Market Overview: Rising Demand for Corrugated and Sustainable Secondary Packaging

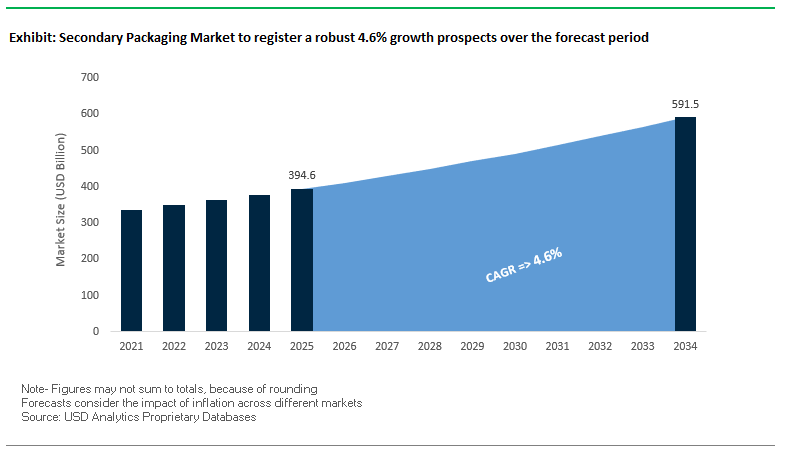

The global secondary packaging market is projected to reach USD 394.6 billion in 2025 and expand to USD 591.5 billion by 2034, growing at a CAGR of 4.6%. This growth is propelled by the increasing demand from e-commerce, FMCG, food & beverage, and pharmaceutical sectors, where packaging plays a critical role in product safety, branding, and logistics efficiency. For industry professionals, the key question is not whether to invest in secondary packaging but how to adopt solutions that balance cost-efficiency, automation, and sustainability.

Corrugated boxes remain the dominant material type, valued for durability, recyclability, and cost-effectiveness. Automation is reshaping the industry as robotics on secondary packaging lines allow faster throughput, labor savings, and consistency. The e-commerce sector continues to push demand for right-sized shippers, protective void-fill reduction, and digitally printed packaging for branding. Moreover, the circular economy is increasingly central, with returnable transit packaging (RTP) gaining traction in retail and automotive supply chains.

Key Insights for Industry Buyers and Professionals:

- Corrugated leads: Cost-effective, versatile, and recyclable, corrugated solutions dominate.

- Automation adoption: Robotics widely deployed since 2024 to improve throughput and reduce costs.

- E-commerce expansion: Growth of online retail fuels demand for protective, branded packaging.

- Sustainability in focus: Returnable transit packaging (RTP) is reshaping logistics models.

Market Analysis: Industry Developments Driving Structural Transformation

The secondary packaging industry is undergoing consolidation, global expansions, and sustainability-driven innovation, with multiple landmark deals reshaping competition.

In August 2025, the merger of Smurfit Kappa and Westrock created Smurfit Westrock, with 17 manufacturing sites and 30 distribution centers, forming one of the largest players in sustainable paper-based packaging. Earlier in July 2025, Packaging Corporation of America (PCA) announced the purchase of Greif’s containerboard business for USD 1.8 billion, a move consolidating its footprint in containerboard supply.

Meanwhile, International Paper’s acquisition of DS Smith received EU clearance in June 2025 and was finalized in January 2025 for over USD 7 billion, reshaping the European and global paper packaging market. Similarly, Amcor’s acquisition of Berry Global in April 2025 for USD 8.4 billion significantly boosted its portfolio in both flexible and rigid packaging formats. On the innovation front, Ranpak partnered with Thalia in May 2025 to deploy 12 automated packaging systems, highlighting the integration of digital and mechanical automation.

Sustainability disclosures are also becoming critical. Graphic Packaging Holding Company’s July 2025 “Toward a Better Future” report reinforced its commitment to transitioning toward recyclable and compostable packaging, setting a benchmark for peers. Strategic investments also continue at the regional level, as WestRock announced in January 2024 a new corrugated box plant in Wisconsin to meet growing U.S. demand.

Secondary Packaging Market: Trends and Opportunities Transforming Sustainable Logistics

The Rapid Integration of Automated Right-Sizing and Dimensioning Technologies

The secondary packaging market is being revolutionized by the adoption of AI-powered automation and right-sizing systems that generate custom packaging tailored to each product or order. This transition away from standardized box sizes delivers significant sustainability and cost benefits. For example, Helly Hansen’s adoption of automated right-sizing solutions enabled the company to triple throughput, reduce labor costs, and eliminate excessive use of corrugated material. Right-sized packaging minimizes dimensional weight shipping charges, which are a key cost driver for e-commerce and CPG companies, while also reducing storage and handling inefficiencies.

