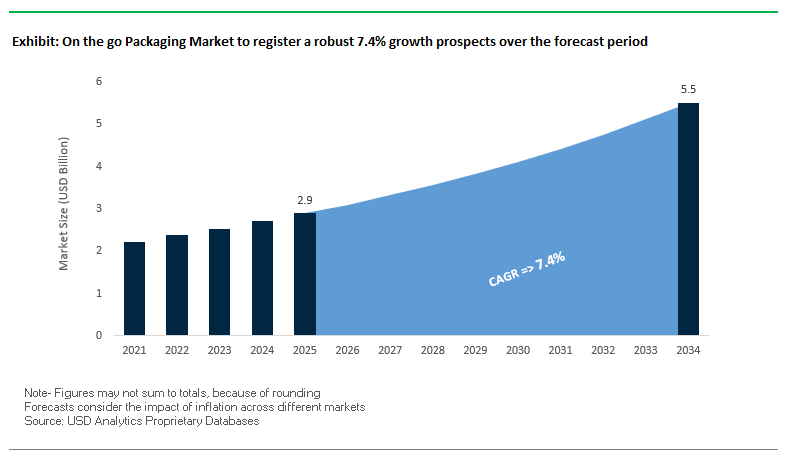

On-the-go Packaging Market Set to Grow from $2.9 Billion in 2025 to $5.5 Billion by 2034 at 7.4% CAGR

The global on-the-go packaging market is poised for significant growth, expanding from $2.9 billion in 2025 to $5.5 billion by 2034, at a CAGR of 7.4%. This growth is driven by the increasing demand for portable, convenient, and ready-to-consume packaging solutions across food, beverages, personal care, and health products. The market’s expansion reflects urbanization, fast-paced lifestyles, and heightened consumer awareness around health, safety, and sustainability.

Key Insights for Industry Professionals:

- Convenience-oriented growth: Rising demand for single-serve pouches, resealable cups, and easy-to-open bottles supports faster consumption in on-the-go contexts.

- Sustainable packaging adoption: Shift from single-use plastics to paper-based, biodegradable, and reusable containers aligns with corporate ESG and global sustainability trends.

- Freshness and preservation: Innovations in barrier films, hermetic seals, and modified atmosphere packaging (MAP) help extend shelf life, maintain product quality, and reduce food waste.

- Smart packaging integration: QR codes, NFC tags, and digital touchpoints provide nutritional information, product traceability, and interactive consumer engagement.

- Alignment with health-conscious trends: Packaging innovations cater to the growing preference for nutritious, functional, and safe on-the-go products.

Recent Developments Demonstrate Industry Shift Toward Sustainability and Smart Packaging

The on-the-go packaging industry is witnessing rapid developments focused on sustainability, technological integration, and market consolidation. In August 2025, DNP introduced mono-material recyclable solutions at Medical Fair Thailand, showcasing innovations applicable to food, beverage, and healthcare packaging. In July 2025, the Amcor-Berry Global all-stock combination officially closed, creating a global leader in flexible and rigid packaging.

In May 2025, Sealed Air Corporation launched Cryovac ICETech, a sustainable insulation material for perishable products designed to lower carbon emissions and minimize waste. International Paper completed its $9.9 billion acquisition of DS Smith in April 2025, expanding its corrugated box and sustainable paper packaging offerings. Amcor introduced the AmFiber Performance Paper stand-up pouch in February 2025, reducing carbon footprint by 73%, while Belgian Boys unveiled its Breakfast All Day boxes and Pancakes & Go cups in November 2024, enhancing mess-free portability.

Earlier in the market timeline, ProAmpac launched the RotiBag in October 2024, offering an eco-friendly alternative to traditional clamshells. Sabert, in September 2024, introduced Hot2Go, a fiber-based recyclable pack for hot foods. In the same month, Shiseido replaced traditional plastic bubble wrap in e-commerce shipments with recyclable Kraft honeycomb wrap, aligning with its sustainability goals.

