Food Safety, Sustainability, and Dairy Dominance Drive Aseptic Packaging Market to USD 191.4 Billion by 2034

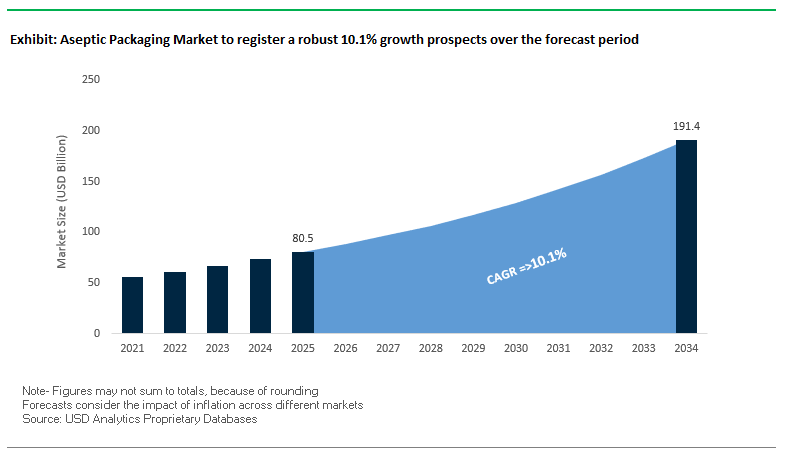

The global aseptic packaging market is valued at USD 80.5 billion in 2025 and is projected to reach USD 191.4 billion by 2034, growing at a robust CAGR of 10.1%. This growth is fueled by the rising demand for food preservation without refrigeration, particularly in beverages and liquid foods. By protecting against spoilage without preservatives, aseptic cartons and pouches enable safe storage at room temperature, reducing cold chain dependency and energy costs across global supply chains.

The market is dominated by the dairy and juice segments, where aseptic cartons help retain nutritional integrity, vitamins, and flavor while ensuring convenience for consumers. A growing emphasis on paperboard as the primary material reflects the packaging industry’s sustainability agenda, as brands respond to regulatory and consumer demand for eco-friendly formats. Beyond beverages, aseptic packaging plays a pivotal role in reducing global food waste, which affects nearly one-third of all food produced, by offering strong protection against oxygen, light, and moisture.

Key Insights for Industry Professionals

- Room-temperature preservation reduces energy use and enhances convenience.

- Dairy and juice applications remain the largest demand drivers for aseptic cartons.

- Paperboard-based formats align with sustainability and renewable material mandates.

- Food waste reduction is a strategic outcome, strengthening the market’s role in food security.

Strategic Expansions, Sustainability Ratings, and Breakthrough Materials Redefine the Aseptic Packaging Industry

The aseptic packaging sector is undergoing significant transformation through strategic expansions, sustainability-driven partnerships, and new material launches. In August 2025, SIG achieved recognition from the Association of Plastic Recyclers (APR) for its recycle-ready wine bag-in-box packaging, setting a new benchmark for recyclability. That same month, Smurfit WestRock officially debuted post-merger, consolidating expertise in paper-based and industrial aseptic solutions.

Sustainability leadership continues to define the industry. In July 2025, Tetra Pak earned the EcoVadis Platinum medal, the highest rating for sustainability, validating its long-term ESG strategy. Also in July, Greatview announced a new aseptic carton facility in Italy, signaling its intent to strengthen its presence in the European market. In June 2025, Elopak expanded into North America with its first U.S. carton converting plant in Arkansas, while Hochwald introduced aluminum-layer-free cartons using SIG Terra packaging for UHT milk.

Innovations in barrier technology are also reshaping the market. In March 2025, Corvaglia Group launched the SabreCap closure for aseptic cartons, designed for seamless integration into existing lines. Earlier, in February 2025, Tetra Pak and Nissha Metallizing Solutions launched a paper-derived barrier carton with 80% paper content, cutting carbon footprint significantly. That same month, SIG opened its first production facility in India, with an annual capacity of 4 billion packs, enhancing access to high-growth emerging markets.

