Water-Based Adhesive Market Size, Overview, and Growth Outlook (2025–2034)

Global Water-Based Adhesive Market Projected to Surpass $86 Billion by 2034 Fueled by Sustainability and VOC Reduction

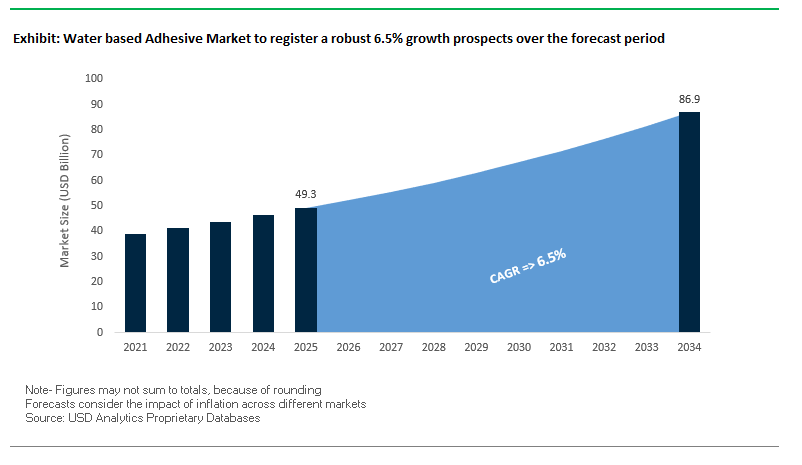

The global water-based adhesives market is expected to grow from $49.3 billion in 2025 to $86.9 billion by 2034, at a CAGR of 6.5%. Water-based adhesives are increasingly preferred over traditional solvent-based formulations due to their low or zero VOC emissions, improved worker safety, and alignment with environmental regulations. This market is central to industries like packaging, construction, automotive, and consumer goods, where sustainable, high-performance adhesive solutions are crucial.

Key Insights for industry professionals and buyers:

- Regulatory compliance with EPA and EU REACH standards is driving widespread adoption of low-VOC water-based adhesives.

- Bio-based formulations using renewable resources such as castor oil are becoming a major trend, reflecting the push toward a circular economy.

- Enhanced performance formulations now offer fast curing, water and heat resistance, and strong bonding across diverse substrates.

- Operational efficiency improves as low-odor, non-toxic adhesives reduce ventilation and PPE requirements, lowering manufacturing costs.

- Market innovation focuses on versatile, high-speed manufacturing solutions to meet industrial and consumer needs.

Market Analysis: Technological Innovations and Strategic Partnerships Are Driving Growth in the Water-Based Adhesives Industry

The water-based adhesives market is witnessing significant innovation and strategic consolidation. In August 2025, Klöckner Pentaplast won the German Packaging Award for its kp 100% Tray2Tray® innovation, showcasing its commitment to sustainable solutions. Coveris completed an $11 million facility upgrade in Germany, adding cast film extrusion and advanced printing capabilities to meet growing customer demands. The same month, a study highlighted composite antimicrobial films with strong bactericidal activity and biodegradability, emphasizing the sector’s focus on performance and environmental safety.

Earlier innovations include Henkel’s November 2024 partnership with Celanese Corporation, producing water-based adhesives from captured CO2 emissions, enabling higher renewable content in packaging and consumer goods. Bostik introduced its Fast Glue Ultra+ in October 2024, a high-performance, 60% bio-based adhesive, while its Kizen™ LIME solution (September 2024) for end-of-line packaging contains 80% renewable ingredients. Sustainable transport solutions were also pursued by Newwen and Parrdekopper (October 2024) with RFID-enabled reusable boxes, and Graco Inc. (July 2024) launched a new brushless airless sprayer series improving adhesive application efficiency.

