Packaging Market Expected to Reach $1,436.7 Billion by 2034 Driven by E-Commerce and Sustainability

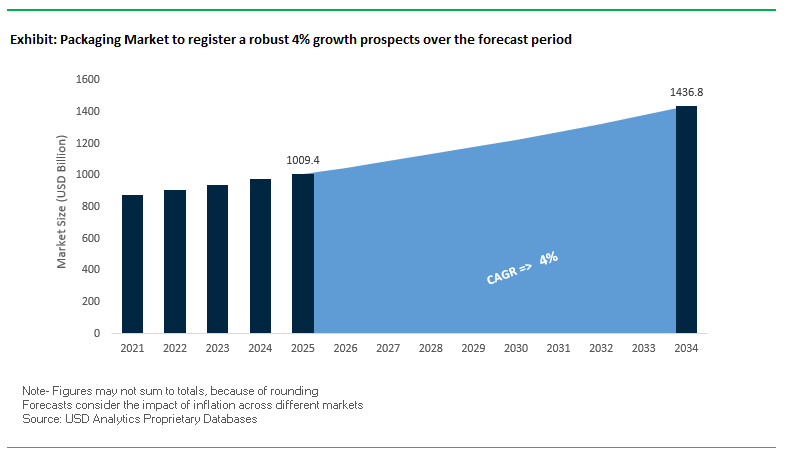

The Global Packaging Market is projected to grow from $1,009.4 billion in 2025 to $1,436.7 billion by 2034, reflecting a CAGR of 4%. This growth underscores the packaging industry’s central role as the critical link between manufacturers and consumers, extending far beyond product containment to protection, branding, and consumer engagement.

The market is shaped by rapid shifts in consumer behavior, e-commerce expansion, and regulatory pressures, requiring manufacturers to adopt innovative, sustainable, and digitally connected packaging solutions.

Key Insights for Industry Professionals:

- E-commerce Growth Driving Protective and Right-Sized Packaging: Rising online shopping is creating demand for packaging that is lightweight, shippable, and capable of enhancing the unboxing experience.

- Circular Economy and Material Innovation: Adoption of mono-materials, bio-based plastics, and high-recycled-content packaging to improve recyclability and reduce environmental impact.

- Smart Packaging and Digital Connectivity: Integration of QR codes, RFID, and digital identifiers enables real-time tracking, anti-counterfeiting, and direct brand-consumer interaction.

- Supply Chain Optimization as a Strategic Focus: Collaborative design efforts aim to reduce shipping costs, minimize packaging dimensions, and improve product protection during transit.

- Regulatory and Sustainability Compliance: Emphasis on packaging solutions that align with evolving environmental regulations and support recyclable or compostable materials.

The packaging industry is increasingly defined by innovation, sustainability, and digitalization, positioning it as a cornerstone of global supply chains and brand engagement strategies.

Market Dynamics Shaped by Strategic Mergers, Expansions, and Technological Breakthroughs

The Global Packaging Industry has witnessed several key developments that highlight its focus on sustainability, digital transformation, and consolidation. In August 2025, Coesia acquired a majority stake in Autoware, a manufacturing software integrator, strengthening its smart manufacturing capabilities.

In July 2025, the all-stock combination of Amcor and Berry Global Group closed, forming a leading global player in flexibles and rigid containers. Simultaneously, UPM Adhesive Materials expanded its advanced label production capacity in North Carolina, reflecting the growing demand for specialized labeling solutions.

May 2025 marked Krones AG’s record profitability, while Avery Dennison opened a joint venture apparel facility in Vietnam, focusing on RFID and Embelex innovations. Earlier, April 2025 saw International Paper complete its $9.9 billion acquisition of DS Smith, reinforcing its position in sustainable paper packaging. Strategic portfolio expansions continued with Arkema acquiring Dow’s flexible packaging laminating adhesives business in December 2024, and Smurfit WestRock’s formation in November 2024, creating a dominant force in corrugated and cushioning solutions.

