specialty packaging. At the same time, AI and predictive analytics were highlighted in an industry report (Aug 2025) as a critical enabler for optimizing supply chain forecasting and inventory management of liners in chemical and food sectors.

Strategic mergers and consolidation are influencing market direction. In July 2025, the merger between Smurfit Kappa and WestRock created Smurfit WestRock, consolidating paper-based packaging supply chains. Although the merger was not directly liner-focused, its scale and reach are expected to influence fiber drum and liner pairings across multiple geographies. Earlier, in February 2025, Berry Global announced a $3.6 billion merger with Glatfelter Corporation, integrating its Health, Hygiene, and Specialties (HNNF) business with Global Nonwovens and Films. This deal enhances Berry’s film and polymer expertise, critical for liner innovation.

Sustainable packaging alternatives are accelerating adoption. In May 2025, DS Smith launched DryPack, a recyclable corrugated solution in North America, often paired with liners to replace EPS foam. Similarly, November 2024 saw Dart Container and PulPac introduce dry-molded fiber packaging in North America technology that could influence next-generation bio-based liners. Combined, these developments confirm an industry-wide pivot toward lower-carbon, recyclable solutions within the protective packaging ecosystem.

Trends and Opportunities Reshaping the Drum Liners Market

Strategic Shift Towards High-Performance, Recyclable Resin Formulations

The drum liners market is undergoing a material transformation as manufacturers pivot away from conventional low-density polyethylene (LDPE) toward advanced mono-material and compatibly blended polyolefin structures. This transition is critical for achieving recyclability while maintaining strength and chemical resistance. Global resin suppliers like Dow are spearheading this change with the development of HDPE resins designed specifically for bottles and drums, offering superior stress crack resistance, chemical compatibility, and recyclability. In addition, Dow’s REVOLOOP™ resin line, which incorporates post-consumer recycled (PCR) content, is enabling manufacturers to meet brand-owner circularity goals without sacrificing product performance. Meanwhile, the emergence of biaxially oriented polyethylene (BOPE) films is enabling thinner yet stronger liners, achieving lightweighting benefits that reduce raw material use, lower transportation costs, and shrink the carbon footprint. Collectively, these innovations demonstrate a strategic pivot toward circular, high-performance resin systems that align with global ESG targets and regulatory frameworks.

Integration of Smart Features for Asset Tracking and Content Integrity

Drum liners are evolving beyond their traditional role as protective barriers to become intelligent, data-enabled packaging solutions. Companies are embedding RFID tags, QR codes, and NFC chips into liners to facilitate real-time tracking, authentication, and inventory management. Unlike traditional barcodes, RFID tags offer line-of-sight–free scanning, allowing warehouses to conduct rapid and error-free inventory audits. For high-value chemicals and pharmaceuticals, these smart liners also serve as a defense against counterfeiting, with unique identifiers allowing end-users to verify authenticity instantly. The most advanced iterations integrate environmental sensors that monitor parameters such as temperature, humidity, and oxygen levels critical for ensuring the integrity of sensitive food ingredients or pharmaceutical products. By enabling condition monitoring and predictive analytics, smart drum liners enhance operational efficiency, reduce loss from compromised shipments, and provide a digital audit trail that strengthens supply chain resilience.

Development of Fluoropolymer-Free Barrier Liners for High-Purity Applications

The growing regulatory scrutiny of PFAS-based fluoropolymers is opening a significant white-space opportunity for developing fluoropolymer-free barrier liners. Traditionally, fluoropolymers such as PTFE and PVDF have dominated high-purity applications like semiconductors, biopharma, and specialty chemicals due to their exceptional chemical resistance. However, mounting restrictions such as the U.S. FDA’s voluntary phase-out of PFAS-containing food-contact agents in 2024 are pushing the industry toward alternatives. Research highlights polypropylene (PP) and polyolefin-based composites as promising candidates, offering comparable resistance with far lower extractables. Companies like Saint-Gobain Medical have indicated that polypropylene is emerging as a viable fluoropolymer substitute for ultra-trace applications, where contamination levels must remain at sub-ppb (parts per billion). For sectors where purity and compliance are mission-critical, the commercialization of non-fluoropolymer high-barrier liners represents not just regulatory alignment but also a next-generation growth avenue.

Closed-Loop Reusable Liner Systems with Advanced Take-Back Logistics

Beyond single-use recycling, the shift toward circular economy packaging models presents a major growth opportunity for closed-loop, reusable liner systems. These involve designing thicker, durable liners capable of multiple trips while building reverse logistics systems for collection, cleaning, and recertification. Research on life cycle impacts shows that reuse can drastically reduce environmental footprints: for example, a steel drum reused 10 times yields far lower emissions than single-use formats a principle now being extended to liners. Forward-looking manufacturers are exploring service-based business models, offering liner reuse programs that include logistics, inspection, and refurbishment, locking in long-term client relationships. By embedding asset-tracking software and IoT-enabled monitoring, companies can optimize liner availability and ensure compliance with strict quality standards. Such models reduce customer costs over time, minimize waste, and allow suppliers to create new recurring revenue streams positioning reusable drum liners as a core component of sustainable industrial supply chains.