Trends and Opportunities Defining the Future of the Water-Based Adhesive Market

Regulatory-Driven Shift Away from Solvent-Based Systems in Key Industries

The water-based adhesive market is undergoing a profound transformation as regulators worldwide enforce stricter VOC (Volatile Organic Compound) reduction mandates. In the U.S., the EPA’s Clean Air Act sets clear limits on VOC emissions in coatings and adhesives, compelling manufacturers to reformulate solvent-heavy products into safer, water-based alternatives. Similarly, in China, national guidelines now require water-based coatings and adhesives in multiple end-use sectors, especially construction and packaging, to minimize emissions and improve urban air quality.

Beyond compliance, corporate sustainability commitments are accelerating adoption. Automotive OEMs, for instance, are adopting low-VOC water-based adhesives to align with both regulatory and internal sustainability benchmarks. Sika’s water-based adhesive portfolio enables automakers to meet these goals while simultaneously improving worker safety and reducing environmental impact. The shift also addresses workplace safety concerns, as solvent-based adhesives often contain hazardous, flammable chemicals. Water-based solutions eliminate these risks, reducing the need for costly ventilation and hazard-control systems. This makes them a preferred choice for industries prioritizing health, safety, and sustainability.

Development of High-Performance Bio-Based and Renewable Feedstocks

The market is expanding beyond simply being “water-based” into bio-based adhesives derived from renewable feedstocks. A 2025 industry analysis highlights the growing traction of adhesives formulated from starch, cellulose, and soy derivatives, reflecting consumer and corporate demand for renewable product lifecycles.

Agricultural and forestry byproducts are emerging as game changers. For instance, lignin-based adhesives derived from the paper industry offer high-performance structural bonding, while casein-based formulations are being increasingly used in food and beverage labeling applications. The emphasis is not only on renewable sourcing but also on achieving technical parity or superiority over petroleum-based adhesives. Automotive applications showcase this shift, with low-VOC, water-based pressure-sensitive adhesives (PSAs) now capable of withstanding high temperatures, chemical exposure, and mechanical stresses within car interiors, while still meeting the stringent VOC limits demanded by regulators and consumers alike.

Enabling the Circular Economy for Plastic Packaging

The circular economy transition in plastic packaging represents a major opportunity for water-based adhesive manufacturers. Traditional adhesives often hinder recycling by leaving residues on PET and HDPE bottles. Wash-off adhesives are now being engineered to address this challenge. For example, Tex Year’s alkaline-soluble wash-off adhesives allow labels to detach completely during the recycling process, ensuring clean PET flakes and high-quality rPET production.

This capability is critical for brand owners and recyclers, as label removal has been a significant bottleneck in achieving closed-loop packaging. Companies like Bostik are already commercializing water-based adhesives designed for packaging substrates with full recycling compatibility, while also reducing odor emissions and improving consumer safety. As global FMCG companies ramp up commitments to 100% recyclable packaging by 2030, recycling-friendly adhesives are becoming an indispensable enabler of sustainability-driven packaging innovation.

Penetration into High-Growth Electric Vehicle (EV) Battery Assembly

The EV battery segment is emerging as a high-value application space for water-based adhesives, driven by the dual needs of structural integrity and thermal management. Adhesives are increasingly replacing mechanical fasteners in battery cell bonding and module assembly, reducing overall pack weight and enabling more compact designs. Leading players such as Henkel and Sika are offering specialized adhesives engineered for EV battery packs, with properties that include high thermal conductivity for heat dissipation and strong structural bonding for crash safety.

Safety and flame retardancy are non-negotiable in EV applications. Adhesives such as Dow’s BETAFORCE™ and BETAMATE™ provide structural reinforcement while meeting stringent flame-retardant and off-gassing requirements, ensuring batteries remain safe under extreme conditions. These formulations also align with sustainability goals, offering room-temperature curing and reduced volatile emissions compared to conventional chemistries. With EV adoption projected to accelerate globally, the market opportunity for water-based, high-performance adhesives in battery systems is poised for significant growth.

Competitive Landscape: Leading Global Players Are Driving Innovation and Sustainability in Water-Based Adhesive Solutions

The water-based adhesives market is shaped by a set of key global players leveraging materials science expertise, manufacturing innovation, and sustainability initiatives to meet the evolving needs of industries worldwide.

