Market Overview: Thermal Protection and Sustainability Drive Demand

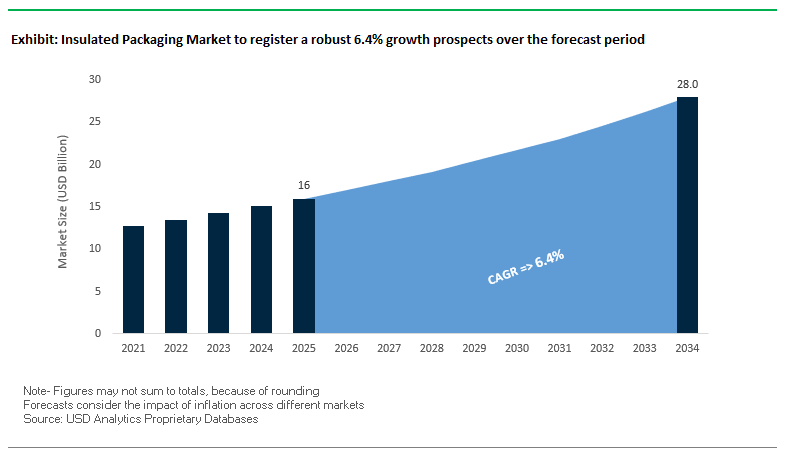

The Insulated Packaging Market is valued at USD 16.0 billion in 2025 and projected to reach USD 28.0 billion by 2034, expanding at a CAGR of 6.4%. This sector plays a pivotal role in maintaining the integrity of temperature-sensitive products across food, pharmaceuticals, and industrial goods. For buyers and industry professionals, the key question is how insulated packaging will adapt to rising e-commerce demand, regulatory compliance, and sustainability pressures.

Key Insights for Industry Professionals:

- Growth vector: USD 16B (2025) → USD 28B (2034) at 6.4% CAGR, driven by pharma logistics, food delivery, and sustainable packaging mandates.

- E-commerce driver: Rapid expansion of home delivery for meal kits, groceries, and perishables requires cost-efficient, lightweight, and validated insulated solutions.

- Sustainability shift: Transition away from EPS foam to paper-based liners, biodegradable foams, and reusable shippers that align with ESG goals.

- Cold chain importance: Rising global transport of biologics, vaccines, and temperature-sensitive pharma fuels demand for validated, regulatory-compliant insulated systems.

- Smart integration: Adoption of temperature sensors, RFID, and real-time data loggers ensures traceability and reduces product loss.

Market Analysis: Recent Developments Emphasize Sustainability and Innovation

The insulated packaging industry is undergoing a period of transformation, marked by strategic investments and technological shifts. In August 2025, DNP introduced mono-material recyclable sterilization pouches and blister packs at Medical Fair Thailand, targeting the medical and pharmaceutical sectors with sustainable alternatives. Also in July 2025, the Amcor–Berry Global merger officially closed, creating a packaging powerhouse with expanded capabilities across rigid and flexible insulated formats.

Parallel to consolidation, smart packaging integration is accelerating. A July 2025 report confirmed rising adoption of QR codes, NFC, and RFID tracking in insulated packaging to enhance shipment traceability. Earlier in February 2025, Amcor launched its AmFiber Performance Paper stand-up pouch, reducing carbon footprints by 73% compared to traditional packs, showing a clear pivot toward recyclable, paper-based insulated formats.

Sustainability startups are also driving innovation. In April 2025, Finland-based Fiberwood secured USD 8.73 million to scale sustainable insulation materials that double as building and packaging solutions. ProAmpac followed in December 2024 with FiberCool, a curbside-recyclable insulated bag designed to minimize material waste while improving thermal performance. Meanwhile, in October 2024, Pelican BioThermal launched the Crēdo Vault™ for bulk pharma shipments, emphasizing validated cold chain control with lighter materials.

