Mailer Packaging Market Overview: Growth Outlook and Strategic Insights

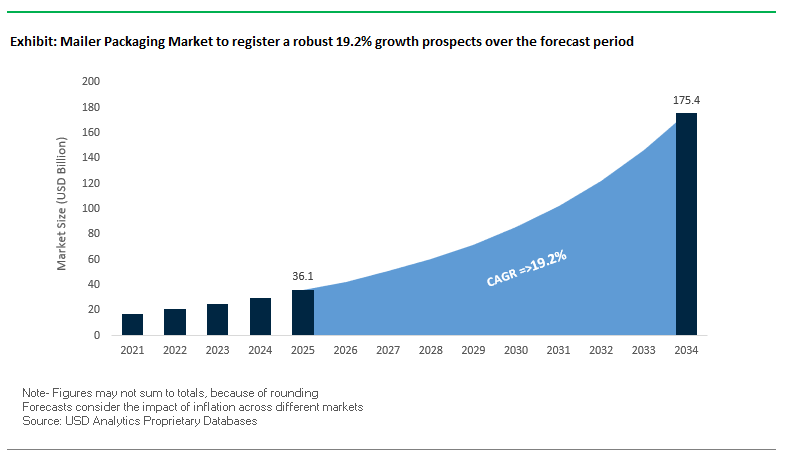

The global mailer packaging market is projected to expand from $36.1 billion in 2025 to $175.4 billion by 2034, representing an exceptional CAGR of 19.2%. This exponential growth is fueled by the dominance of e-commerce, where mailer packaging has become a backbone of the direct-to-consumer (D2C) economy. In 2024, over 50% of revenue share came from e-commerce shipments, reflecting rising demand for lightweight, protective, and branded mailers that meet the logistics requirements of global online retail.

A major structural shift is underway toward paper-based and fiber-based packaging, which accounted for more than 50% of the market share in 2024. This change is being accelerated by regulatory pressures, consumer demand for curbside recyclability, and brand commitments to sustainability. At the same time, tamper-evident, puncture-resistant, and water-resistant features have become standard expectations, especially for sectors such as electronics, pharmaceuticals, and cosmetics where secure delivery is critical.

Innovation is extending beyond materials into smart packaging integration, where QR codes and RFID-enabled mailers are emerging as differentiators. These technologies allow real-time product tracking, improve supply chain visibility, and strengthen brand-consumer engagement through authentication and transparency. As a result, the market is not only about safe transport but also about enhancing consumer experience and sustainability credentials, making mailer packaging an essential component of future commerce.

Key Insights for Industry Stakeholders

- Market Growth: $36.1B (2025) → $175.4B (2034) at CAGR of 19.2%.

- E-commerce Dominance: Over 50% revenue from online retail shipments in 2024.

- Paper-Based Leadership: Paper segment held 50%+ share in 2024, driven by recyclability.

- Protective Features: Tear, puncture, and water resistance are now baseline requirements.

- Smart Mailers: RFID and QR code integration for tracking, efficiency, and authentication.

Market Analysis: Recent Developments Reshaping the Mailer Packaging Industry

The mailer packaging market is evolving rapidly with a blend of sustainability-driven initiatives and consumer behavior shifts. In February 2025, Pregis’s EverTec cushioned paper mailer earned an independent certification of recyclability, underscoring the industry’s transition from plastic-based to fiber-based protective solutions. Similarly, in January 2025, New York lawmakers advanced the Packaging Reduction & Recycling Act, a policy move expected to accelerate demand for recyclable paper mailers and discourage excessive use of plastics. At the same time, DS Smith presented its ePack solutions in January 2025, showcasing a blend of customization, practicality, and eco-friendly materials, a response to the growing pressure on brands to balance personalization with sustainability.

