Print Label Market Overview: Sustainability, Digital Transformation, and Material Innovation

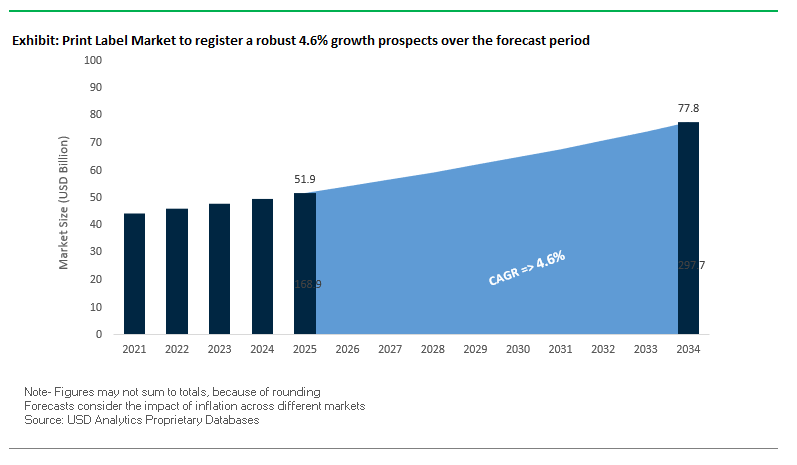

The Global Print Label Market is projected to reach $51.9 billion in 2025 and expand to $77.8 billion by 2034, growing at a CAGR of 4.6%. Labels are no longer just identifiers but strategic tools for branding, supply chain visibility, and regulatory compliance. Pressure-sensitive labels continue to dominate the industry, valued for their ease of application, flexibility, and ability to integrate RFID and NFC technologies.

The industry is in the midst of a digital transformation, with flexographic printing retaining its dominance in large-volume runs while digital printing rapidly gains share in short runs and customized applications. Sustainability remains a defining factor, as brands demand eco-friendly materials, linerless labels, and recycled-content substrates. This convergence of sustainability, digitalization, and intelligent labeling systems is reshaping the competitive landscape.

Key Insights for Industry Professionals

- Pressure-sensitive labels dominate, widely adopted across food, beverage, pharma, and logistics.

- Flexographic printing holds scale advantage, making it ideal for long-run, high-volume jobs.

- Sustainability drives innovation, with linerless and recycled-content labels gaining traction.

- Digital label printing grows rapidly, enabling personalization, localized campaigns, and shorter lead times.

Market Analysis: Recent Developments Driving Growth and Innovation

The print label market is experiencing a blend of strategic investments, acquisitions, and innovation-focused launches that are shaping its trajectory. In August 2025, Mondi introduced a new paper-based packaging solution under its Ad/Vantage Smooth Brown Semi Extensible line, strengthening its reputation in sustainable material innovation. A month earlier, in July 2025, Labelexpo Europe announced its upcoming “Festival of Innovation” in Barcelona, set to spotlight breakthrough technologies across printing and labeling.

The market is also seeing significant capital investments. In June 2025, R.R. Donnelley allocated $25 million to expand its Georgia facility, adding new digital presses and robotic automation, effectively doubling its workforce capacity. Similarly, in May 2025, Ahlstrom completed the acquisition of Stevens Point operations and invested in a new parchmentizer at its Saint-Séverin plant, strengthening its specialty label paper capabilities.

Financial and structural performance updates have further highlighted industry resilience. In April 2025, 3M reported an operating margin above 20%, reflecting its strength across diversified label solutions. Meanwhile, Constantia Flexibles has been particularly active: in March 2025, it partnered with Aluflexpack AG to expand its premium flexible packaging footprint, and in January 2025, it received two WorldStar Global Packaging Awards for EcoPeelCover and EcoLamHighPlus. These innovations point to a rising demand for recyclable and high-barrier label materials.

Industry consolidation also continues to reshape competition. In January 2025, International Paper completed its $7.2 billion acquisition of DS Smith, reinforcing its leadership in sustainable fiber-based packaging, with implications for the print label sector. However, macroeconomic challenges remain an October 2024 report revealed a historic decline in Europe’s label industry output in 2023, underscoring the volatility in raw material costs and demand cycles.

Print Label Market: Transformative Trends and Emerging Opportunities

Accelerated Adoption of Digital Print for On-Demand and Short Runs

The print label market is experiencing a rapid transition from traditional analog processes such as flexographic and offset printing toward digital printing technologies, which are becoming the cornerstone of modern label production. This shift is being driven by brand demand for agility, shorter lead times, and cost-effective customization. Digital printing eliminates the need for expensive plates and lengthy setup procedures, making it economically viable for small and medium print runs. This flexibility enables companies to launch new product lines, prototypes, or targeted marketing campaigns quickly and without significant financial risk. Beyond prototyping, digital printing also supports leaner inventory management by enabling just-in-time production, significantly reducing the risk of label obsolescence and associated waste. Moreover, variable data printing (VDP) capabilities allow every label in a run to carry unique text, designs, or serialized data. This is particularly valuable for personalization strategies, loyalty programs, and compliance labeling, where dynamic information is critical. Together, these advantages are redefining how brands manage product launches and consumer engagement, positioning digital print as an indispensable tool for growth in the label industry.