Material savings are another major advantage. Packaging experts report that corrugated usage can be reduced by nearly a third when automated right-sizing is implemented at scale. This aligns with consumer and regulatory expectations. Surveys cited by supply chain professionals in 2025 indicate that 80% of consumers prefer corrugated materials with less void fill, echoing the EU’s packaging regulations, which require companies to minimize empty space ratios and restrict the use of unnecessary filler. This combination of cost efficiency, consumer satisfaction, and compliance is making automated right-sizing a strategic imperative for global logistics operations.

The Strategic Shift from Plastic to Paper-Based Tertiary and Secondary Packaging

A second defining trend is the accelerated replacement of plastic in secondary and tertiary packaging with engineered paper-based alternatives. The shift is strongly influenced by Extended Producer Responsibility (EPR) regulations and fiscal measures such as Spain’s €0.45/kg plastic tax (2023) and Italy’s planned implementation of similar legislation in 2026. These fiscal pressures, combined with increasing EPR fees, are making plastic shrink wraps, stretch films, and laminated solutions less economically viable compared to recyclable paper-based alternatives.

Leading corporations are spearheading the move away from plastics. Amazon’s elimination of plastic mailers is part of a broader corporate strategy to decarbonize its packaging footprint. On the innovation front, companies like Ranpak are introducing paper-based thermal liners capable of keeping cold-chain shipments stable for up to 48 hours while maintaining recyclability. This convergence of regulatory drivers, brand commitments, and technological breakthroughs is setting the stage for a large-scale transition to paper-based secondary packaging as the default solution for logistics, e-commerce, and retail supply chains.

Development of High-Performance, Recyclable Water-Based Barrier Coatings

A significant growth opportunity lies in the development of bio-based and water-based barrier coatings that make paper packaging more functional without sacrificing recyclability. Traditional polyethylene (PE) liners and laminated films provide protection but disrupt fiber recovery during recycling. Companies like H.B. Fuller are advancing water-based functional coatings that improve fiber yield during repulping, directly addressing recycling inefficiencies.

Barrier technologies are also evolving into application-specific solutions. For example, taco shell packaging requires coatings with low moisture vapor transmission rates (MVTR) to prevent sogginess, while pet food bags with high oil content require advanced grease resistance. Importantly, these coatings are free from harmful substances such as BPA and phthalates, making them safer for consumers and aligned with global chemical reduction goals. As brands continue replacing plastic barriers with water-based alternatives, the market is poised for rapid adoption in segments like foodservice, retail-ready packaging, and consumer goods.

Embedded Digitalization for Smart Logistics and Circular Economy Tracking

Secondary packaging is increasingly doubling as a digital information platform, creating opportunities for smart logistics, recycling optimization, and consumer engagement. Initiatives like HolyGrail 2.0 have demonstrated that digital watermarks embedded in corrugated cases enable 99% accurate sorting of packaging waste, a breakthrough for separating food-grade and non-food-grade recycling streams at scale. This directly supports the circular economy transition by improving the quality of recycled materials.

On the logistics side, RFID-enabled packaging provides real-time supply chain visibility without requiring manual scanning, offering major efficiencies in global distribution networks. This technology is particularly valuable for industries with high compliance needs, such as pharmaceuticals and food & beverage. Additionally, digital identifiers like QR codes create a new channel for direct-to-consumer engagement, allowing brands to share detailed product information, sustainability certifications, and even user tutorials. By embedding intelligence into secondary packaging, companies are moving beyond protection and containment to unlock end-to-end transparency, efficiency, and customer loyalty.

Competitive Landscape: Key Players in the Global Secondary Packaging Market

The global secondary packaging market is highly competitive, shaped by mega-mergers, automation investments, and strong commitments to sustainability. Leading companies are expanding through acquisitions, optimizing global networks, and introducing eco-friendly alternatives to single-use plastics.

Smurfit Westrock: New Global Powerhouse in Sustainable Paper Packaging

Formed in August 2025 through the merger of Smurfit Kappa and Westrock, Smurfit Westrock is now one of the largest global players in fiber-based packaging. With 17 plants and 30 distribution centers, it offers corrugated board, folding cartons, and retail-ready packaging. Its scale, backed by 100,000 employees across 40 countries, provides unmatched global reach. By combining networks and expertise, the company is positioned as a leader in sustainable, paper-based secondary packaging.

