Plastic Container Market Size, Overview, and Growth Outlook (2025–2034)

Global Plastic Container Market to Reach $126 Billion by 2034 Driven by Food, Beverage, and Sustainability Trends

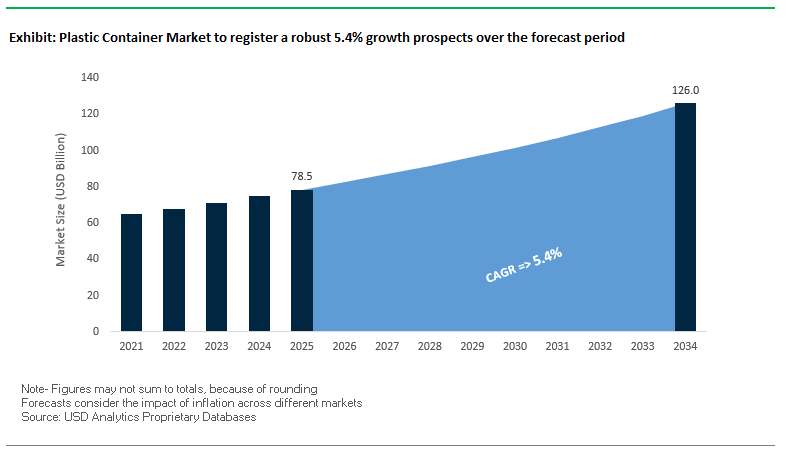

The global plastic container market is projected to grow from $78.5 billion in 2025 to $126 billion by 2034, registering a CAGR of 5.4%. Growth is largely fueled by demand from the food and beverage sector, the continued dominance of PET and HDPE materials, and the industry-wide adoption of lightweighting and recycled content. Manufacturers are increasingly focusing on durable, cost-effective, and environmentally friendly designs to meet consumer and regulatory demands.

Key Insights for industry professionals and buyers:

- Food and Beverage Segment Leads Demand: High consumption of bottled water, soft drinks, dairy, sauces, and ready-to-eat products drives container requirements.

- PET and HDPE Dominate Material Usage: PET for beverage clarity and strength; HDPE for household, personal care, and industrial applications.

- Lightweighting Reduces Costs and Carbon Footprint: Thin-wall designs and optimized container shapes lower material use and transportation costs.

- Recycled Content Adoption is Rising: Incorporation of post-consumer recycled (PCR) plastics aligns with sustainability goals and consumer preference for eco-friendly packaging.

- Sustainability Drives Innovation: Nanocoatings, bio-based plastics, and smart reusable packaging are emerging as competitive differentiators.

Market Analysis: Plastic Container Industry Witnesses Strategic Expansion, Sustainable Innovation, and Mergers Driving Global Growth

The plastic container market is experiencing significant developments driven by sustainability, M&A activity, and material innovation. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, enabling better service to pharmaceutical and medical device markets. That same month, Inteplast Group acquired Germany’s Con-pearl, enhancing its product portfolio and market reach. By July 2025, WestRock and Smurfit Kappa debuted as Smurfit WestRock, creating a global leader in paper-based packaging and exerting competitive pressure on plastic container suppliers.

Sustainability innovations are shaping material usage and design strategies. In June 2025, Graphic Packaging International launched its PaperSeal® Pressed MAP Tray, reducing plastic use by up to 85% in modified atmosphere packaging applications. April 2025 saw Amcor collaborate with Nfinite Nanotechnology to validate nanocoatings for recyclable and compostable containers, enhancing oxygen barrier performance critical for food and beverage packaging.

Reusability and plant-based alternatives are also gaining traction. January 2025 marked the launch of ReInPack’s AI-powered smart packaging service for reusable containers, streamlining delivery and collection of empty packages. Earlier, in November 2024, Amcor introduced a line of fully recyclable containers made from PCR materials, while Berry Global in September 2024 launched containers with 30% plant-based content, reflecting ongoing commitments to circular economy principles and carbon footprint reduction.

Emerging Trends and Opportunities Transforming the Plastic Container Market

Strategic Shift to Integrated Recycling and rPET Procurement

The plastic container market is increasingly shaped by direct corporate investments into recycling infrastructure and integrated supply chains for food-grade recycled PET (rPET). Beverage leaders are moving upstream to secure reliable feedstock amid tightening regulations and escalating demand for rPET. Coca-Cola HBC, for example, launched its first company-owned collection hub in Nigeria in January 2025, with capacity to process 13,000 metric tonnes of PET bottles annually. This investment directly supports its target of achieving 35% recycled PET in bottles by 2025, underscoring how infrastructure ownership ensures consistent access to quality recycled resin. Similarly, Nestlé has committed $30 million to the Closed Loop Leadership Fund, a private equity vehicle focused on modernizing U.S. recycling systems. By strengthening local recycling infrastructure, Nestlé not only helps close systemic collection gaps but also guarantees a stable supply of high-quality food-grade rPET for its global packaging operations. Collectively, these strategic initiatives demonstrate how leading CPG companies are no longer treating recycling as a compliance obligation but as a core supply chain strategy for ensuring material security and cost competitiveness.