Integration of Smart and Connected Technologies for Traceability

Labels are evolving into intelligent platforms that connect consumers, retailers, and manufacturers in ways that go far beyond static branding. The integration of QR codes, NFC chips, and digital watermarks is transforming labels into interactive gateways that provide transparency, authentication, and engagement. Mass adoption of QR codes under initiatives like SmartLabel has allowed major CPG brands to communicate detailed sourcing, nutritional, and recycling information directly to consumers, enhancing trust and compliance with transparency regulations. In higher-value segments such as luxury goods, spirits, and pharmaceuticals, NFC-enabled labels are being deployed to combat counterfeiting, providing each product with a secure digital identity that can be verified with a smartphone. These connected labels are also strengthening supply chain integrity by enabling end-to-end traceability, allowing companies to track products from manufacturing through to final purchase. This dual role of enhancing consumer engagement and improving operational oversight underscores the strategic importance of smart label integration, making it a central trend in the industry’s digital transformation.

Development of Sustainable Label Substrates and Adhesives

A critical opportunity in the print label market lies in developing substrates and adhesives that align with global recycling and sustainability goals. Labels and adhesives often act as contaminants in recycling streams, especially for PET bottles, where residue can compromise the quality of recyclates. In response, innovators are designing wash-off adhesives that detach easily during the recycling process, enabling cleaner PET recovery and directly supporting the circular economy. At the same time, label producers are launching materials that contain post-consumer recycled content, such as Ahlstrom’s pressure-sensitive liners that incorporate 15% recycled fibers. These innovations reduce the overall carbon footprint while responding to brand owners’ demands for packaging compatibility across PET, glass, and aluminum recycling systems. The shift toward recyclable, compostable, and recycled-content labels reflects not only regulatory and consumer pressure but also a strategic growth avenue, as sustainability becomes a decisive purchasing factor for global brands.

Advanced NFC/RAIN RFID Integration for Premium Product Authentication

Beyond the ubiquity of QR codes, the print label market is seeing significant opportunity in advanced NFC and RAIN RFID technologies. These solutions provide robust anti-counterfeiting measures, enhanced consumer experiences, and powerful logistics tools, particularly for high-value industries. Luxury fashion brands have pioneered this approach, embedding NFC chips into premium goods to give customers instant authentication capabilities. In the spirits market, NFC-enabled labels can deliver immersive brand storytelling, such as virtual distillery tours or curated cocktail recipes, which elevate consumer engagement and build loyalty. From a supply chain perspective, RAIN RFID offers unprecedented efficiency by enabling real-time inventory management handheld readers can scan hundreds of items in seconds, reducing errors and optimizing logistics. These capabilities not only safeguard brand reputation against counterfeit risks but also deliver operational advantages that improve profitability. As regulatory scrutiny and consumer expectations for authenticity rise, the integration of NFC and RFID technologies is positioned to become a defining feature of premium and high-value product labeling.

Competitive Landscape: Leaders Driving Growth in the Print Label Industry

The global print label industry is marked by a mix of established multinationals and specialized innovators, all focusing on sustainability, printing efficiency, and intelligent labeling technologies. Below are the key companies shaping the market.

Avery Dennison Corporation: Expanding Intelligent and Sustainable Labels

Avery Dennison is a global leader in pressure-sensitive labels, intelligent labels, and merchandise tagging solutions. Its print label portfolio spans food, beverage, logistics, and healthcare applications. In mid-2025, the company extended its partnership with the Premier League for five years, reinforcing its expertise in high-performance label branding. Its strategic focus includes sustainability and digital adoption, exemplified by its white paper on circular packaging. With its leadership in RFID-enabled intelligent labels, Avery Dennison stands out as a pioneer in supply chain transparency and brand protection.

CCL Industries Inc.: Expanding Scale Through Acquisitions

CCL Industries specializes in specialty label solutions, shrink sleeves, and in-mould labels. In 2024, the company posted record revenues of $7.2 billion, fueled by nine acquisitions, highlighting its aggressive expansion strategy. Its focus spans personal care, food & beverage, and healthcare packaging, while investments in modern facilities, including a wine label plant in California and a sleeve plant in Russia, reinforce its global footprint. Its vertically integrated model, from materials science to printing, gives it strong control over innovation and supply consistency.

