Healthcare Packaging Market Overview: Rising Demand for Sustainable and Safe Solutions

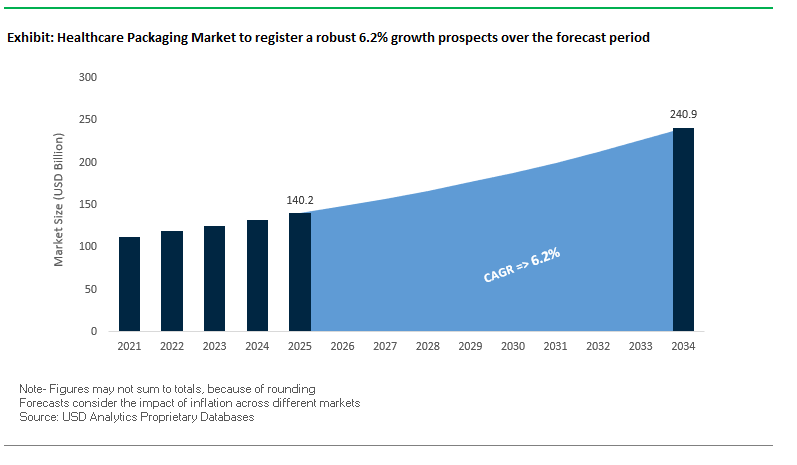

The Global Healthcare Packaging Market is valued at $140.2 billion in 2025 and is projected to reach $240.9 billion by 2034, growing at a steady CAGR of 6.2%. Demand is primarily driven by the pharmaceutical and biologics sectors, which require advanced packaging to preserve the efficacy of temperature-sensitive drugs, ensure sterility, and protect against contamination. The rapid rise of biologics and specialty drugs is further reinforcing the need for specialized, high-barrier packaging formats.

Plastics dominate the market due to their versatility in manufacturing blister packs, sterile barrier systems, and medical vials, while sustainability pressures are fueling investment in recycled plastics, bio-based polymers, and paper-based alternatives. Another major driver is adherence packaging, particularly child-resistant and senior-friendly formats, which are increasingly essential in addressing medication compliance amid the rising incidence of chronic diseases and aging populations.

Key Insights for Industry Professionals

- Pharmaceutical and biologics dominate global healthcare packaging demand, driven by strict safety and efficacy requirements.

- Plastics remain the most widely used material, but demand for PCR (post-consumer recycled), bio-based plastics, and paper is accelerating.

- Adherence packaging is becoming critical, as aging populations require senior-friendly and child-resistant solutions to improve medication compliance.

- Sustainability initiatives are reshaping portfolios, with companies setting measurable goals to transition toward circular packaging systems.

Market Analysis: Strategic Developments Shaping Healthcare Packaging

The healthcare packaging industry is undergoing rapid consolidation and innovation, with companies focusing on sustainability, biologics-friendly formats, and global capacity expansion. In August 2025, Currier Plastics Inc. appointed Rob Knapp as Business Development Manager to strengthen client relationships, while Nuoyuan Medical in China completed a Phase I clinical trial for a fluorescent imaging agent, signaling opportunities for packaging tailored to diagnostics and advanced drug delivery systems.

In July 2025, Amcor expanded its healthcare packaging footprint in Costa Rica, enhancing its presence in Latin America, while Aptar Pharma launched its first nasal pump with 52% bio-based material, underscoring the shift toward eco-friendly healthcare packaging. Around the same period, Neopac received global recognition with a WorldStar Award for its Polyfoil® Mono-Material Barrier Tube, designed for recyclability and high-barrier protection.

Earlier, in November 2024, Amcor acquired Berry Global in an $8.4 billion merger, creating one of the largest global players in healthcare packaging, with a broader portfolio across plastics and flexible solutions. Similarly, March 2025 saw Constantia Flexibles align with Aluflexpack AG to strengthen sustainability and innovation in premium pharmaceutical packaging. Strategic moves like Neopac’s Polyfoil® MMB mini tubes introduced in October 2024 for pharma and oral care, and Sonoco’s portfolio restructuring in April 2025, highlight how industry players are streamlining operations, scaling sustainable innovations, and targeting new geographies to meet growing healthcare needs.

Healthcare Packaging Market: Emerging Trends and Strategic Opportunities

Integration of Serialization and Aggregation for Enhanced Traceability

The healthcare packaging market is being reshaped by the mandatory integration of serialization and aggregation systems designed to strengthen global supply chain security. Regulatory frameworks such as the U.S. Drug Supply Chain Security Act (DSCSA) and the EU Falsified Medicines Directive (FMD) have established serialization as a baseline requirement, mandating unique product identifiers on every saleable unit. Aggregation linking units to cases and pallets provides the hierarchical visibility needed for authentication, inventory management, and rapid recalls. Industrial adoption is being driven not only by compliance deadlines but also by the growing threat of counterfeit drugs, which the World Health Organization (WHO) estimates affect up to 10% of medical products in low- and middle-income countries. By implementing end-to-end traceability, serialization ensures a verifiable chain of custody, enabling pharmacists, distributors, and regulators to instantly verify product authenticity. The Pharmaceutical Security Institute (PSI) continues to highlight the scale of counterfeit penetration in legitimate supply chains, further cementing serialization as an indispensable tool for healthcare packaging.