Lightweighting and Right-Sizing Driven by EPR Cost Pressures

Extended Producer Responsibility (EPR) laws are fundamentally reshaping container design by tying compliance costs to packaging volume and material usage. Under these frameworks, producers pay fees based on the weight of packaging introduced into the market, creating direct financial incentives for lightweighting and right-sizing. A report from the Association of Plastic Recyclers (APR) highlights that fees are charged per pound, making weight reduction an immediate and quantifiable cost-saving strategy. Procter & Gamble (P&G) is aggressively pursuing this approach to meet its commitment to reduce virgin petroleum-based resin usage by 50% per production unit by 2030. By lightweighting bottles and other plastic containers, P&G not only cuts material consumption but also lowers greenhouse gas emissions from logistics, since lighter loads reduce fuel usage in transport. Policy frameworks are accelerating this shift: as of 2025, 19 U.S. states have bans on certain single-use plastics, while California’s plastic reduction program rewards companies for using recycled content alongside lightweighting initiatives. This dual pressure—regulatory and economic—is making lightweighting a cornerstone strategy for global packaging sustainability.

Advanced Recycling Technology for Food-Grade rPET

A critical opportunity for the plastic container market lies in scaling advanced chemical recycling technologies to secure food-grade rPET supply. Mechanical recycling, while cost-efficient, is limited by contamination and material degradation, leaving a performance gap for high-purity applications like beverage and food containers. Depolymerization offers a breakthrough solution by breaking PET down into its base monomers, enabling virgin-quality resin production. Koch Technology Solutions and Ioniqa Technologies have already commercialized such a process, converting low-quality post-consumer PET into high-purity feedstock while cutting carbon emissions by

50% compared to virgin resin production. Industry momentum is accelerating, with Plastics Europe projecting chemical recycling investments to grow from €2.6 billion in 2025 to €8 billion in 2030. These investments are not only vital for scaling food-grade rPET but also for diversifying supply streams away from mechanical recycling constraints, ensuring that even low-quality or colored plastics can be reprocessed into safe, high-value applications.

Integration of Digital Watermarks for Intelligent Sorting

The adoption of digital watermarking presents another transformative opportunity to maximize recycling efficiency and increase the value of recovered plastics. The cross-industry HolyGrail 2.0 initiative has validated this technology through industrial-scale trials in Germany, where invisible watermarks embedded in packaging were detected at high speeds by sorting cameras. The trials demonstrated purity rates above 93% for distinguishing attributes such as food-grade versus non-food-grade packaging—levels of precision that conventional sorting technologies cannot achieve. For plastic container producers, this precision translates into higher-quality recycled streams suitable for closed-loop applications. Beyond compliance, the ability to generate ultra-pure material streams directly enhances the economic value of recycled plastics, making recycling a more profitable and scalable model. By enabling seamless differentiation of packaging at end-of-life, digital watermarking strengthens circularity, supports compliance with EU mandates for higher recycling targets, and positions plastic containers as a viable contributor to a fully circular economy.

Competitive Landscape: Leading Companies Are Driving Innovation, Sustainability, and Market Expansion in Plastic Containers

The plastic container market is dominated by companies investing in lightweighting, recycled materials, and functional designs, catering to diverse industries such as food, beverage, personal care, healthcare, and industrial applications.

Amcor plc: Expanding Global Reach and Advancing Sustainable Packaging Solutions

Amcor offers a wide portfolio of rigid containers, bottles, jars, and tubs for beverages, food, personal care, and pharmaceuticals. Its strategy emphasizes sustainability and innovation, aiming for all packaging to be recyclable or reusable by 2025. In August 2025, Amcor expanded its healthcare packaging network in Costa Rica, strengthening its service to growing pharmaceutical and medical device markets. The company combines advanced material science with lightweight, recyclable designs to appeal to environmentally conscious consumers.

Berry Global Group, Inc.: Pioneering Plant-Based Containers and High-Performance Packaging Films

Berry Global manufactures rigid containers, closures, and flexible films for food, beverage, personal care, and industrial applications. Its strategy focuses on sustainable solutions using recycled content, aiming for 100% of packaging to be reusable, recyclable, or compostable by 2025. In September 2024, Berry introduced plastic containers made from 30% plant-based materials, advancing the company’s sustainability initiatives and reducing its carbon footprint.