Henkel AG & Co. KGaA: Pioneering Sustainable Adhesives with CO2-Based Innovations

Henkel is a global leader with its AQUENCE® brand delivering high-performance water-based adhesives for packaging, woodworking, and consumer goods. In November 2024, Henkel partnered with Celanese Corporation to produce adhesives from captured CO2 emissions, strengthening its sustainability profile. Henkel’s Purposeful Growth strategy focuses on R&D and innovation to support the circular economy while delivering superior value to customers globally.

H.B. Fuller Company: Expanding Innovation in Sprayable and High-Performance Adhesives

H.B. Fuller offers a wide range of water-based adhesives across packaging, tapes, labels, and engineering applications. The September 2024 acquisition of Sanglier Limited, a UK-based sprayable adhesives manufacturer, expanded its portfolio and innovation capabilities. The company is also developing Water-Based Superabsorbent Polymers (WBSAP) for hygiene products, emphasizing sustainable materials and high-performance solutions.

Bostik (Arkema Company): Driving Bio-Based Adhesive Innovation for Packaging Applications

Bostik provides advanced water-based adhesives under its Aquagrip™ brand, serving construction, industrial, and consumer markets. In October 2024, it launched Bostik Fast Glue Ultra+, formulated with 60% bio-based content, and in September 2024, the Kizen™ LIME range for recyclable packaging featured 80% renewable ingredients. Bostik focuses on sustainable innovation to enhance operational efficiency and product performance across regions.

Sika AG: Developing High-Performance Water-Based Systems for Construction and Automotive

Sika specializes in water-based adhesives and specialty chemicals for construction and automotive sectors. Its Strategy 2028 emphasizes innovation and sustainability, including Co-Elastic Technology (CET), which enables durable and flexible water-based sealants. Sika’s focus on advanced materials and performance solutions strengthens its global market presence.

3M Company: Integrating Smart Adhesive Technologies for Precision and Efficiency

3M offers a wide range of water-based adhesives under Fastbond™ and Scotch-Weld™ brands, with solutions for industrial, construction, and consumer applications. The company is investing in automated dispensing compatibility and exploring smart adhesive technologies that provide real-time performance data, improving operational efficiency and product reliability.

Water based Adhesive Market Share Insights, 2025-2034

Vinyl Acetate Adhesives Dominate Market Share by Product Type in the Water-Based Adhesive Industry

Vinyl acetate adhesives, particularly Polyvinyl Acetate (PVA) and Ethylene-Vinyl Acetate (EVA), hold the largest share at about 45%, underlining their versatility and cost-effectiveness across industries. These adhesives are widely used in woodworking, packaging, textiles, and paper converting, where their strong bond strength on porous substrates and ease of application deliver unmatched value. Their water-based, non-flammable nature makes them safe for large-scale industrial use, while their clarity and fast-setting capability make them highly adaptable for both structural and aesthetic applications. Regulatory pressures to eliminate solvent-based adhesives and the growing adoption of environmentally friendly bonding solutions have further strengthened vinyl acetate’s dominance, positioning it as the industry’s workhorse for sustainable adhesive systems.

Paper & Packaging Holds the Largest Market Share by Application in the Water-Based Adhesive Industry

Paper and packaging applications account for nearly 40% of the water-based adhesive market, making this the single largest and most influential end-use sector. From corrugated board manufacturing and case/carton sealing to bookbinding and paper bag production, water-based adhesives are integral to packaging efficiency and sustainability. The rise of e-commerce and the global shift toward recyclable, fiber-based packaging materials have reinforced this segment’s dominance, as water-based adhesives align perfectly with porous substrates while meeting environmental and regulatory compliance. Their compatibility with high-speed automated lines and their role in reducing VOC emissions ensure that paper and packaging remain the strongest demand driver, continually shaping product innovations and adhesive performance standards across the market.