Adoption of Patient-Centric Smart Packaging for Adherence

A parallel trend in the healthcare packaging industry is the move toward patient-centric smart packaging designed to improve adherence and safety. The stakes are high: medication non-adherence is responsible for an estimated $100 billion in avoidable hospitalizations annually, according to AARDEX Group. Smart packaging integrates NFC, QR codes, or embedded sensors to passively monitor medication intake with accuracy levels reaching up to 97%, far surpassing patient self-reporting. In clinical trial contexts, where non-adherence rates can reach 40% after one year, connected packaging delivers time-stamped dosing data, providing researchers with objective insights that improve trial efficiency and reduce costs. Beyond digital innovations, patient-centric design extends to physical usability, with features such as child-resistant closures, senior-friendly opening mechanisms, calendar blister packs, multilingual instructions, and Braille labeling. These enhancements improve user safety and reduce dosing errors, particularly for aging populations and patients with complex medication regimens. Together, these advancements position smart, patient-centric packaging as a key driver of improved health outcomes and a competitive differentiator for pharmaceutical companies.

Development of High-Barrier Recyclable Polymers for Drugs

One of the most pressing opportunities lies in developing recyclable, high-barrier packaging solutions capable of protecting sensitive pharmaceuticals while aligning with global sustainability targets. Traditional multi-layer laminates, while highly effective against oxygen and moisture ingress, are incompatible with recycling streams due to their mixed-material composition. As regulators push for circular economy solutions, the industry is investing heavily in mono-polymer designs such as all-PE or all-PP structures equipped with advanced coatings that replicate the barrier performance of traditional laminates. Some companies are experimenting with recyclable fiber-based barrier papers and mono-material tubes featuring integrated EVOH layers, both of which provide enhanced protection without disrupting recyclability. However, achieving regulatory approval remains a major hurdle. Pharmaceutical packaging must meet ultra-stringent standards for safety, stability, and non-reactivity across the full product shelf life, making R&D timelines and certification costs substantial. Despite these challenges, the successful commercialization of high-barrier recyclable polymers would position manufacturers at the forefront of both compliance and sustainability innovation.

Expansion of Connected Packaging for Clinical Trials and Real-World Data

A second transformative opportunity is the expansion of connected packaging solutions to capture real-world data (RWD) and generate real-world evidence (RWE), both of which are increasingly recognized by regulators such as the FDA as valuable tools for decision-making. By embedding technologies such as NFC or Bluetooth, connected packaging can track adherence in real-time, capturing granular insights into patient behavior including missed doses, timing intervals, and persistence with long-term therapies. This data is invaluable for clinical trial optimization, providing pharmaceutical sponsors with actionable insights to improve trial design, reduce dropout rates, and enhance safety monitoring. Beyond the trial environment, connected packaging can support new patient engagement models, including personalized adherence support programs, reminders, or digital health platforms that provide patients with feedback and encouragement. This integration of packaging and data analytics not only strengthens clinical outcomes but also creates new business models where packaging becomes a service platform, offering opportunities for differentiation, brand loyalty, and patient-centered healthcare delivery.

Competitive Landscape: Leading Companies in Global Healthcare Packaging Industry

The global healthcare packaging market is highly competitive, led by companies advancing sustainable innovation, global expansion, and adherence-focused solutions.

Amcor plc: Expanding Healthcare Leadership through Berry Acquisition

Amcor is a global leader in flexible and rigid healthcare packaging, offering sterile pouches, barrier films, and trays. With the late 2024–early 2025 acquisition of Berry Global, Amcor consolidated its position in healthcare and consumer packaging. Its AmPrima™ Recycle Ready Solutions enable recyclability without performance compromise, aligning with its goal of 100% recyclable or reusable packaging by 2025.

Gerresheimer AG: Investing in High-Quality Glass and Plastic Primary Packaging

Gerresheimer specializes in pre-fillable syringes, vials, ampoules, and cartridges. In late 2024, it invested €100 million in a new facility in Querétaro, Mexico, strengthening its North American supply capacity. With a commitment to 50% CO2 reduction by 2030, Gerresheimer leverages expertise in glass and polymer packaging to meet the strictest regulatory and hygiene standards.