Silgan Holdings Inc.: Delivering Custom, High-Quality Containers Across Multiple End Markets

Silgan’s custom container segment provides engineered plastic containers for food, beverage, personal care, and pharmaceuticals. The company is recognized for quality, technological support, and design-focused solutions, with a strong presence across North America. Its 2024 custom container sales of $650 million underscore market strength, while initiatives using PCR and bio-resins highlight a commitment to sustainable packaging.

Sonoco Products Company: Diversifying Packaging Solutions Through Recycled and Renewable Materials

Sonoco offers rigid plastic containers for consumer and industrial applications, including high-barrier food containers and cartridges for adhesives. Its strategic focus on sustainable solutions includes products made with recycled and renewable materials. Recent acquisitions in the plastic cartridge segment have expanded its portfolio and reinforced market presence, while paper-based containers enhance shelf appeal for on-the-go food products.

Pactiv Evergreen Inc.: Integrating Sustainability and Convenience Across Food Packaging Solutions

Pactiv Evergreen provides hinged-lid containers, trays, and cups for foodservice and fresh food packaging. The company announced a combination with Novolex, creating a leading platform in food, beverage, and specialty packaging. Its strategic goal is for 100% of net revenues by 2030 to come from recycled, recyclable, or renewable materials. Notable offerings include EarthChoice hinged-lid containers with 25% post-consumer recycled content and tamper-evident features.

Plastic Container Market Share Insights, 2025-2034

Bottles and Jars Dominate Market Share by Container Type in the Plastic Container Industry

Bottles and jars command the largest share at 48% of the plastic container industry, underscoring their role as the universal workhorse across beverages, sauces, condiments, spreads, and personal care. Their dominance is driven by global bottled water consumption, the surge in on-the-go beverages, and the versatility of PET and HDPE in meeting both cost-efficiency and performance requirements. Innovation in this segment focuses on lightweighting, neck redesign, and recycled resin integration (rPET, rPP) to meet stringent sustainability goals while maintaining product protection and clarity. Tubs, cups, and bowls follow as the second-largest category at 22%, anchored in foodservice and dairy applications where single-serve and ready-to-eat convenience packaging are in high demand. Clamshells remain essential for fresh produce and bakery packaging, though they face regulatory and consumer backlash, pushing converters towards compostable and high-recycled content options. HDPE jugs continue as the bulk liquid specialist for dairy and household chemicals, while pails serve industrial and construction supply chains where durability and chemical resistance are non-negotiable. This segmentation highlights how bottles and jars dominate on volume and consumer reach, while industrial pails and tubs secure value through application-specific performance and resilience.

Food and Beverages Hold the Largest Market Share by End-Use Industry in Plastic Containers

The food and beverages sector leads with 55% of end-use demand, reflecting the sheer scale of bottled water, carbonated drinks, sauces, spreads, dairy, and fresh produce packaging. It is also the epicenter of sustainability regulation, as FMCG brands face pressure to meet recycled content mandates and shift towards recyclable mono-material designs without compromising safety or shelf appeal. Household care follows as a stable, high-volume segment, where HDPE bottles and jugs dominate for detergents, disinfectants, and cleaning sprays, supported by innovation in dispensing systems and concentrate formats that reduce overall plastic use. Cosmetics and personal care represent a premium-value market, where containers must balance advanced aesthetics, consumer convenience, and recyclability, driving innovation in tactile finishes and post-consumer resin (PCR) clarity solutions. Pharmaceuticals and healthcare form a compliance-driven niche, requiring USP- and FDA-approved containers to guarantee sterility and safety for medicines, vials, and devices. Industrial demand is sustained by durable pails, drums, and jugs, where performance against chemicals, UV exposure, and mechanical stress outweighs appearance. This segmentation underscores how food and beverages define scale and regulatory scrutiny, while pharmaceuticals and cosmetics lead innovation in barrier properties, compliance, and sustainability integration.

United States Plastic Container Market Driven by FDA Standards and State-Level Plastic Bans

The United States plastic container market is strongly regulated by the Food and Drug Administration (FDA), which enforces stringent standards for food-contact materials to prevent contamination and ensure consumer safety. Alongside federal oversight, state-level bans and mandates are shaping the industry. For example, California’s SB 54 requires a 25% reduction in virgin plastic packaging by 2032, with producers mandated to join a Producer Responsibility Organization (PRO) by 2025. These laws are creating long-term demand for post-consumer recycled (PCR) plastic containers.

