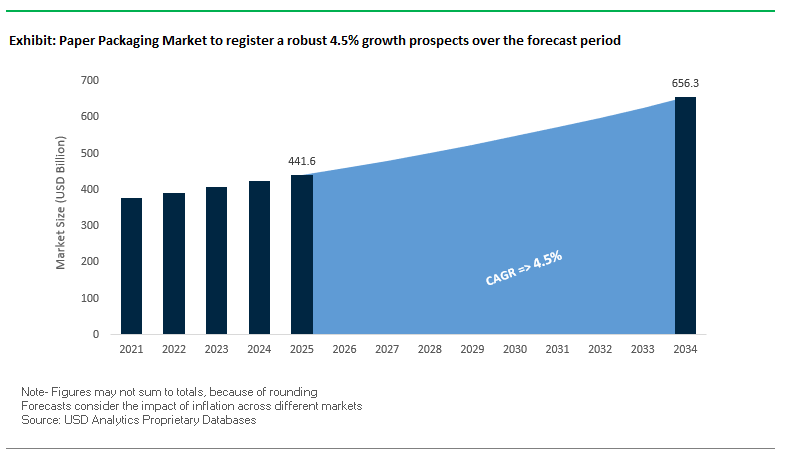

Paper Packaging Market Set to Grow from $441.6 Billion in 2025 to $656.3 Billion by 2034 as E-Commerce and Sustainability Drive Demand

The Global Paper Packaging Market is projected to grow from $441.6 billion in 2025 to $656.3 billion by 2034, at a CAGR of 4.5%, fueled by the explosive growth of e-commerce, D2C channels, and the global push for sustainable packaging solutions. Paper packaging, encompassing corrugated boxes, folding cartons, flexible paper bags, and liquid packaging, is a critical component in protecting, transporting, and marketing products across industries such as food & beverages, e-commerce, personal care, and industrial goods.

Key Insights for Industry Professionals:

- E-Commerce Surge Fuels Packaging Innovation: The shift to online shopping and parcel delivery demands lightweight, robust, and customizable boxes that ensure product safety and enhance brand experience.

- Sustainability Shapes Material Adoption: Growing preference for renewable, recyclable, and compostable fibers is driven by regulatory mandates, corporate sustainability goals, and consumer demand for eco-friendly solutions.

- Enhanced Functionality and Printability are Critical: Advanced coatings, moisture and grease resistance, and superior print surfaces allow brands to maintain aesthetics while protecting products.

- Optimizing Packaging for Automation: Lightweight boards and innovative structures reduce material usage and transportation costs while performing efficiently on high-speed automated packing lines.

- Transition from Plastic to Fiber-Based Packaging: Companies are increasingly replacing plastic packaging with high-performance, fiber-based alternatives, supporting circular economy initiatives.

The industry’s growth trajectory is defined by innovation, sustainability, and supply chain optimization, making it a strategic priority for manufacturers, distributors, and industrial buyers.

Recent Developments Highlight the Industry’s Focus on Sustainability, Automation, and Strategic Consolidation

The Paper Packaging Industry is witnessing significant transformation driven by technological advancements, eco-friendly innovations, and market consolidation. In August 2025, Graphic Packaging International expanded its PaperSeal® Pressed MAP Tray portfolio, showcasing the shift toward fiber-based alternatives to plastic trays. During the same month, Mondi plc launched Ad/Vantage Smooth Brown Semi Extensible, a new paper grade tailored for demanding packaging applications, demonstrating a focus on performance and versatility.

August 2025 also saw International Paper invest $250 million at its Riverdale mill in Alabama to convert a machine for containerboard production, while closing four Georgia facilities, reflecting strategic optimization of operations. In July 2025, Stora Enso received the Red Dot Design Award for its recyclable gift packaging, emphasizing the growing importance of design-driven sustainable solutions.

