Market Overview: Folding Carton Industry Expands with Sustainability and Premium Packaging Demand

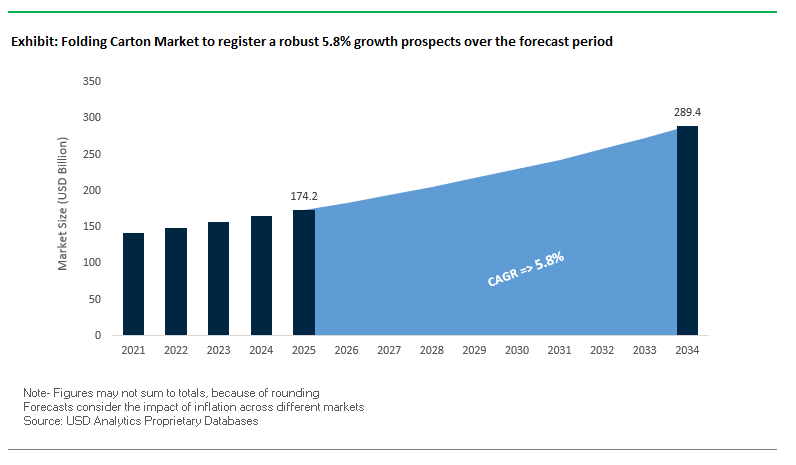

The Folding Carton Market is expected to grow from $174.2 billion in 2025 to $289.3 billion by 2034, registering a CAGR of 5.8%. This strong growth is attributed to rising adoption of recycled fiber-based cartons, booming demand from the food and beverage sector, and increasing consumer preference for premium packaging in cosmetics and personal care. Folding cartons are gaining prominence as brands align with sustainability regulations and consumers shift away from single-use plastics.

The market is characterized by a high degree of concentration, with the top five producers controlling over 25% of global production volume in 2024, and the top ten players collectively accounting for almost 40%. This concentration reflects the dominance of a few global players who leverage vertical integration, large-scale production capabilities, and sustainability-focused innovation to maintain market leadership.

Recycled materials are central to growth. In 2024, recycled paper and paperboard accounted for a significant market share, driven by regulations banning plastics and consumer demand for environmentally friendly packaging. Food and beverage remains the largest end-user, supported by rising demand for convenience foods and sustainable options. Meanwhile, personal care and cosmetics brands are pushing the boundaries of premium packaging by adopting cartons with advanced finishes and design elements that reflect product value.

Key Insights for Industry Professionals

- Recycled fiber adoption accelerates: Driven by sustainability regulations and consumer demand.

- Food & beverage dominates: Convenience foods and sustainable packaging fuel market expansion.

- Cosmetics drive premium demand: Folding cartons increasingly used for high-quality, experiential packaging.

- Market remains concentrated: Top five producers account for 25%+ of global volume.

Market Analysis: Recent Developments Driving Folding Carton Innovation

The global folding carton industry has experienced significant activity in the past two years, with mergers, acquisitions, and sustainability initiatives reshaping competition and capacity.

In August 2025, Smurfit Kappa and WestRock completed their merger to form Smurfit WestRock, a global packaging powerhouse with enhanced reach in folding cartons and other paper-based packaging. That same month, Mayr-Melnhof Karton AG (MM) reported a profit boost, supported by the sale of its TANN Group and improvements in its Board & Paper division, signaling resilience amid a competitive environment.

Earlier in July 2025, Graphic Packaging International released its 2024 Impact Report, announcing it had replaced approximately 1 billion plastic packages with paperboard solutions a major milestone in sustainability. In May 2025, MM Karton showcased premium papers at an event in Paris, reinforcing its role in sustainable luxury packaging.

The sector is also being transformed by partnerships. In April 2025, DS Smith partnered with TPV Automotive to deliver plastic-free packaging for BMW wheel carriers, reflecting how folding carton innovation is expanding into luxury and industrial applications.

Key consolidation trends continue. The February 2025 merger of Smurfit Kappa and WestRock created a $12.7 billion entity, strengthening global supply. In November 2024, MM rebranded its recycled cartonboard portfolio, sharpening its premium positioning. Strategic acquisitions also remain critical Graphic Packaging’s $262.5 million acquisition of Bell Inc. (September 2023) expanded its presence in foodservice and mailer packaging.

Emerging Trends and Opportunities Defining the Folding Carton Market

Accelerated Transformation of Folding Cartons through Digital and Sustainable Innovations

The folding carton market is undergoing a major shift as brands prioritize agility, personalization, and sustainability in their packaging strategies. Digital finishing technologies and advanced barrier coatings are setting new benchmarks for efficiency, consumer engagement, and environmental performance. At the same time, opportunities are opening for molded fiber integration and e-commerce–ready designs that support circular economy principles and enhance retail performance.