Key Trends and Emerging Opportunities in the Insulated Packaging Market

Strategic Shift Towards Fiber-Based Recyclable Insulation Materials

The insulated packaging market is experiencing a major transformation as leading e-commerce and logistics companies transition from polymer-based foams such as EPS to recyclable fiber-based insulation. This shift is largely driven by stringent ESG mandates, regulatory pressures on plastic waste, and corporate sustainability goals.

Major logistics players like FedEx have committed to achieving carbon-neutral operations by 2040, with packaging innovation as a core component. Similarly, UPS, through its Eco Responsible Packaging Program, actively encourages businesses to adopt recyclable and reusable materials with high recycled content, signaling a strong industry preference for sustainable solutions.

Material innovation is advancing rapidly. Cold Chain Technologies launched the CCT TRUEtemp® Naturals shipper, a curbside-recyclable, paper-based solution offering 48 hours of thermal protection for 2°C–8°C products. Mondi’s Snug&Strong corrugated solution provides a 100% paper-based alternative for electronics and white goods, delivering a flat-packed, recyclable, and space-efficient insulation solution. These initiatives showcase how fiber-based materials are replacing EPS in multiple packaging applications, aligning with circular economy principles.

Proliferation of Parcel-Level Real-Time Temperature Monitoring

With the growth of high-value pharmaceuticals, premium meal kits, and specialty foods, there is a rising need for IoT-enabled parcel-level monitoring to ensure a verifiable chain-of-custody and product integrity.

In the pharmaceutical sector, partnerships such as Cold Chain Technologies and Cellbox Solutions focus on maintaining precise temperature ranges for sensitive materials like live cells, reflecting demand for specialized cold-chain solutions. For consumer-facing applications, companies like TempAid integrate single-use temperature data loggers to verify perishable goods remained within required temperature limits.

Telenor IoT emphasizes that continuous temperature and humidity monitoring enhances transparency, reduces spoilage, and builds consumer trust, providing a competitive advantage in the high-value insulated packaging sector. This trend highlights the convergence of digital monitoring, IoT integration, and sustainable insulated packaging to support premium logistics solutions.

Development of High-Performance Bio-Based Insulation Foams

There is a significant opportunity for the R&D and commercialization of bio-based insulation materials derived from organic sources such as seaweed, mycelium, and agricultural waste, offering home compostability without compromising thermal performance.

Startups like Cruz Foam utilize agricultural waste like chitin to create bio-based EPS and EPE alternatives, reducing reliance on fossil-fuel-based plastics while valorizing byproducts. Academic studies confirm that these materials exhibit thermal conductivity comparable to traditional foams, establishing a scientific basis for their adoption.

Partnerships between brands and material innovators align with sustainability goals, helping companies meet consumer demand for eco-friendly solutions. Regulatory frameworks, including the EU Packaging and Packaging Waste Regulation (PPWR), provide incentives for bio-based materials, creating a favorable environment for commercial deployment of high-performance, compostable insulation foams.

Standardization of Reusable Container Pools for Urban Logistics

The economic and environmental pressures of urban last-mile delivery are creating opportunities for standardized, durable, and reusable insulated containers, managed through shared pooling systems.

Companies like OLIVO Logistics are investing in expanded polypropylene (EPP) reusable totes, reducing waste and operational costs. Collaborative pooling systems, exemplified by IFCO’s SmartCycle program, demonstrate how shared logistics infrastructure can maximize reuse while minimizing environmental impact. Startups such as BOXO further enhance scalability by providing reusable shipping bags for e-commerce, leveraging robotics to sort and clean materials efficiently.

Competitive Landscape: Key Players Reshaping Global Insulated Packaging

The insulated packaging market is shaped by global leaders blending materials expertise, cold chain validation, and sustainable product innovation to meet rising demand across healthcare, food, and industrial sectors.