Sustainability is increasingly intersecting with corporate innovation strategies. The merger activities between DS Smith and Mondi (March 2024) and Smurfit Kappa with WestRock (2024) illustrate how consolidation is reshaping the industry landscape, creating larger entities with vertically integrated and globalized capabilities to meet growing e-commerce packaging demand. Furthermore, the rollout of sustainability roadmaps such as Mondi’s MAP2030 and Sealed Air’s 2025 recyclability goal indicates a strong alignment between environmental goals and long-term competitiveness.

Consumer trends also play a subtle but important role. Studies in March 2025 highlighted a rise in demand for customizable packaging solutions, paralleling the personalization trend in consumer products. While seasonal spikes in packaging-related searches (as tracked in August 2025) were primarily tied to lunch bag data, the underlying insight is clear: consumer expectations for functional, customizable, and eco-friendly packaging are shaping design choices across multiple categories, including mailers.

Transformative Trends and Emerging Opportunities in the Global Mailer Packaging Market

Rapid Adoption of Curbside-Recyclable Polyethylene Film Solutions

The mailer packaging market is undergoing a major sustainability transformation as e-commerce and retail companies pivot to curbside-recyclable polyethylene films. Traditional plastic mailers are increasingly being replaced with formulations designed for compatibility with store drop-off and municipal recycling streams, driven by both consumer demand and corporate ESG commitments. Initiatives like the Hefty ReNew™ program and the Flexible Film Recycling Alliance (FFRA) are enabling curbside collection of flexible plastics, paving the way for greater consumer participation. Industry-wide collaborations, such as the UK’s FlexCollect initiative, demonstrate that flexible plastics can be efficiently collected and sorted, with nearly 90% of the material meeting high-quality targets. Significant investments in mechanical and chemical recycling technologies by leading brands ensure that post-consumer recycled (PCR) content performs reliably, with Unilever’s “Future Flexibles” program illustrating how data-driven characterization of 160 grades of recycled plastic accelerates R&D by 25%. This trend underscores the market’s move beyond generic recyclable claims toward technically verified, high-performance sustainable mailers.

Integration of Automation-Optimized, Right-Sized Packaging Designs

The rise of dimensional weight pricing and operational efficiency demands is accelerating the adoption of automation-driven right-sizing technologies in mailer packaging. E-commerce giants are leveraging systems that select the smallest possible mailer for a product, reducing shipping costs, eliminating void fill, and improving fulfillment throughput. For instance, Helly Hansen’s collaboration with packaging automation providers enabled tripled throughput by cutting cartons to the precise fill height. Right-sizing mailers not only optimizes payload and reduces shipping fees with carriers like FedEx and UPS but also addresses consumer expectations for functional, sustainable, and frustration-free unboxing experiences. Advanced systems such as Smurfit Westrock’s “Pak On Demand” create custom mailers that conform to product shape, eliminating excess packaging while enhancing brand credibility and operational efficiency.

Development of High-Performance, Bio-Based and Compostable Barrier Films

The mailer packaging sector has a prime opportunity to replace fossil-fuel-based plastics with bio-based, compostable alternatives without compromising performance. Materials like polylactic acid (PLA) and polybutylene succinate (PBS) offer tensile strength and barrier properties comparable to conventional plastics. BASF’s ecovio® product demonstrates that compostable films can maintain durability while supporting industrial and home composting pathways, creating a circular economy model. Additionally, renewable-based polymers can reduce carbon footprint substantially, with potential annual CO2 savings of up to 315 million tons, addressing both sustainability goals and regulatory pressures. This opportunity positions bio-based barrier films as a premium, environmentally conscious alternative for brands targeting eco-aware consumers.

Expansion of Reusable and Returnable Mailer Systems for B2C and B2B Applications

Beyond material innovation, the shift toward reusable mailer systems represents a transformative opportunity in both B2C and B2B segments. Models like EcoPackables’ 100% recycled polyester mailers for subscription boxes and apparel rentals enable multiple shipping cycles with return-to-brand or network collection systems. In B2B applications, companies such as THIELMANN and iCan Fluid Transfer System have proven that reusable logistics networks can dramatically cut waste and operational costs for industrial shipments. These systems offer high durability, often exceeding 20 reuse cycles, making them economically viable and environmentally sustainable over the long term. By enabling durable, high-performance reusable mailers, brands can reduce single-use waste, lower logistics costs, and enhance their ESG credentials.