AptarGroup, Inc.: Driving Innovation in Drug Delivery Systems

AptarGroup is a leader in dispensing and drug delivery packaging. In July 2025, it launched its metal-free APF Futurity™ nasal spray pump, a recyclable innovation with Class A.A. certification. Aptar’s focus on adherence solutions such as Advaspray® and HeroTracker® Sense underlines its mission to improve patient outcomes while advancing sustainable, patient-friendly drug delivery packaging.

Sonoco Products Company: Strengthening Cold Chain Packaging Leadership

Sonoco, through its ThermoSafe division, is a leader in temperature-assured packaging for pharmaceuticals, vaccines, and biologics. Its ISC Labs® provide regulatory testing and qualification for custom cold chain solutions. In April 2025, Sonoco divested its flexibles business to TOPPAN Holdings to streamline its focus, reinforcing its position as a specialist in cold chain healthcare logistics.

Constantia Flexibles Group GmbH: Leading in High-Barrier Sustainable Packaging

Constantia Flexibles serves the pharmaceutical industry with labels, foils, and blister pack laminates. In 2025, it won two WorldStar Global Packaging Awards for EcoPeelCover and EcoLamHighPlus, both designed to enhance recyclability while maintaining high-barrier performance. Its global Centers of Competence ensure consistent innovation and compliance, making it a leader in sustainable pharmaceutical packaging solutions.

Healthcare Packaging Market Share Insights

Blister Packs Hold the Largest Market Share by Product Type in the Healthcare Packaging Industry

Blister packs account for 25% of the healthcare packaging market, underscoring their unique ability to balance product protection with patient compliance. Their strength lies in providing tamper evidence, unit-dose accuracy, and extended shelf life through high-barrier films that protect against oxygen and moisture ingress. Beyond containment, blister packs are increasingly integrated with compliance aids, such as calendar layouts, and digital features like NFC-enabled authentication for anti-counterfeiting. With rising chronic disease prevalence and an aging population, the format’s role in ensuring correct dosage and reducing medication errors positions blister packaging as the most critical enabler of patient safety and adherence in healthcare delivery.

Pharmaceutical Manufacturing Drives Market Share by End-Use Industry in Healthcare Packaging

Pharmaceutical manufacturing represents 50% of healthcare packaging demand, cementing its role as the industry’s regulated core. Unlike consumer-driven markets, this segment is dictated by stringent compliance and stability requirements, with every packaging format from vials and ampoules to pre-filled syringes considered part of the drug delivery system itself. Serialization mandates under frameworks such as the EU Falsified Medicines Directive (FMD) and the U.S. DSCSA mean that packaging carries equal regulatory weight to the drug product, with anti-counterfeiting, tamper evidence, and global traceability systems now baseline requirements. As biologics, injectables, and personalized medicines expand, pharmaceutical manufacturers are increasingly demanding pre-sterilized, ready-to-use formats and packaging innovations that reduce contamination risks while improving patient outcomes.

United States: Smart and Sustainable Healthcare Packaging Driving Innovation

The U.S. healthcare packaging market is witnessing strong growth due to increasing consumer demand for sustainable packaging, particularly for OTC medications and nutraceuticals. Rising awareness of environmental impacts is prompting companies to adopt recyclable and compostable packaging solutions. Technological advancements, including smart packaging and serialization technologies, are accelerating adoption, especially as the U.S. Drug Supply Chain Security Act (DSCSA) mandates track-and-trace systems to prevent counterfeiting and ensure patient safety.

Government support through initiatives like the Department of Energy’s $52 million funding for cellulose-based films is reinforcing the shift toward eco-friendly healthcare packaging materials. Key applications include biologics, home-care, and personalized medicine, where the trend toward home-based treatments for chronic diseases is driving demand for user-friendly and portable packaging. Corporate initiatives by companies such as Amcor, introducing solutions like AmLite Ultra Recyclable high-barrier films, are significantly reducing carbon footprints while maintaining product integrity and compliance. Additionally, state-level Extended Producer Responsibility (EPR) regulations are encouraging companies to rethink their supply chains and integrate end-of-life management for packaging materials.

Germany: Circular Economy and Regulatory Compliance Shaping Healthcare Packaging

Germany’s healthcare packaging market is strongly influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR 2025), driving demand for eco-friendly and recyclable packaging. The country’s commitment to a circular economy is fueling innovation in materials, with a focus on mono-material films such as polyethylene (PE) and polypropylene (PP) to enhance recyclability.

Technological innovation is accelerating the adoption of oxygen-barrier labels that integrate unique device identification (UDI), ensuring drug stability and compliance with EU MDR regulations. Governmental mandates like the PPWR, combined with updates favoring fiber-based packaging over plastics, are reshaping pharmaceutical packaging, particularly in the high-value medical segment. German converters are also exploring automation and smart-labeling technologies to optimize efficiency and sustainability across healthcare packaging supply chains.