Key consolidation moves include April 2025, when International Paper completed its $9.9 billion acquisition of DS Smith, strengthening its European market presence, and November 2024, when Smurfit Kappa acquired WestRock, forming Smurfit WestRock, a leading player in corrugated packaging and sacks. Earlier in October 2024, Graphic Packaging restructured its paperboard pricing strategy to gain greater control over pricing. Other functional innovations include Billerud’s heat-sealable, fossil-free paper (March 2025), reflecting the industry’s focus on low-carbon, recyclable solutions.

Trends and Opportunities Defining the Growth of the Paper Packaging Market

Unprecedented Demand Surge from Single-Use Plastic Legislation

One of the most transformative forces shaping the paper packaging market is global legislation targeting single-use plastics. The European Union’s Packaging and Packaging Waste Regulation (PPWR), coupled with the plastics tax introduced in 2021, imposes penalties on non-recycled plastic packaging, making paper-based solutions a cost-effective alternative. This regulatory framework is not isolated to Europe; India’s July 2022 ban on a wide range of single-use plastic items such as straws, cutlery, and trays has forced an immediate transition to paper and paperboard substitutes. The regulatory-driven shift is not only altering supply chains but also spurring direct corporate action. Amazon, for example, has replaced 99.7% of its plastic padded mailers with curbside-recyclable paper packaging, while JDE Peet’s announced plans to roll out paper pouches for coffee. Similarly, Nissin Foods USA has transitioned its Cup Noodles into paper cups incorporating 40% recycled content. These corporate moves, driven by compliance and ESG objectives, are accelerating market demand. To meet this surge, manufacturers are ramping up capacity, as evidenced by a $21 million Indian investment in 2025 to upgrade a paper machine for an additional 60,000 tons of output annually. This synergy of legislation, corporate responsibility, and capital expenditure is setting the stage for exponential growth in paper packaging.

Strategic Adoption of Advanced, Recyclable Barrier Coatings

Beyond demand growth, innovation in barrier coatings is strategically expanding the scope of paper packaging applications. Traditionally, paperboard has been limited by its inability to resist moisture, grease, or oxygen infiltration. However, new water-based and bio-based coatings now provide functional performance while remaining compatible with recycling streams. Mineral-rich coatings are emerging as direct replacements for plastic, acting like clay during pulping and ensuring full fiber recovery. Recent launches, such as a barrier paper for flexible food packaging introduced in July 2025, use low-aluminum content to deliver high oxygen-barrier performance while remaining recyclable. This is allowing paper to move into applications such as snacks, coffee, and seasonings—segments historically dominated by plastics. Similarly, innovations in ready-meal packaging have reduced plastic usage by 25% while maintaining tray strength and performance. By replacing multi-material laminates that are difficult to recycle, these next-generation coatings are positioning paper packaging as both a sustainable and high-performance solution.

Commercialization of Molded Pulp for Expanded Applications

Molded pulp, once confined to egg cartons and basic trays, is emerging as a fast-growing segment in the global paper packaging market. Its versatility and ability to replace petroleum-based foams make it attractive for high-value applications such as electronics, where custom-molded pulp inserts now protect smartphones, laptops, and tablets. This not only provides superior shock absorption but also elevates the consumer experience with premium eco-friendly unboxing. Molded pulp clamshells are also gaining adoption in the food and consumer goods sectors as sustainable alternatives to plastic clamshells. Manufacturers are investing in refining and pressing technologies that deliver smoother surfaces and detailed finishes, making molded pulp suitable for high-end cosmetics packaging where aesthetics are critical. This evolution highlights molded pulp’s transformation from a simple protective solution to a multi-functional, brand-enhancing packaging material.

