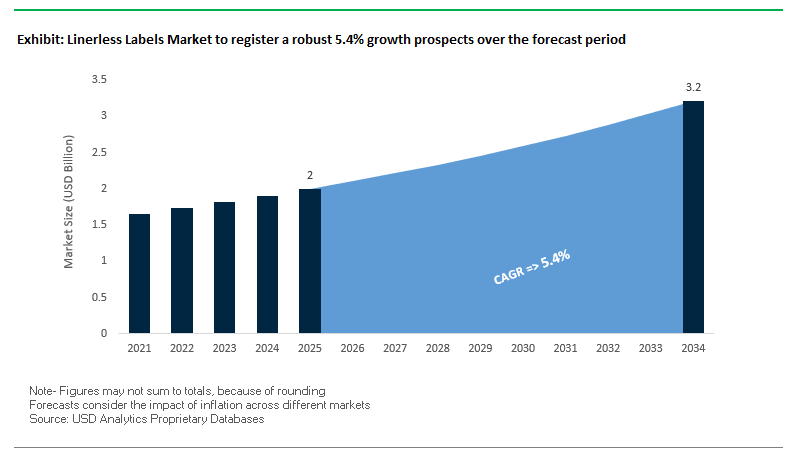

Linerless Labels Market Overview: Waste Reduction and Sustainability Driving Growth (MV: USD 2 Bn in 2025 → USD 3.2 Bn by 2034, CAGR 5.4%)

The global linerless labels market is witnessing robust growth as industries prioritize sustainability, efficiency, and operational savings. Unlike conventional pressure-sensitive labels, linerless formats eliminate the backing liner, resulting in 15–40% less material waste and lower disposal costs. For businesses, this not only reduces environmental impact but also provides direct cost savings in waste management.

The market is further fueled by operational efficiency gains, with rolls carrying up to 40–80% more labels, reducing machine downtime and increasing throughput in high-speed production lines. The demand is particularly strong in e-commerce, logistics, food, and retail, where variable information labeling is critical. Meanwhile, sustainable packaging commitments and regulatory pressure are accelerating adoption, with linerless solutions emerging as a key enabler of corporate ESG targets.

Key Insights for Industry Professionals

- Waste Reduction Champion: Eliminates liners, cutting label-related waste by up to 40%.

- Efficiency Gains: Enables more labels per roll, improving line uptime and productivity.

- Sustainability Premium: Aligns with brand and regulatory demand for eco-friendly solutions.

- E-commerce Growth: Strong adoption for shipping and logistics due to cut-to-length flexibility.

Market Analysis: Recent Industry Developments Expand Sustainable Capacity

The linerless labels market has seen significant innovation and capacity expansion in 2025, reflecting strong demand from logistics, food packaging, and retail sectors. In August 2025, Siegwerk partnered with Ravenwood Packaging to advance linerless labeling with new ink and coating technologies, while Domino Printing Sciences launched its N410 digital LED inkjet press, optimized for variable-data applications. Also in August 2025, Avery Dennison showcased its decorative linerless pressure-sensitive labels using patented micro-perforation technology, underscoring the trend toward premium shelf appeal combined with sustainability.

Earlier, in July 2025, Comexi introduced a retrofit-enabled flexo press for linerless production, demonstrating strong equipment-side innovation. In June 2025, UPM Raflatac rebranded as UPM Adhesive Materials, signaling an expanded role in linerless and specialty adhesives. In May 2025, CCL Industries announced a new production capacity investment in North America, directly addressing growing customer demand. Material science advancements also shaped the year—Bostik (Arkema Group) committed $27M in March 2025 to boost adhesive production for linerless applications, while Henkel’s January 2025 Technology Center opening in New Jersey further positioned adhesives at the heart of linerless growth.

Key Trends and High-Impact Opportunities in the Linerless Labels Market

Rapid Adoption in E-Commerce Fulfillment to Address Labor and Throughput Constraints

The linerless labels market is experiencing accelerated adoption in e-commerce fulfillment centers due to operational efficiency and cost optimization pressures. By eliminating the silicone-backed liner, linerless labels allow more labels per roll—up to 50% more according to Lowry Solutions—reducing roll changes and minimizing production downtime. This innovation improves workplace safety by removing the slip hazards posed by discarded liners and lowers disposal costs, as highlighted by RRD. Additionally, fewer rolls reduce shipping and storage requirements, providing tangible economic benefits for high-volume logistics operations. Optimized print-and-apply systems, such as Zebra Technologies’ direct thermal printers with non-stick platen rollers, enable rapid label application at high speeds while minimizing maintenance. These capabilities position linerless labels as a key enabler for scalable, high-throughput e-commerce operations.

