Market Overview: E-commerce, Recycling, and Single-Wall Board Define Growth

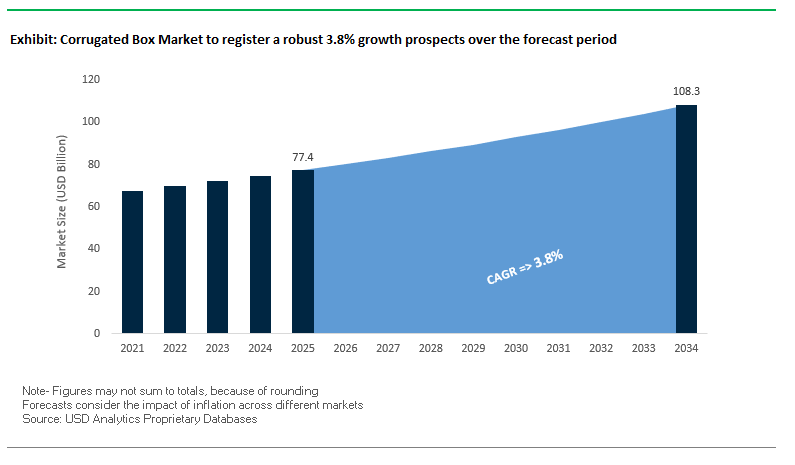

The global corrugated box market is forecasted to grow from USD 77.4 billion in 2025 to USD 108.3 billion by 2034, expanding at a CAGR of 3.8%. This steady growth is fueled by rising e-commerce shipments, food & beverage packaging demand, and a highly efficient recycling ecosystem. For buyers and industry professionals, the key questions revolve around how corrugated packaging can maintain its cost-effectiveness, sustainability leadership, and adaptability to new industries while meeting rising global logistics needs.

Corrugated boxes have become the backbone of e-commerce logistics, with over 60% of online retail shipments in North America using corrugated packaging. The food & beverage industry remains the largest end-use sector, requiring durable, stackable, and printable packaging for goods ranging from fresh produce to processed foods. Sustainability is a major driver, with the U.S. recycling more than 90% of old corrugated containers (OCC) in 2024, making it one of the most circular packaging materials globally. From a material perspective, single-wall board remains dominant, striking the balance between strength, versatility, and material efficiency.

Key Insights for Industry Professionals:

- E-commerce fuels demand: Corrugated boxes dominate online retail packaging with over 60% usage in North America.

- Food & beverage leadership: Largest end-use sector driven by protective, stackable solutions.

- Circular economy success: Over 90% recycling rate of OCC in the U.S. strengthens sustainability credentials.

- Single-wall dominance: Remains the most cost-effective and versatile corrugated material type.

Market Analysis: Recent Industry Developments Driving Strategic Shifts

The corrugated box industry is witnessing major consolidations, capacity expansions, and sustainability-led innovations.

In August 2025, Graphic Packaging secured child-resistant certification for its CleanClose™ detergent pod packaging, expanding corrugated’s role in non-traditional applications. The same month, Smurfit Westrock announced progress on merger synergies, improving operational efficiency following the combination of Smurfit Kappa and WestRock. Earlier, in July 2025, Packaging Corporation of America (PCA) signed a USD 1.8 billion agreement to acquire Greif’s containerboard business, significantly strengthening its North American position. In the same month, Graphic Packaging released its 2024 Impact Report, reiterating sustainability commitments under its “Better by 2030” strategy, while Smurfit Westrock reported operational improvements in North America tied to merger efficiencies.

In April 2025, International Paper acquired a 66.3% share in DS Smith, bolstering its footprint across the UK and European corrugated market. That same month, DS Smith collaborated with TPV Automotive to design fiber-based wheel carriers, showcasing corrugated’s adaptability in heavy-duty industrial applications. In January 2025, International Paper began construction on a new corrugated box plant in Waterloo, Iowa, strengthening its regional production capacity.

Trends and Opportunities Driving the Corrugated Box Market Transformation

Strategic Downsizing and Right-Sizing Driven by E-Commerce Logistics Economics

The corrugated box market is experiencing a pivotal transformation as right-sizing technologies emerge as a direct response to dimensional weight (DIM weight) pricing models used by global shipping carriers such as FedEx and UPS. By leveraging AI and machine learning algorithms, e-commerce giants and retailers are now able to automatically select the smallest viable box for each shipment, reducing material usage, optimizing truckload efficiency, and minimizing shipping fees. According to Packsize, companies adopting automated right-sizing have achieved up to 40% reduction in packaging volume, directly lowering logistics costs while cutting CO₂ emissions by fitting more parcels per truckload.