Competitive Landscape – Leading Players in the Global Mailer Packaging Market

The mailer packaging industry is dominated by global packaging giants that are investing in sustainability, automation, and smart packaging technologies to differentiate in a high-growth, highly competitive market. Companies such as Smurfit Westrock, Sealed Air, International Paper, DS Smith, and Mondi are leading through mergers, material innovations, and strong commitments to circular economy principles.

Smurfit Westrock – Scale and Automation Drive Competitive Advantage

Smurfit Westrock, formed through the 2024 merger of Smurfit Kappa and WestRock, is a global powerhouse in paper-based packaging solutions. Its offerings range from corrugated postal packs to automated bagging systems tailored for e-commerce. The company is investing heavily in on-demand packaging solutions like EZ-Wrap™ and Pak On Demand™, which create custom-sized, recyclable mailers and reduce waste. Its integration into Amazon’s APASS program and eSmart optimization services position Smurfit Westrock as a trusted partner for D2C logistics.

Sealed Air Corporation – Protective Mailers with a Sustainability Focus

Sealed Air, widely recognized for its Bubble Wrap brand, is equally influential in mailer packaging with cushioned and non-cushioned mailer solutions. The company has committed to ensuring 100% recyclability or reusability of its packaging by 2025, reflecting its strong sustainability agenda. Its innovation strategy focuses on protective features, material efficiency, and supply chain optimization, making it a preferred choice for sensitive shipments such as electronics and pharmaceuticals.

International Paper Company – Fiber-Based Leadership and Global Scale

International Paper brings unmatched scale to the mailer packaging sector through its fiber-based packaging portfolio. The company is advancing sustainability through initiatives like incorporating recycled content and its ForSite fiber mapping tool for supply chain traceability. With ownership of raw materials and vertically integrated operations, International Paper is positioned to provide consistent quality and innovative, recyclable mailer packaging solutions across diverse industries including e-commerce, food, and industrial applications.

DS Smith Plc – Customization and Circular Economy Integration

DS Smith’s ePack brand has become synonymous with e-commerce-focused, customizable, and sustainable packaging. With the potential merger with Mondi announced in March 2024, DS Smith is poised to expand its global footprint significantly. The company’s focus on circular economy principles, material efficiency, and design-led customization ensures that it stays at the forefront of meeting retailer and consumer sustainability demands while offering highly tailored packaging solutions.

Mondi Group – Vertically Integrated Sustainability Leader

Mondi is a leading global supplier of paper and packaging products with a robust portfolio spanning paper mailers, bags, and corrugated solutions. The company’s MAP2030 commitments—aiming for all products to be recyclable, reusable, or compostable by 2025—underscore its sustainability-first approach. Mondi’s vertically integrated operations, from forest management to finished packaging, provide unmatched control over quality and sustainability, making it a key global player in the rapidly growing mailer packaging industry.

Mailer Packaging Market Share Insights

Cushioned Mailers Hold Majority Market Share by Product Type in the Mailer Packaging Industry

Cushioned mailers dominate with a 60% share of the global mailer packaging market, positioning themselves as the default e-commerce packaging format. Their integrated bubble or foam linings deliver lightweight protection for a wide range of products, from apparel and cosmetics to electronics and books, without the bulk or expense of corrugated boxes. Retailers rely on cushioned mailers to optimize shipping costs by reducing dimensional weight (DIM) charges and improving storage efficiency in fulfillment centers. Their high adoption rate also reflects their versatility in supporting custom branding, sustainable material substitutions (such as paper-based cushioning), and operational efficiency in automated packing lines, making them the uncontested standard across online retail ecosystems.