Integration of Digital Watermarking for Intelligent Recycling

The adoption of digital watermarking represents a groundbreaking opportunity for the future of paper packaging. Trials under the HolyGrail 2.0 initiative, conducted in Germany from August to December 2024, proved that industrial-scale waste sorting systems equipped with this technology can identify and separate digitally watermarked packaging with over 90% accuracy. This high-resolution sorting enables SKU-level differentiation, allowing recyclers to distinguish between food-grade and non-food-grade packaging or between different barrier coatings. Such precision not only creates clean, high-quality recycled paper streams but also ensures compliance with increasingly stringent recycled content regulations. For brands, digital watermarking provides a verifiable tracking mechanism that supports Extended Producer Responsibility (EPR) requirements and broader sustainability commitments. By improving transparency and material recovery, this innovation bridges the gap between circular economy ambitions and practical recycling outcomes, making it a critical opportunity for the industry.

Key Industry Players Are Shaping the Future of Sustainable and High-Performance Paper Packaging

The competitive landscape is dominated by companies leveraging materials expertise, global scale, and innovative packaging design to provide high-performance, sustainable solutions across industries.

Smurfit Westrock plc Combines Scale and Sustainability to Lead Global Paper Packaging

Smurfit Westrock, created from the Smurfit Kappa and WestRock merger, operates 500+ converting operations and 62 mills in 40 countries, ensuring a consistent supply of high-performance corrugated packaging. In August 2025, the company reported Q2 results and announced facility optimizations in the U.S. and Germany. Its portfolio includes corrugated containers, folding cartons, and specialty packaging for food, e-commerce, and industrial goods, with a strong commitment to circular economy principles and renewable materials.

International Paper Company Streamlines Operations to Focus on Sustainable Packaging Leadership

International Paper is a global leader in fiber-based packaging and pulp, with extensive mills and converting plants worldwide. In August 2025, it sold its Global Cellulose Fibers business for $1.5 billion to concentrate on core sustainable packaging, while investing $250 million in Riverdale mill for containerboard production. The company offers corrugated boxes, containerboard, and bleached paperboard, widely used in industrial, food, and consumer packaging, with a focus on cost efficiency, customer experience, and sustainability.

Graphic Packaging International, LLC Pioneers Replacement of Plastic with Fiber-Based Solutions

Graphic Packaging specializes in consumer packaging, cartons, and paperboard, emphasizing vertical integration and design-driven solutions. In August 2025, the company replaced approximately 1 billion plastic packages with paperboard alternatives, advancing sustainability initiatives. Its offerings include folding cartons, flexible packaging, and paperboard cups for food, beverage, and foodservice applications, aligned with its Vision 2030 plan for circularity and operational excellence.

Mondi Group Expands Barrier Paper Innovations to Meet Growing Demand for Eco-Friendly Packaging

Mondi provides both paper- and plastic-based packaging solutions, enabling customers to pursue sustainable transitions. In August 2025, it ramped production of FunctionalBarrier Paper Ultimate, and in June 2025 launched re/cycle PaperPlus Bag Advanced for humidity-sensitive products. Its portfolio includes corrugated packaging, sack kraft paper, and flexible packaging, emphasizing high-performance, recyclable, and plastic-replacing materials under its MAP2030 sustainability framework.

Stora Enso Oyj Leads Renewable Packaging Innovation Through Investment in High-Performance Paperboard

Stora Enso focuses on renewable packaging, biomaterials, and wooden construction. In August 2025, it inaugurated Europe’s most modern consumer board production line in Finland, boosting capacity for sustainable packaging. The company exceeded its 2030 emission reduction targets, achieving a 53% reduction by 2024, while offering folding boxboard, liquid packaging board, and containerboard for consumer and industrial applications.

Billerud AB Develops High-Performance, Sustainable Paperboard Solutions for Diverse Applications

Billerud is a leader in high-strength, durable, and printable paper materials for packaging. Its investments in Michigan mills advance innovation and sustainability in North America, complemented by a Gold EcoVadis rating in November 2024. Billerud offers fluting, liner, and cartonboard for industrial bags, liquid packaging, and consumer goods, with a focus on low-carbon, high-performance packaging materials.