Material savings are equally significant. By eliminating void fill and oversized cartons, corrugated consumption can be reduced by nearly one-third, helping retailers meet aggressive sustainability targets. The consumer experience is also elevated, as customers increasingly value efficient, waste-free packaging that ensures product safety without excess material. Brands that avoid oversized boxes enhance customer loyalty and avoid negative unboxing reviews that can hurt brand perception. For example, apparel company Helly Hansen’s automated right-sizing system tripled throughput, cut labor costs, and eliminated unnecessary corrugated use, setting a precedent for how logistics optimization can simultaneously drive sustainability and profitability in the corrugated packaging industry.

Rapid Adoption of High-Performance, Lighter-Weight Liners and Fluting

Another major transformation in the corrugated box industry lies in material innovation, as manufacturers adopt lighter-weight liners and advanced fluting structures engineered for a superior strength-to-weight ratio. These developments reduce fiber consumption while delivering equal or better durability, an outcome critical for cost reduction and sustainability compliance. For example, Billerud’s 130 gsm fluting is proven to be 22% lighter than recycled high-performance fluting while outperforming it in sustained load testing. This lightweighting advantage reduces resource use, lowers transport emissions, and improves the overall carbon footprint of packaging operations.

Operational efficiency also improves significantly with lighter-weight corrugated. Flat-packing becomes more space-efficient, cutting storage and transportation costs for warehouses managing high e-commerce volumes. For retailers and CPG companies with ambitious sustainability agendas, these lightweight materials, often made from renewable and biodegradable sources, align perfectly with corporate targets to cut virgin fiber use. As sustainability regulations and cost pressures intensify, the shift toward lighter-weight liners and optimized fluting represents a strategic response that allows the corrugated box market to maintain its role as the backbone of e-commerce and retail packaging.

Development and Integration of Digital Watermarking for Circular Economy Compliance

One of the most promising opportunities for the corrugated packaging sector is the integration of digital watermarking technologies to enable precise sorting at material recovery facilities (MRFs). The HolyGrail 2.0 initiative, a coalition of over 130 companies, has validated that watermarked corrugated packaging can be automatically identified by high-resolution cameras, ensuring cleaner recycling streams. This allows for separation of food vs. non-food contact packaging and boosts the quality of post-consumer recycled (PCR) fiber, supporting brands in meeting stringent Extended Producer Responsibility (EPR) obligations under the EU’s Packaging and Packaging Waste Regulation (PPWR).

The technology not only enhances the recyclability of corrugated but also positions it as a circular economy champion, strengthening its competitive edge over plastic-based packaging. By promoting traceable recycling streams and higher-quality recycled content, digital watermarking ensures compliance with evolving global packaging laws while creating a direct pathway for brands to meet recycled-content quotas. For producers, this represents a dual advantage: strengthening sustainability credentials and maintaining regulatory compliance at reduced long-term costs.

Expansion of Coated and Functionalized Surfaces for Direct-to-Consumer Branding

With the rise of direct-to-consumer (DTC) retail and e-commerce, the corrugated box has evolved beyond a shipping vessel into a branded marketing channel. This creates a major opportunity to integrate advanced coatings and functionalized surfaces that enhance aesthetics, durability, and consumer engagement. For example, Sun Chemical’s water-based inks and coatings deliver high-resolution graphics that are rub- and scuff-resistant, ensuring vibrant branding survives the logistics journey. Similarly, water-resistant coatings provide a wax-like finish that maintains recyclability while protecting packaging from moisture damage during shipping.

These innovations improve not only brand visibility but also customer satisfaction by ensuring that products arrive in pristine condition. For categories like electronics and premium consumer goods, abrasion-resistant coatings reduce reliance on excess protective packaging while preventing scratches, dents, and returns due to transit damage. Moreover, as the unboxing experience becomes a viral marketing tool on social media, functionalized surfaces enhance packaging’s role in storytelling and customer loyalty. By transforming corrugated boxes into high-impact branding assets, manufacturers are unlocking new revenue streams while helping e-commerce brands strengthen identity and consumer engagement.

Competitive Landscape: Leading Players in the Corrugated Box Market

The global corrugated box market is highly competitive, led by multinational players pursuing strategic mergers, sustainability innovation, and global expansion.

Smurfit Westrock plc: Leveraging Merger Synergies for Global Leadership

Smurfit Westrock, formed by the merger of Smurfit Kappa and WestRock, is a leader in corrugated packaging solutions, offering traditional slotted boxes, high-graphics displays, and e-commerce packaging. In July 2025, it reported significant performance improvements in North America, driven by merger synergies, alongside plans to eliminate 600,000 tons of non-strategic capacity. With a global presence in 30+ countries, the company focuses on optimizing operations while driving sustainability in paper-based packaging.