Competitive Landscape: Key Players Driving Innovation in the Drum Liners Market

The drum liners market is moderately concentrated, with large packaging multinationals and polymer producers shaping standards for durability, sustainability, and compliance. Competitive positioning depends on global scale, integration, material innovation, and customer-specific customization.

Greif, Inc. strengthens integrated drum and liner solutions

Greif is a global leader in steel, plastic, and fiber drums complemented by an extensive range of liners and inserts. Its vertically integrated portfolio gives customers end-to-end solutions across chemicals, agrochemicals, food, and pharmaceuticals. In August 2025, the company’s stronger margins reflected a strategic pivot to value-added specialty markets. With 2030 goals targeting 100% recyclability and 60% recycled raw material content, Greif aligns its liner products with global circular economy standards.

Berry Global Group innovates with PCR and sustainable film technologies

Berry Global is a top manufacturer of polyethylene drum liners and form-fit inserts, engineered for leak prevention and high chemical resistance. In February 2025, its merger with Glatfelter ($3.6B) underscored its focus on specialty films and nonwovens. Berry is pushing post-consumer recycled (PCR) integration, recently winning recognition for packaging with 30% PCR content. Its extrusion blow molding process ensures seamless liners, while its 240+ global facilities support supply continuity and customization.

CDF Corporation specializes in high-performance industrial liners

CDF Corporation is a niche leader in drum and pail liners, plus IBC inserts, with a reputation for technical excellence. Its portfolio spans vacuum-formed, blow-molded, and barrier liners like the UltraLiner and ChemLiner, designed for oxygen- and vapor-sensitive contents. CDF’s strategic focus is on minimizing waste and improving plant efficiencies, offering customers high-performance liners that extend drum life while supporting sustainability initiatives.

SABIC secures its role as a polymer backbone for liners

While not a direct producer of liners, SABIC supplies the polyethylene and polypropylene resins essential for drum liner manufacturing. Its strategy built on transformation, portfolio management, and sustainability supports liner producers with low-carbon polymer innovation. SABIC’s ongoing investments, including a new petrochemical complex in China, will boost supply of PE/PP and enable next-generation circular packaging feedstocks. Its role as a materials innovator is pivotal for the evolution of recyclable, high-strength liners.

Drum Liners Market Share Insights

Flexible Drum Liners Dominate Market Share by Product Type

Flexible drum liners account for 75% of the global drum liners market in 2025, making them the undisputed leader by product type. Their dominance is driven by unmatched versatility and cost-effectiveness, as they can be manufactured in a wide range of thicknesses and polymer formulations to meet diverse chemical and mechanical requirements. Industries prefer flexible liners because they are compatible with both open-head and tight-head drums, making them suitable for storing liquids, powders, and semi-solids. Their lightweight nature lowers transportation costs while enabling quick installation and removal, streamlining operations in high-volume industrial environments. By minimizing product contamination and ensuring complete evacuation of valuable or hazardous contents, flexible drum liners directly address regulatory compliance and sustainability objectives two of the strongest market drivers in packaging today.

Industrial Chemicals Lead Market Share by Application

Industrial chemicals represent 40% of the drum liners market by application in 2025, making this segment the largest demand driver. Drum liners in this segment are indispensable for preventing corrosive reactions between aggressive chemicals and metal drum surfaces, while also ensuring product purity for high-value specialty chemicals. With rising environmental regulations and stricter handling protocols, chemical manufacturers are increasingly adopting liners to reduce hazardous residue and extend drum reusability, lowering total lifecycle costs. Paints and coatings account for 20% of demand, relying heavily on liners to maintain pigment consistency, prevent contamination, and ensure uniform product quality across every batch. The food and beverages sector represents another high-compliance user group, requiring FDA-approved and ultra-clean liners for syrups, flavorings, and edible oils, where contamination control is non-negotiable. Petroleum and lubricants depend on liners to mitigate corrosion and leaks during storage and transport of viscous or hazardous oils. Meanwhile, pharmaceuticals and cosmetics represent a high-value niche, demanding certified low-extractable materials that ensure the purity and efficacy of sensitive formulations, underscoring the critical safety role drum liners play in regulated industries.