Paper Packaging Market Share Insights, 2025-2034

Corrugated Boxes Dominate Market Share by Product Type in the Paper Packaging Industry

Corrugated boxes represent 58% of the global paper packaging market, underscoring their role as the cornerstone of global e-commerce and logistics systems. Their unmatched strength-to-weight ratio, stackability, and adaptability make them the preferred solution for shipping and distribution across virtually all industries. Technological advances such as lightweighting (right-weighting), RFID-enabled smart packaging, and high-graphic digital printability have further entrenched corrugated’s dominance by aligning with supply chain efficiency and branding demands. Folding cartons hold a substantial 18% share, serving as the primary packaging for consumer goods, food, and pharmaceuticals, where high-impact printability and recyclability are equally important for compliance and shelf appeal. Paper bags and sacks are surging due to plastic bag bans and industrial multi-wall sack applications, with growth focused on retail, agriculture, and cement packaging. Cups and trays play a pivotal role in foodservice, where innovation centers on recyclable and compostable barriers to replace polyethylene linings. Liquid cartons remain a high-value aseptic packaging format for dairy, juice, and soups, though challenged by recyclability concerns. Emerging product types, such as molded pulp protective packaging, are capturing attention as eco-friendly alternatives to plastics in electronics and fragile goods. Collectively, corrugated’s scale dominance, combined with carton and bag growth, positions paper packaging as the core driver of sustainable packaging adoption worldwide.

Food & Beverages Hold the Largest Market Share by Application in the Paper Packaging Industry

The food and beverage sector accounts for 42% of demand, making it the undisputed leader in paper packaging applications. Its scale is driven by the ubiquity of cartons for cereals, sacks for flour, corrugated boxes for beverages, and cups and trays for foodservice, positioning the industry at the center of regulatory and sustainability transformations. Packaging here must balance food safety compliance, extended shelf-life, and consumer-facing branding requirements, ensuring performance while addressing recyclability and compostability mandates. E-commerce and retail follow closely at 38%, functioning as the primary growth driver for corrugated packaging. Beyond shipping, this segment emphasizes shelf-ready formats and durability for last-mile delivery, blending performance and branding imperatives. Industrial goods rely on heavy-duty corrugated and multi-wall sacks to transport machinery, chemicals, and building materials, prioritizing strength and efficiency over aesthetics. Healthcare and pharmaceuticals form a high-value, compliance-driven niche, demanding tamper-evident and regulatory-compliant folding cartons for medicines and devices. Personal care and cosmetics prioritize premium folding cartons with advanced printing and luxury finishes, merging brand differentiation with sustainability messaging. Electronics and appliances emphasize engineered corrugated and molded pulp structures to protect high-value products from transit damage while aligning with recyclability goals. Together, the application segmentation demonstrates that while food and beverages dominate in volume, e-commerce, healthcare, and cosmetics are reshaping paper packaging into a performance- and sustainability-led industry.

United States Paper Packaging Market Driven by E-Commerce and Sustainability Mandates

The United States paper packaging market is experiencing strong growth due to the booming e-commerce sector, which demands lightweight corrugated packaging capable of withstanding the rigors of direct-to-consumer shipping. The U.S. Environmental Protection Agency (EPA), through its Comprehensive Procurement Guidelines (CPG) program, is encouraging federal procurement of paper and paperboard products containing recycled content, incentivizing companies to expand their use of post-consumer materials. Additionally, the U.S. Food and Drug Administration (FDA) ban on PFAS in food-contact materials has accelerated the shift toward fluorine-free barrier coatings for paperboard, a crucial development for food and beverage packaging.

Major corporations like International Paper and WestRock are investing heavily in sustainability initiatives, developing fiber-based alternatives to single-use plastics and innovating with smart and digital printing. This trend allows brands to offer highly customized, graphically rich paper packaging, which is particularly critical for direct-to-consumer brands competing in a crowded marketplace. The U.S. is also emerging as a hub for smart packaging adoption, with QR codes and NFC-enabled paperboard solutions enhancing customer engagement while reducing plastic usage.