International Paper Company: Expanding European and North American Corrugated Operations

International Paper is a major global producer of containerboard and corrugated packaging. In April 2025, it acquired a majority stake in DS Smith to expand its European market share, and in January 2025, it began constructing a new corrugated plant in Iowa. With over 66% of its fiber sourced from certified forests, International Paper underscores its focus on responsible sourcing while investing in modern production facilities to meet rising demand.

Packaging Corporation of America (PCA): Growing Through Strategic Acquisitions

PCA is a leading provider of containerboard and corrugated packaging for food, consumer products, and industrial markets. Its USD 1.8 billion acquisition of Greif’s containerboard business in July 2025 marks a key step in strengthening its North American market share. PCA is also investing in carbon capture initiatives, targeting a 35% reduction in Scope 1 and 2 emissions by 2030. Its corrugated products are widely used in e-commerce and consumer packaged goods, offering customized solutions for supply chain efficiency.

DS Smith plc: Driving Circular Economy and Smart Packaging Innovations

DS Smith specializes in sustainable corrugated packaging with a strong focus on circular economy models. In January 2025, it launched TailorTemp, a fiber-based alternative to EPS for cold chain logistics. Its “box-to-box in 14 days” recycling model and Circular Design Metrics tool are central to its sustainability leadership. With partnerships such as TPV Automotive (2025) and BeFC for bioenzymatic smart packaging, DS Smith is integrating technology and design innovation into its corrugated portfolio.

Graphic Packaging Holding Company: Innovating Beyond Traditional Corrugated Solutions

Graphic Packaging offers corrugated and folding carton solutions for food, beverage, and personal care markets. In August 2025, it introduced child-resistant CleanClose™ detergent pod packaging and PaperSeal® Pressed MAP trays, diversifying corrugated applications. Its investment in Waco, Texas a recycled paperboard facility set to start in Q4 2025 demonstrates its commitment to expanding capacity. Guided by its “Better by 2030” sustainability roadmap, the company focuses on fiber-based alternatives to plastics.

Corrugated Box Market Share Insights

Slotted Boxes Dominate Corrugated Box Market Share by Product Type

Slotted boxes (RSCs) account for nearly 55% of the global corrugated box market, cementing their position as the universal standard across shipping and distribution. Their efficient design minimizes material waste, reduces manufacturing costs, and ensures compatibility with high-speed automated filling lines. This cost-effectiveness, combined with their ability to handle diverse product categories from e-commerce parcels to bulk retail shipments drives their dominance. Trays and folded boxes follow, serving high-volume retail and food applications, while telescope boxes and rigid boxes are critical for premium goods, electronics, and fragile items that demand enhanced protection. Corrugated sheets support customized in-house production for manufacturers with box-making equipment, while niche formats like Bliss boxes and partitions cater to highly specific industrial needs. The overwhelming market share of slotted boxes reflects their unmatched versatility, recyclability, and ability to adapt to sustainability trends such as right-sizing and lightweighting, making them the cornerstone of global corrugated packaging demand.

E-Commerce & Logistics Drive Corrugated Box Market Share by End-Use Industry

E-commerce and logistics hold the largest share of the corrugated box industry at 35%, making them the defining growth engine of the sector. Online retail’s rapid expansion has placed corrugated boxes at the center of the “last-mile” delivery challenge, requiring packaging that balances durability, cost-efficiency, and sustainability. This segment drives innovation in automation-ready packaging, right-sized designs that reduce void space, and enhanced printability for branded unboxing experiences. Food & beverages represent the second-largest share, consuming vast volumes of corrugated cases and trays for shipping packaged foods and beverages to retailers and direct-to-consumer buyers. Electronics and personal care demand higher-grade constructions with anti-static and moisture-resistant features, while pharmaceuticals require compliance-driven packaging with serialization and traceability. Other industries including automotive, textiles, and agriculture rely heavily on corrugated packaging for safe and efficient global trade. The dominance of e-commerce and logistics underscores the critical role of corrugated boxes in shaping the future of supply chain packaging solutions.

United States: E-Commerce Boom Driving Advanced and Sustainable Corrugated Boxes

The U.S. corrugated box market is experiencing rapid growth, primarily fueled by the booming e-commerce and logistics sectors. The surge in online shopping has created a strong demand for durable, lightweight, and customizable corrugated boxes designed for last-mile delivery, ensuring product protection and customer satisfaction. Companies are increasingly integrating value-added features, including moisture-resistant coatings, “smart boxes” with QR codes and RFID tags, and other innovations to enhance traceability, consumer engagement, and operational efficiency.