Development of High-Performance Functional Coatings for Demanding Applications

Significant R&D in linerless label technology is enhancing performance in challenging environments, including cold storage, oily surfaces, and curved packages. UPM Raflatac’s freezer-grade adhesives maintain strong adhesion even at −20°C, with clean-cut technology that minimizes residue on printer blades, optimizing uptime in cold-chain logistics. Advanced release coatings protect against moisture and chemicals, extending label durability and shelf life. Modern adhesives adhere to diverse substrates, including plastics and moisture- or oil-coated surfaces, expanding linerless labels’ applicability across industrial, food, and logistics environments. The integration of clean-cut technology further reduces printer maintenance needs and enhances reliability, allowing companies to leverage linerless labeling for high-speed automated production lines.

Integration with Blockchain and IoT for Enhanced Fresh Food Traceability

Linerless labels provide an ideal platform for integrating traceability solutions with blockchain and IoT technologies. Each label can carry unique digital IDs, enabling immutable, item-level traceability for fresh produce and premium food products. Blockchain ensures secure, tamper-proof tracking of products from farm to fork, as highlighted in MDPI’s academic review, fostering consumer trust and regulatory compliance. Integration allows accelerated recall processes, reducing response times from weeks to seconds, and enhances food safety by isolating contamination events swiftly. QR codes on linerless labels create a direct link for consumers to access verified product origin and sustainability credentials, supporting brand transparency and enabling premium pricing for ethically sourced or organic products.

On-Demand, Sustainable Labeling for In-Store Bakeries and Delis

Retail grocery stores are increasingly leveraging linerless labels to provide on-demand labeling for fresh, variable-weight items while reducing waste. The variable length capability allows precise label sizing, eliminating pre-cut label waste and minimizing inventory requirements. Integrated printer-scale systems enable fast, accurate labeling of deli meats, cheeses, baked goods, and prepared foods, ensuring compliance and speed in high-volume environments. The elimination of the non-recyclable liner directly contributes to retailers’ sustainability initiatives. UPM Raflatac’s OptiCut™ WashOff solution allows labels to be removed cleanly from reusable containers, promoting circularity and reducing environmental impact across food logistics and in-store operations.

Competitive Landscape: Leading Companies in the Linerless Labels Industry

The linerless labels market is led by global players that are expanding production, investing in adhesives, and integrating advanced printing technologies to align with sustainability and automation trends.

Avery Dennison Corporation: Pioneering Decorative Linerless Technology

Avery Dennison has established itself as a leader in pressure-sensitive and linerless labeling, leveraging its strength in adhesives and material science. In August 2025, it unveiled decorative linerless solutions at Labelexpo Europe with patented micro-perforation technology, designed to enhance shelf appeal. Its AD LinrSave and AD LinrConvert products directly support sustainability and waste reduction, while the company’s RFID and smart-label integration keeps it at the forefront of digital identification and traceability.

UPM Adhesive Materials: Expanding Beyond Labels with Sustainable Solutions

Formerly UPM Raflatac, the company rebranded in June 2025 to reflect a broader focus beyond label materials. Its portfolio includes direct thermal linerless products and the innovative OptiCut WashOff linerless label, developed for returnable plastic containers. UPM’s large distribution network ensures global availability, while its fossil-free roadmap and focus on adhesive residue-free separation strengthen its sustainability positioning.

CCL Industries Inc.: Investing in North American Capacity Expansion

CCL Industries is a global leader in specialty labels and packaging, with strong exposure to consumer packaged goods, healthcare, and personal care. In May 2025, it announced a new North American linerless capacity expansion, directly targeting the fast-growing logistics and retail sectors. Beyond linerless, CCL continues to innovate with RFID, anti-theft, and intelligent labeling technologies, offering customers both sustainability and traceability advantages.

3M Company: Innovating with Industrial Linerless Adhesive Solutions

3M remains a powerhouse in adhesive technologies, offering linerless tapes and label materials designed for industrial, electrical, and specialty use. Its Scotch® Linerless Rubber Splicing Tape 130C is a benchmark product, providing UV resistance, moisture sealing, and high durability. The company continues to push innovation in sustainable adhesive chemistry, making its solutions adaptable for diverse linerless label applications.

Henkel AG & Co. KGaA: Driving Adhesive Innovation for Linerless Applications

Henkel plays a critical role as an adhesive solutions provider for linerless labeling. In January 2025, it opened its Bridgewater, New Jersey Technology Center, emphasizing sustainability and innovation in adhesives. Henkel’s portfolio includes hotmelt, UV-curing, and water-based adhesives optimized for linerless applications. Its strength lies in partnerships with converting equipment manufacturers, ensuring seamless integration into production lines while maintaining food safety compliance and performance.