China Paper Packaging Market Strengthened by Circular Economy and High-Volume Production

The China paper packaging market is expanding rapidly, driven by government-led plastic waste reduction policies and the National Clean Air Programme. With the explosive growth of e-commerce, China has become a global leader in producing durable, lightweight corrugated boxes and other paperboard formats tailored for parcel delivery and protective shipping. Domestic paper manufacturers are making significant investments in expanding capacity, particularly in the production of recycled fiber-based packaging-grade paper and board, to meet growing domestic and international demand.

China’s quick-service and takeaway food sector is also fueling demand for cost-efficient, grease-resistant wraps and folding cartons, as consumer lifestyles shift toward convenience. At the same time, large-scale export-oriented manufacturing is pushing innovation in lightweight designs to reduce shipping costs. With sustained growth in both e-commerce and foodservice packaging, and continuous government pressure on plastic alternatives, China remains at the forefront of high-volume, innovative paper packaging solutions worldwide.

India Paper Packaging Market Accelerated by Plastic Waste Rules and Expanding Retail

The India paper packaging market is undergoing rapid transformation, driven by the government’s Plastic Waste Management Rules and the Extended Producer Responsibility (EPR) framework, which are compelling industries to replace plastic with sustainable alternatives. The country’s fast-growing food processing sector is a major consumer of paper and paperboard, as regulatory and consumer pressure push companies to reduce their plastic footprint. Additionally, the Food Safety and Standards Authority of India (FSSAI) is encouraging the adoption of glass, paper, and metal packaging, further accelerating demand.

India’s Make in India initiative is strengthening domestic manufacturing of sophisticated packaging materials, while major domestic firms such as Andhra Paper, Orient Paper & Industries, and Satia Industries are investing heavily in capacity expansion and modernization. Rapid urbanization, organized retail, and the e-commerce boom are creating high demand for corrugated boxes, folding cartons, and barrier-coated paper packaging. E-commerce giants like Flipkart are publicly committing to eliminate plastic cushioning in deliveries, further boosting paper packaging adoption. Combined with simplified GST policies supporting the paper industry, India is positioning itself as one of the fastest-growing global markets for eco-friendly paper packaging solutions.

Germany Paper Packaging Market Driven by EU PPWR and Sustainable Material Innovation

The Germany paper packaging market is shaped by the European Union’s Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging must be reusable or recyclable by 2030. This has accelerated innovation in mono-material paper packaging solutions designed for easy recyclability. The demand for FSC and PEFC-certified paperboard is also rising, as German brands emphasize responsibly sourced raw materials in line with EU sustainability standards.

German manufacturers are leaders in specialty-coated paperboard solutions for electronics, luxury goods, and high-end retail packaging. Investments in water-based coating technologies are enabling packaging with enhanced barrier properties—such as resistance to grease, moisture, and oxygen—without compromising recyclability. Germany’s strong recycling infrastructure and push for a circular economy further support the growth of paper packaging. The country’s reputation for precision manufacturing and environmental compliance makes it a benchmark for sustainable packaging innovation in Europe.

United Kingdom Paper Packaging Market Supported by Plastic Packaging Tax and E-Commerce Expansion

The United Kingdom paper packaging market is witnessing significant growth due to the Plastic Packaging Tax, which penalizes packaging containing less than 30% recycled plastic. This regulatory framework is compelling companies to adopt paperboard and corrugated solutions, making the UK a leading market for sustainable packaging innovation. The country’s robust e-commerce ecosystem, particularly in subscription services and premium goods, is fueling demand for rigid and corrugated boxes that offer both protection and brand appeal.

UK manufacturers are focusing on glue-free, interlocking paperboard designs that enhance recyclability and reduce waste, aligning with circular economy principles. Premium and luxury goods brands in the UK are adopting embossed, foiled, and graphically rich paperboard packaging to enhance brand value, while simultaneously meeting consumer demand for eco-friendly solutions. The combination of regulatory push, e-commerce growth, and consumer preference for sustainable luxury packaging positions the UK as a dynamic and high-value market for paper packaging in Europe.

