Market Overview: Industry Statistics

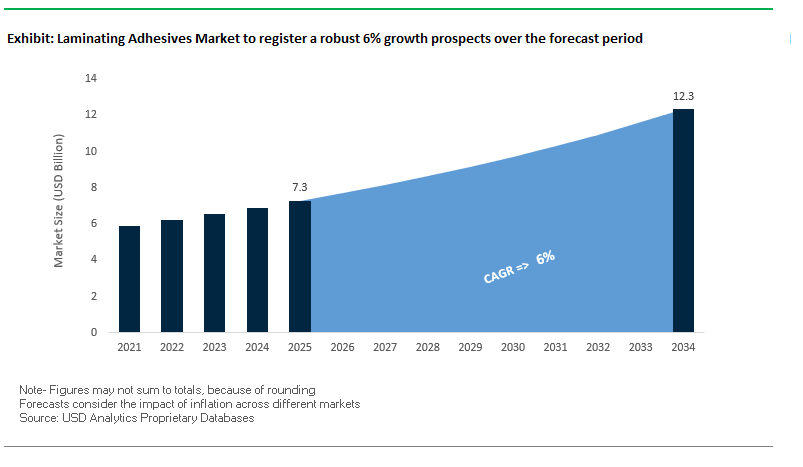

The Global Laminating Adhesives Market is projected to expand from USD 7.3 billion in 2025 to USD 12.3 billion by 2034, growing at a CAGR of 6%. Laminating adhesives play a pivotal role in the flexible packaging industry, enabling high-performance bonding solutions across food, medical, and industrial applications. With rising regulatory pressure and sustainability commitments, the industry is shifting toward solvent-free, water-based, and bio-based adhesives, offering both environmental and performance advantages.

For buyers and professionals, the market answers critical questions about food safety compliance, material evolution, and performance durability. The increasing use of adhesives that resist migration and eliminate primary aromatic amines (PAAs) underscores the sector’s alignment with health and safety standards. Meanwhile, demand is surging from flexible packaging producers who seek lightweight and cost-efficient solutions compared to rigid packaging.

Key Insights for Industry Leaders

- Sustainability focus: Over 70% of packaging manufacturers prefer solvent-free and bio-based laminating adhesives to cut VOC emissions.

- Performance edge: Food and pharma applications require adhesives that withstand heat, moisture, and chemical exposure without compromising safety.

- Flexible packaging driver: Laminating adhesives are essential to the global shift toward flexible packaging, now a dominant trend across FMCG and healthcare.

- Food safety compliance: Rising demand for PAA-free and migration-resistant adhesives aligns with evolving food contact regulations.

Market Analysis: Recent Developments in Laminating Adhesives

The laminating adhesives sector is witnessing rapid innovation and strategic consolidation as manufacturers adapt to rising sustainability expectations and market expansion in Asia-Pacific. In August 2025, Henkel AG & Co. KGaA launched its Adhesin® 4275 water-based laminating adhesive line, targeting food packaging with improved bond strength and faster curing times. In the same month, H.B. Fuller opened a new technical center in Shanghai to accelerate sustainable adhesive development in the Asia-Pacific region, reinforcing China’s role as a growth hub.

Major acquisitions are shaping the competitive landscape. In July 2025, Arkema Group finalized its USD 150 million acquisition of Dow Chemical’s flexible packaging laminating adhesives business, adding well-established brands like MOR-FREE™ and ADCOTE™. Earlier, in June 2025, Bostik (Arkema Group) invested USD 27 million in its Middleton, Massachusetts facility to boost production capacity. Strategic expansion was also evident in May 2025, when Sun Chemical (DIC Corporation) acquired Italian polyurethane manufacturer SAPICI, strengthening its high-performance adhesives portfolio.