Linerless Labels Market Share Insights

Food & Beverages Dominate Market Share by Application in the Linerless Labels Industry

Food and beverages lead the linerless labels industry with a 32% market share in 2025, making this the largest application area. Fresh produce, bakery, and prepared foods require fast, flexible, and reliable labeling systems for variable information such as price, weight, and barcodes. Linerless technology eliminates liner waste, improving sustainability while streamlining operations in supermarkets, butcher counters, and delis. Retail and e-commerce hold the second-largest share at 25%, fueled by the explosive growth of omnichannel fulfillment and last-mile logistics, where linerless shipping labels reduce costs and waste. Industrial and logistics applications contribute a significant portion, relying on durable linerless pallet and tracking labels to improve supply chain efficiency. Pharmaceuticals and healthcare, while smaller in volume, represent a high-value segment where linerless labeling ensures accuracy, sterility, and contamination-free application for patient wristbands, lab samples, and prescription packaging. Consumer goods and other applications follow as niche adopters, typically for inventory management or promotional labels. This distribution highlights how food and beverages anchor linerless adoption, while retail and e-commerce act as the engine of rapid future growth.

Paper Secures Market Share Leadership by Facestock Material in the Linerless Labels Industry

Paper facestock dominates with a 65% share of the linerless labels industry in 2025, cementing its role as the sustainable backbone of this market. Its renewable nature, biodegradability, and wide recyclability align perfectly with the industry’s mission to eliminate liner waste, making it the preferred choice across food, retail, and logistics. Paper also offers superior printability for barcodes and variable data, ensuring operational efficiency in high-volume labeling environments. Plastic films, however, maintain a critical 30–35% share for applications demanding durability, chemical resistance, or extreme temperature performance, such as outdoor logistics, automotive, and chemical labeling. These synthetic substrates are essential where moisture, abrasion, or UV exposure challenge paper’s performance. The small “others” segment, around 2–3%, represents emerging innovations like direct thermal facestocks and advanced composites designed to improve sensitivity, print life, or adhesion on difficult surfaces. This segmentation reflects a clear hierarchy: paper as the sustainability leader, plastics as the performance enabler, and niche materials as the innovation frontier.

United States Linerless Labels Market Gains Momentum Through Regulatory Compliance and Sustainable Innovations

The U.S. linerless labels market is shaped by a fragmented regulatory landscape, with FDA regulations ensuring safety and integrity across pharmaceuticals, food, and beverages. State-level plastic waste reduction initiatives are driving the shift toward sustainable linerless solutions that eliminate backing liners, reduce waste, and optimize logistics.

Technological advancements, such as UPM Raflatac’s OptiCut™ WashOff, enable residue-free labeling for returnable and reusable food containers, supporting industrial and home applications. Corporate investments, exemplified by Avery Dennison’s acquisition of Catchpoint Ltd.’s linerless technology, aim to expand sustainable labeling solutions. High demand is seen in e-commerce, food service, and retail sectors, particularly for variable length labeling and track-and-trace applications, emphasizing the growing importance of eco-friendly, high-performance linerless labels.

Germany Leads the Linerless Labels Market With Circular Economy and High-Performance Innovations

Germany’s linerless label industry operates under the strict EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating recyclable and reusable packaging by 2030. This framework encourages widespread adoption of sustainable linerless labeling solutions that reduce material waste at the source.

German manufacturers leverage Industry 4.0 technologies, including advanced adhesives and release coatings, to create high-performance linerless labels with improved durability and peelability. The Packaging Act (VerpackG) incentivizes recyclable designs, strengthening the position of eco-friendly linerless labels in the market. Companies like Henkel are expanding capabilities to meet the growing demand for sustainable, high-performance labeling solutions, positioning Germany as a global hub for innovation in linerless technology.

China Linerless Labels Market Accelerates With Green Policies and Smart Manufacturing

China’s linerless labels market is evolving under the dual carbon goal, promoting eco-friendly materials and recycling initiatives. Government programs like the Action Plan for Large-Scale Equipment Updates and the China Environmental Labeling program encourage the adoption of sustainable labeling solutions, including linerless labels.

Regulatory reforms, such as GB/T 31268, address excessive packaging in consumer goods and e-commerce, driving demand for high-efficiency, variable data printing linerless labels. Investments in automation, AI, and RFID-enabled smart manufacturing are enhancing production efficiency and supply chain optimization. Domestic manufacturers are expanding capacity to cater to rapidly growing e-commerce, electronics, and food sectors, positioning China as a major market for specialized, circular linerless labels.