Accelerated Adoption of Digital Finishing for Versioning and Personalization

Folding cartons are increasingly being transformed into dynamic marketing tools through the use of advanced digital finishing technologies. Digital embellishment techniques ranging from spot UV and foiling to high-speed die-cutting are being scaled by packaging converters to offer short-run and variable packaging at competitive costs. Companies like Koenig & Bauer are pioneering hybrid solutions that merge offset printing with digital inkjet, allowing brands to personalize packaging with variable data and region-specific messaging. This shift reduces reliance on costly printing plates and enables agile versioning for limited editions, seasonal promotions, and regional campaigns. The operational impact is significant: brands adopting digital finishing reduce inventory waste by producing only the quantities needed in a “just-in-time” model, avoiding obsolete pre-printed cartons. The result is not just improved sustainability but also faster response to consumer micro-trends. In fast-moving consumer goods (FMCG) markets, where speed-to-shelf can determine competitiveness, digital finishing has become a critical enabler of brand agility and consumer engagement.

Integration of Advanced Barrier Coatings to Replace Plastic Lamination

Sustainability regulations and corporate commitments are driving rapid adoption of folding cartons with plastic-free barrier solutions. Traditional plastic-laminated cartons, often non-recyclable, are being phased out in favor of water-based dispersion and polyvinyl alcohol (PVdH) coatings that maintain product protection while ensuring recyclability. The European Union’s Packaging and Packaging Waste Regulation (PPWR) requires recyclability at scale by 2035, accelerating this transition. Packaging leaders such as Mondi have invested heavily in expanding production of high-performance barrier papers, designed to block oxygen, grease, and water vapor without plastic layers. Meanwhile, research on bio-based coatings demonstrates the efficacy of cellulose and chitosan in replacing conventional liners, opening new pathways for food-grade and sensitive product applications. Global brands like Nestlé are already transitioning entire product lines to recyclable mono-material solutions, underscoring the commercial viability of advanced coatings. As plastic reduction becomes a regulatory mandate, folding cartons with barrier coatings are emerging as a strategic cornerstone of the sustainable packaging market.

Development of High-Performance Molded Fiber Solutions within Cartons

A key opportunity lies in integrating molded fiber trays, dividers, and cushioning elements directly into folding carton designs to create all-paper, curbside recyclable solutions. This innovation directly targets the replacement of expanded polystyrene (EPS) and other plastic inserts in high-value segments such as consumer electronics, cosmetics, and industrial parts. Case studies from the electronics sector reveal that companies are rapidly transitioning to molded fiber inserts for packaging laptops, smartphones, and accessories, both to improve sustainability credentials and to enhance the premium unboxing experience. Beyond aesthetics, molded fiber delivers superior functional benefits: it is customizable for precise fit, offers excellent shock absorption, and reduces CO2 emissions by 40–60% compared to plastics. As molded fiber is derived from recycled paper, it adds circularity to the supply chain while aligning with corporate ESG goals. For folding carton manufacturers, this represents a high-margin diversification strategy into protective and specialty packaging.

Expansion into E-commerce Ready and Shelf-Ready Packaging (SRP) Designs

The convergence of e-commerce and retail channels is creating a surge in demand for folding cartons designed as “one-pack” solutions durable enough for direct shipping yet visually appealing for retail shelves. These hybrid cartons eliminate the need for secondary shipping boxes, reducing packaging waste and lowering logistics costs. For e-commerce platforms, lightweight yet sturdy folding cartons help optimize pallet space and reduce shipping-related emissions, while simplifying consumer unboxing. On the retail side, shelf-ready packaging (SRP) designs streamline store operations. Industry research indicates SRP can reduce restocking time by up to 40%, translating to measurable labor savings for retailers. Additionally, SRP designs with perforated openings allow products to transition seamlessly from shipping to shelf display, improving efficiency and brand visibility. The dual role of folding cartons in supply chain efficiency and consumer experience makes this opportunity particularly compelling for brands navigating the omnichannel retail landscape.

Competitive Landscape: Leading Companies Shaping the Folding Carton Industry

The folding carton market is dominated by global leaders that combine scale, vertical integration, and sustainability-driven innovation. Companies are leveraging mergers, acquisitions, and advanced technologies to strengthen their portfolios and respond to rising demand for eco-friendly and premium packaging.

Graphic Packaging International: Expanding with Bell Inc. Acquisition

Graphic Packaging is a global leader in fiber-based consumer packaging, offering folding cartons, cups, and sustainable solutions across food, beverage, and household markets. In September 2023, it acquired Bell Inc. for $262.5 million, gaining new capabilities in foodservice and mailers. The company emphasizes replacing plastics with paperboard through proprietary technologies such as Boardio™ and EnviroClip™. With a new recycled paperboard mill in Waco, Texas scheduled for 2025, Graphic Packaging is positioning itself as a long-term leader in sustainable carton innovation.