Chemicals Industry Anchors Market Share by End-Use

The chemicals industry holds 45% of the drum liners market share by end-use in 2025, confirming its role as the anchor sector. This dominance reflects the sector’s massive production volumes, ranging from bulk industrial chemicals to specialty formulations, all requiring contamination-free handling and compliance with global safety standards. Paints and coatings follow with a 22% share, supported by consistent demand from construction and manufacturing, where uniform color and quality depend on drum integrity. The food and beverage industry further strengthens the market base by adopting liners for safe, contamination-free bulk transport of ingredients. Pharmaceuticals, while representing a smaller percentage by volume, command disproportionately high value due to their stringent regulatory demands for traceability, certified materials, and controlled manufacturing environments. Petroleum and lubricants complete the end-use mix, leveraging liners as an additional barrier for highly corrosive additives and oils. Collectively, these industries not only sustain large-scale demand but also set evolving benchmarks for liner performance, safety, and sustainability, shaping the strategic direction of innovation in the drum liners market.

United States: Regulatory Compliance and Sustainable Innovation Driving Drum Liners Market

The U.S. drum liners market is significantly shaped by stringent environmental and safety regulations from agencies like the EPA and FDA, which mandate the use of leak-proof liners to prevent contamination of hazardous and sensitive materials. This is particularly critical in the food, pharmaceutical, and chemical industries, where sterility and product integrity are paramount. Manufacturers are responding with high-barrier, customizable drum liners designed to meet specific drum sizes and material requirements, ensuring optimal protection against moisture, chemicals, and other environmental factors.

Sustainability is another key driver. Companies are introducing recyclable, biodegradable, and mono-material drum liners, aligning with circular economy principles. The growth of industrial sectors and e-commerce in the food and beverage industry further fuels demand for reliable, cost-effective packaging solutions. Technological advancements in material science are enabling innovative designs that enhance performance while reducing environmental impact, reflecting the U.S. market’s dual focus on safety and sustainability.

Germany: Eco-Friendly and High-Performance Drum Liners Lead the European Market

Germany’s drum liners market is at the forefront of Europe’s sustainability push, driven by the European Green Deal and national environmental regulations. The market is focused on developing recyclable and environmentally responsible liners that cater to the country’s large chemical and pharmaceutical sectors. Products offering excellent chemical resistance, temperature stability, and superior barrier properties are highly sought after to ensure safe storage and transport of sensitive materials.

Key players are launching eco-friendly drum liners designed for the food and beverage industry, demonstrating a strong commitment to sustainable solutions. Circular economy principles are also central, with reusable drums and liners minimizing cleaning requirements, extending drum life cycles, and reducing operational costs. Germany’s market exemplifies how innovation, sustainability, and high-performance standards converge to create advanced drum liner solutions.

China: Industrial Expansion and Sustainable Diversification Drive Market Growth

China’s drum liners industry is heavily influenced by its position as a global industrial and chemical manufacturing hub. The country’s expanding industrial and chemical sectors drive strong demand for high-quality drum liners for safe handling, storage, and transport of chemicals, petroleum, and other materials. Manufacturers are increasingly focused on cost-effective, high-volume solutions to serve both the domestic and international markets.

The government emphasizes modernizing supply chains and industrial logistics, encouraging the adoption of advanced, secure packaging solutions. Additionally, Chinese manufacturers are diversifying their portfolios to include eco-friendly and sustainable drum liners, aligning with growing international demand for environmentally responsible packaging. This combination of industrial scale, technological advancement, and sustainability initiatives positions China as a key player in the global drum liners market.

India: Industrial Expansion and Regulatory Support Fuel Drum Liners Market

India’s drum liners market is experiencing robust growth, driven by the expansion of the industrial, chemical, pharmaceutical, and food sectors. The need for contamination-free, high-barrier liners is paramount, particularly for ensuring the purity and safety of sensitive products during storage and transportation. The market is also influenced by government initiatives aimed at boosting domestic manufacturing and infrastructure, creating a favorable environment for new investments.

Domestic manufacturers are focusing on producing high-quality drum liners that meet international standards, with significant contracts highlighting the strategic importance of reliable packaging solutions. Companies are investing in advanced production technologies and expanding facilities to cater to both local and export markets, while sustainability trends encourage the development of reusable and eco-friendly liners. This combination of regulatory support, industrial growth, and innovation makes India a rapidly expanding market for drum liners.

Brazil: Agriculture and Chemicals Drive Demand for Flexible and Sustainable Drum Liners

Brazil’s drum liners market is heavily driven by its strong agriculture and chemical industries, where protective liners are essential for storing, transporting, and exporting chemicals, powders, and food ingredients. The market is witnessing rising adoption of flexible drum liners, valued for their cost-effectiveness, ease of use, and compatibility with fiber drums.