India Linerless Labels Market Expands With Circular Economy Initiatives and Advanced Adhesives

India’s linerless labels market is benefiting from circular economy initiatives and regulatory pushes, including the ban on single-use plastics in 2022, which accelerated the adoption of sustainable flexible packaging. Innovative solutions, such as Pidilite Industries’ water-based adhesives, are enabling the development of eco-friendly linerless labels for diverse applications.

Corporate investments are rising to meet demand from food and beverage, pharmaceutical, and e-commerce sectors, driven by the need for high-performance labeling solutions. The country’s growing industrial exports, particularly in pharmaceuticals, are further stimulating demand for modern, sustainable linerless labels that comply with international safety and quality standards.

Japan Linerless Labels Market Strengthens With Advanced Materials and Specialty Adhesives

Japan’s linerless labels industry leverages its precision manufacturing expertise to deliver next-generation labeling solutions. Companies like LINTEC are innovating in adhesive technologies and advanced label materials to meet stringent regulatory standards. The Plastic Resource Circulation Act and revised food contact material regulations provide guidance for eco-friendly labeling and reducing single-use plastics.

The market focuses on high-performance, value-added linerless labels with features like superior durability, barrier properties, and self-sealing functionality. Japanese manufacturers are catering to food, beverage, and industrial sectors, emphasizing innovation in label functionality and environmental sustainability.

Brazil Linerless Labels Market Expands With Sustainable Practices and Premium Applications

Brazil’s linerless labels market is evolving under the National Solid Waste Policy, which modernizes waste management and promotes sustainability. Technological advancements are focused on biodegradable, recyclable, and compostable labeling materials, reducing environmental impact.

High demand is observed in food and beverage and agricultural sectors, with companies like Beontag introducing premium self-adhesive wine labels for Latin American markets. Corporate investments are being bolstered by the EU-Mercosur trade agreement, facilitating market diversification and encouraging adoption of high-performance, eco-friendly linerless labels across domestic and international applications.

Linerless Labels Market Report Scope

Linerless Labels Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Adhesive Type (Hot-melt Adhesives, Water-based Adhesives, Others), By Printing Technology (Thermal Printing, Digital Printing, Flexographic Printing, Offset Printing), By Application (Food & Beverages, Retail & E-commerce, Consumer Goods, Industrial & Logistics, Pharmaceuticals & Healthcare, Other Applications), By Facestock Material (Paper, Plastic Films, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, UPM Raflatac, CCL Industries Inc., 3M Company, Fuji Seal International, Inc., LINTEC Corporation, SATO Holdings Corporation, Mondi Group, Beontag, Irplast S.p.A., Catchpoint Ltd., Ritrama S.p.A. (a part of Fedrigoni), R.R. Donnelley & Sons Company, Sticky Labels, Hub Packaging

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Linerless Labels Market Segmentation

By Adhesive Type

- Hot-melt Adhesives

- Water-based Adhesives

- Others

By Printing Technology

- Thermal Printing

- Digital Printing

- Flexographic Printing

- Offset Printing

By Application

- Food & Beverages

- Retail & E-commerce

- Consumer Goods

- Industrial & Logistics

- Pharmaceuticals & Healthcare

- Other Applications

By Facestock Material

- Paper

- Plastic Films

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Linerless Labels Market

- Avery Dennison Corporation

- UPM Raflatac

- CCL Industries Inc.

- 3M Company

- Fuji Seal International, Inc.

- LINTEC Corporation

- SATO Holdings Corporation

- Mondi Group

- Beontag

- Irplast S.p.A.

- Catchpoint Ltd.

- Ritrama S.p.A. (a part of Fedrigoni)

- R.R. Donnelley & Sons Company

- Sticky Labels

- Hub Packaging

* List Not Exhaustive

Methodology

The research methodology for the Linerless Labels Market conducted by USDAnalytics combines primary and secondary research approaches to ensure high accuracy and actionable insights. Primary research involved extensive interviews with packaging manufacturers, adhesive suppliers, logistics operators, and technology providers to capture real-time industry trends, regulatory challenges, and end-user preferences. Secondary research leveraged annual reports, government publications, trade associations, sustainability reports, and technical white papers to validate data and assess market dynamics. Both top-down and bottom-up estimation methods were used to determine market size, factoring in macroeconomic conditions, e-commerce growth, technological innovations, and ESG-driven policies. Forecasting models were designed to account for regulatory shifts, raw material trends, and technological adoption, providing a comprehensive market outlook. This integrated methodology allows USDAnalytics to deliver industry intelligence that supports strategic decision-making for professionals in packaging, logistics, retail, and manufacturing sectors.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.