Earlier developments reinforced the industry’s sustainability-driven growth. In March 2025, Henkel inaugurated its Technology Center in Bridgewater, New Jersey, enhancing collaboration with regional clients. Meanwhile, H.B. Fuller’s minority stake in Beardow Adams in September 2024 expanded its sustainable adhesive expertise in Europe. Beyond adhesives, Smurfit Kappa and WestRock’s October 2024 merger reshaped global fiber-based packaging supply chains, indirectly impacting adhesive demand for paper-based laminations.

Key Trends and Emerging Opportunities in the Laminating Adhesives Market

Rapid Adoption of Solventless Polyurethane Adhesives for Sustainable Flexible Packaging

The laminating adhesives market is experiencing a significant shift toward solventless polyurethane (PU) adhesives, driven by environmental regulations, energy efficiency, and brand sustainability initiatives. These 100% solids adhesives eliminate the need for drying, reducing VOC emissions and energy consumption while improving operational efficiency. Henkel Adhesive Technologies has introduced a solvent-free system for retort packaging in pet food, offering low monomer content (below 0.1%) and no epoxy silane, aligning with stringent food safety regulations. Solventless adhesives also enhance production efficiency by enabling faster curing and reduced process times, as demonstrated by H.B. Fuller's laminating solutions. Furthermore, these adhesives are gaining recognition for recyclability, with certifications from initiatives like RecyClass ensuring compatibility with mechanical recycling processes. The adoption of solventless PU adhesives not only helps brands meet regulatory compliance but also supports corporate sustainability goals by minimizing CO2 emissions and energy costs.

Development of High-Performance Adhesives for Multi-Material and EV Battery Laminates

Advanced laminating adhesives are becoming critical in industrial applications such as automotive and electronics, particularly for electric vehicle (EV) battery assemblies. These adhesives are engineered to bond dissimilar materials—metals, plastics, and composites—while providing thermal management and dielectric insulation. H.B. Fuller’s EV Bond series demonstrates structural strength and rapid curing, ideal for cell-to-carrier bonding. Thermal interface materials from Dow, including DOWSIL™ and VORATRON™, dissipate heat efficiently, extending battery life and enhancing safety. Flame-retardant adhesives like H.B. Fuller’s EV Protect help mitigate thermal propagation and fire risks, while lightweight polyurethane foams contribute to vehicle range optimization by reducing pack weight. This trend highlights the growing importance of laminating adhesives in high-performance, safety-critical, and multi-material industrial applications.

Creation of Functional Adhesives for PCR Content Packaging Laminates

The global push toward using Post-Consumer Recycled (PCR) plastics in flexible packaging Laminates presents a unique opportunity for adhesive developers. PCR materials are often inconsistent in melt flow, stiffness, and cleanliness, which can compromise lamination performance. H.B. Fuller has developed adhesives capable of bonding PCR films reliably while maintaining optical clarity, ensuring consumer appeal is not compromised. Collaborative initiatives like RecyClass provide standards for adhesives that support PCR recycling processes, creating a structured pathway for circular packaging solutions. The growing adoption of PCR content by major brands drives demand for specialized adhesives, helping businesses meet sustainability commitments, reduce virgin plastic use, and comply with emerging environmental policies.

Adhesives Enabling Fiber-Based Material Replacement for Plastic Barriers

The transition from multi-layer plastics to mono-material fiber-based packaging is accelerating, creating a demand for water-based and bio-based laminating adhesives capable of bonding barrier coatings (e.g., PVOH, biopolymers) to paper and board substrates. These adhesives support recyclability and compostability, providing moisture, grease, and oxygen resistance without hindering industrial composting processes. H.B. Fuller’s water-based barrier coatings offer a sustainable alternative to traditional polyethylene layers, while adhesives like Rakoll U320 incorporate bio-based raw materials, reducing reliance on fossil fuels. Flextra® compostable adhesives are designed to mineralize into CO2 and water, ensuring compliance with compostability standards and supporting the development of environmentally responsible packaging solutions. This trend emphasizes the convergence of sustainability, material innovation, and regulatory compliance in the laminating adhesives market.