Trends and Opportunities Reshaping the Global Packaging Market

The Global Implementation of Extended Producer Responsibility (EPR) Regulations

The packaging market is undergoing a regulatory transformation as Extended Producer Responsibility (EPR) becomes a global standard. The European Union’s Packaging and Packaging Waste Regulation (PPWR) is one of the most comprehensive frameworks, mandating legally binding recycled content targets. By 2030, all PET food-contact packaging must contain a minimum of 30% recycled content, a figure that will rise further by 2040. The regulation also bans single-use plastic packaging for fresh produce and requires producers to register with national authorities, adding a compliance layer that compels accountability. Similar momentum is seen in India, where the Plastic Waste Management (Amendment) Rules, 2022 enforce nationwide recycling targets and penalties for non-compliance, forcing producers and brand owners to embed recyclability into their operations.

Global corporations are proactively adapting. Unilever has pledged to halve virgin plastic usage and is investing in advanced R&D tools, including a digital platform that maps over 160 grades of recycled plastics to ensure consistency in color and performance. Additionally, fee modulation policies under EPR systems link financial charges directly to recyclability performance, creating a clear cost incentive for redesigning packaging to meet circularity goals. These frameworks not only create long-term demand for recycled polymers but also accelerate the redesign of packaging systems worldwide, making EPR one of the most powerful drivers reshaping the global packaging landscape.

The Strategic Shift from Plastic to Fiber-Based Packaging Solutions

The packaging market is witnessing an aggressive transition from plastic to fiber-based alternatives, driven by both regulatory bans and corporate sustainability targets. IKEA’s pledge to eliminate all plastics from consumer packaging by 2028 exemplifies this shift, with the retailer already replacing 8,000 tons of EPS annually with molded fiber and corrugated materials. This transition is being mirrored at the corporate level, where International Paper and DS Smith’s merger in early 2025 created a new leader in fiber-based solutions, enhancing capacity for sustainable e-commerce and retail packaging.

E-commerce leaders are also shaping demand. Amazon India’s complete phase-out of single-use plastic packaging, substituting bubble wrap and plastic air pillows with recyclable paper mailers, demonstrates the scalability of fiber alternatives in high-volume fulfillment operations. Performance is no longer a constraint, with academic research highlighting new bio-based coatings that give paper resistance to water, grease, and oils—capabilities previously limited to plastics. These advancements confirm that the transition to fiber is not merely a sustainability choice but a performance-driven innovation, with fiber-based solutions increasingly competing in foodservice, retail, and e-commerce segments once dominated by plastics.

Development and Scaling of Advanced Chemical Recycling Infrastructure

One of the most significant opportunities in the global packaging market is the scaling of advanced chemical recycling to process hard-to-recycle plastics. Planned investment in Europe alone is expected to grow from €2.6 billion in 2025 to €8 billion by 2030, as detailed by Plastics Europe. This infrastructure is critical for handling multi-material films and food-contaminated packaging that cannot be processed through traditional mechanical recycling. Companies like Agilyx and Circular Resources are forming joint ventures to accelerate commercialization in Europe and North America, targeting closed-loop solutions that feed directly into brand-owner supply chains.

The value proposition lies in producing virgin-quality polymers. LyondellBasell’s CirculenRenew portfolio demonstrates this by turning plastic waste into certified food-contact materials with the same performance as virgin resin. Such innovations are essential for brands in sectors like food and healthcare, where safety and performance cannot be compromised. Governmental backing further reinforces this trend—through initiatives like the EU Circular Plastics Alliance, which has set a target of 10 million tons of recycled plastics by 2025. With corporate investment and regulatory support aligning, chemical recycling is positioned as a transformative enabler of circularity in the packaging industry.

Integration of Digital Watermarking for Intelligent Packaging Sortation

The integration of digital watermarking into packaging is emerging as a breakthrough opportunity to improve recycling efficiency and traceability. The HolyGrail 2.0 initiative, a collaboration led by AIM, has completed successful industrial-scale trials with over 90% detection efficiency. These pilots processed tens of thousands of packages daily, proving that digital watermarking can separate packaging not only by polymer type but also by food-contact status and even by brand, enabling high-quality recycled streams.