Sonoco Products Company: Refining portfolio for sustainable growth

Sonoco has a strong foothold in protective and temperature-controlled packaging. In January 2024, it sold its Protective Solutions business to streamline operations and focus on core insulated packaging segments. Its offerings include insulated shippers, thermal containers, and cleanroom-certified medical packaging. Sonoco’s strategy emphasizes sustainable innovation and portfolio optimization, targeting healthcare and industrial customers seeking reliable thermal assurance.

Pelican BioThermal: Leadership in reusable pharma cold chain solutions

Pelican BioThermal, a subsidiary of Pelican Products, dominates reusable pharma shippers. In October 2024, it introduced the Crēdo Vault™, designed for bulk pharmaceutical shipments requiring validated, extended cold chain performance. With solutions like Crēdo™ reusable containers and CoolGuard™ insulated shippers, the company ensures compliance with stringent pharma regulations. Its focus remains on reducing emissions, reusability, and durable cold chain logistics.

Sealed Air Corporation: Advanced insulation for perishable goods

Sealed Air leverages its expertise in protective and food packaging to develop innovative insulation materials. In May 2024, it launched Cryovac ICETech, a sustainable insulation designed to cut waste and lower emissions. Its portfolio includes Instapak® foam systems and TempGuard® insulated bags, delivering up to 72 hours of temperature protection for perishables and e-commerce shipments. Sealed Air’s strategy is to secure global food supply chains through sustainable, efficient insulated solutions.

TemperPack Technologies, Inc.: Pioneer in curbside-recyclable insulated liners

TemperPack has positioned itself as a disruptor in EPS replacement. Following its September 2022 acquisition of KTM Industries, maker of Green Cell Foam, it expanded its sustainable portfolio. Products like ClimaCell™ and WaveKraft™ are paper-based insulated liners, certified for curbside recycling. TemperPack’s mission is clear: eliminate Styrofoam from e-commerce and pharma cold chain, aligning with consumer and regulatory pressure for eco-friendly alternatives.

Insulated Packaging Market Share Insights

Boxes & Containers Dominate Market Share by Packaging Type in Insulated Packaging

Boxes and containers account for 45% of the insulated packaging market in 2025, establishing themselves as the most versatile and widely adopted format. Their leadership is attributed to their ability to deliver turnkey thermal protection for single shipments across food, beverage, and pharmaceutical supply chains. Incorporating materials like expanded polystyrene (EPS), polyurethane (PU) foam, or increasingly recycled fiberboard, these solutions combine durability, thermal performance, and ease of use, making them indispensable for meal kits, direct-to-consumer groceries, and last-mile pharma logistics. Pallet shippers and covers, while lower in overall volume, are critical in bulk pharmaceutical and biologics transportation, where strict cold-chain compliance is non-negotiable. Bags, pouches, and liners, on the other hand, are gaining traction as flexible, lightweight alternatives that lower freight costs and optimize storage space, particularly for e-commerce grocery and subscription-based meal delivery services. This segmentation illustrates how rigid boxes anchor the market through reliability, while flexible formats expand share through cost and logistics advantages.

Food & Beverages Lead Market Share by Application in Insulated Packaging

The food and beverages sector holds 50% of the insulated packaging market share in 2025, making it the largest and most influential application segment. The surging adoption of online grocery shopping, ready-to-eat meal kits, and specialty perishable shipping has created unprecedented demand for insulated liners and containers that maintain freshness and prevent spoilage during transit. This segment is highly volume-driven and directly tied to evolving consumer lifestyles that prioritize convenience and food safety. Pharmaceuticals & healthcare, while slightly smaller in scale, represent a high-value, risk-sensitive application where failure in temperature control can lead to catastrophic financial and patient safety outcomes. As a result, pharmaceutical shipments often rely on premium pallet shippers, validated insulated boxes, and advanced phase-change materials to ensure compliance with strict 2–8°C or -20°C protocols. Chemicals and cosmetics, though niche, demonstrate the market’s diversification, where insulated formats protect high-purity reagents, natural oils, and active ingredients from degradation. Together, these segments show how food secures bulk demand, while pharmaceuticals sustain high-margin growth in insulated packaging.