Smurfit WestRock: A Global Giant Formed Through Merger

Smurfit WestRock, created in 2025, is now one of the largest paper-based packaging companies in the world. Its folding carton offerings include custom-designed cartons with advanced finishing for premium goods and corrugated solutions for e-commerce. Its vertical integration from forests to recycling ensures closed-loop sustainability and quality. The merger combines extensive footprints and innovation pipelines, positioning the company as a dominant supplier to global brands.

Mayr-Melnhof Karton AG: Strengthening Through Fit-for-Future Strategy

Mayr-Melnhof Karton AG (MM) is Europe’s leading cartonboard producer, serving food, pharma, and premium packaging markets. Its Fit-For-Future program aims to deliver over €150 million in profit improvements by 2027. In August 2025, MM reported profit growth, aided by the sale of TANN Group and operational improvements. With vertical integration across cartonboard and folding cartons, MM ensures strong supply chain control while advancing premium and sustainable offerings.

Amcor plc: Innovating Premium Cartons with Sustainable Features

Amcor combines its global expertise in flexible and rigid packaging with a strong presence in specialty folding cartons. Known for advanced printing such as scented varnishes and optical effects, Amcor helps brands elevate shelf impact. Its AmSky Blister System, a mono-material PE solution, showcases its sustainability focus. Amcor is targeting 100% recyclability by 2025, while providing premium folding carton designs with tactile and visual enhancements for high-value markets.

DS Smith Plc: Scaling with International Paper Merger

DS Smith is a leader in 100% recycled fiber-based cartons, supporting closed-loop models. Its late 2024 approval of a merger with International Paper represents a major consolidation move that will expand its reach across Europe and North America. The company’s strategy, “Redefining Packaging for a Changing World,” centers on eliminating plastics and advancing fiber-based alternatives. With integrated recycling and paper operations, DS Smith ensures consistent supply for sustainable folding carton customers.

Folding Carton Market Share Insights

Food & Beverages Drive Market Share by End-Use Industry in Folding Cartons

Food and beverages dominate folding carton demand, accounting for 40% of global share, underpinned by the sector’s reliance on paperboard solutions for cereals, frozen foods, dairy, tea, and ready-to-eat products. The key driver is the pivot away from plastic trays and clamshells toward recyclable and compostable paperboard cartons, aligning with stringent packaging waste directives in the EU and rising consumer pressure for eco-friendly formats. Cartons provide expansive billboard space for branding and regulatory information, offering manufacturers an unmatched platform to differentiate products in crowded retail environments. Their machinability on high-speed filling lines and compatibility with digital print also make them well-suited for e-commerce-ready designs, where durability and graphic quality are equally critical. The segment’s leadership reflects its ability to balance cost efficiency, sustainability, and marketing effectiveness, making food packaging the cornerstone of folding carton industry revenues.

Lithography Secures Leading Market Share by Printing Technology in Folding Cartons

Offset lithography retains its leadership with a 60% share of folding carton printing, reflecting its unique ability to deliver consistent brand colors, fine detail, and cost efficiency for high-volume runs. It remains the gold standard for the food, pharmaceutical, and personal care sectors, where brand identity and regulatory information demand precision. The dominance of litho is further reinforced by its scalability, allowing converters to manage medium-to-very-long runs without compromising print quality. While flexo and digital technologies are growing, they remain complementary; flexo is gaining traction for corrugated and simpler cartons, and digital printing excels in personalization. Yet, lithography’s entrenched infrastructure, broad substrate compatibility, and unmatched cost-per-unit economics keep it at the forefront, anchoring the global folding carton supply chain.

United States: Rising Sustainability Awareness Drives Demand for Recyclable Folding Cartons

The U.S. folding carton market is experiencing robust growth, driven by consumer and corporate demand for sustainable, recyclable paperboard packaging across food, pharmaceutical, and consumer goods sectors. Increasing awareness of eco-friendly packaging solutions has prompted investments in advanced paper recycling infrastructure, with the American Forest & Paper Association (AF&PA) reporting over $4.5 million in projects from 2019 to 2025 to enhance recycled paper capacity.

Technological innovation is another key driver. Smart packaging solutions, including QR codes and RFID integration, are being adopted to enhance product traceability, consumer engagement, and supply chain transparency. The surge in e-commerce is also fueling demand for folding cartons that are protective, visually appealing, and tamper-evident, supporting premium and fast-moving consumer goods alike. Major corporations, such as Stora Enso, are developing recyclable packaging boards suitable for chilled and frozen food, reducing reliance on plastics and aligning with corporate sustainability goals.