The technology also enables the creation of a digital product passport, embedding SKU-level information into each package. This allows recyclers to sort with unprecedented precision while providing brands with data to meet EPR compliance and sustainability reporting requirements. Major corporations like Procter & Gamble have already piloted digitally watermarked packaging in Europe for real-world collection and recycling, highlighting industry readiness for large-scale adoption. Sorting technology providers such as Pellenc ST and Tomra are now commercializing add-on modules to integrate digital watermark reading into existing sorting lines, lowering the barriers to infrastructure upgrades. By unlocking high-purity post-consumer resin and enabling traceable packaging ecosystems, digital watermarking is set to redefine the economics of recycling and close the loop in the global packaging industry.

Competitive Landscape Highlighting Global Leaders in Sustainable and Innovative Packaging Solutions

The Global Packaging Industry is dominated by a group of key players leveraging expertise in materials science, manufacturing, and design to deliver high-performance, sustainable, and innovative packaging solutions.

Smurfit WestRock: Creating a Global Paper Packaging Giant with Sustainable Fiber Solutions

Smurfit WestRock, formed in November 2024, is a leading provider of paper-based packaging solutions, integrating sustainable forest management, paper manufacturing, and converting. Its portfolio includes corrugated partitions, paper cushion pads, and corrugated rolls, serving industrial and consumer applications. The company emphasizes a circular business model, replacing plastic with renewable fiber-based materials while driving cost-effective, sustainable solutions globally.

Amcor PLC: Driving Consumer Packaging Innovation with Mono-Material and Recyclable Films

Amcor is a global leader in flexible and rigid packaging, recently combining with Berry Global Group in July 2025 to strengthen its market position. It specializes in mono-material PE flexible films and high-barrier laminates designed for recyclability. Amcor’s offerings, including AmLite Recyclable film, highlight its commitment to sustainable, consumer-friendly packaging solutions across food, beverage, and healthcare sectors.

International Paper Company: Expanding Fiber-Based Packaging Leadership through Strategic Acquisitions

International Paper, a leader in fiber-based packaging and pulp, completed its $9.9 billion acquisition of DS Smith in April 2025, significantly enhancing its European presence. Its offerings include containerboard, corrugated boxes, and specialty paper-based packaging. The company focuses on operational excellence, innovation, and sustainable solutions, aiming to maintain leadership in fiber-based packaging markets.

Sealed Air Corporation: Enhancing Product Protection and Shelf Life with Innovative Foam and Film Solutions

Sealed Air is renowned for protective and food packaging solutions, including Cryovac® films and Instapak® foam-in-place systems. Recent initiatives emphasize touchless automation and recyclable packaging by 2025, supporting e-commerce and industrial logistics. Its strategy focuses on creating secure, efficient, and waste-reducing supply chains, with a commitment to sustainable innovation.

Mondi Group: Advancing Sustainable Laminates and Recyclable Packaging for Consumer Goods

Mondi Group, a global leader in paper and plastic-based laminated packaging, invested €400 million in May 2025 in its Štětí mill to expand production capacity. Collaborative efforts with Nestlé in October 2024 led to fully recyclable pet food pouches, demonstrating Mondi’s commitment to sustainable, high-performance packaging solutions. Its offerings span flexible laminates, paper-based sacks, and , addressing the eco-friendly packaging trend.

Packaging Market Share Insights, 2025-2034

Flexible Packaging Holds the Largest Market Share by Packaging Type in the Packaging Industry

Flexible packaging maintains a strong 47% share of the global packaging market, positioning it as the industry’s fastest-growing and most transformative segment. Its dominance is attributed to lightweight structures, material efficiency, and superior barrier performance, which collectively reduce transportation costs, extend product shelf-life, and align with sustainability mandates. Flexible formats such as pouches, sachets, and films dominate in snacks, beverages, frozen foods, and pharmaceuticals, benefiting from resealability and consumer convenience. Rigid packaging remains essential in categories like carbonated beverages, dairy, and luxury cosmetics, where structural integrity and premium branding are non-negotiable. Semi-rigid packaging continues to serve niche applications in ready-to-eat meals, produce trays, and blister packs, bridging the gap between flexibility and protection. However, it is flexible packaging’s ability to combine performance, sustainability, and e-commerce compatibility that cements its leadership in a market increasingly driven by consumer demand for convenience and circular economy goals.