E-commerce Continues to Dominate Market Share by End-User in the Mailer Packaging Market

The e-commerce sector accounts for 70% of the mailer packaging industry, underscoring its role as the single largest and fastest-growing end-user. Online marketplaces and DTC brands demand mailers that combine durability for last-mile delivery, cost efficiency for high-volume shipments, and enhanced unboxing experiences for consumers. Custom-printed mailers are increasingly used as a branding tool, reinforcing customer loyalty and reducing reliance on secondary packaging. This dominance is further accelerated by global e-commerce penetration, with growth in markets like Asia-Pacific and Latin America creating sustained demand for high-performing and sustainable packaging formats. The overwhelming influence of e-commerce ensures that mailer innovation—whether in recycled content, automation compatibility, or customer-centric design—is directly shaped by the needs of this channel.

United States Mailer Packaging Market Driven by EPR Regulations and Smart Packaging Innovations

The U.S. mailer packaging industry is heavily influenced by California’s Extended Producer Responsibility (EPR) laws, particularly Senate Bill 54, which mandates that packaging must be recyclable or compostable. This fragmented regulatory environment is pushing manufacturers to adopt sustainable and eco-friendly mailer solutions. Technological advancements, including smart packaging, QR codes, and RFID integration, are enhancing supply chain visibility and providing real-time tracking, improving both logistics and the unboxing experience.

Corporate investments highlight this sustainability trend, exemplified by Georgia-Pacific’s new facility producing recyclable paper-padded mailers. Key applications remain in the e-commerce sector, especially for apparel, books, and non-fragile electronics. The rise of direct-to-consumer (DTC) brands is driving demand for customized, branded, and lightweight mailers that combine durability with sustainability. Pregis’ EverTec mailer, independently certified for recyclability, underscores the growing focus on eco-conscious packaging in e-commerce.

Germany’s Mailer Packaging Market Excels in Circular Economy and Plastic-Free Solutions

Germany’s mailer packaging market operates under the German Packaging Act (VerpackG) and EU regulations, incentivizing the adoption of recyclable materials and efficient recycling systems. Technological innovations are spearheaded by companies like Mondi, which showcases sustainable, plastic-free mailer designs, integrating kraft paper and fluted inserts for fully recyclable solutions.

Germany leads in circular economy initiatives, collaborating with global e-commerce players like Amazon to introduce eco-friendly protective mailers. Key applications include e-commerce, healthcare, and personal care, where consumers increasingly prefer sustainable, branded packaging. The country’s emphasis on high-performance, recyclable mailers positions Germany as a benchmark for sustainable European mailer packaging solutions.

China Mailer Packaging Market Expands Through Government Green Policies and Domestic Production

China’s mailer packaging industry is driven by governmental initiatives such as the dual carbon goal and the Action Plan for Promoting Large-Scale Equipment Updates, promoting the adoption of sustainable materials and reduced excessive packaging. Regulatory reforms set standards for materials used in insulated mailers for food and pharmaceuticals, ensuring safety and compliance.

Technological advancements in automation and AI improve production efficiency, while domestic manufacturing expansion addresses the growing demand for high-quality, circular mailer products. The booming e-commerce and logistics sectors fuel market growth, highlighting a rising trend for durable, sustainable, and technologically advanced mailer packaging solutions.

India Mailer Packaging Market Accelerates With QR Code Mandates and E-Commerce Growth

India’s mailer packaging market is seeing strong growth driven by government initiatives, including updated CPCB labeling and QR code guidelines for plastic packaging effective from July 2025. This move enhances traceability, recycling, and waste management, creating opportunities for sustainable packaging adoption.

Technological advancements focus on bio-based plastics and recyclable materials, while corporate investments are rising to meet e-commerce and urban sector demand. Key applications include e-commerce and manufacturing, where the growth of online transactions and the formalization of QR code regulations are boosting the adoption of modern, high-performance, and sustainable mailer solutions.