Graphic Packaging Holding Company: Innovating with Paper-Based Alternatives

Graphic Packaging specializes in folding cartons, beverage carriers, and customized secondary solutions. Its innovations include KeelClip™, replacing plastic rings in beverage multipacks, and PaperSeal™ trays, offering a recyclable alternative to plastic. The company’s Vision 2025 program, supported by major investment in its Waco, Texas facility, underscores its sustainability leadership. Its vertically integrated supply chain gives it control from recycled fiber to finished products, ensuring efficiency and innovation.

International Paper: Expanding Global Presence Through DS Smith Acquisition

International Paper is a global leader in containerboard and corrugated packaging, and its January 2025 acquisition of DS Smith expanded its European reach. The company’s USD 250 million investment in its Riverdale, Alabama mill conversion in August 2025 further strengthens its containerboard capacity. Its expertise in paper science and vast global manufacturing footprint make it a cornerstone in delivering durable and recyclable secondary packaging.

Amcor plc: Strengthening Flexible and Rigid Secondary Packaging Offerings

Amcor operates across rigid and flexible formats, with secondary packaging solutions serving food, beverage, and healthcare industries. The USD 8.4 billion acquisition of Berry Global in April 2025 expanded its plastic packaging portfolio, positioning Amcor as a broader solutions provider. The company remains committed to 100% recyclable or compostable packaging by 2025, aligning with brand-owner sustainability goals. Its focus on both function and branding gives it a strong edge in consumer-facing packaging markets.

DS Smith Plc: Integrating with International Paper for Circular Growth

Previously a leader in fiber-based packaging, DS Smith is now integrated into International Paper following the January 2025 merger. The company was known for its “Box to Box in 14 days” model, emphasizing rapid recycling and circularity. Its “Now and Next” strategy focused on replacing problematic plastics and lowering carbon emissions, positioning DS Smith as a critical part of International Paper’s sustainability roadmap. Its expertise in retail-ready displays and corrugated innovation continues to influence the market.

Secondary Packaging Market Share Insights

Corrugated Boxes Dominate Secondary Packaging Market Share by Product Type

Corrugated boxes hold a commanding 40% share of the secondary packaging market in 2025, reflecting their position as the backbone of global shipping, retail, and e-commerce logistics. Their scalability, durability, cost-efficiency, and high recyclability make them indispensable for industries ranging from consumer goods to industrial shipments. Folding cartons and set-up boxes account for 18%, driven by their dual role in protection and retail-ready branding for food, cosmetics, and electronics. Flexible films and bags, shrink wraps, trays, and specialty tubes collectively address multi-packing, product bundling, and premium protective needs. With sustainability mandates and automation driving innovation in formats and materials, corrugated boxes continue to dominate while adjacent categories secure relevance in specialized roles. This segmentation demonstrates how corrugated boxes remain the uncontested leader, with films, wraps, and trays supporting evolving e-commerce and retail supply chains.

Food & Beverage Leads Secondary Packaging Market Share by End-Use Industry

The food and beverage sector represents 30% of the secondary packaging market in 2025, making it the single largest end-use industry. Its dominance is anchored in the constant, non-discretionary demand for packaged foods and drinks, requiring corrugated shipping cases, shrink wrap for multi-packs, and trays for fresh produce and meat. E-commerce and logistics follow closely at 28%, reshaping secondary packaging through the need for right-sized corrugated boxes, flexible mailers, and automation-driven fulfillment packaging solutions. Industrial and commercial applications provide stable demand for durable, heavy-duty solutions, while pharmaceuticals and medical segments prioritize tamper-evidence, serialization, and compliance for sensitive goods. Cosmetics and personal care further strengthen demand through premium printed boxes and protective inserts that elevate consumer experience during unboxing. This segmentation highlights how food and beverage secures consistent demand, while e-commerce accelerates innovation and medical sectors drive high-value compliance-based growth.

United States: E-Commerce Expansion and Sustainability Transforming Secondary Packaging

The U.S. secondary packaging market is heavily influenced by the exponential rise of e-commerce, where corrugated mailers, folding cartons, and protective secondary packaging are essential for safeguarding goods during transit while enhancing the customer’s unboxing experience. Lightweight yet durable solutions are in high demand, particularly as online shopping volumes continue to soar. At the same time, sustainability regulations are reshaping the industry. California’s SB-54 Extended Producer Responsibility (EPR) law and mandates for PFAS-free materials are pushing brands and manufacturers to adopt eco-friendly and compliant packaging solutions across nationwide supply chains. Technological advancements such as automated production lines and digital printing have further enabled greater customization and short-run flexibility, catering to niche brands and personalized consumer preferences. Additionally, investments in reusability are on the rise, with players like Greif, Inc. expanding their stake in Centurion Container LLC to strengthen their reusable packaging portfolio. These combined forces are positioning the U.S. as a global leader in sustainable, tech-enabled secondary packaging innovation.