Food & Beverage Industry Dominates Market Share by End-User in the Packaging Industry

The food and beverage sector consumes 55% of global packaging output, establishing itself as the anchor end-user for both flexible and rigid packaging formats. This dominance is the result of sheer consumption volume combined with stringent requirements for food safety, preservation, and branding. Flexible packaging plays a pivotal role in snacks, frozen meals, and dairy products, while rigid containers remain irreplaceable for carbonated drinks and premium food categories. Semi-rigid solutions such as trays and tubs further strengthen the segment’s dominance in ready-to-eat and fresh produce applications. Beyond food and beverage, pharmaceutical packaging remains the most value-intensive, focusing on high-barrier laminates and tamper-evident features. E-commerce packaging is rapidly reshaping demand for corrugated boxes, mailers, and protective solutions, while personal care and consumer electronics emphasize premium aesthetics and protection. Yet, food and beverage continues to be the strategic cornerstone, setting the pace for innovation, sustainability adoption, and the overall direction of the packaging industry.

United States Packaging Market Driven by EPR Laws, GS1 Sunrise 2027, and Federal R&D Programs

The United States packaging market is undergoing transformation under the GS1 Sunrise 2027 Project, which mandates the shift to 2D barcodes, driving adoption of smart packaging and RFID-enabled labels. At the same time, Extended Producer Responsibility (EPR) laws passed in states like Maine, Maryland, and Washington are pressuring companies to incorporate recyclable substrates and post-consumer recycled (PCR) content in packaging. These overlapping regulatory initiatives are compelling manufacturers to redesign packaging solutions with compliance, sustainability, and traceability in mind.

Federal support is amplifying this momentum. The National Advanced Packaging Manufacturing Program (NAPMP), part of the CHIPS for America Act, has earmarked up to $1.6 billion in R&D for semiconductor advanced packaging—directly boosting demand for high-tech precision packaging systems. On the technology side, U.S. packaging producers are investing in automation, AI, and robotics, with fully automatic machinery reducing labor costs, improving efficiency, and enabling predictive maintenance. Strong demand is seen across e-commerce, food, and pharmaceuticals, where packaging plays a critical role in safety, consistency, and fast last-mile delivery.

Germany Packaging Market Strengthened by PPWR Regulations and Circular Economy Standards

Germany’s packaging market is regulated by the EU Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. This framework mandates recyclability, reuse, and minimum percentages of recycled content by 2030 and 2040, while restricting certain single-use plastics. Combined with the German Packaging Act (VerpackG), significantly expanded in 2022, these laws are forcing packaging companies to adopt sustainable materials and advanced recycling systems.

Germany is also a global leader in circular economy packaging technologies. AI-enabled sorting and optical recycling systems are being deployed to meet high recovery targets for plastics, paper, and glass. In 2025, new transparency rules also introduced stricter labeling and disclosure requirements, obligating packaging to display material content and recyclability status. Key applications include food, beverage, and cosmetics packaging, where high-quality presentation and EU environmental compliance are critical for both domestic and export markets.

China Packaging Market Accelerated by Made in China 2025 and GB 7718-2025 Standards

The packaging market in China is experiencing rapid modernization under the Made in China 2025 plan, which prioritizes automation, AI, and intelligent manufacturing systems. This initiative is supported by billions in state-backed investment aimed at propelling packaging machinery and materials into mid- and high-end markets. Simultaneously, express delivery sector regulations are mandating degradable and reusable packaging, fueling demand for sustainable packaging across industries.

On the regulatory side, the GB 7718-2025 food labeling standard, effective March 16, 2027, will require mandatory allergen labeling for eight substances, legible date marking, and restrictions on misleading claims. It also permits digital labeling via QR codes, offering flexibility for brands to share supplementary product information. With over 175 billion parcel deliveries in 2024, China’s booming e-commerce, consumer goods, and electronics sectors are creating unprecedented demand for automation-ready packaging materials that combine compliance, efficiency, and scalability.

India Packaging Market Supported by Make in India, EPR Rules, and Digital Printing Growth

India’s packaging market is being propelled by the government’s Make in India initiative and the Production Linked Incentive (PLI) scheme, both of which are encouraging local manufacturing and industrial investment. Regulatory changes, particularly EPR rules mandating 30% recycled content in rigid plastics by April 2025, are accelerating adoption of recyclable and circular packaging solutions.