Japan Paper Packaging Market Strengthened by Green Innovation and Premium Design

The Japan paper packaging market is characterized by its dual focus on sustainability and high-quality design. Leading companies like Oji Holdings and Nippon Paper Industries are pioneering fiber-based innovations and expanding their global reach to meet rising international demand. The Japanese government’s Green Innovation policies are incentivizing the development of biodegradable and compostable materials, pushing manufacturers toward advanced R&D in barrier coatings and recyclable formats.

Japan’s food and beverage sector remains a core application area, with rising demand for lightweight, protective packaging that ensures product freshness and extends shelf life. Additionally, the country’s cultural emphasis on aesthetic and functional packaging drives innovation in visually appealing paperboard containers that double as brand assets. With strong ties to both sustainable forestry management and precision manufacturing, Japan is a leader in premium and eco-friendly paper packaging solutions across Asia.

Paper Packaging Market Report Scope

Paper Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$441.6 Billion

|

|

Market Size (2034)

|

$656.3 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Type (Corrugated Boxes, Folding Cartons, Liquid Cartons, Paper Bags & Sacks, Paperboard Cups & Trays, Other Product Types), By Material Grade (Virgin Fiber, Recycled Fiber, Hybrid/Mixed Fiber), By Application (Food & Beverages, E-commerce & Retail, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Industrial Goods, Electronics & Appliances, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

International Paper Company, WestRock Company, Smurfit Kappa Group, DS Smith Plc, Oji Holdings Corporation, Mondi Group, Stora Enso Oyj, Graphic Packaging Holding Company, Packaging Corporation of America, Nippon Paper Industries Co., Ltd., Sonoco Products Company, Amcor Plc, BillerudKorsnäs AB, Huhtamäki Oyj, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paper Packaging Market Segmentation

By Product Type

- Corrugated Boxes

- Folding Cartons

- Liquid Cartons

- Paper Bags & Sacks

- Paperboard Cups & Trays

- Other Product Types

By Material Grade

- Virgin Fiber

- Recycled Fiber

- Hybrid/Mixed Fiber

By Application

- Food & Beverages

- E-commerce & Retail

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Goods

- Electronics & Appliances

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Paper Packaging Market

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Oji Holdings Corporation

- Mondi Group

- Stora Enso Oyj

- Graphic Packaging Holding Company

- Packaging Corporation of America

- Nippon Paper Industries Co., Ltd.

- Sonoco Products Company

- Amcor Plc

- BillerudKorsnäs AB

- Huhtamäki Oyj

- Greif, Inc.

* List Not Exhaustive

Methodology

The methodology for the Paper Packaging Market analysis by USDAnalytics integrates comprehensive primary and secondary research to deliver actionable insights for industry professionals. Primary research involved in-depth interviews with packaging engineers, sustainability officers, supply chain managers, and executives from leading end-use sectors including food & beverages, e-commerce, healthcare, and industrial goods. Secondary research encompassed reviewing company reports, investor presentations, regulatory documents, trade publications, patents, and market intelligence on innovations in fiber-based packaging, barrier coatings, and molded pulp applications. Market sizing and forecasts were derived using top-down and bottom-up approaches, validated through data triangulation, incorporating global e-commerce growth, single-use plastic bans, regulatory mandates like EU PPWR and Plastic Packaging Tax, and consumer demand for sustainable solutions. USDAnalytics analyzed regional dynamics, product type adoption, material preferences, and application-specific trends, while evaluating the competitive landscape of major players such as Smurfit Westrock, International Paper, and Mondi Group. This rigorous methodology ensures a holistic understanding of market drivers, technological innovations, sustainability adoption, and emerging opportunities in the global paper packaging ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.