Strategic mergers and acquisitions are shaping the competitive landscape. For example, Menasha Packaging’s acquisition of Color-Box has expanded its geographic reach and diversified its corrugated packaging portfolio. Sustainability is another major driver, as corrugated boxes are highly recyclable, made from renewable resources, and align with corporate environmental and ESG goals. These combined factors underscore the U.S. market’s emphasis on innovative, sustainable, and technology-enabled corrugated packaging solutions.

Germany: Regulatory Compliance and Circular Economy Strengthening Corrugated Packaging

Germany’s corrugated box industry is driven by stringent regulations, particularly the EU Packaging and Packaging Waste Regulation (PPWR) effective from February 2025. These regulations mandate the use of eco-friendly, recyclable, and high-quality packaging materials, pushing manufacturers to adopt sustainable production practices. Germany’s leadership in the circular economy fosters collaboration between manufacturers and end-users, encouraging the use of recycled content while reducing environmental impact.

Technological advancements play a critical role in enhancing production efficiency. Automated corrugated production lines and robotic solutions now allow short-run printing for promotional campaigns without compromising cost efficiency. Governmental mandates on waste reduction, improved recyclability, and increased recycled content further drive innovation in sustainable packaging solutions, solidifying Germany’s position as a global benchmark for environmentally responsible corrugated box manufacturing.

China: Industrial Expansion and Circular Packaging Systems Boost Corrugated Box Demand

China’s corrugated box market benefits from the country’s massive industrial expansion, particularly in the food, e-commerce, and manufacturing sectors, which require reliable, durable, and high-quality packaging. The introduction of new government regulations on delivery packaging since June 2025 encourages recycled materials and reusable systems, promoting sustainability and efficiency.

Closed-loop systems are also transforming production. For instance, companies in Zhejiang province recycle leftover box production scraps back into paper mills, creating a circular economy model that reduces waste and enhances resource efficiency. Strategic acquisitions, such as China Baowu Steel Group’s acquisition of CPMC Holdings, expand market reach and strengthen production capabilities, supporting China’s leadership in the eco-friendly corrugated packaging sector.

India: E-Commerce and Government Initiatives Driving Sustainable Corrugated Box Growth

India’s corrugated box industry is seeing strong growth, supported by the government’s “Make in India” and “Zero Effect Zero Defect” initiatives, which promote high-quality domestic production and industrial investment. The rapid rise of e-commerce and organized retail is driving demand for safe, hygienic, and durable corrugated packaging, particularly in food, consumer goods, and pharmaceutical segments.

Investment in manufacturing infrastructure is accelerating market expansion. For example, the Tinplate Company of India (TCIL) is establishing a new manufacturing facility to meet rising demand. Sustainability remains central, with government regulations such as the Plastic Waste Management (Amendment) Rules pushing adoption of paper-based, biodegradable, and eco-friendly packaging alternatives. These developments position India as a fast-growing market for technologically advanced and sustainable corrugated box solutions.

Brazil: Regulatory and Technological Developments Enhancing Eco-Friendly Corrugated Packaging

The Brazilian corrugated box market is being shaped by stringent regulations, such as the National Solid Waste Policy, which discourages single-use plastics and promotes a circular economy. This has driven the adoption of reusable and durable corrugated packaging. Technological advancements, including AI and robotics, are improving production efficiency, quality control, and defect detection, enabling more precise and faster operations.

The market is also witnessing a shift toward sustainable materials, such as paperboard, recycled PET (rPET), and bioplastics, aligning with both consumer preferences and regulatory support. Strategic investments from global and domestic players in the industrial packaging sector are further driving demand for high-quality corrugated boxes, creating opportunities for innovation and sustainable packaging solutions in Brazil.

Japan: Innovation and Bio-Based Materials Leading Sustainable Corrugated Box Development

Japan’s corrugated box industry leverages advanced recycling systems, boasting one of the world’s highest rates of waste paper and plastic collection, which supports the production of recycled packaging solutions. The government’s Plastic Resource Circulation Act encourages circular packaging, while the country is increasingly adopting bio-polypropylene (bio-PP) and other bio-based materials, especially in cosmetic and food packaging applications.