Technological progress is evident in India’s growing adoption of automation, robotics, and AI-driven packaging solutions. The Huhtamaki Foundation’s CloseTheLoop initiative, which is building plastic recycling plants, underscores rising investment in the country’s circular economy infrastructure. Strong demand is being driven by the food and beverage sector, which accounts for a major share of India’s packaging consumption. Meanwhile, the rise of online retail and convenience packaging is accelerating demand for advanced substrates and machinery, particularly flexible packaging formats tailored for juices, sports drinks, and RTD beverages.

Japan Packaging Market Evolving with Positive List Regulations and Sustainable Material Innovation

Japan’s packaging market is adjusting to the positive list system for food-contact materials, effective June 1, 2025, which restricts synthetic substances to only those approved for use. This regulatory change is reshaping packaging development, encouraging adoption of compliant and recyclable substrates for food and beverage applications. Alongside regulation, Japan is also embracing e-labeling, with QR codes and digital formats supporting traceability and consumer-friendly transparency.

Japanese companies are at the forefront of bio-based and recyclable packaging innovation. Stora Enso’s collaboration with local firms to develop paper-based barrier materials illustrates Japan’s shift toward sustainable and functional solutions. National climate goals—cutting emissions 46% by 2030 and achieving net zero by 2050—are accelerating this transformation. Demand is particularly strong in ready-to-drink teas, coffees, and snack packaging, where Japanese consumers value lightweight, durable, and aesthetically appealing designs that combine safety, sustainability, and premium quality.

Packaging Market Report Scope

Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1009.4 Billion

|

|

Market Size (2034)

|

$1436.7 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastics, Glass, Metal, Wood, Others), By Packaging Type (Rigid, Flexible, Semi-Rigid), By End-Use Industry (Food & Beverage, Consumer Electronics, Healthcare & Pharmaceutical, Personal Care & Cosmetics, E-commerce & Logistics, Other Industrial Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, Amcor plc, WestRock Company, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Ball Corporation, Crown Holdings Inc., Sealed Air Corporation, Huhtamaki Oyj, Berry Global Inc., Sonoco Products Company, Graphic Packaging Holding Company, Avery Dennison Corporation, Tetra Pak

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Plastics

- Glass

- Metal

- Wood

- Others

By Packaging Type

- Rigid

- Flexible

- Semi-Rigid

By End-Use Industry

- Food & Beverage

- Consumer Electronics

- Healthcare & Pharmaceutical

- Personal Care & Cosmetics

- E-commerce & Logistics

- Other Industrial Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Packaging Market

- International Paper Company

- Amcor plc

- WestRock Company

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Ball Corporation

- Crown Holdings Inc.

- Sealed Air Corporation

- Huhtamaki Oyj

- Berry Global Inc.

- Sonoco Products Company

- Graphic Packaging Holding Company

- Avery Dennison Corporation

- Tetra Pak

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-layered research methodology to provide an authoritative analysis of the Global Packaging Market. Our research integrates primary data collected through interviews with packaging manufacturers, material suppliers, brand owners, and end-users across food & beverage, healthcare, personal care, e-commerce, and industrial sectors, alongside secondary research from company reports, regulatory filings, industry journals, and sustainability initiatives. We apply quantitative modeling to estimate market size, forecast growth from 2025 to 2034, and analyze trends across material types, packaging formats, and end-use industries. Our approach emphasizes emerging technologies and innovations, including flexible packaging, bio-based materials, digital watermarking, smart packaging, AI-enabled automation, and chemical recycling infrastructure. Regional analysis spans North America, Europe, China, India, Japan, and Brazil, examining regulatory frameworks such as Extended Producer Responsibility (EPR), PPWR, GB 7718-2025, and Make in India initiatives that influence market adoption and sustainability compliance. Competitive strategies, mergers, acquisitions, and R&D developments from leading players like Smurfit WestRock, Amcor, International Paper, and Mondi are assessed to provide actionable insights for investment, operational optimization, and product innovation. By combining these elements, USDAnalytics delivers a comprehensive, market-ready perspective tailored to industry professionals navigating sustainability, digitalization, and consumer-driven packaging trends.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.