Key Trends Transforming the Future of the Aseptic Packaging Market

Strategic Capacity Expansion in North America to Enhance Supply Chain Resilience

One of the most prominent trends in the aseptic packaging market is the wave of capacity expansion initiatives in North America, as manufacturers aim to strengthen supply chains and cut logistical dependencies. A prime example is SIG’s €73 million investment in a new state-of-the-art plant in Querétaro, Mexico, operational since early 2023, which caters to the U.S., Canada, and Mexico markets. This facility not only shortens lead times but also aligns with the post-pandemic push for supply chain resilience and cost efficiency. Further strengthening its regional foothold, SIG announced an additional $35 million investment in 2025, projected to increase production by 50% and diversify carton formats ranging from on-the-go packs to large family-size cartons. The plant’s strategic location provides a logistical edge by ensuring faster turnaround and reduced delivery costs, while also aligning with the surging demand for shelf-stable, portion-controlled products in North America. These expansions are more than capacity increases they represent a structural shift toward regionalized production models that offer both sustainability and agility.

Accelerated Adoption of Full-Cycle Sustainable Material Sourcing

The second major trend shaping the global aseptic packaging industry is the accelerated adoption of renewable, plant-based polymers and recycled content. Companies like Tetra Pak are pioneering this transition: in 2022 alone, it sold 8.8 billion packages and 11.9 billion caps made with plant-based plastic, marking 24% and 12% year-on-year growth, respectively. Lifecycle assessments confirm that packaging like the Tetra Brik® Aseptic 1000 Edge with plant-based coatings achieves a 37% lower carbon footprint compared to standard formats. This shift is backed by responsible sourcing initiatives, such as Tetra Pak’s collaboration with Braskem, ensuring sugarcane bioethanol is produced in line with Bonsucro standards for sustainable agriculture. Beyond short-term measures, Tetra Pak has pledged €100 million annually for the next 5–10 years to advance fiber-based barriers and eventually replace aluminum foil, which currently complicates recyclability. For brand owners, this transition supports ESG compliance, helps cut Scope 3 emissions, and enables consumer-facing sustainability credentials like Carbon Trust certification. The commitment signals that sustainable sourcing is no longer a niche initiative but a mainstream transformation defining future competitiveness in the aseptic packaging market.

Emerging Opportunities Driving Growth in the Aseptic Packaging Industry

Integration of Digital Watermarks for Precision Recycling

A transformative opportunity in the aseptic packaging market is the integration of digital watermarking technology, which solves the long-standing challenge of recycling multilayer cartons. Initiatives like HolyGrail 2.0 have demonstrated promising results, with trials at a Swisttal, Germany recovery facility achieving 87.9%–93.8% detection accuracy and processing over 56,000 packages per day. The technology combines near-infrared (NIR) spectroscopy with digital watermark detection, enabling granular sorting by SKU and distinguishing between food-grade and non-food-grade packaging. This capability produces high-quality, segregated recycling streams, significantly improving the recovery of polyAlu materials. With over 130 companies from the packaging value chain including SIG and Tetra Pak collaborating under HolyGrail 2.0, the push toward large-scale commercial adoption is strong. Moreover, as the EU Packaging and Packaging Waste Regulation (PPWR) tightens requirements for recycled content by 2030, watermark-enabled sorting positions aseptic packaging to meet regulatory benchmarks while reinforcing its role in the circular economy of food packaging.

Penetration into New High-Value Food Categories

Another critical growth avenue lies in extending aseptic packaging applications beyond dairy and juice into new categories such as liquid eggs, plant-based beverages, wine, soups, and sauces. The format offers clear advantages: extended shelf life, preservation of nutrients and taste without preservatives, and reduced food waste. For instance, aseptic technology enables liquid eggs to remain shelf-stable without refrigeration, a solution that enhances convenience and safety for commercial kitchens. In the plant-based beverage market, aseptic cartons support the surging demand for oat, almond, and soy milk, offering freshness and sustainability while eliminating the cold chain. In developing regions, aseptic packaging is enabling safe distribution of products like ghee in India, expanding market access where refrigeration infrastructure is limited. Furthermore, advances in aseptic processing now accommodate particulate-rich products such as soups and sauces, unlocking new opportunities in the convenience food sector. This diversification beyond traditional segments makes aseptic packaging a growth accelerator across multiple high-value food categories worldwide, ensuring strong market penetration in both developed and emerging regions.

Global Packaging Leaders Compete Through Sustainable Innovation, Expansions, and Material Science Expertise

The competitive landscape of the aseptic packaging market is defined by global leaders in carton, film, and closure systems. Companies are differentiating themselves through sustainability commitments, circular economy initiatives, and product diversification.