Sustainability is increasingly influencing product development. Companies are introducing eco-friendly and reusable plastic liners, addressing environmental concerns and creating new market opportunities. The combined focus on affordable, functional, and sustainable solutions is shaping Brazil’s drum liners market, ensuring it meets both domestic industrial needs and international export requirements.

Drum Liners Market Report Scope

Drum Liners market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$480.7 Million

|

|

Market Size (2034)

|

$660.9 Million

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Product Type (Flexible Drum Liners, Rigid Drum Liners, Semi-rigid Drum Liners), By Material Type (Polyethylene, Polypropylene, PVC, Other Polymers), By Application (Industrial Chemicals, Petroleum & Lubricants, Food and Beverages, Cosmetics and Pharmaceuticals, Paints and Coatings, Other Applications), By End-Use Industry (Chemicals, Food and Beverages, Pharmaceuticals, Paints and Coatings, Petroleum & Lubricants)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global Inc., CDF Corporation, Greif, Inc., Sealed Air Corporation, CDF Corporation, Fujimori Kogyo Co., Ltd., NITTEL, International Plastics, Protective Lining Corp, Vestil Manufacturing Co., ILC Dover LP, The Cary Company, Welch Fluorocarbon, Inc., Dana Poly, Inc., SPP Poly Pack

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Drum Liners Market Segmentation

By Product Type

- Flexible Drum Liners

- Rigid Drum Liners

- Semi-rigid Drum Liners

By Material Type

- Polyethylene

- Polypropylene

- PVC

- Other Polymers

By Application

- Industrial Chemicals

- Petroleum & Lubricants

- Food and Beverages

- Cosmetics and Pharmaceuticals

- Paints and Coatings

- Other Applications

By End-Use Industry

- Chemicals

- Food and Beverages

- Pharmaceuticals

- Paints and Coatings

- Petroleum & Lubricants

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Drum Liners Market

- Berry Global Inc.

- CDF Corporation

- Greif, Inc.

- Sealed Air Corporation

- CDF Corporation

- Fujimori Kogyo Co., Ltd.

- NITTEL

- International Plastics

- Protective Lining Corp

- Vestil Manufacturing Co.

- ILC Dover LP

- The Cary Company

- Welch Fluorocarbon, Inc.

- Dana Poly, Inc.

- SPP Poly Pack

* List Not Exhaustive

Research Coverage

This USDAnalytics report investigates the global drum liners market, highlighting breakthroughs in sustainable materials, smart packaging integration, and circular economy solutions. The analysis reviews market dynamics, regulatory impacts, and technological innovations shaping the industry, with particular focus on chemical, pharmaceutical, and food-grade applications. The report highlights opportunities across recyclable, fluoropolymer-free, and high-performance polyethylene and polypropylene liners, while examining advanced features such as RFID-enabled asset tracking and closed-loop reusable systems. USDAnalytics provides comprehensive insights into material trends, capacity expansions, mergers, and strategic partnerships driving industry evolution. This report is an essential resource for procurement leaders, packaging engineers, and sustainability strategists aiming to optimize total cost of ownership, enhance product integrity, and future-proof operations in alignment with global environmental and safety regulations. Historic data from 2021 to 2024 and forecasts to 2034 allow professionals to benchmark growth, plan investments, and identify strategic gaps, while detailed company profiles support competitive intelligence and partnership decisions.

Scope Highlights:

- Segmentation: By Product Type (Flexible Drum Liners, Rigid Drum Liners, Semi-rigid Drum Liners), By Material Type (Polyethylene, Polypropylene, PVC, Other Polymers), By Application (Industrial Chemicals, Petroleum & Lubricants, Food and Beverages, Cosmetics and Pharmaceuticals, Paints and Coatings, Other Applications), By End-Use Industry (Chemicals, Food and Beverages, Pharmaceuticals, Paints and Coatings, Petroleum & Lubricants)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis and profiles of 15+ companies, including Berry Global Inc., CDF Corporation, Greif, Inc., Sealed Air Corporation, Fujimori Kogyo Co., Ltd., NITTEL, and Vestil Manufacturing Co.

Methodology

The study employs a multi-tiered research methodology combining primary interviews with industry executives, procurement managers, and regulatory experts, alongside extensive secondary research of company reports, trade journals, and government publications. Quantitative data were triangulated using supply-demand modeling, capacity analysis, and historical shipment trends. USDAnalytics applied statistical forecasting methods to project growth trajectories from 2025 to 2034, incorporating scenario-based analysis to reflect regulatory changes, sustainability adoption, and emerging technologies. Competitive benchmarking assessed product portfolios, innovation pipelines, and market penetration of leading manufacturers. ESG and sustainability performance were integrated into the evaluation to ensure insights address both compliance and long-term strategic opportunities. The methodology ensures the report provides actionable intelligence, reliable forecasts, and industry-specific guidance for decision-makers in high-value, regulated applications.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.