Innovation is also reshaping the U.S. market. Companies are developing PCR-based food and beverage containers, with firms like Tekni-Plex introducing an updated foam polystyrene egg carton containing 25% PCR material. The rise of e-commerce continues to drive demand for robust containers that withstand shipping, highlighted by Amazon’s switch to paper-based alternatives, which eliminated 15 billion plastic air pillows. In parallel, manufacturers are adopting smart packaging technologies such as QR codes and NFC tags, offering consumers greater transparency about sourcing and recycling. On the manufacturing side, the plastics industry has accelerated automation, adding over 1,600 robotics units in 2023, streamlining throughput and boosting quality yields.

European Union Plastic Container Market Shaped by PPWR and Tethered Cap Mandates

The European Union plastic container market is undergoing significant transformation under stringent sustainability laws. From July 2024, the Single-Use Plastics Directive requires tethered caps on all beverage containers up to three liters, ensuring caps are recycled together with bottles. The implementation of the Packaging and Packaging Waste Regulation (PPWR) in February 2025 further pushes manufacturers to redesign plastic containers for recyclability, reusability, and PFAS-free compliance. From August 2026, food packaging containing PFAS above specified thresholds will be banned, impacting container material choices.

By 2028, all plastic packaging must carry a harmonized recycling label, driving demand for clearer and standardized consumer communication. Companies are focusing heavily on design-for-recycling solutions, with PPWR requiring that containers with recyclability grades below 70% will no longer qualify as recyclable by 2030. While many producers are investing in mono-material and circular packaging solutions, groups such as the Alliance for Sustainable Packaging are lobbying for a pause in the regulation, citing potential environmental trade-offs of exclusive reusable systems. The EU remains a global leader in sustainable packaging innovation, with its regulations setting the pace for other regions.

China Plastic Container Market Strengthened by Domestic Recycling Infrastructure

The China plastic container market is adapting to strong government interventions designed to combat plastic waste and promote circular economy models. A new packaging regulation effective June 2025 emphasizes recycled materials and reusable systems, particularly in the e-commerce sector, which generates vast amounts of delivery waste. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are jointly spearheading efforts to reduce plastic pollution.

China’s ban on plastic waste imports since 2018 has accelerated domestic recycling infrastructure, creating opportunities for food-grade rPET containers. The positive list system for food-contact materials and new adhesive standards introduced in February 2025 are shaping the production of compliant plastic packaging. Local innovation is also on the rise: Coca-Cola launched 500 ml bottles made from 100% rPET in Hong Kong using raw materials from its facilities in mainland China. Companies like Jingxing Packaging Materials Co. are adopting closed-loop systems by recycling leftover scraps into new packaging. These trends underscore China’s commitment to scaling sustainable, compliant, and high-volume container manufacturing.

India Plastic Container Market Driven by EPR and Large-Scale PET Recycling Investments

The India plastic container market is guided by strict frameworks under the Plastic Waste Management Rules (2016, amended 2022), which mandate Extended Producer Responsibility (EPR) for plastic waste collection, recycling, and disposal. The Swachh Bharat Abhiyan (Clean India Mission) complements these regulations, encouraging segregated waste collection and recycling adoption at the community level.

The Food Safety and Standards Authority of India (FSSAI) is currently consulting on guidelines for sustainable packaging in the food sector, promoting biodegradable and recyclable plastic containers. To support innovation, India has launched Centres of Excellence (CoEs) for advancing petrochemical technologies and R&D in sustainable packaging. On the investment front, Varun Beverages and Indorama Ventures are building a large-scale PET recycling plant to meet rising demand for food-grade rPET containers. This complements local startup activity, with firms like Dharaksha Ecosolutions developing packaging from agricultural waste. India’s unique position as both a high-volume plastics producer and global exporter is accelerating demand for eco-friendly and tamper-resistant containers.

Brazil Plastic Container Market Accelerated by Investments and E-commerce Growth

The Brazil plastic container market is expanding rapidly, supported by large-scale investments and booming e-commerce. According to industry body Abiplast, Brazil’s plastics sector expects R$10.5 billion ($1.8 billion) in annual investments in factory expansions, sustainable packaging solutions, and new recycling technologies. The National Solid Waste Policy is targeting a 27% recycling rate for plastic packaging by 2024, which is spurring container manufacturers to adopt new eco-friendly designs and technologies.

Brazil’s e-commerce sector grew by 26.9% in 2022, creating significant demand for durable and protective plastic containers suited for logistics and last-mile delivery. International players are also investing: Berry Global Group launched a rectangular PCR-based container in January 2024, offering up to 100% recycled content. Meanwhile, Braskem’s development of an ethane import terminal is ensuring a stable supply of feedstock for container production, signaling stronger supply chain resilience and growth potential in Brazil’s packaging ecosystem.