Tetra Pak International: Leading with Renewable Cartons and Recycling Partnerships

Tetra Pak remains the undisputed leader in aseptic carton packaging, offering comprehensive solutions from filling systems to processing. In April 2025, it partnered with Lactalis to launch the first carton made from certified recycled polymers, reinforcing its circular economy focus. Earlier, in 2024, it launched the Tetra Prisma Aseptic 300 Edge, designed for ergonomic handling. With deep vertical integration and global presence, Tetra Pak continues to lead in sustainability and product innovation.

SIG Combibloc: Commercializing Aluminum-free Cartons to Cut Carbon by 61%

SIG is reshaping the industry with its aluminum-free aseptic carton, launched in 2025, which reduces carbon footprint by 61%. The company’s SIG Terra portfolio focuses on renewable and recyclable solutions, while its flexible filling systems allow customers to switch between formats and volumes with efficiency. SIG’s expansion into India (February 2025) further strengthens its global reach in high-growth regions.

Elopak ASA: Strengthening North America with U.S. Converting Plant

Elopak’s expansion in June 2025 with its first U.S. carton converting plant reflects its strategy to penetrate North America. Its Pure-Pak brand continues to drive sustainability with tethered caps and lightweight formats. The company reported record revenues in 2024 and aims to double by 2030, highlighting its aggressive growth and sustainability-driven strategy under the vision of “Repackaging tomorrow.

Amcor plc: Scaling Circular Economy Solutions Across Flexible Aseptic Formats

Amcor remains a leader in flexible aseptic packaging for sensitive foods, including baby food. In August 2025, it upgraded its Heanor recycling facility in the UK, boosting recycled polymer output to integrate into its packaging lines. With a target to make all packaging recyclable or reusable by 2025, Amcor aligns its strategy with circular economy goals. Its aseptic pouches and films combine high-barrier performance with easy integration into customer production systems.

Aseptic Packaging Market Share Insights

Cartons Lead Aseptic Packaging Market Share by Product Type

Cartons dominate the aseptic packaging market, projected to capture 45% of total share in 2025, due to their cost-efficiency, recyclability, and scalability in high-speed filling lines for liquid foods such as milk, juices, and plant-based beverages. Bags and pouches follow with a strong share, driven by versatility across both bulk and single-serve applications, while pre-filled syringes and vials occupy a high-value niche in pharmaceuticals where sterility and drug safety are paramount. Bottles and cans continue to serve premium beverage categories where resealability and portability are key consumer preferences. The product type landscape highlights the balance between volume leadership in food and beverage packaging and premium growth opportunities in pharmaceuticals and functional beverages.

Food & Beverages Anchor Aseptic Packaging Market Share by End-Use Industry

Food and beverages represent the foundation of aseptic packaging, commanding 70% of market share in 2025 as global demand for preservative-free, nutrient-retaining products surges. Pharmaceuticals represent the second most critical segment, with aseptic packaging indispensable for injectables, biologics, and advanced therapies that cannot be terminally sterilized. Cosmetics and personal care are emerging as a growth niche, leveraging aseptic packaging to market preservative-free clean beauty products, while other industries such as chemicals and veterinary care expand aseptic adoption for specialized sterile applications. Together, these industries demonstrate the broadening relevance of aseptic technology across sectors, with food & beverages securing volume dominance and pharmaceuticals reinforcing value-driven growth.

United States: FDA Oversight, Industry Consolidation, and Sustainability in Aseptic Packaging

The United States aseptic packaging market is shaped by the U.S. Food and Drug Administration (FDA), which regulates food-contact substances and provides a robust pre-market consultation framework. This regulatory clarity fosters innovation while ensuring consumer safety, particularly for new aseptic technologies in food and pharmaceuticals. Companies are investing heavily in sustainability and consumer convenience, with packaging solutions emphasizing recyclability, reduced plastic and aluminum layers, and lightweight designs. Notably, Berry Global’s partnership with Pylote in 2022 to create multi-dose aseptic eye drops with antimicrobial protection underscores the sector’s diversification into pharmaceutical-grade aseptic packaging.