UPM Raflatac: Leading Beyond Fossil-Based Label Materials

UPM Raflatac is a sustainability-driven provider of self-adhesive label materials for food, beverage, and personal care applications. In early 2025, it launched the Carbon Action Plastic Labels portfolio, designed to cut carbon emissions across packaging lifecycles. With its bold goal of becoming the “world’s first label materials company beyond fossils,” UPM is targeting traceability across its supply chain by 2030 while committing to a 65% GHG reduction from 2015 levels. Its Label Life service provides lifecycle assessments to help brands choose more sustainable label solutions.

3M Company: Innovation Powerhouse in Durable Labels

3M brings its expertise in adhesives, films, and durable labeling materials to the print label market, catering to industries like automotive, electronics, and healthcare. In April 2025, it reported a 20.9% operating margin, reflecting strong profitability amid industry headwinds. With over 60,000 products and 3,000 patents filed annually, 3M leverages deep R&D to remain at the forefront of innovation. Its strength lies in material science leadership, making it a critical supplier for high-performance and industrial labeling solutions.

Mondi Group: Innovating with Fiber-Based Label Materials

Mondi Group is a leader in sustainable packaging and paper, with a growing footprint in the print label segment. Its innovations include the FunctionalBarrier Paper Ultimate, a recyclable, ultra-high-barrier paper solution that replaces traditional plastics and aluminum in premium labels. In August 2025, Mondi announced a biomass power plant in Slovakia to increase energy self-sufficiency to 90%, further aligning its production with sustainability. With strong expertise in paper-based and hybrid label solutions, Mondi positions itself as a key enabler of the transition to fiber-based labeling systems.

Print Label Market Share Insights

Pressure-Sensitive Labels Hold the Largest Market Share by Label Type in Print Labels

Pressure-sensitive labels (PSLs) dominate the global print label market with a 55% share, driven by their unmatched versatility, compatibility with diverse substrates, and efficiency on automated high-speed labeling lines. Their leadership is reinforced by continuous innovation from premium finishes such as foils and tactile coatings that elevate shelf appeal to RFID-embedded smart labels that enhance supply chain visibility. Unlike legacy wet-glue formats, PSLs deliver faster application, minimal waste, and adaptability across sectors from beverages to industrial goods. As sustainability becomes non-negotiable, advancements in recyclable face stocks, thinner liners, and linerless PSL systems are securing their relevance. This makes pressure-sensitive labels the most resilient and future-proof segment within the global label landscape.

Food & Beverages Dominate Market Share by End-Use Industry in Print Labels

Food and beverages account for 35% of print label demand, reflecting their indispensable role in compliance, branding, and consumer engagement. Beyond serving as vehicles for nutritional information, origin labeling, and regulatory traceability, F&B labels are evolving into interactive marketing tools through QR codes, NFC tags, and augmented reality campaigns. The segment’s scale is reinforced by the global packaged food boom and rising e-commerce penetration, which require both primary labels for retail appeal and secondary logistics labels for last-mile delivery. In addition, the push for sustainable packaging is accelerating demand for recyclable substrates and compostable adhesives in F&B applications. As one of the most innovation-intensive segments, food and beverages continue to anchor print label growth while shaping the industry’s material and technology roadmap.

United States: Sustainability and Digital Printing Drive Innovation in the Print Label Market

The U.S. print label industry is experiencing significant transformation, driven by rising consumer and corporate demand for sustainable packaging solutions. This has created strong market traction for recyclable, compostable, and paper-based labels across food, beverage, and personal care sectors. Technological advancements, particularly digital printing technology, are enabling shorter production runs, rapid design changes, and product personalization, which are essential for seasonal promotions and limited-edition product launches.

The focus on sustainability is further reinforced by initiatives like How2Recycle Plus, which includes QR codes for consumers to verify recyclability locally. Corporate commitments to material reduction and recyclable label designs are driving demand, especially in sectors such as pharmaceuticals, where compliance with the Drug Supply Chain Security Act (DSCSA) and advanced track-and-trace labeling systems is critical. The integration of barcodes and RFID tags ensures product safety and regulatory compliance, making U.S. print labels both eco-friendly and technologically advanced.

Germany: Circular Economy and Regulatory Compliance Strengthen Eco-Friendly Labeling

Germany’s print label market is strongly influenced by a stringent regulatory environment, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates eco-friendly and fully recyclable packaging. The country’s leadership in the circular economy ensures that labels are designed for recyclability, with high recycled content, meeting both national and EU sustainability targets.

Technological innovation is a key trend, with the adoption of mono-material films such as polyethylene (PE) and polypropylene (PP) to enhance label recyclability and circularity. Governmental mandates under the PPWR, combined with growing consumer awareness, have significantly accelerated demand for sustainable labeling solutions, positioning Germany as a hub for eco-conscious, technologically advanced print labels.