Trends and Opportunities Shaping the On-the-Go Packaging Market

Accelerated Deployment of Advanced Fiber-Based Materials for Hot and Greasy Foods

The on-the-go packaging market is undergoing a rapid shift toward next-generation fiber-based packaging as Quick Service Restaurants (QSRs) and foodservice providers seek to eliminate plastics and comply with upcoming PFAS bans. Fiber-based clamshells, wraps, and trays designed to handle heat, grease, and moisture are replacing traditional plastic formats, creating a surge in demand for sustainable alternatives. Corporate commitments are a strong catalyst: McDonald’s has pledged to source 100% of its primary guest packaging from renewable, recycled, or certified materials by the end of 2025, accelerating the transition away from virgin plastics. Regulatory frameworks further reinforce this shift. As of January 1, 2025, PFAS bans have come into effect in states like Minnesota, Oregon, and Rhode Island, forcing brands to adopt PFAS-free barrier coatings. Industry-wide adoption is visible in the growing deployment of bio-based coatings derived from vegetable oils and starches, engineered to maintain grease resistance while being compostable and recyclable. Collectively, these shifts mark a structural change where fiber-based solutions are becoming the default choice for hot and greasy food packaging in the on-the-go sector.

Integration of Smart and Connected Packaging for Enhanced User Experience and Traceability

The integration of smart and connected packaging technologies is redefining consumer interaction and end-of-life management for on-the-go products. Packaging is being equipped with QR codes, NFC tags, and invisible digital watermarks that enhance traceability, enable interactive consumer engagement, and streamline recycling. The HolyGrail 2.0 initiative demonstrates the effectiveness of digital watermarks: industrial-scale trials achieved over 90% detection efficiency, creating high-purity recycling streams and overcoming challenges posed by multi-material packaging. At the consumer interface, brands are leveraging QR-enabled packaging for transparency and engagement. For example, Hershey’s has embedded QR codes in its holiday packaging, offering direct access to product sourcing and ingredient information, while PepsiCo has used QR-enabled bottles in marketing campaigns, delivering personalized digital content. These innovations elevate packaging from a static container to a dynamic communication channel, offering functionality, consumer trust, and supply chain efficiency in equal measure.

Development of High-Performance, Monomaterial Flexible Pouches

A major growth opportunity lies in the development of high-barrier, monomaterial flexible pouches that address recyclability challenges associated with traditional multi-layer laminates. Flexible packaging for snacks, sauces, and beverages often relies on complex laminates that are difficult to recycle. By advancing all-PE or all-PP structures, brands can achieve both barrier integrity and recyclability. Progress is already underway: the Mondi Group introduced award-winning monomaterial barrier solutions for high-protection products like snacks and coffee, balancing product safety with circularity. Collaboration is central to this innovation—Paulig, a European coffee company, partnered with Mondi to create a recyclable monomaterial coffee pouch, proving the technical and commercial viability of such solutions. For the on-the-go segment, where lightweight, durable, and shelf-stable packaging is critical, high-performance monomaterial pouches present a clear pathway to achieving sustainability goals without sacrificing performance.

Scaling of Reusable Packaging Systems for Urban Delivery and Quick Commerce

The rise of urban quick commerce and rapid grocery delivery is fueling demand for reusable packaging systems that can displace single-use bags and boxes. Durable, trackable containers designed for collection, sanitization, and redeployment offer a sustainable model for dense urban centers. Leading corporations are setting ambitious targets to support this shift. The Coca-Cola Company aims to have 25% of its beverages sold in refillable/reusable bottles by 2030, signaling a broader industry pivot from recycling to reuse. Infrastructure collaboration is also scaling: the NextGen Consortium, involving Starbucks and McDonald’s, is piloting reusable cup systems to make reuse both convenient and commercially viable. At the same time, Loop’s circular platform is pioneering durable, returnable containers across categories by partnering with global retailers and FMCG brands. These systems not only reduce single-use waste but also create opportunities for brand loyalty and customer engagement in the rapidly growing on-the-go packaging ecosystem.

Competitive Landscape Highlighting Leaders Driving Innovation in On-the-go Packaging

The on-the-go packaging industry is shaped by a set of strategic global players leveraging advanced materials, design expertise, and sustainable practices to meet evolving consumer needs. These companies provide flexible, rigid, and smart packaging solutions for a wide array of food, beverage, and personal care applications.

Amcor PLC Drives Sustainable Innovations Across Flexible and Rigid Packaging

Amcor PLC is a global leader in flexible and rigid packaging, serving food, beverage, and healthcare segments. In February 2025, the company launched AmFiber Performance Paper stand-up pouch, a paper-based solution with a 73% lower carbon footprint. Its July 2025 merger with Berry Global reinforced its leadership in the consumer packaging industry. Amcor offers flexible pouches, rigid containers, and easy-to-open packaging, combining convenience with sustainability. Its strategic focus is on recyclable and reusable products, supported by ongoing investments in material innovation and eco-friendly technologies.