United States: VOC Regulations, E-Commerce Packaging, and Bio-Based Adhesives

The United States water-based adhesive market is being shaped by the U.S. Environmental Protection Agency (EPA) and other regulatory bodies, which are tightening controls on volatile organic compounds (VOCs). This is accelerating the shift from solvent-based to water-based formulations across industries. The surge in e-commerce and sustainable packaging is further fueling demand, as brands prioritize non-toxic adhesives for carton sealing, labeling, and paper lamination to enhance environmental compliance.

Innovation is a defining factor in the U.S. market, with manufacturers developing formulations offering superior bond strength, faster curing times, and enhanced temperature resistance to match solvent-based alternatives. The construction sector is a key growth area, as water-based adhesives are being used in flooring, insulation, and wall applications due to their low emissions and safety benefits. Additionally, the adoption of bio-based adhesives using renewable plant polymers and the integration of smart applicator systems for precision and reduced waste highlight the market’s pivot toward sustainable, high-performance solutions.

European Union: PPWR Compliance, Horizon Europe Funding, and Automotive Growth

The European Union water-based adhesive market is expanding under strong regulatory and financial support for sustainability. The Packaging and Packaging Waste Regulation (PPWR), effective February 2025, and stricter Extended Producer Responsibility (EPR) policies across member states like Denmark are pushing packaging manufacturers to adopt recyclable and sustainable adhesives. Funding from Horizon Europe is boosting R&D into bio-based and compostable adhesive materials, positioning Europe as a leader in next-generation water-based technologies.

The European Water Resilience Strategy (June 2025) promotes water-efficient industrial processes, aligning perfectly with eco-friendly adhesives. Demand is also strong in the automotive sector, where water-based adhesives are increasingly used in lightweight materials and interiors to improve fuel efficiency and indoor air quality. Together, these drivers are making Europe a hub for innovation in both packaging and automotive adhesive applications.

China: 14th Five-Year Plan, Eco-Friendly Dominance, and Smart Adhesive Systems

The China water-based adhesive market is dominated by eco-friendly solutions, driven by the government’s 14th Five-Year Plan to reduce plastic pollution and promote remanufacturing and green technology adoption through tax incentives. Water-based adhesives are the largest adhesive category in China, favored for their low VOC emissions, cost-effectiveness, and compliance with environmental regulations.

Chinese manufacturers are ramping up R&D investments to produce advanced, durable adhesives tailored to the booming construction, infrastructure, and automotive markets. Another key trend is the rise of automated and intelligent adhesive application systems in large-scale factories, which improve efficiency, cut labor costs, and ensure uniform bonding in mass production. This reflects China’s strategy of merging sustainability with digital transformation in manufacturing.

India: EPR Regulations, Smart Cities Demand, and Domestic Manufacturing Growth

The India water-based adhesive market is being propelled by regulatory and industrial initiatives. The Plastic Waste Management (Amendment) Rules, 2024, effective April 1, 2025, emphasize Extended Producer Responsibility (EPR), compelling packaging and adhesive makers to adopt sustainable solutions. The “Make in India” and Smart Cities initiatives are fueling demand in construction, woodworking, and automotive sectors, where eco-friendly adhesives are being widely used.

Domestic companies such as Pidilite Industries are at the forefront of innovation, introducing stronger and faster-curing water-based adhesives. However, challenges remain with fluctuating raw material costs and the high R&D investments required. To address these, Indian companies are expanding R&D capabilities to develop adhesives tailored for local market needs while aligning with global environmental standards.

Japan: Plastic Resource Circulation Strategy and High-Performance Emulsions

The Japan water-based adhesive market is advancing under the Plastic Resource Circulation Strategy, which mandates all plastic packaging to be reusable or recyclable by 2025. This regulatory push is fostering the replacement of traditional adhesives with eco-friendly, solvent-free alternatives. Japanese manufacturers are at the forefront of emulsion-based adhesive technologies, creating products that are both safe and high-performing.

The market is focusing on multi-material bonding solutions for the automotive industry, where lightweight materials require adhesives that deliver both strength and durability. Advanced applications also include waterproof composite adhesives for construction that can be applied at room temperature. This demonstrates Japan’s strategy of combining sustainability with high-tech innovation to remain a global leader in specialty adhesive solutions.