China: Policy Support and E-Commerce Expansion Drive Print Label Adoption

China’s print label industry is being shaped by the government’s dual carbon goals, which aim to achieve carbon peak and carbon neutrality, fostering a transition toward eco-friendly and reusable label materials. Manufacturers are embracing automation, AI, and “5G plus industrial internet” integration to enhance production efficiency, optimize processes, and improve flexible manufacturing capabilities.

Sustainability-focused policies, such as restrictions on non-degradable plastics by 2025, have increased demand for paper-based and recyclable labels. Rapid growth in e-commerce platforms has further driven the adoption of intelligent labels with QR codes and anti-counterfeiting features, enabling traceability and authenticity verification. This combination of governmental support, technological investment, and e-commerce growth positions China as a key market for innovative, sustainable print label solutions.

India: Government Initiatives and Technological Investments Propel Print Label Market

India’s print label market is benefiting from initiatives like Make in India and Zero Effect Zero Defect, which encourage high-quality domestic manufacturing and sustainable production practices. The National Packaging Initiative (2021) further promotes product safety and logistics efficiency, creating strong market demand for eco-friendly printed labels.

Regulatory measures, including the Plastic Waste Management (Amendment) Rules and Food Safety and Standards Packaging Regulations, are accelerating the shift toward sustainable and compliant labeling solutions. Investments in technology, such as FUJIFILM India’s Revoria Press™ series and Epson India’s ColorWorks CW-C8050 high-speed label printer, are enhancing production efficiency, color accuracy, and high-speed capabilities, particularly for pharmaceutical and industrial segments. Corporate initiatives and technology adoption ensure India’s print label market remains competitive, innovative, and aligned with global sustainability trends.

Print Label Market Report Scope

Print Label Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.9 Billion

|

|

Market Size (2034)

|

$77.8 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Label Type (Pressure-Sensitive Labels, Wet-Glue Labels, Linerless Labels, In-Mold Labels, Shrink Sleeves, Stretch Sleeves, Other Labels), By Printing Technology (Flexography, Digital Printing, Gravure, Offset, Letterpress, Screen Printing, Electrophotography), By End-Use Industry (Food & Beverages, Home & Personal Care, Consumer Goods, Pharmaceuticals & Healthcare, Retail, Industrial, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Avery Dennison Corporation, CCL Industries Inc., UPM Raflatac, Fuji Seal International, Inc., Lintec Corporation, HP Inc., Mondi Group, 3M Company, Nippon Paper Industries Co., Ltd., SATO Holdings Corporation, Toray Industries, Inc., Multi-Color Corporation (a part of CCL Industries), Cenveo Worldwide Limited, Smyth Companies, Fort Dearborn Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Print Label Market Segmentation

By Label Type

- Pressure-Sensitive Labels

- Wet-Glue Labels

- Linerless Labels

- In-Mold Labels

- Shrink Sleeves

- Stretch Sleeves

- Other Labels

By Printing Technology

- Flexography

- Digital Printing

- Gravure

- Offset

- Letterpress

- Screen Printing

- Electrophotography

By End-Use Industry

- Food & Beverages

- Home & Personal Care

- Consumer Goods

- Pharmaceuticals & Healthcare

- Retail

- Industrial

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Print Label Market

- Avery Dennison Corporation

- CCL Industries Inc.

- UPM Raflatac

- Fuji Seal International, Inc.

- Lintec Corporation

- HP Inc.

- Mondi Group

- 3M Company

- Nippon Paper Industries Co., Ltd.

- SATO Holdings Corporation

- Toray Industries, Inc.

- Multi-Color Corporation (a part of CCL Industries)

- Cenveo Worldwide Limited

- Smyth Companies

- Fort Dearborn Company

* List Not Exhaustive

Methodology

USDAnalytics employed a robust research methodology to deliver precise and actionable insights into the global Print Label Market. Our approach combined extensive primary research, including interviews with label manufacturers, brand owners in food, beverage, pharmaceutical, personal care, and industrial sectors, and sustainability and supply chain experts, with secondary research from company reports, press releases, trade events such as Labelexpo Europe, regulatory updates, and market intelligence databases. Market sizing, growth projections, and CAGR estimations were derived from historical trends, technological adoption in digital, flexographic, and hybrid printing, and emerging innovations such as NFC/RFID-enabled smart labels, recyclable substrates, and linerless labels. Segmentation analysis encompassed label types, printing technologies, and end-use industries, while qualitative insights highlighted mergers, acquisitions, capacity expansions, and sustainable material development by key players including Avery Dennison, CCL Industries, UPM Raflatac, 3M, and Mondi Group. This methodology ensured USDAnalytics provided a comprehensive, forward-looking perspective tailored for industry professionals seeking strategic, regulatory, and technology-driven insights in the evolving print label landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.