Sealed Air Corporation Provides Advanced Thermal Protection for On-the-go Products

Sealed Air Corporation specializes in protective and food packaging solutions, with strengths in foam-in-place, air-filled, and insulated packaging. In May 2025, it introduced Cryovac ICETech, a sustainable insulation material for perishable goods. The company offers Instapak® thermal foam and TempGuard® insulated bags, supporting just-in-time and last-mile delivery. Sealed Air focuses on efficient, secure, and low-waste supply chains, developing sustainable solutions for e-commerce and perishable foods.

Huhtamaki Oyj Expands Recyclable and Compostable Food-on-the-go Packaging

Huhtamaki Oyj is a global player in flexible and rigid sustainable packaging. In July 2025, it launched an innovative recyclable and compostable packaging solution, earning a fifth consecutive EcoVadis gold medal. Its offerings include paper cups, lids, flexible pouches, and ProDairy single-coated cups, reducing plastic content below 10%. The company’s strategy emphasizes protecting food, people, and the environment, while advancing circular economy practices and reducing food loss.

ProAmpac Focuses on High-Performance Flexible Solutions for On-the-go Consumption

ProAmpac is a leader in flexible packaging, specializing in microwavable wraps, pouches with handles, and carton board sandwich wedges. It launched the RotiBag in October 2024 and FiberCool curbside insulated bag in May 2025, addressing eco-friendly and e-commerce packaging needs. ProAmpac emphasizes recyclable solutions compatible with existing production lines, ensuring convenience, shelf-life extension, and sustainability for on-the-go food products.

DS Smith Plc Provides Sustainable Paper-Based Packaging Alternatives for Portability

DS Smith Plc excels in corrugated and collapsible packaging, offering paper-based alternatives to rigid containers. In 2024, the company achieved 2% like-for-like box volume growth and surpassed its goal to replace over one billion plastic packaging items by 2025. Following its acquisition by International Paper in April 2025, DS Smith continues to provide innovative, recyclable packaging for food service, e-commerce, and home delivery, supporting a circular economy and reduced environmental footprint.

On the go Packaging Market Share Insights

Beverages Dominate Market Share by Product Type in the On-the-Go Packaging Industry

Beverages account for the largest share at 35% of the on-the-go packaging industry in 2025, underscoring the centrality of hydration and convenience in consumer purchasing behavior. This segment is defined by a format battle between PET bottles, aluminum cans, and aseptic cartons, each chosen for its balance of cost, functionality, and sustainability. PET continues to dominate water and soft drink packaging due to its lightweight, shatter-resistant nature, but rapid growth in recycled aluminum cans highlights a premium and eco-conscious shift, especially in carbonated and energy drinks. Ready-to-Eat (RTE) meals and snacks capture 30% share, driven by urban consumers seeking portable, microwave-ready options with compartmentalized designs for freshness. Bakery and confectionery products hold 20%, where flexible films, recyclable PET packs, and molded fiber trays are steadily replacing non-recyclable clamshells to meet both sustainability demands and impulse-driven retail visibility. Fruits and vegetables, at 10%, emphasize freshness through PET clamshells and breathable films, with increasing experimentation in compostable trays and fiber-based packs to reduce plastic intensity. The remaining 5% “Others” category includes condiments and small-format nutritional pouches, illustrating how format diversification and sustainability mandates are reshaping even niche categories.

Retail Retains the Largest Market Share by End-User in the On-the-Go Packaging Industry

Retail dominates with 40% share in 2025, reflecting the significance of supermarkets and hypermarkets as the primary distribution channel for on-the-go packaged goods. Packaging formats here emphasize multi-packs, shelf optimization, and private-label differentiation, where recyclable PET, paperboard, and molded fiber designs enhance both cost efficiency and environmental performance. Convenience stores follow with 25% share, where packaging innovation is geared towards single-serve, impulse-driven formats that fit cup holders, support one-handed consumption, and capture consumer attention in chilled aisles. Food service providers hold 15% share, where quick-service restaurants and cafes are embracing a wholesale shift to compostable paper-based packaging for wraps, fries, and cups, using packaging as a visible sustainability statement. E-commerce, representing 12% share, is the fastest-growing end-user, requiring durable, right-sized packaging that balances shipping protection with material efficiency in subscription boxes and online grocery fulfillment. Vending, though smaller at 8%, demands uniform, durable, and tamper-proof packaging that ensures reliable dispensing and clear product visibility, with innovation increasingly tied to digital integration such as NFC tags for payment or promotions. The clear insight is that retail anchors demand at scale, while convenience and e-commerce channels shape the future of packaging innovation and sustainability adaptation.