Innovation in functionality is a key differentiator. Companies such as Rengo Co., Ltd. have developed solutions like the S-Lock Tray for fruit, which optimizes material usage while improving assembly efficiency. Collaborations between industry leaders like LyondellBasell, Shiseido, Futamura Chemical, and Iwatani further advance bio-PP integration, helping Japan meet its 2030 and 2050 environmental targets. These initiatives establish Japan as a front-runner in functional, sustainable, and innovative corrugated packaging solutions.

Corrugated Box Market Report Scope

Corrugated Box Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$77.4 Billion

|

|

Market Size (2034)

|

$108.3 Billion

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Material Type (Linerboard, Medium, Recycled Paperboard, Virgin Paperboard), By Wall Type (Single Wall, Double Wall, Triple Wall, Single Faced), By Product Type (Slotted Boxes, Telescope Boxes, Rigid Boxes, Folded Boxes, Trays, Sheets, Other Products), By End-Use Industry (Food & Beverages, E-commerce & Logistics, Electronics & Electricals, Personal Care & Homecare, Pharmaceuticals & Healthcare, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper, Smurfit Kappa Group plc, WestRock, Oji Holdings Corporation, DS Smith Plc, Packaging Corporation of America (PCA), Rengo Co., Ltd., Mondi Group, Shanying Paper Co., Ltd., Graphic Packaging Holding Company, Sonoco Products Company, Klabin S.A., BWAY Corp., Cascades Inc., Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Corrugated Box Market Segmentation

By Material Type

- Linerboard

- Medium

- Recycled Paperboard

- Virgin Paperboard

By Wall Type

- Single Wall

- Double Wall

- Triple Wall

- Single Faced

By Product Type

- Slotted Boxes

- Telescope Boxes

- Rigid Boxes

- Folded Boxes

- Trays

- Sheets

- Other Products

By End-Use Industry

- Food & Beverages

- E-commerce & Logistics

- Electronics & Electricals

- Personal Care & Homecare

- Pharmaceuticals & Healthcare

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Corrugated Box Market

- International Paper

- Smurfit Kappa Group plc

- WestRock

- Oji Holdings Corporation

- DS Smith Plc

- Packaging Corporation of America (PCA)

- Rengo Co., Ltd.

- Mondi Group

- Shanying Paper Co., Ltd.

- Graphic Packaging Holding Company

- Sonoco Products Company

- Klabin S.A.

- BWAY Corp.

- Cascades Inc.

- Greif, Inc.

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the global corrugated box market, examining key breakthroughs, competitive dynamics, and strategic developments shaping the industry. The analysis reviews how e-commerce expansion, sustainability mandates, and material innovations are driving both operational efficiency and environmental compliance. Highlights include trends in automation, lightweighting, digital watermarking for recycling, and advanced surface functionalization, offering detailed insights into emerging opportunities across food & beverage, e-commerce, and industrial applications. This report is an essential resource for manufacturers, packaging engineers, sustainability officers, and logistics planners seeking actionable intelligence to optimize production, adopt high-performance materials, and align with regulatory frameworks worldwide. By integrating historic performance with forward-looking projections, this study provides a comprehensive understanding of market evolution, enabling informed decisions on capacity expansions, technological adoption, and strategic partnerships.

Scope Highlights:

- Segmentation: By Material Type (Linerboard, Medium, Recycled Paperboard, Virgin Paperboard), By Wall Type (Single Wall, Double Wall, Triple Wall, Single Faced), By Product Type (Slotted Boxes, Telescope Boxes, Rigid Boxes, Folded Boxes, Trays, Sheets, Other Products), By End-Use Industry (Food & Beverages, E-commerce & Logistics, Electronics & Electricals, Personal Care & Homecare, Pharmaceuticals & Healthcare, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ companies, including International Paper, Smurfit Kappa Group plc, WestRock, DS Smith plc, PCA, Graphic Packaging Holding Company, Rengo Co., Ltd., Mondi Group, Sonoco Products Company, and others

Methodology

This USDAnalytics report employs a robust multi-step methodology to ensure data accuracy, relevance, and actionable insights. Market sizing and forecasts are derived using a combination of primary research, including interviews with senior executives, packaging engineers, and supply chain managers, and secondary research comprising corporate filings, trade publications, regulatory reports, and industry databases. Quantitative data was validated through triangulation across production volumes, shipment statistics, and historical growth trends, while qualitative analysis examined emerging material innovations, sustainability adoption, and automation in packaging operations. The methodology integrates regional market dynamics, end-use segmentation, and competitive benchmarking to provide a global perspective, ensuring that forecasts reflect both macroeconomic factors and micro-level operational realities. USDAnalytics also incorporates scenario-based projections to account for potential regulatory shifts, technological breakthroughs, and changing consumer preferences in e-commerce and industrial supply chains.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.