Competitive Landscape: Top Companies in Laminating Adhesives

The competitive environment is defined by global adhesive leaders and specialty material innovators driving sustainability, flexible packaging growth, and regulatory compliance.

Henkel AG & Co. KGaA: Driving sustainability and global expansion

Henkel is a market leader in solvent-free, solvent-based, and water-based laminating adhesives under brands like Loctite and Technomelt. In August 2025, it launched Adhesin® 4275, a water-based solution tailored for food packaging. Henkel’s focus is on bio-based formulations with over 30% plant-derived content, aligning with circular economy goals. Its global R&D network and investments in U.S. and China technology centers reinforce its leadership.

H.B. Fuller Company: Innovating with microsphere and bio-based adhesives

H.B. Fuller provides laminating adhesives across hot melts, PSAs, and water-based chemistries. In August 2025, it expanded with a Shanghai technical center to meet Asia-Pacific demand. Fuller is pioneering microsphere adhesive technology, offering peelable solutions ideal for linerless labels. Its strategic investment in Beardow Adams (September 2024) also strengthens its sustainable product portfolio.

Arkema Group (Bostik): Expanding with Dow Chemical acquisition

Through Bostik, Arkema specializes in laminating adhesives for packaging, hygiene, and construction. Its USD 150 million acquisition of Dow’s laminating adhesives business in July 2025 broadened its market reach with established product lines like MOR-FREE™. Arkema also invested USD 27 million in June 2025 to expand U.S. manufacturing capacity, highlighting its commitment to sustainability and high-performance solutions.

3M Company: Leveraging R&D strength in durable adhesives

3M offers a wide spectrum of adhesives, films, and tapes for industrial and consumer applications. Its Versatile Print Label Material demonstrates innovation in printing compatibility and resilience under extreme conditions. 3M is committed to recycled-content and eco-friendly adhesives, backed by its extensive global R&D network, making it a key innovator in durable laminating adhesives.

Ashland Global Holdings Inc.: Focused on Purethane™ brand innovation

Ashland, under its Purethane™ brand, delivers water-based and solvent-free laminating adhesives for flexible packaging. It is actively developing adhesives with enhanced bond strength and fast curing times, suited for food packaging and industrial laminations. Ashland’s vertically integrated manufacturing ensures strict quality control, while its partnerships with printer OEMs expand product compatibility with digital printing technologies.

Laminating Adhesives Market Share Insights

Solvent-Free Adhesives Lead Market Share by Technology in the Laminating Adhesives Industry

Solvent-free laminating adhesives represent the largest technology share at 35%, cementing their role as the most widely adopted solution in 2025. Their leadership stems from their ability to deliver superior performance, faster processing speeds, and compliance with global sustainability mandates by eliminating VOC emissions. These adhesives drastically cut energy consumption by removing the need for drying ovens, making them cost-effective while reducing environmental impact. Their adoption is strongest in flexible packaging for food, beverages, and healthcare products, where high bond strength, optical clarity, and food safety compliance are critical. Water-based and hot-melt adhesives continue to expand, particularly in industrial and non-food applications, while solvent-based systems remain a niche solution for extreme chemical and thermal resistance. However, the shift toward eco-friendly, high-speed, solvent-free systems ensures their dominance in large-scale commercial adoption.

Flexible Packaging Overwhelmingly Dominates Market Share by Application in the Laminating Adhesives Industry

Flexible packaging accounts for a commanding 70% of laminating adhesives demand in 2025, underscoring its role as the backbone of this market. The sector’s dominance is anchored in the exponential rise of multi-layer packaging structures designed to extend shelf life, preserve flavor, and enhance product safety across food, beverage, pharmaceutical, and consumer goods industries. Laminating adhesives here must deliver exceptional bond strength, aroma and moisture barrier performance, and clarity, while fully complying with food safety and migration standards. The surge in e-commerce, convenience foods, and single-serve formats has further accelerated demand for flexible packaging solutions, directly fueling laminating adhesive consumption. While industrial, automotive, and electronics applications represent high-value niches requiring specialized adhesives, the sheer global scale and regulatory intensity of flexible packaging guarantee its market leadership.