Germany: Circular Economy Leadership Shapes High-Quality Folding Carton Production

Germany’s folding carton industry is strongly influenced by the EU Packaging and Packaging Waste Regulation (PPWR 2025), which mandates fully recyclable packaging by 2030 and sets reuse and refill targets. This stringent regulatory environment is accelerating the adoption of eco-friendly, recyclable paperboard solutions and driving innovation across packaging supply chains.

The country is a global leader in circular economy practices, with manufacturers focusing on high recycled content in folding cartons and advanced converting equipment to enable cost-effective production of short runs for consumer-focused branding. The PPWR framework, combined with technological advancements in sustainable materials, is creating a highly competitive market that prioritizes both recyclability and premium-quality packaging solutions.

China: Government Policies and E-Commerce Expansion Fuel Sustainable Folding Carton Growth

China’s folding carton market is being reshaped by dual carbon goals, promoting the use of eco-friendly, reduced, and reusable materials across the paper and packaging industries. The government’s circular economy initiatives encourage the adoption of recycled fiber, with manufacturers rewarded under the national carbon credit scheme for increasing recovered content.

Technological advancements, such as AI-driven production and 5G-enabled industrial integration, are enhancing efficiency and flexibility in carton manufacturing. The import ban on unsorted solid waste has further stimulated domestic sourcing of recycled paper, boosting local paper mills and processing capacities. Additionally, the rapid expansion of e-commerce channels has increased demand for secure, tamper-proof, and recyclable folding cartons, with government policies promoting biodegradable and eco-friendly alternatives in express delivery packaging.

India: Government Support and E-Commerce Expansion Accelerate Sustainable Folding Carton Adoption

India’s folding carton industry benefits from government initiatives like Make in India and Zero Effect Zero Defect, which promote high-quality domestic production and investment in industrial infrastructure. The rapid growth of food processing and e-commerce sectors is a major catalyst, driving demand for affordable, protective, and eco-friendly packaging for a wide range of consumer goods.

Sustainability is a core focus, supported by policies such as the Plastic Waste Management (Amendment) Rules, which aim to phase out certain single-use plastics, increasing demand for recyclable alternatives. Investment in advanced manufacturing technologies is also enhancing production efficiency and product quality. For example, TCPL recently commissioned three new automated rigid box-making lines for luxury packaging of mobile phones, smartwatches, and wearables, demonstrating India’s growing capability in producing premium, sustainable folding cartons.

Folding Carton Market Report Scope

Folding Carton Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$174.2 Billion

|

|

Market Size (2034)

|

$289.3 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Material Type (FBB, SBS, CUK, WLC, URB), By End-Use Industry (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Tobacco, Consumer Electronics, Other Industries), By Printing Technology (Flexography, Lithography, Digital Printing, Gravure)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

WestRock Company, Graphic Packaging Holding Company, Smurfit Kappa Group, DS Smith plc, International Paper, Mayr-Melnhof Karton AG, Mondi Group, Amcor plc, Stora Enso Oyj, AR Packaging, Parksons Packaging Ltd., TCPL Packaging Ltd., Sonoco Products Company, Huhtamaki Oyj, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Folding Carton Market Segmentation

By Material Type

By End-Use Industry

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Tobacco

- Consumer Electronics

- Other Industries

By Printing Technology

- Flexography

- Lithography

- Digital Printing

- Gravure

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Folding Carton Market

- WestRock Company

- Graphic Packaging Holding Company

- Smurfit Kappa Group

- DS Smith plc

- International Paper

- Mayr-Melnhof Karton AG

- Mondi Group

- Amcor plc

- Stora Enso Oyj

- AR Packaging

- Parksons Packaging Ltd.

- TCPL Packaging Ltd.

- Sonoco Products Company

- Huhtamaki Oyj

- Greif, Inc.

* List Not Exhaustive

Methodology

The methodology for the Folding Carton Market research integrates both primary and secondary approaches to provide a comprehensive, industry-focused analysis. Primary research included in-depth interviews with key stakeholders such as folding carton manufacturers, packaging designers, sustainability experts, and end-use industry executives to understand evolving trends, technological adoption, and market challenges. Secondary research leveraged company press releases, financial statements, trade journals, regulatory updates, and market reports to validate findings and track competitive developments, including mergers, acquisitions, and sustainability initiatives. Market sizing employed a top-down approach, beginning with the global packaging market and narrowing to folding cartons by material type, end-use industry, and printing technology, while CAGR projections were calculated using historical and forecasted growth data. The study analyzed regional dynamics in major markets such as the U.S., Germany, China, and India, considering regulatory frameworks, e-commerce growth, and sustainability adoption. Quantitative analysis included market share, production capacity, and investment trends, while qualitative assessment examined innovation in digital finishing, plastic-free barrier coatings, molded fiber solutions, and e-commerce-ready designs. The methodology ensures a data-driven, actionable perspective for industry professionals seeking to align with sustainability mandates, regulatory requirements, and premium packaging strategies.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.