United States: Eco-Friendly and Smart Packaging Innovations Drive On-the-Go Market Growth

The U.S. on-the-go packaging market is increasingly shaped by state-level regulations and sustainability initiatives. The U.S. Economic Development Administration (EDA) is supporting environmentally sustainable packaging with a $500,000 grant to the University of Wisconsin-Stevens Point, aimed at validating the recyclability and compostability of innovative packaging solutions.

Technological advancements are focused on smart and interactive packaging, incorporating QR codes, NFC, and RFID to provide consumers with real-time product freshness and nutritional information, while enhancing supply chain traceability. Government initiatives, combined with growing consumer demand for eco-friendly products, are pushing companies to adopt sustainable, lightweight, and tamper-evident packaging formats. The quick-service restaurant (QSR) and food delivery sectors are major drivers, with packaging designed to maintain food quality and withstand transport, particularly in the rapidly expanding online food delivery market.

Germany: Circular Economy and Biodegradable Innovations Lead Sustainable On-the-Go Packaging

Germany’s on-the-go packaging market operates under the EU Packaging and Packaging Waste Regulation (PPWR), which mandates that all packaging on the EU market be recyclable by 2030. Updated recyclability standards by ZSVR (Central Agency Packaging Register), effective January 2026, require companies to comply with practical, material-focused guidelines.

Technological innovation is centered on biodegradable films, recyclable paper-based solutions, and next-generation extrusion and pre-stretch systems for industrial and food applications. Germany’s robust recycling infrastructure and deposit-return system reinforce the adoption of eco-friendly packaging, especially for beverages. Key applications include energy drinks and soft drinks in cans, reflecting a consumer-driven “craze for cans” and emphasizing the demand for highly recyclable, convenient packaging.

China: Dual-Carbon Targets and E-Commerce Expansion Boost Sustainable Packaging Adoption

China’s on-the-go packaging industry is supported by governmental dual-carbon targets, aiming for carbon peaking by 2030 and carbon neutrality by 2060, which encourage eco-friendly materials and a circular economy. The State Council’s eco-friendly delivery regulations mandate retailers to provide in-store take-back facilities and publicly report packaging reduction metrics.

Technological advancements focus on automation, AI, and intelligent production systems to enhance efficiency and quality control, with companies like Amcor’s Huizhou facility exemplifying this trend. The market is fueled by the booming e-commerce sector and growing consumer goods market, with 175 billion parcel deliveries in 2024 driving demand for durable, automation-ready on-the-go packaging. Sustainability trends include a shift toward fiber-based packaging solutions and lightweight, high-performance containerboard with moisture-resistant coatings.

India: Government Programs and Circular Economy Initiatives Propel On-the-Go Packaging

India’s on-the-go packaging market benefits from Make in India and Production Linked Incentive (PLI) schemes, promoting domestic manufacturing and adoption of infinitely recyclable materials. Additional government initiatives are focused on supporting exporters with branding and packaging assistance, encouraging innovation in sustainable packaging.

Technological advancements include efficient GST-compliant packaging designs to minimize pre-printed material waste, while corporate initiatives like the Huhtamaki Foundation’s “CloseTheLoop” program set up recycling plants with a Rs. 10 crore (US$ 1.18 million) investment, reinforcing circular economy practices. Key applications cover juices, snacks, and ready-to-drink teas and coffees, where packaging is critical for brand presentation, product protection, and convenience, especially with the growth of online retail and quick-service restaurants.

Japan: Advanced Bio-Based Materials and Sustainability Drive High-Quality On-the-Go Packaging

Japan’s on-the-go packaging market is governed by food container regulations effective June 1, 2025, introducing a “positive list” for synthetic materials, which encourages the use of paper-based packaging with approved coatings and additives.