The U.S. market is experiencing rapid technological advancements in smart and active packaging, which extend shelf life without refrigeration critical for beverages, dairy, and preservative-free foods. Key applications span both beverages (milk, juices, plant-based drinks) and pharmaceuticals (prefilled syringes, biologics, and cartridges), making it one of the most diverse aseptic markets worldwide. Another defining trend is industry consolidation, highlighted by PCI Pharma Services’ acquisition of Ajinomoto Althea in 2025, expanding sterile fill-finish capabilities. This combination of strict FDA oversight, sustainability commitments, and M&A activity cements the U.S. as a leader in aseptic packaging innovation.

Germany: EU Circular Economy Mandates Driving Aseptic Packaging Innovation

Germany’s aseptic packaging industry is built on the EU Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be fully recyclable or reusable by 2030. Alongside this, Germany’s Packaging Act (VerpackG) places lifecycle responsibility on producers, pushing companies to adopt highly recyclable aseptic carton designs. These frameworks are reshaping the market, driving investments into materials like grass paper, high-strength recycled fibers, and aluminum-free cartons. A prime example is Hochwald’s launch of UHT milk in SIG Terra Alu-free cartons, which cut carbon emissions by 34% compared to standard cartons.

The country’s leadership in the circular economy makes it a hub for R&D in packaging technology, with companies and universities collaborating on lighter, stronger, and eco-friendly aseptic solutions. The food and beverage industry remains the strongest application segment, with aseptic cartons widely used for soups, juices, and milk. Meanwhile, the pharmaceutical sector is increasingly reliant on aseptic packaging to ensure the sterility of biologics and other sensitive products. Germany’s heavy investment in research, regulatory-driven innovation, and sustainable production systems position it as a global leader in eco-conscious aseptic packaging.

China: Dual Carbon Policy and AI-Driven Aseptic Packaging Manufacturing

China’s aseptic packaging market is undergoing a transformation led by the government’s “dual carbon” strategy, which restricts non-degradable plastics and accelerates adoption of paper-based and recyclable aseptic cartons. Regulatory oversight by the State Administration for Market Regulation (SAMR), through GB standards for food safety and additives, ensures compliance with global norms. Frequent updates to these standards reinforce consumer protection and align China’s industry with international benchmarks.

At the same time, AI, automation, and 5G-enabled industrial internet technologies are redefining production lines, improving flexibility and efficiency in aseptic carton manufacturing. A core trend is domestic substitution, as Chinese companies expand their capacity to replace imported aseptic packaging solutions, particularly for liquid milk and beverage products. Corporate investments into local manufacturing capacity are reshaping the competitive landscape while fueling growth in the food, beverage, and e-commerce-driven packaged food sectors. Combined with new labeling regulations (GB 28050-2025), which improve transparency, China is rapidly becoming a global force in the aseptic packaging market.

India: Expanding Dairy Sector and Global Investments Bolster Aseptic Packaging Growth

India’s aseptic packaging industry is supported by government initiatives like “Make in India” and “Zero Effect Zero Defect”, which prioritize quality domestic production. The Food Safety and Standards Authority of India (FSSAI) plays a crucial role, enforcing packaging standards under the Food Safety and Standards (Packaging) Regulations, 2018. In April 2025, the FSSAI elevated packaging materials to “critical” in inspections, underscoring their importance in food safety compliance.

India is attracting heavy corporate and infrastructure investments, such as SIG’s €90 million aseptic carton plant (2025), which produces up to 4 billion cartons annually. This investment reflects the surging demand driven by the country’s booming food processing sector, particularly dairy and fruit beverages. Technology adoption is advancing with automated packaging systems and QR code-enabled traceability, enhancing consumer trust and supply chain visibility. Sustainability is also emerging as a priority, with innovations in biodegradable and compostable aseptic cartons gaining ground. Together, these factors position India as a high-growth hotspot for aseptic packaging in both domestic and export markets.

Brazil: ANVISA Regulations and Robotics Powering Aseptic Packaging Expansion

Brazil’s aseptic packaging market is defined by evolving regulations from ANVISA, which introduced RDC 983/2025 to allow depletion of old stock before compliance with new packaging rules requiring regulatory numbering. This flexibility ensures smooth industry transition while avoiding material waste. Additionally, Brazil’s January 2025 solid waste law, which promotes domestic recycling and circular economy practices, indirectly accelerates demand for recyclable aseptic packaging solutions.