Germany: Regulatory Compliance and Circular Economy Shaping Paper-Based Secondary Packaging

Germany’s secondary packaging market is deeply influenced by one of the strictest regulatory landscapes in Europe, led by the German Packaging Act (VerpackG) and the EU’s new Packaging and Packaging Waste Regulation (PPWR). The introduction of the Single-Use Plastics levy in 2024 has further heightened the urgency for recyclable and eco-friendly secondary packaging materials. As a leader in the circular economy, Germany is fostering collaboration between manufacturers and end-users to design packaging with higher recycled content that aligns with EU environmental targets. Innovation is particularly strong in paper-based solutions, with companies like Mondi Group introducing recyclable trays with barrier layers that replace plastic in fresh food packaging a key development that meets both consumer sustainability preferences and regulatory compliance. With its strong industrial base and innovation-driven ecosystem, Germany continues to be at the forefront of sustainable secondary packaging solutions in Europe.

China: Industrial Expansion and Sustainability Goals Driving Secondary Packaging Demand

China’s secondary packaging market is expanding rapidly, supported by its massive industrial base, e-commerce boom, and logistics sector growth. Domestic paper production capacity grew by 10% in 2024 compared to the previous year—the fastest growth in five years—reflecting the rising demand for corrugated boxes and folding cartons in the domestic market. The government’s “dual carbon” policy, targeting carbon peak and carbon neutrality, is a central force driving sustainability initiatives, particularly in the express delivery sector. New policies to curb over-packaging are prompting manufacturers to adopt lightweight and efficient secondary packaging solutions. At the same time, advancements in automation, AI, and robotics are being leveraged by Chinese manufacturers to boost efficiency and meet the evolving needs of automated logistics. With a strong export market and rising domestic consumption, China is set to remain one of the most influential players in the global secondary packaging industry.

India: E-Commerce Growth and Recycling Capacity Expansion Fueling Secondary Packaging Market

India’s secondary packaging market is evolving rapidly, driven by regulatory action, e-commerce expansion, and technological progress. The Plastic Waste Management (Amendment) Rules are accelerating the shift toward sustainable, reusable packaging and phasing out single-use plastics. The e-commerce boom—especially in online grocery and food delivery—has significantly boosted demand for water-resistant, durable corrugated packaging. Government initiatives such as the Integrated Cold Chain and Value Addition Infrastructure are also stimulating demand for insulated secondary packaging, particularly in the pharmaceutical and perishable food sectors. On the innovation front, over INR 10,000 crore has been invested since 2022 to upgrade recycling technologies, including wash lines, extruders, and decontamination units, enhancing the country’s recycling capacity. With its dynamic regulatory landscape and rising consumer demand, India is poised to be a high-growth market for sustainable secondary packaging solutions.

Brazil: Circular Economy and Food Packaging Innovation Redefining Secondary Packaging

Brazil’s secondary packaging market is being reshaped by stringent regulations against single-use plastics and the implementation of the National Solid Waste Policy, which promotes a circular economy. The emphasis on recycling, reuse, and waste reduction has led companies to adopt closed-loop systems that recycle post-consumer plastics into new packaging. Innovation in food packaging is particularly noteworthy, with technological progress in coatings enabling paperboard to replace laminated plastic in takeaway and food service applications, aligning with consumer demand for sustainable alternatives. The personal care and hygiene markets are also thriving, driving strong demand for hygienic and convenient secondary packaging formats. With regulatory pressure, industry innovation, and consumer demand working in tandem, Brazil is rapidly emerging as a sustainability-driven hub for secondary packaging solutions.

Japan: Bio-Based Innovation and Recycling Efficiency Elevating Secondary Packaging Market

Japan’s secondary packaging industry is advancing through a combination of bio-based innovation, advanced recycling systems, and functional design improvements. The shift toward bio-polypropylene (bio-PP) is gaining momentum through collaborations between LyondellBasell, Shiseido, Futamura Chemical, and Iwatani, supporting the country’s ambitious environmental targets for 2030 and 2050. Japan also benefits from one of the highest waste plastic collection and recycling rates in the world, reinforced by the Plastic Resource Circulation Act, which mandates circular packaging solutions. On the innovation front, global packaging leader Amcor has launched its “Transparence” program in Japan, aiming to reduce secondary packaging use and ensure that all products are recyclable or reusable by 2025. These developments highlight Japan’s role as a global frontrunner in sustainable, high-performance secondary packaging, blending material science with regulatory compliance and consumer-focused functionality.