United States Laminating Adhesives Market Driven by FDA Regulations and Automotive Innovations

The U.S. laminating adhesives market is heavily influenced by a fragmented regulatory environment. FDA regulations ensure product integrity and safety across flexible packaging in the food, beverage, and pharmaceutical industries. Additionally, the Drug Supply Chain Security Act (DSCSA) mandates unique identifiers on pharmaceutical packaging, increasing demand for high-performance laminating adhesives for secure and durable labels.

Technological advancements are driving market growth, with innovations such as low-VOC water-based adhesives for multi-layer film lamination and eco-friendly, reusable solutions integrated with real-time tracking capabilities. Strategic corporate moves, such as Arkema’s $150 million acquisition of Dow's flexible packaging laminating adhesives business in May 2024, have expanded production capacity and market presence. Key applications include the e-commerce and automotive sectors, particularly in electric vehicles, where adhesives are essential for lightweight, high-performance components. Sustainability remains central, with increasing adoption of eco-friendly laminating adhesives aligning with regulatory compliance and consumer demand for green packaging solutions.

Germany Laminating Adhesives Market Strengthened by EU Regulations and Circular Economy Leadership

Germany’s laminating adhesives market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR) effective February 2025. The regulation mandates fully recyclable or reusable packaging by 2030, driving demand for sustainable laminating adhesive solutions.

The market emphasizes technological innovation, with companies like Henkel launching bio-based flexible laminating adhesives containing over 30% plant-derived content for pharmaceutical and food packaging. Germany’s Packaging Act (VerpackG) incentivizes recyclability, supporting circular economy initiatives and sustainable product design. Corporate investments in high-performance, eco-friendly adhesives further reinforce Germany’s leadership in the European laminating adhesives market, catering to evolving regulatory and market demands.

China Laminating Adhesives Market Accelerated by Green Policies and AI-Enabled Production

China’s laminating adhesives market is shaped by government initiatives promoting sustainability and digitalization. The “dual carbon” goal and the Action Plan for Large-Scale Equipment Updates encourage recycling and the use of sustainable materials in all industries, including laminating adhesives. A mandatory AI labeling law, rolled out in September 2025, opens new applications for digital-enabled laminating adhesives, particularly in e-commerce and high-value packaging.

Regulatory reforms, including GB/T 31268 addressing excessive packaging, impact packaging design for consumer goods. Chinese manufacturers are investing in automation, 5G-enabled industrial internet, and AI technologies to enhance production efficiency and flexible manufacturing capacity. Domestic production initiatives reduce reliance on imports, with booming e-commerce, electronics, and automotive sectors driving demand for high-quality, circular laminating adhesives.

India Laminating Adhesives Market Expands Through Circular Economy and Pharmaceutical Growth

India’s laminating adhesives market is expanding due to government initiatives promoting a circular economy and domestic manufacturing. The Make in India initiative and PLI schemes for Pharmaceuticals and Medical Devices are driving technological upgradation and increased production capacity. Recent reports indicate cumulative pharmaceutical sales exceeding INR 2.66 lakh crore, boosting demand for compliant, high-performance laminating adhesives.

Technological advancements, such as Pidilite Industries’ water-based adhesives, support the development of eco-friendly laminating adhesives. Corporate investments are increasing to meet the growing needs of food and beverage, pharmaceutical, and e-commerce sectors. Rising industrial exports, especially pharmaceuticals, are fueling demand for modern, durable laminating adhesives that meet international safety and regulatory standards.

Japan Laminating Adhesives Market Propelled by Advanced Manufacturing and Regulatory Compliance

Japan’s laminating adhesives market benefits from precision manufacturing and innovation. Companies like Toyo-Morton and LINTEC lead in advanced adhesive technologies, including epoxy-silane-free and specialty laminating adhesives for sustainable packaging solutions.