On the technology front, Brazilian manufacturers are increasingly implementing robotics and AI for automated defect detection, quality control, and sorting, enhancing both efficiency and consistency in production. The food and beverage sector remains the largest demand driver, especially for milk, juices, and soy-based beverages, supported by Brazil’s fast-growing processing industry. Pharmaceutical applications are also expanding, with safe, sterile packaging becoming a priority. With sustainability goals, strategic investments, and government support converging, Brazil is emerging as a strong growth market in Latin America’s aseptic packaging landscape.

Japan: Smart Packaging and Biopolymer Research Redefining Aseptic Packaging

Japan stands at the forefront of aseptic packaging innovation, combining precision manufacturing excellence with cutting-edge research. The 2025 Food Sanitation Act revision introduced by the Ministry of Health, Labour and Welfare (MHLW) requires a positive list of permitted substances for food-contact packaging, ensuring safety and compliance. This provides a strong regulatory backbone for Japan’s aseptic packaging sector.

One of the most distinctive trends in Japan is the adoption of smart packaging technologies, integrating sensors and digital monitoring tools to track freshness, safety, and shelf life. Companies like Toyo Seikan Group are pioneering lightweight and recyclable aseptic cartons, while universities are actively researching biopolymers and natural additives to develop sustainable, high-performance packaging. Functional innovations such as enhanced dimensional stability and deformation resistance make Japanese aseptic packaging highly specialized for demanding applications. With corporate collaborations, academic research, and regulatory precision, Japan is setting global benchmarks for the future of aseptic packaging.

Aseptic Packaging Market Report Scope

Aseptic Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$80.5 Billion

|

|

Market Size (2034)

|

$191.4 Billion

|

|

Market Growth Rate

|

10.1%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Biopolymers, Metals), By Product Type (Cartons, Bottles & Cans, Bags & Pouches, Pre-filled Syringes & Vials), By Technology (Active Release, Controlled Release, BFS), By End-Use Industry (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Others), By Application (Beverages, Food Products, Medical & Surgical Devices, Pharmaceuticals & Biologics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Tetra Pak, SIG Combibloc Group AG, Elopak ASA, Amcor plc, Mondi Group, Greatview Aseptic Packaging Co., Ltd., DS Smith Plc, Smurfit Kappa Group Plc, Nippon Paper Industries Co., Ltd., Huhtamäki Oyj, Sonoco Products Company, WestRock Company, Becton, Dickinson and Company, IPI Srl, Uflex Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aseptic Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Biopolymers

- Metals

By Product Type

- Cartons

- Bottles & Cans

- Bags & Pouches

- Pre-filled Syringes & Vials

By Technology

- Active Release

- Controlled Release

- BFS

By End-Use Industry

- Food & Beverages

- Pharmaceuticals

- Cosmetics & Personal Care

- Others

By Application

- Beverages

- Food Products

- Medical & Surgical Devices

- Pharmaceuticals & Biologics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Aseptic Packaging Market

- Tetra Pak

- SIG Combibloc Group AG

- Elopak ASA

- Amcor plc

- Mondi Group

- Greatview Aseptic Packaging Co., Ltd.

- DS Smith Plc

- Smurfit Kappa Group Plc

- Nippon Paper Industries Co., Ltd.

- Huhtamäki Oyj

- Sonoco Products Company

- WestRock Company

- Becton, Dickinson and Company

- IPI Srl

- Uflex Limited

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and integrated research methodology to provide precise insights into the global aseptic packaging market. This methodology combines primary research including interviews with industry executives, packaging manufacturers, regulatory authorities, and food & beverage producers with comprehensive secondary research from company reports, trade journals, patents, and verified news sources. Market sizing, forecasts, and growth projections are derived using proprietary quantitative models that account for historical trends, material innovations, regulatory frameworks, sustainability mandates, and evolving consumer preferences for eco-friendly packaging. Competitive intelligence covers strategic mergers, capacity expansions, sustainability initiatives, and product innovations by leading players such as Tetra Pak, SIG Combibloc, Elopak, and Amcor, while regional analyses focus on the U.S., Germany, China, India, Brazil, and Japan, highlighting regulatory impacts, technological adoption, and market expansion strategies. USDAnalytics triangulates data across multiple sources, ensuring high accuracy and actionable insights for industry professionals seeking investment guidance, operational efficiency improvements, and sustainable packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.