Secondary Packaging Market Report Scope

Secondary Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$394.6 Billion

|

|

Market Size (2034)

|

$591.5 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Material Type (Paper & Paperboard, Plastics, Glass, Metal, Other Materials), By Product Type (Boxes & Cartons, Trays & Wrappers, Films & Bags, Shrink Wraps, Corrugated Boxes, Tubes & Containers, Other Products), By End-Use Industry (Food & Beverage, Pharmaceuticals & Medical, Cosmetics & Personal Care, E-commerce & Logistics, Industrial & Commercial, Other End-use Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Westrock (formerly Smurfit Kappa and WestRock), International Paper, DS Smith Plc, Mondi Group, Amcor plc, Graphic Packaging Holding Company, Sonoco Products Company, AptarGroup, Inc., Sealed Air Corporation, Huhtamäki Oyj, Rengo Co., Ltd., AR Packaging, Oji Holdings Corporation, Ball Corporation, Sidel

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Secondary Packaging Market Segmentation

By Material Type

- Paper & Paperboard

- Plastics

- Glass

- Metal

- Other Materials

By Product Type

- Boxes & Cartons

- Trays & Wrappers

- Films & Bags

- Shrink Wraps

- Corrugated Boxes

- Tubes & Containers

- Other Products

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Medical

- Cosmetics & Personal Care

- E-commerce & Logistics

- Industrial & Commercial

- Other End-use Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Secondary Packaging Market

- Smurfit Westrock (formerly Smurfit Kappa and WestRock)

- International Paper

- DS Smith Plc

- Mondi Group

- Amcor plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- AptarGroup, Inc.

- Sealed Air Corporation

- Huhtamäki Oyj

- Rengo Co., Ltd.

- AR Packaging

- Oji Holdings Corporation

- Ball Corporation

- Sidel

*List not Exhaustive

Research Coverage

This report by USDAnalytics investigates the rapidly evolving global secondary packaging market, examining technological breakthroughs, material innovations, and strategic industry developments that are shaping the future of sustainable logistics. The analysis reviews historical market performance from 2021 to 2024 and provides detailed forecasts through 2034, offering professionals actionable insights on market dynamics, adoption of automation, and sustainable packaging trends. The report highlights critical innovations, including automated right-sizing, AI-powered dimensioning, paper-based barrier solutions, and embedded digitalization for smart logistics and circular economy initiatives. It evaluates the competitive landscape, analyzing over 15 key companies including Smurfit Westrock, International Paper, DS Smith Plc, Amcor plc, and Graphic Packaging Holding Company, emphasizing merger activity, regional expansions, and sustainability-focused product launches. Designed as an essential resource for packaging professionals, supply chain executives, and strategic investors, this report equips readers with comprehensive intelligence on market opportunities, regulatory impact, and material performance, enabling informed decision-making in a sector experiencing rapid transformation due to e-commerce growth, environmental mandates, and consumer-driven sustainability demands.

Scope Highlights:

- Segmentation: By Material Type (Paper & Paperboard, Plastics, Glass, Metal, Other Materials); By Product Type (Boxes & Cartons, Trays & Wrappers, Films & Bags, Shrink Wraps, Corrugated Boxes, Tubes & Containers, Other Products); By End-Use Industry (Food & Beverage, Pharmaceuticals & Medical, Cosmetics & Personal Care, E-commerce & Logistics, Industrial & Commercial, Other End-use Industries).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Temporal Coverage: Historic data from 2021–2024; forecast data from 2025–2034.

- Company Profiles: In-depth analysis of 15+ leading players, including mergers, acquisitions, and product innovations.

Methodology

The research methodology integrates both primary and secondary data collection techniques to ensure comprehensive market coverage. Primary research involved consultations with senior executives, packaging engineers, and industry consultants from leading corporations to obtain insights on product innovations, automation adoption, sustainability practices, and regional dynamics. Secondary research comprised company reports, regulatory filings, trade journals, and industry publications, ensuring validation of market trends and competitive intelligence. Quantitative analysis was conducted using historical market data from 2021–2024, with forecasting models developed using CAGR-based projections and scenario analysis through 2034. Market sizing, share analysis, and segmentation assessments were cross-verified through triangulation, ensuring accuracy and consistency. Special attention was given to emerging technologies such as AI-powered right-sizing, recyclable barrier coatings, and digitalized logistics, providing a robust framework to evaluate both short-term opportunities and long-term strategic trends. The methodology ensures the report is a reliable tool for industry professionals seeking actionable insights on competitive positioning, investment priorities, and sustainability-led innovations in secondary packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.