China: Government Policies and Automation Propel Sustainable Healthcare Packaging

China’s healthcare packaging industry is being driven by the government’s dual carbon targets, which promote the adoption of eco-friendly and reusable materials. Manufacturers are increasingly investing in automation and AI technologies, integrating 5G plus industrial internet solutions to optimize production efficiency and enhance flexible manufacturing capacity.

Sustainability measures, such as restrictions on non-degradable plastics in express delivery by 2025, are spurring demand for paper-based and sustainable packaging alternatives. The growth of domestic e-commerce platforms is driving demand for secure and tamper-proof packaging, particularly for OTC medical supplies and devices. Additionally, regulatory reforms introduced in July 2025, including fast-tracking standards for high-end medical devices such as AI-enabled devices and medical robots, are reinforcing innovation and quality requirements in healthcare packaging.

India: Smart Labels and Eco-Friendly Packaging Transform Healthcare Packaging

India’s healthcare packaging market is benefiting from Make in India and Zero Effect Zero Defect initiatives, which support quality domestic production and sustainable packaging solutions. Government incentives like the Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, are enhancing manufacturing capabilities and standardization, driving demand for high-quality healthcare packaging.

The industry is responding to rising consumer awareness and regulatory support by adopting eco-friendly alternatives, in line with the Plastic Waste Management (Amendment) Rules and Food Safety and Standards (Packaging and Labelling) Regulations. Investments in smart labeling technologies, including RFID-enabled and high-speed color inkjet printers, are increasing, allowing companies to enhance traceability, anti-counterfeiting measures, and product compliance. Corporations like Epson India are pioneering these innovations to serve pharmaceuticals and industrial healthcare segments, ensuring both efficiency and sustainability in packaging solutions.

Healthcare Packaging Market Report Scope

Healthcare Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$140.2 Billion

|

|

Market Size (2034)

|

$240.9 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Material Type (Plastics, Paper & Paperboard, Glass, Metal & Foils, Bioplastics), By Product Type (Blister Packs, Bottles & Containers, Vials & Ampoules, Pouches & Bags, Pre-Filled Syringes, Medication Tubes, Labels & Closures), By Packaging Format (Primary Packaging, Secondary Packaging, Tertiary Packaging), By End-Use Industry (Pharmaceutical Manufacturing, Medical Device OEMs, Nutraceuticals & OTC, Home-Healthcare Providers, Contract Packaging Organizations)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Berry Global Inc., WestRock Company, Gerresheimer AG, Mondi Group, AptarGroup, Inc., Sonoco Products Company, Huhtamaki Oyj, CCL Industries Inc., West Pharmaceutical Services, Inc., SGD Pharma, Origin Pharma Packaging, Becton Dickinson and Company, Constantia Flexibles, Unither Pharmaceuticals SAS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Healthcare Packaging Market Segmentation

By Material Type

- Plastics

- Paper & Paperboard

- Glass

- Metal & Foils

- Bioplastics

By Product Type

- Blister Packs

- Bottles & Containers

- Vials & Ampoules

- Pouches & Bags

- Pre-Filled Syringes

- Medication Tubes

- Labels & Closures

By Packaging Format

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

By End-Use Industry

- Pharmaceutical Manufacturing

- Medical Device OEMs

- Nutraceuticals & OTC

- Home-Healthcare Providers

- Contract Packaging Organizations

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Healthcare Packaging Market

- Amcor plc

- Berry Global Inc.

- WestRock Company

- Gerresheimer AG

- Mondi Group

- AptarGroup, Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- CCL Industries Inc.

- West Pharmaceutical Services, Inc.

- SGD Pharma

- Origin Pharma Packaging

- Becton Dickinson and Company

- Constantia Flexibles

- Unither Pharmaceuticals SAS

* List Not Exhaustive

Methodology

USDAnalytics has employed a comprehensive, multi-layered research methodology to provide an authoritative analysis of the global Healthcare Packaging Market. Our approach combines extensive primary research, including interviews with pharmaceutical manufacturers, medical device OEMs, contract packaging organizations, and sustainability experts, alongside secondary research sourced from company filings, press releases, regulatory frameworks, trade publications, and industry events. Market sizing, CAGR projections, and forecast modeling are derived from historical demand trends, emerging regulations such as serialization mandates under the U.S. DSCSA and EU Falsified Medicines Directive, and innovations in high-barrier recyclable polymers, bio-based materials, and smart, patient-centric packaging solutions. Segmentation analysis spans material type, product type, packaging format, and end-use industry, while qualitative insights highlight strategic developments including mergers and acquisitions, global expansion, and sustainability-driven innovation. This methodology ensures USDAnalytics delivers actionable, data-driven insights for industry professionals, equipping stakeholders with a robust understanding of market dynamics, growth drivers, competitive landscapes, and emerging trends shaping healthcare packaging worldwide.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.