Canada Plastic Container Market Transitioning to Zero Plastic Waste by 2030

The Canada plastic container market is being reshaped by the Single-use Plastics Prohibition Regulations (SUPPR), which ban the manufacture, import, and sale of items such as checkout bags and single-use food service ware. This forms part of Canada’s zero plastic waste by 2030 strategy, requiring container producers to shift towards compostable, recyclable, and non-conventional materials.

Government incentives are encouraging innovation in recycling. The federal and Quebec governments provided $2.9 million to Exxel Polymers in 2024 for equipment that will boost production of 100% recycled plastics. Consumer preferences are also accelerating the adoption of rPET bottles and containers, particularly in beverage and food packaging. The SUP ban is expected to eliminate 1.3 million tonnes of hard-to-recycle plastic waste, positioning Canada as a leader in the adoption of bio-based plastics such as PLA. This regulatory and investment environment is fostering growth in the Canadian plastic container market, emphasizing sustainability and compliance.

Plastic Container Market Report Scope

Plastic Container Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$78.5 Billion

|

|

Market Size (2034)

|

$126 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (PET, HDPE, LDPE, PP, PVC, PS, Recycled Content Plastics, Bio-based Plastics), By Container Type (Bottles & Jars, Jugs, Pails, Tubs/Cups/Bowls, Clamshells), By End-Use Industry (Food & Beverages, Cosmetics & Personal Care, Household Care, Pharmaceuticals & Healthcare, Industrial), By Manufacturing Process (Extrusion Blow Molding, Injection Blow Molding, Injection Molding, Thermoforming)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global, Inc., Novolex Holdings, LLC, Sonoco Products Company, Silgan Holdings Inc., Tekni-Plex, Inc., Alpla-Werke Alwin Lehner GmbH & Co KG, Graham Packaging Company, Plastic Omnium, Comar, Bormioli Pharma S.p.A., Plastipak Holdings, Inc., Greif, Inc., RPC Group (Berry Global, Inc.), Evergreen Packaging (Pactiv Evergreen Inc.)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Plastic Container Market Segmentation

By Material

- PET

- HDPE

- LDPE

- PP

- PVC

- PS

- Recycled Content Plastics

- Bio-based Plastics

By Container Type

- Bottles & Jars

- Jugs

- Pails

- Tubs/Cups/Bowls

- Clamshells

By End-Use Industry

- Food & Beverages

- Cosmetics & Personal Care

- Household Care

- Pharmaceuticals & Healthcare

- Industrial

By Manufacturing Process

- Extrusion Blow Molding

- Injection Blow Molding

- Injection Molding

- Thermoforming

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Plastic Container Market

- Amcor plc

- Berry Global, Inc.

- Novolex Holdings, LLC

- Sonoco Products Company

- Silgan Holdings Inc.

- Tekni-Plex, Inc.

- Alpla-Werke Alwin Lehner GmbH & Co KG

- Graham Packaging Company

- Plastic Omnium

- Comar

- Bormioli Pharma S.p.A.

- Plastipak Holdings, Inc.

- Greif, Inc.

- RPC Group (Berry Global, Inc.)

- Evergreen Packaging (Pactiv Evergreen Inc.)

* List Not Exhaustive

Methodology

The research methodology for the Plastic Container Market integrates both primary and secondary approaches to deliver accurate, actionable insights for industry professionals. Primary research involved structured interviews with packaging engineers, sustainability experts, CPG executives, and supply chain stakeholders across key regions to capture real-world perspectives on material adoption, recycling initiatives, and innovative container designs. Secondary research comprised analysis of company annual reports, regulatory filings, patents, sustainability disclosures, verified industry journals, and trade publications. USDAnalytics applied advanced data triangulation to validate market sizing, CAGR, and segment-level forecasts, incorporating material trends (PET, HDPE, LDPE, PP, bio-based and recycled plastics), container types (bottles, jars, tubs, pails, clamshells), manufacturing processes (injection blow molding, extrusion, thermoforming), and regulatory frameworks including EPR, SUPD, PPWR, and FDA standards. Top-down and bottom-up forecasting approaches were employed to ensure consistency across regional and global projections, while market dynamics were contextualized against sustainability trends, corporate recycling investments, and digital innovations like smart packaging and watermarking. This comprehensive methodology ensures USDAnalytics provides fact-based, forward-looking insights that reflect the evolving demands, regulatory pressures, and technological advancements shaping the global plastic container market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.