Brazil: Cost-Effective Packaging Solutions and VOC Restrictions in Footwear

The Brazil water-based adhesive market is led by packaging and footwear industries, where these adhesives are valued for their low costs, ease of use, and compliance with environmental regulations. The National Solid Waste Policy (PNRS) provides the regulatory foundation, emphasizing reuse, recycling, and reduction of waste, which directly benefits water-based adhesive adoption.

A significant trend is the shift in footwear manufacturing toward water-based adhesives, driven by regulations limiting VOC emissions. This transition aligns with Brazil’s broader sustainability efforts and its focus on reducing occupational hazards in industrial processes. Combined with strong demand in flexible packaging applications, Brazil continues to prioritize water-based adhesive technologies as part of its eco-friendly industrial strategy.

Water based Adhesive Market Report Scope

Water based Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$49.3 Billion

|

|

Market Size (2034)

|

$86.9 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Resin Type (Acrylic Polymer Emulsion, PVA, VAE, SB Latex, PUD, Other Resins), By Product Type (Vinyl Acetate, Starch/Dextrin, Rubber Latex, Protein/Casein, Other Products), By Application (Tapes & Labels, Paper & Packaging, Building & Construction, Woodworking, Automotive & Transportation, Footwear & Leather, Other Applications), By End-Use Industry (Packaging & Paper, Building & Construction, Automotive & Transportation, Woodworking & Furniture, Consumer Goods, Other)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema S.A. (Bostik), 3M Company, Sika AG, The Dow Chemical Company, PPG Industries, Inc., Ashland Global Holdings Inc., Akzo Nobel N.V., Pidilite Industries Ltd., Hubei Huitian New Materials Co., Ltd., Lord Corporation (part of Parker Hannifin), DuPont de Nemours, Inc., DIC Corporation, Royal Adhesives & Sealants (part of H.B. Fuller)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water based Adhesive Market Segmentation

By Resin Type

- Acrylic Polymer Emulsion

- PVA

- VAE

- SB Latex

- PUD

- Other Resins

By Product Type

- Vinyl Acetate

- Starch/Dextrin

- Rubber Latex

- Protein/Casein

- Other Products

By Application

- Tapes & Labels

- Paper & Packaging

- Building & Construction

- Woodworking

- Automotive & Transportation

- Footwear & Leather

- Other Applications

By End-Use Industry

- Packaging & Paper

- Building & Construction

- Automotive & Transportation

- Woodworking & Furniture

- Consumer Goods

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water based Adhesive Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema S.A. (Bostik)

- 3M Company

- Sika AG

- The Dow Chemical Company

- PPG Industries, Inc.

- Ashland Global Holdings Inc.

- Akzo Nobel N.V.

- Pidilite Industries Ltd.

- Hubei Huitian New Materials Co., Ltd.

- Lord Corporation (part of Parker Hannifin)

- DuPont de Nemours, Inc.

- DIC Corporation

- Royal Adhesives & Sealants (part of H.B. Fuller)

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver precise insights into the global water-based adhesive market. Our approach integrates primary research with industry stakeholders, including adhesive manufacturers, packaging and construction companies, and automotive OEMs, alongside secondary sources such as regulatory publications, company reports, trade journals, and market databases. The study examines market dynamics including VOC regulations, sustainable adhesive innovations, renewable feedstock development, EV battery applications, and circular economy solutions for recyclable packaging. Regional market trends across North America, Europe, China, India, Japan, and Brazil are analyzed, accounting for government initiatives, industry investments, and strategic partnerships. USDAnalytics also evaluates segmentation by resin type, product type, application, and end-use industry, enabling actionable insights for R&D planning, product development, operational efficiency, and sustainability compliance. By emphasizing technological innovation, bio-based formulations, and regulatory alignment, our methodology provides decision-makers with a clear understanding of growth opportunities, competitive positioning, and future market directions in the evolving water-based adhesive sector.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.