Technological advancements are focused on high-quality, functional, and eco-friendly packaging, including the use of bio-polypropylene (bio-PP). Collaborative initiatives by LyondellBasell, Futamura Chemical, and Iwatani have integrated bio-PP into packaging for the cosmetic and food sectors, reflecting a wider trend toward sustainability. Japan’s GHG reduction targets (46% by 2030, net-zero by 2050) will see approximately 2 million tonnes per year of bio-PP products by 2030, significantly influencing on-the-go plastic packaging. Key applications include ready-to-drink tea, coffee, and snack products, with demand for lightweight, durable, aesthetically pleasing, and sustainable packaging driven by a consumer preference for quality and convenience.

Brazil: Regulatory Reforms and Bio-Based Packaging Propel Functional Beverage Growth

Brazil’s on-the-go packaging market is impacted by Law No. 15,088 (January 2025), amending the National Solid Waste Policy to ban the import of solid waste and enforce recycling responsibilities on manufacturers, importers, and consumers. The government is also promoting bio-based packaging from corn starch, sugarcane bagasse, and cellulose sources.

Technological innovations include aluminum cans for water and beverages, led by Ambev, aligning with the circular economy goals. Key applications highlight the dominance of carbonated soft drinks, with the functional beverages segment emerging as the fastest-growing. This growth drives demand for innovative, convenient, and protective packaging to preserve product integrity, particularly in the on-the-go beverage sector.

On the go Packaging Market Report Scope

On the go Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Material (Plastic, Paper & Paperboard, Metal, Glass, Others), By Product Type (RTE Meals & Snacks, Beverages, Bakery & Confectionery, Fruits & Vegetables, Others), By Packaging Format (Flexible Packaging, Rigid Packaging, Vending & Dispensing), By End-User (Food Service, Retail, Convenience Stores, E-commerce, Vending)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., Huhtamaki Oyj, WestRock Company, Mondi Group, DS Smith Plc, Sonoco Products Company, Tetra Pak International S.A., Ball Corporation, Crown Holdings, Inc., International Paper Company, Graphic Packaging Holding Company, Rengo Co., Ltd., Sealed Air Corporation, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

On the go Packaging Market Segmentation

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Others

By Product Type

- RTE Meals & Snacks

- Beverages

- Bakery & Confectionery

- Fruits & Vegetables

- Others

By Packaging Format

- Flexible Packaging

- Rigid Packaging

- Vending & Dispensing

By End-User

- Food Service

- Retail

- Convenience Stores

- E-commerce

- Vending

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in On the go Packaging Market

- Amcor plc

- Berry Global Inc.

- Huhtamaki Oyj

- WestRock Company

- Mondi Group

- DS Smith Plc

- Sonoco Products Company

- Tetra Pak International S.A.

- Ball Corporation

- Crown Holdings, Inc.

- International Paper Company

- Graphic Packaging Holding Company

- Rengo Co., Ltd.

- Sealed Air Corporation

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-layered methodology to analyze the global on-the-go packaging market, integrating primary research, secondary data, and advanced analytical techniques. Primary research includes detailed interviews with packaging engineers, product developers, supply chain managers, sustainability experts, and key decision-makers across food, beverage, personal care, and health sectors. Secondary sources encompass corporate filings, patent databases, industry journals, regulatory guidelines, and trade publications. Market sizing and forecasts are derived from historical trends, adoption of convenience-oriented packaging formats, and shifts toward sustainable and reusable materials, including fiber-based, monomaterial, biodegradable, and bio-PP solutions. USDAnalytics evaluates technological innovations, such as smart packaging with QR codes, NFC, digital watermarks, and high-barrier films, assessing their impact on shelf-life extension, traceability, and consumer engagement. Regional regulatory frameworks—including EU Packaging and Packaging Waste Regulation (PPWR), U.S. state-level PFAS bans, Japan’s “positive list” for food container materials, and Brazil’s bio-based packaging policies—are incorporated into market projections. Competitive analysis focuses on strategic initiatives, mergers, product innovations, and sustainability programs by leading players such as Amcor plc, Huhtamaki Oyj, ProAmpac, DS Smith, Sealed Air, and Mondi Group, ensuring USDAnalytics provides actionable insights for manufacturers, retailers, and e-commerce and foodservice providers seeking efficiency, convenience, and environmental compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.