United States Insulated Packaging Market Strengthened by EPR Regulations and Smart Cold Chain Solutions

The U.S. insulated packaging market is heavily influenced by state-level Extended Producer Responsibility (EPR) regulations, notably California’s SB-54, which mandates a 25% reduction in plastic usage by 2032. This regulatory framework encourages a shift toward sustainable materials like paper, cardboard, and other recyclable substrates. Additionally, the Drug Supply Chain Security Act (DSCSA) drives the adoption of smart packaging solutions with real-time tracking, particularly for pharmaceutical cold chain applications.

Technological innovations are transforming the market, including reusable bulk insulated containers for dry ice and perishable goods, as launched by Sonoco ThermoSafe in August 2025. IoT-enabled smart packaging solutions for temperature monitoring are also gaining traction to ensure product safety during transport. Corporate investments focus on expanding production for sustainable and specialized cold chain packaging, with companies like Sonoco ThermoSafe and Cold Chain Technologies leading the way. Strong demand persists in the e-commerce, food delivery, and pharmaceutical sectors, driven by the “Amazon Effect” and the need for temperature-controlled transport for mRNA vaccines and high-value biologics. Sustainability remains a key priority, with recyclable paper-based insulation and non-toxic gel packs becoming standard.

Germany Insulated Packaging Market Advancing Through Circular Economy and Alu-Free Innovations

Germany’s insulated packaging industry operates under the stringent EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates full recyclability or reusability of packaging by 2030. The country’s Single-Use Plastics levy further encourages businesses to adopt reusable or recyclable insulated containers, making sustainability a primary driver of innovation.

Technological advancements focus on high-performance, environmentally friendly solutions such as aluminum-layer-free aseptic cartons, pioneered by Hochwald and SIG. These innovations maintain thermal insulation while significantly reducing carbon footprint. Germany’s Packaging Act (VerpackG) incentivizes recyclable design through modulated fees, promoting reusable insulated containers over single-use options. Corporate investments in SIG Terra aluminum-free materials exemplify Germany’s commitment to sustainable, high-quality insulated packaging for liquid and perishable goods.

China Insulated Packaging Market Gaining Momentum Through Green Initiatives and Domestic Manufacturing

China’s insulated packaging market is propelled by the government’s “dual carbon” goals and the March 2024 Action Plan for Large-Scale Equipment Updates, which promote the use of sustainable materials and recycling across the cold chain sector. Regulatory reforms, including the GB/T 31268 standard restricting excessive packaging, directly impact e-commerce and retail packaging practices.

Technological innovation is driving efficiency with AI, automation, and “5G plus industrial internet” integration. The focus on domestic manufacturing supports local capacity expansion, meeting the increasing demand for high-performance, circular insulated packaging solutions. Companies are investing in advanced insulation materials and manufacturing technologies to serve the growing needs of food, e-commerce, and pharmaceutical cold chains.

India Insulated Packaging Market Expanding Through Circular Economy Incentives and Advanced Cold Chain Solutions

India’s insulated packaging market is benefiting from government initiatives promoting a circular economy. In September 2025, the GST on paper sacks and biodegradable bags was reduced to 5%, encouraging sustainable packaging adoption. Regulatory support combined with the ban on single-use plastics is driving demand for reusable insulated solutions.

Technological advancements include automated production lines and the development of materials derived from agricultural waste. Companies like Archian Foods Pvt. are adopting chill boxes for rural food distribution, while Tetra Pak introduced certified recycled polymer packaging in February 2025. Expanding food processing and pharmaceutical sectors are fueling demand for high-performance, internationally compliant insulated packaging solutions.

Japan Insulated Packaging Market Leveraging Precision Manufacturing and Specialty Thermal Solutions

Japan’s insulated packaging industry is a key component of its next-generation production ecosystem. Innovations in vacuum-insulated panels (VIPs) and paper-based thermal wraps provide performance and sustainability advantages, increasingly adopted across Asia and Europe.