United Kingdom Mailer Packaging Market Shifts Toward Compostable and Brand-Oriented Solutions

The UK market is shaped by Extended Producer Responsibility (EPR) and the Plastic Packaging Tax, driving the adoption of recycled and compostable mailers. Innovations include home-compostable, paper-based, and seaweed-based mailers, with startups like OCEANIUM leading in sustainable material development.

Corporate initiatives, including Mondi’s partnership with Amazon, reflect the growing focus on eco-friendly and branded mailer solutions. Demand is particularly strong in e-commerce, where consumers increasingly prefer sustainable delivery packaging to enhance brand image and comply with environmental policies.

Brazil Mailer Packaging Market Grows Through Bio-Based Materials and E-Commerce Expansion

Brazil’s mailer packaging market is supported by the National Solid Waste Policy, encouraging sustainable packaging practices. Technological advancements include the development of biodegradable, recyclable, and compostable mailers, with innovations like bio-based polyethylene from sugarcane reducing fossil fuel dependence and carbon footprint.

Corporate investments from both domestic and international players are strengthening local manufacturing capabilities, reducing reliance on imports. Key applications include e-commerce, food and beverage, and agricultural sectors, where growing online retail and packaged goods demand are driving the adoption of modern, eco-friendly mailer packaging solutions.

Mailer Packaging Market Report Scope

Mailer Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$36.1 Billion

|

|

Market Size (2034)

|

$175.4 Billion

|

|

Market Growth Rate

|

19.2%

|

|

Segments

|

By Product Type (Cushioned Mailers, Non-Cushioned Mailers, Insulated Mailers), By Material (Paper, Plastic, Other Materials), By End-User (E-commerce, Shipping & Logistics, Manufacturing & Warehousing, Food & Beverage, Healthcare, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group, Mondi plc, International Paper, WestRock Company, Sealed Air Corporation, ProAmpac, Pregis LLC, DS Smith Plc, Rengo Co., Ltd., Georgia-Pacific LLC, Sonoco Products Company, Amcor plc, Greif, Inc., Huhtamaki Oyj, Shurtape Technologies, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mailer Packaging Market Segmentation

By Product Type

- Cushioned Mailers

- Non-Cushioned Mailers

- Insulated Mailers

By Material

- Paper

- Plastic

- Other Materials

By End-User

- E-commerce

- Shipping & Logistics

- Manufacturing & Warehousing

- Food & Beverage

- Healthcare

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Mailer Packaging Market

- Smurfit Kappa Group

- Mondi plc

- International Paper

- WestRock Company

- Sealed Air Corporation

- ProAmpac

- Pregis LLC

- DS Smith Plc

- Rengo Co., Ltd.

- Georgia-Pacific LLC

- Sonoco Products Company

- Amcor plc

- Greif, Inc.

- Huhtamaki Oyj

- Shurtape Technologies, LLC

* List Not Exhaustive

Methodology

The research methodology for the global Mailer Packaging market combines rigorous primary and secondary research techniques to provide comprehensive insights tailored for industry professionals. Primary research involved structured interviews and consultations with packaging manufacturers, supply chain managers, sustainability officers, e-commerce logistics experts, and retail brand strategists to capture real-time perspectives on material innovations, smart packaging, automation-driven solutions, and sustainability initiatives. Secondary research included an exhaustive review of company annual reports, government regulations, trade publications, press releases, and market intelligence reports to validate industry trends, regional developments, and growth projections. Market sizing, CAGR calculations, and segment forecasts were derived using top-down and bottom-up approaches across product types, materials, and end-user industries, with special emphasis on the rising adoption of paper-based and fiber-based mailers, cushioned mailers dominance, smart packaging technologies like RFID and QR codes, and reusable/compostable material innovations. This methodology ensures that USDAnalytics delivers precise, actionable, and data-driven insights into the evolving mailer packaging market, highlighting growth drivers, technological innovation, and sustainability-led opportunities across key global regions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.