The Plastic Resource Circulation Act and revised food contact material regulations (effective June 2026) guide the market toward eco-friendly and high-performance adhesives. Innovation focuses on self-sealing, barrier-enhanced laminating adhesives for automotive, pharmaceuticals, and packaging industries, catering to both functional and aesthetic requirements. The market is shifting toward value-added products, emphasizing durability, high performance, and environmental compliance.

Brazil Laminating Adhesives Market Driven by Sustainability Initiatives and Corporate Investments

Brazil’s laminating adhesives market is growing due to sustainable waste management policies, such as the National Solid Waste Policy and the 2024 ban on imported solid waste, which encourage local recycling and circular packaging solutions. These initiatives create opportunities for laminating adhesives made from recycled materials.

Technological innovation is being driven by companies like Henkel, which announced plans to build a new Inspiration Center for Adhesive Technologies in São Paulo to enhance collaboration and sustainable solutions. Key applications are concentrated in the food, beverage, and agricultural sectors, while the EU-Mercosur trade agreement is expected to attract further investments and diversification. Brazil’s market combines sustainability, innovation, and regulatory alignment to strengthen its role in the Latin American laminating adhesives industry.

Laminating Adhesives Market Report Scope

Laminating Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.3 Billion

|

|

Market Size (2034)

|

$12.3 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Technology (Water-based, Hot-melt-based, Solvent-based, Solvent-free, Others), By Resin (Polyurethane, Acrylic, Epoxy, Others), By Application (Flexible Packaging, Industrial, Automotive, Electronics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema SA, 3M Company, Dow Chemical Company, Toyo-Morton, Ltd., DIC Corporation, Sika AG, Pidilite Industries Ltd., Ashland Global Holdings Inc., Bostic S.A., Vimasco Corporation, Daicel Corporation, Coim Group, DuPont de Nemours Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Laminating Adhesives Market Segmentation

By Technology

- Water-based

- Hot-melt-based

- Solvent-based

- Solvent-free

- Others

By Resin

- Polyurethane

- Acrylic

- Epoxy

- Others

By Application

- Flexible Packaging

- Industrial

- Automotive

- Electronics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Laminating Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema SA

- 3M Company

- Dow Chemical Company

- Toyo-Morton, Ltd.

- DIC Corporation

- Sika AG

- Pidilite Industries Ltd.

- Ashland Global Holdings Inc.

- Bostic S.A.

- Vimasco Corporation

- Daicel Corporation

- Coim Group

- DuPont de Nemours Inc.

* List Not Exhaustive

Methodology

USDAnalytics combines primary and secondary approaches to ensure data reliability and market accuracy for the Laminating Adhesives Market; primary research comprised structured interviews with adhesive R&D leaders, packaging engineers, procurement heads, converter operations managers, sustainability officers, and supply-chain stakeholders across North America, Europe, Asia-Pacific and Latin America, while secondary research covered company annual reports, regulatory databases (FDA, EU PPWR), patent filings, sustainability disclosures, trade statistics, and peer-reviewed industry journals. Advanced data triangulation validated market sizing and growth projections by integrating macroeconomic indicators, resin and raw-material pricing trends, converter capacity deployments, and technological adoption models for solvent-free, water-based and bio-based chemistries. Forecasts were built using blended top-down and bottom-up methodologies—combining unit-volume estimates (flexible packaging lamination runs, EV battery laminates, PCR film uptake) with revenue benchmarks and vendor shipment data—while regional insights were contextualized against policy frameworks (EPR, recyclability mandates), retailer recycling stream profiles, and trade flows. Scenario stress-testing assessed risks and opportunities from accelerated PCR adoption, mono-material packaging mandates, and industrial shifts toward solventless PU systems, ensuring the report delivers accurate, actionable, evidence-based guidance for R&D, procurement, sustainability and operations teams.

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.