The Plastic Resource Circulation Act (April 2022) guides manufacturers toward environmentally responsible designs, reducing single-use plastics. Japanese companies focus on high-performance, specialty insulated packaging, including self-sealing and superior barrier solutions, to meet the needs of diverse industries ranging from pharmaceuticals to food logistics. Functional innovation and premium aesthetics are central to product differentiation in this market.

Brazil Insulated Packaging Market Driven by Sustainable Policies and Logistics Innovation

Brazil’s insulated packaging market is shaped by sustainable waste management policies under the National Solid Waste Policy, updated in April 2022. Government initiatives aim to modernize solid waste management and promote eco-friendly packaging solutions.

Technological advancements include shuttle systems combining frozen, chilled, and ambient items to optimize last-mile delivery for food and beverages. Key applications are in frozen foods, fresh produce, and ready-to-eat meals, where temperature control is critical. Corporate investments, such as Klabin’s BRL 188 million expansion of sustainable corrugated board production, reinforce the adoption of insulated packaging solutions across the cold chain and logistics sectors.

Insulated Packaging Market Report Scope

Insulated Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16 Billion

|

|

Market Size (2034)

|

$28 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Material (EPS, PUR, PP, Paper & Paperboard, Others), By Packaging Type (Boxes & Containers, Pallet Shippers & Covers, Bags & Pouches, Liners), By Application (Food & Beverages, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Chemicals), By End-Use (Industrial, Commercial, Household)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Sonoco Products Company, Cold Chain Technologies, Inc., Amcor plc, DS Smith Plc, Cool Logistics Group, Mondi Group, Insulated Products Corporation (IPC), Cryopak Industries Inc., Pelican Products, Inc., Sofrigam Group, Exeltainer, Placon Corporation, Marko Foam Products Inc., Thermal Packaging Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Insulated Packaging Market Segmentation

By Material

- EPS

- PUR

- PP

- Paper & Paperboard

- Others

By Packaging Type

- Boxes & Containers

- Pallet Shippers & Covers

- Bags & Pouches

- Liners

By Application

- Food & Beverages

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Chemicals

By End-Use

- Industrial

- Commercial

- Household

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Insulated Packaging Market

- Sealed Air Corporation

- Sonoco Products Company

- Cold Chain Technologies, Inc.

- Amcor plc

- DS Smith Plc

- Cool Logistics Group

- Mondi Group

- Insulated Products Corporation (IPC)

- Cryopak Industries Inc.

- Pelican Products, Inc.

- Sofrigam Group

- Exeltainer

- Placon Corporation

- Marko Foam Products Inc.

- Thermal Packaging Solutions

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-faceted research methodology to evaluate the Insulated Packaging Market, combining primary interviews with packaging engineers, logistics specialists, foodservice operators, and pharmaceutical cold chain experts alongside secondary research from company reports, regulatory filings, trade journals, and verified industry databases. Market sizing, CAGR projections, and forecasts were developed using a combination of bottom-up and top-down approaches, validated against historical trends, material consumption data, and product adoption across key geographies. The analysis incorporates innovations in EPS, PUR, polypropylene, paper-based insulation, and bio-based foams, alongside advancements in IoT-enabled temperature monitoring, RFID integration, and smart packaging systems. Sustainability trends, ESG-driven initiatives, and regulatory frameworks such as Extended Producer Responsibility (EPR), the EU Packaging and Packaging Waste Regulation (PPWR), and single-use plastic bans were factored into growth projections. Regional dynamics across North America, Europe, Asia-Pacific, India, and Latin America were analyzed, alongside competitive strategies of market leaders including Sonoco, Pelican BioThermal, Sealed Air, TemperPack, and Amcor, highlighting innovations in reusable, recyclable, and high-performance insulated solutions for food, pharmaceuticals, and industrial applications.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.